We live in a world where decentralized finance (“defi”) market structures and trade executions are constantly changing, and most people know very little about them. Amid this complexity, it’s easy to forget that the market structure for defi today is very different from the current state of traditional finance (“tradfi”). From its permissionless, global, decentralized origins, DeFi has been well on its way to addressing some of the criticisms leveled at tradfi execution by market participants and regulators.

In this article, we will focus on the state of DeFi order and transaction flow today. We will show how DeFi differs from traditional order flow markets and discuss the challenges of realizing our shared dream of a system that maximizes user benefit while remaining decentralized.

We believe that the SEC, Citadel, and Flashbots (as well as many other agencies) have been fully aligned from the beginning in identifying market failures and desired market outcomes. We will outline some of the issues tradfi market participants themselves have identified in the payments for order flow (“PFOF”) landscape and argue that defi has the opportunity to directly address these market failures.

We will show that Ethereum’s order flow landscape represents a nascent and fragile opportunity, demonstrating a decentralized version of a robust order flow processing network using centralized infrastructure. We believe that a permissionless searcher network and liquidity provision can create competitive order execution, moving away from tradfi's reliance on a small number of established market makers. We believe what is needed for DeFi to truly realize its vision and promise is to maintain the existing decentralization of this market while increasing competition and the ability to decentralize infrastructure at every layer of the stack.

In the process, cryptocurrencies attempt to take a step toward the fundamental elements of a fair, robust, antifragile, and decentralized financial system.

SEC Proposes Rule 615: A Fascinating Prelude to Defi

To understand the history of order flow and execution, it is critical to understand the mature U.S. stock market structure. Tradfi’s market structure begins with market makers’ preference to trade with “retail investors” due to lower adverse selection risk, meaning there is a lower likelihood that the stock price will move against the market maker as a result of order execution. Today, more than 90% of retail orders are sent directly to six wholesale market makers rather than to Ignite’s public exchanges. This practice, widely known as Pay for Order Flow (PFOF), is where market makers are paid to trade based on retail order flow and, in return, provide users with commission-free trades.

The quality of user trade execution in PFOF is maintained through two main practices:

- Price improvements: Market makers must fill user orders at a price that is at least better than the National Best Bid and Offer (NBBO), which is the highest bid price across all exchanges and lowest selling price

- Fair competition: Order flow is allocated to market makers in batches based on execution quality indicators such as total price improvement in the previous period, and a unified PFOF rate is charged to all participating market makers.

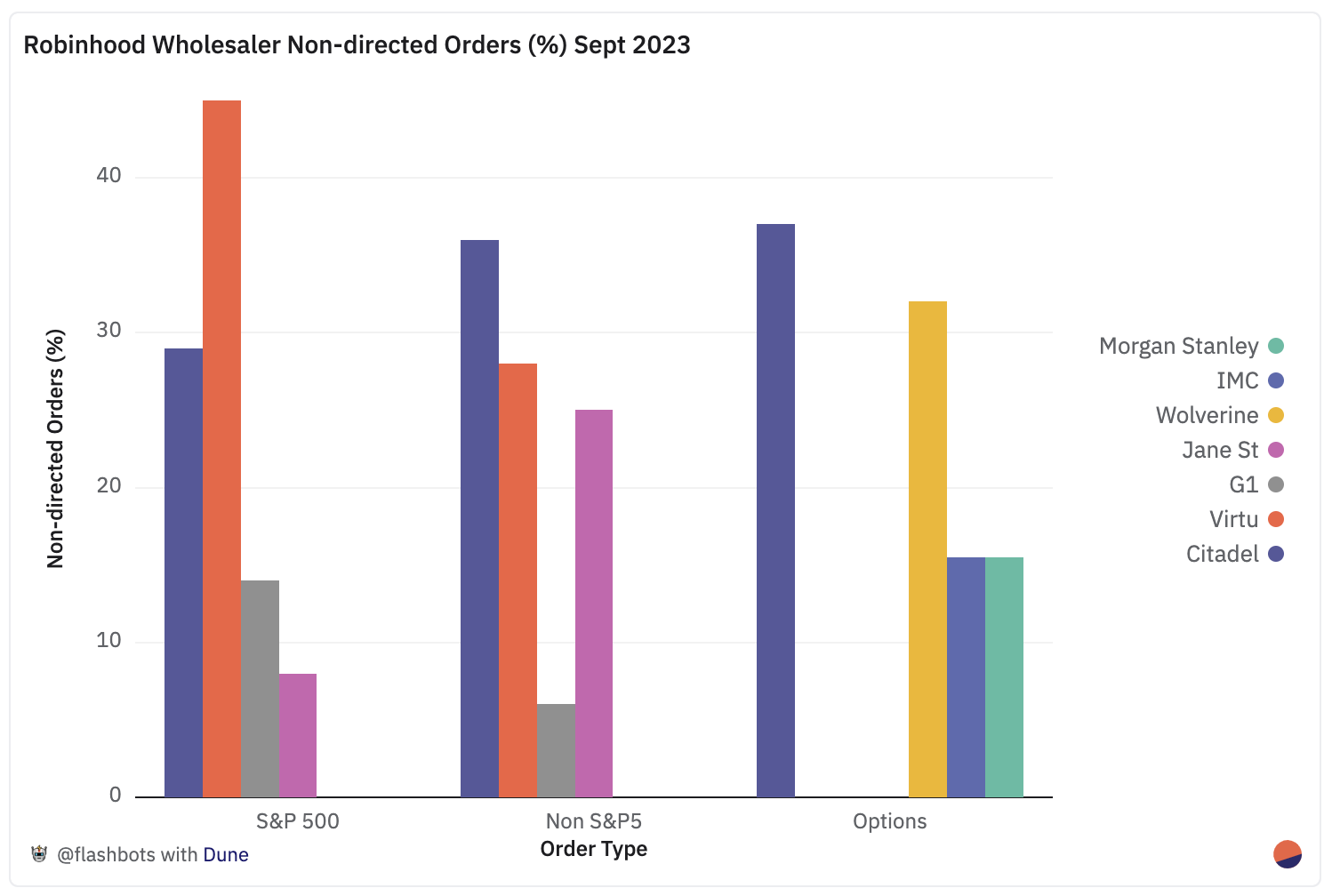

Robinhood is one of the largest and most prominent brokers using PFOF to monetize retail order flow. In August 2023, Robinhood users traded $59.8B in stocks, $107.3M in options, and $2.2B in cryptocurrencies . Robinhood made $1.1 million from PFOF from S&P 500 stocks, $9 million from non-S&P 500 stocks, and $43.4 million from options trades .

Source: Robinhood Q3 2023 Rule 606 Report.

Figure 1. Percentage of non-directed orders received by each wholesaler on Robinhood. Orders are broken down by S&P 500 stocks, non-S&P 500 stocks and options.

Figure 1 shows that there are up to four wholesale market makers per order type on Robinhood. Of the four market makers, Citadel fills 29% of S&P 500 orders, 36% of non-S&P orders and 37% of options orders. Virtu executes 45% of S&P 500 orders and 28% of non-S&P orders.

The market structure that resulted in retail users trading with Citadel and Virtu did not appear to be good for users, nor did the SEC. The SEC lists two main criticisms of the PFOF market structure:

- Order flow segmentation: The segmentation of retail flow from active exchanges to market makers benefits market makers and taxes other market participants. As the likelihood of adverse selection increases, market makers begin to expand their quotes on exchanges with lower trading volumes, resulting in poorer execution quality for traders such as institutional investors on these exchanges.

- Misaligned incentives for price increases in a single order: Since the order flow is allocated to market makers in batches and is only evaluated based on the total price increase, the market maker has the right to decide whether to give the user a better price or to give the user a better price when a single order is executed. Keep the profits for yourself. When execution exploits competition only through indirect means, the surplus flows to wholesale buyers because they have no incentive to offer the best possible price to each user.

Additionally, over time, the expansion of quote ranges on bright exchanges and the failure to account for trade routes through hidden liquidity on exchanges and alternative trading systems such as dark pools has eroded the NBBO, further reducing market makers’ profitability. Minimum execution quality.

To address these issues, the SEC proposed in December 2022 to change the stock market structure from a PFOF to a 100- to 300-millisecond tick-by-tick auction operated by an "open competitive trading center" (such as an exchange). This change is intended to drive better execution of user orders by democratizing retail order flow to the wider market (such as institutional investors) and adjusting market maker incentives on an order-by-order basis.

The most competitive, accessible, and incentivized pay-to-order auction is exactly what DeFi has been trying on a massive scale over the past two years!

Order flow power

To tie into the conversation about DeFi market structure, we will first cover the order flow market share of each front-end. Understanding order flow market share is important for reasoning about who has enough power to influence the market structure of DeFi, who controls which parts of the market, and who those market parts are valuable to.

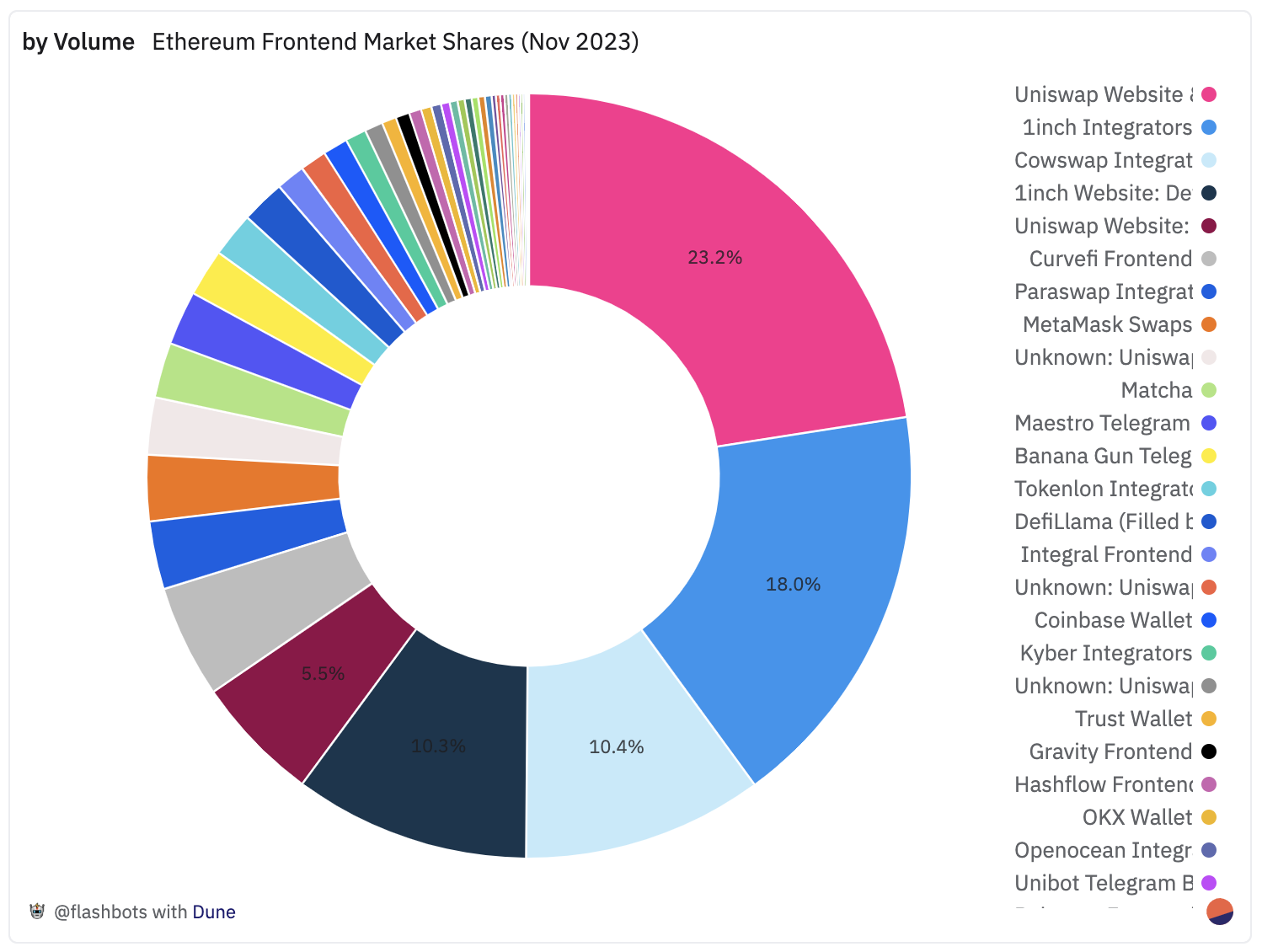

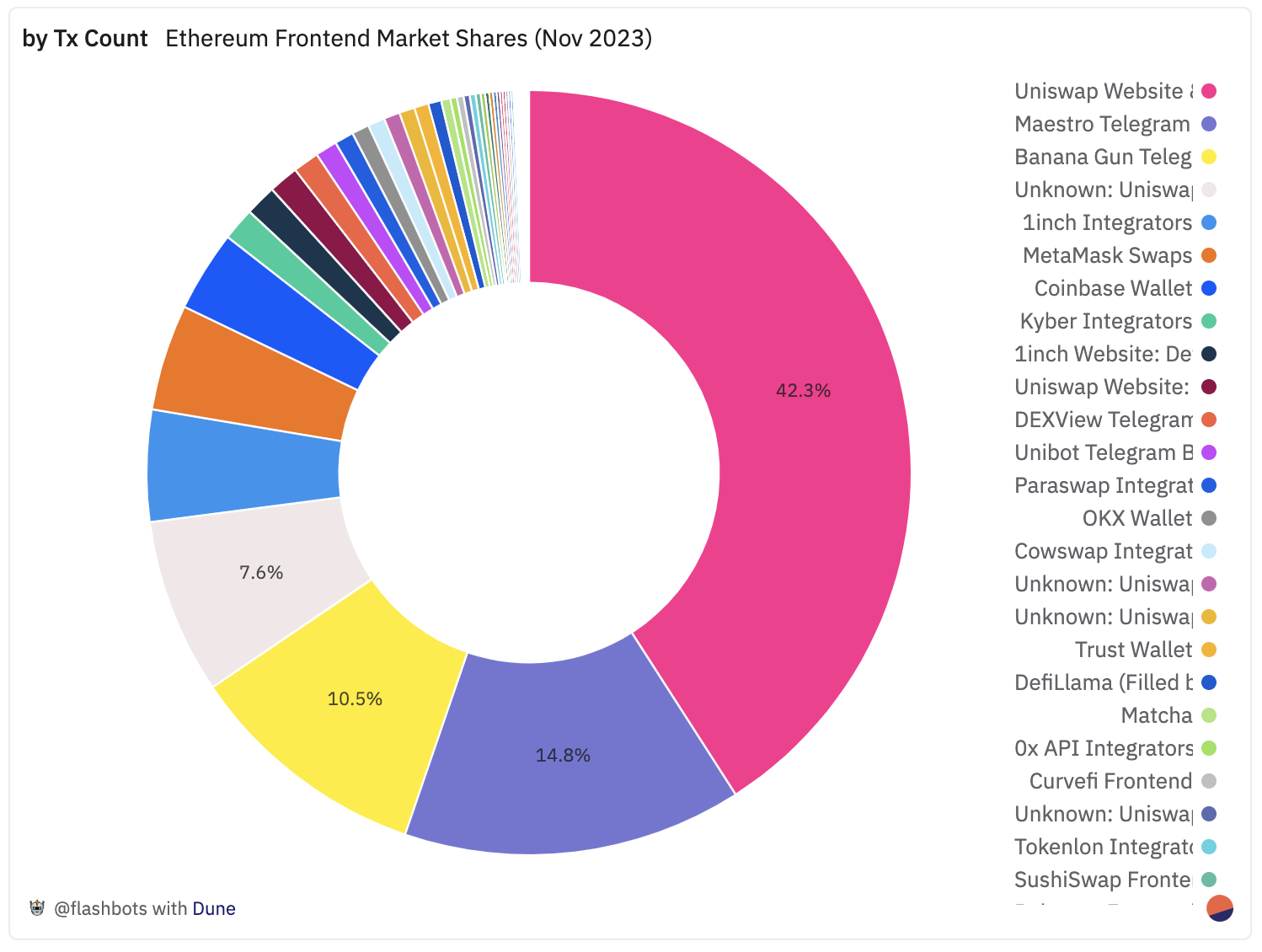

The data we will provide was collected from the Ethereum blockchain between November 1, 2023, and November 30, 2023.

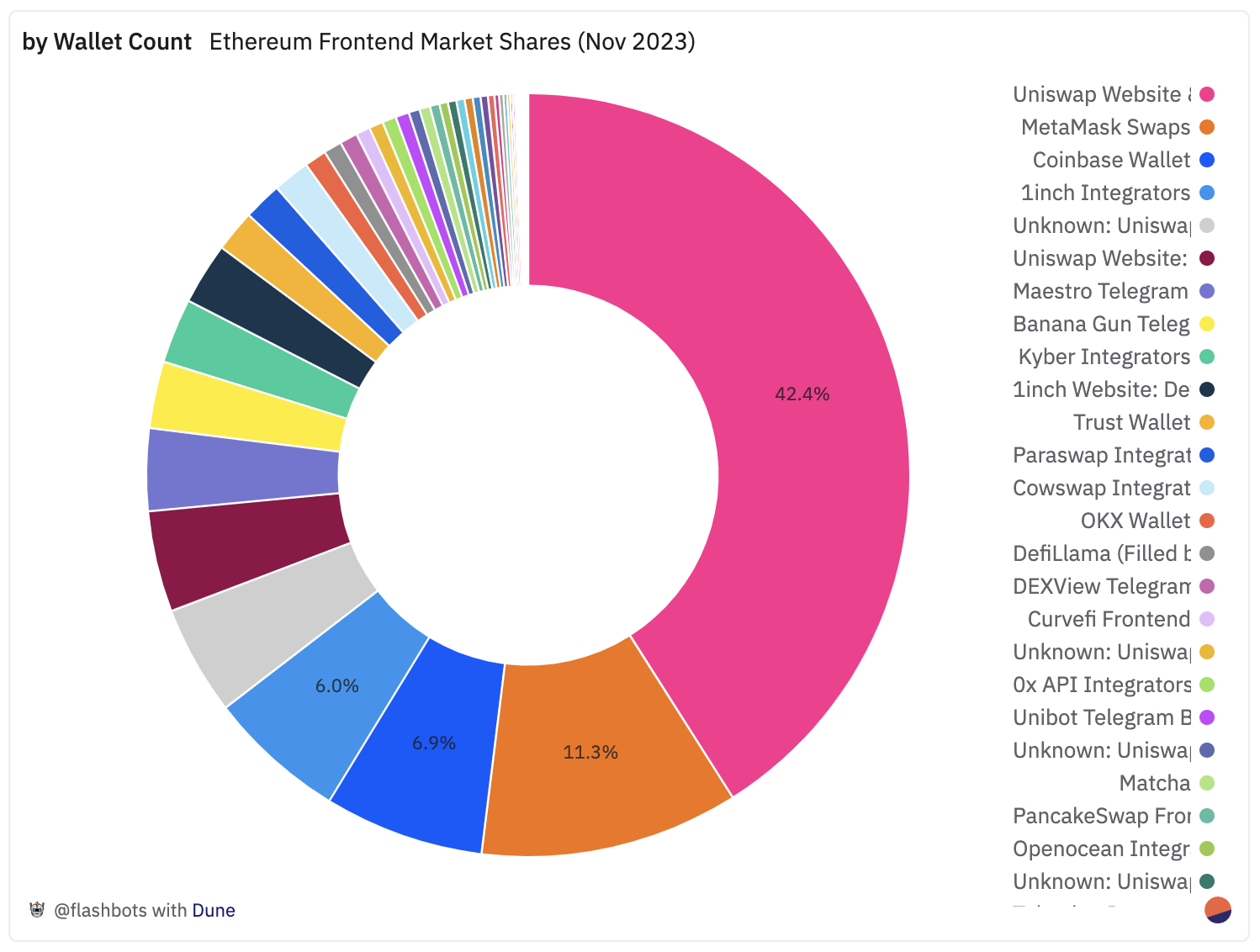

Figures 2, 3, and 4. Market share percentage by transaction volume, number of transactions, and users for the 45 tracked Ethereum frontends1 between November 1, 2023, and November 30, 2023.

Figure 2 shows that $14B of Ethereum DEX trading volume in November 2023 originated from transactions directly calling the front-end router contract, which we estimate is mostly retail, non-toxic order flow.

Figure 2-4 shows that order flow on Ethereum is dominated by Uniswap’s website application and wallet. In November, they processed more than 2.2 million transactions for 370,000 users and a transaction volume of $4.03B, accounting for 29% of the market share respectively. , 44% and 47%. Next is frontend and API integrator 1inch, which has $3.9B in trading volume across 68,000 users. Figure 3 shows that Telegram bots Maestro (750,000 transactions, 15%) and Banana Gun (537,000 transactions, 10%) are second only to Uniswap in terms of number of transactions. Figure 4 shows that Uniswap’s user base is followed by the popular in-app wallet exchange platform Metamask (90,000 users, 11%) and Coinbase Wallet (55,000 users, 7%).

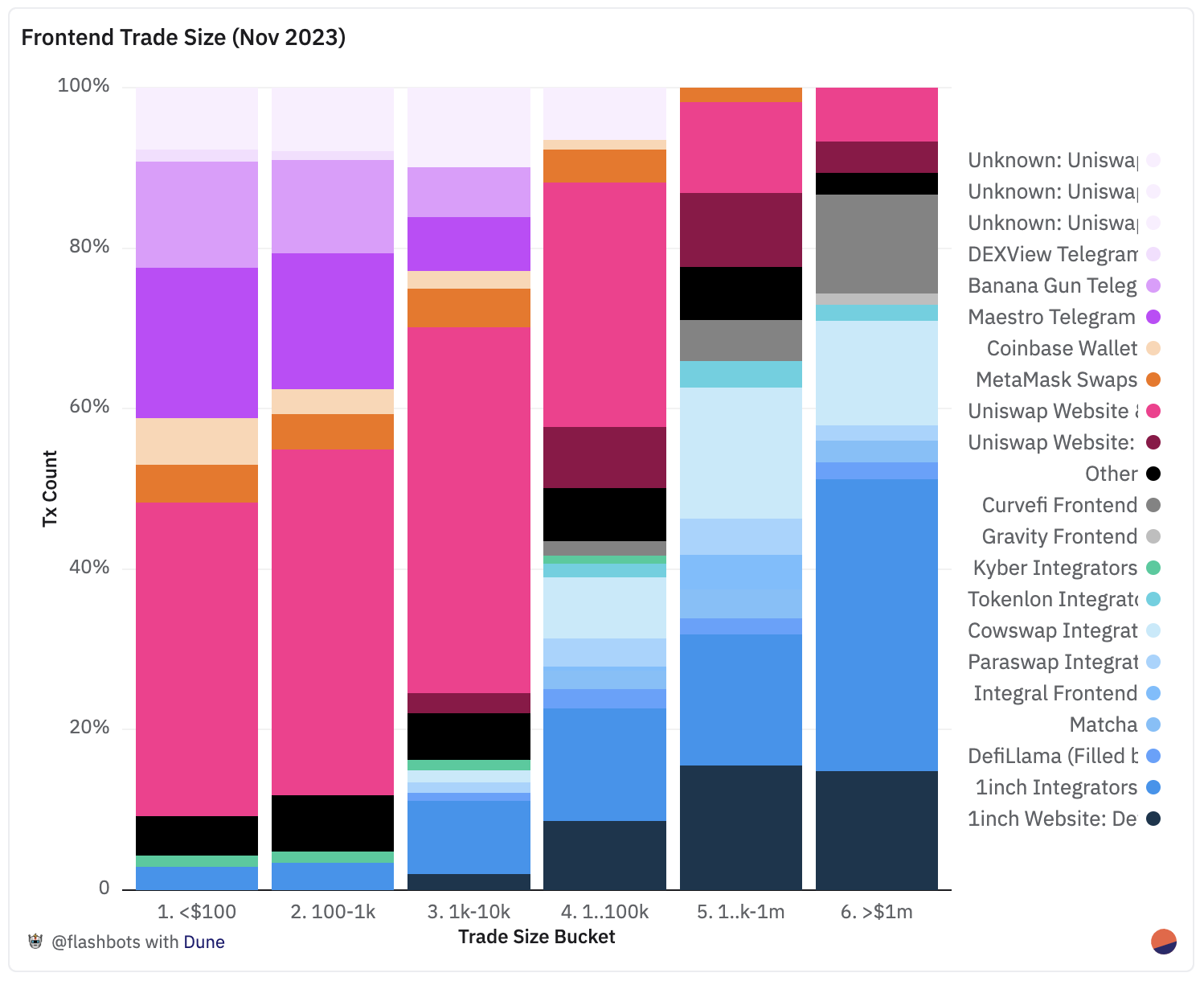

Figure 5. Market share percentage per frontend by number of deals across various deal sizes from <$100 to >$1M, from November 1, 2023, to November 30, 2023.

Figure 6. Transaction volume of different token pair categories on the Ethereum front-end in November. ETH/BTC represents ETH and BTC paired with USDC/USDT/DAI. Pegs include popular stablecoin pairs such as USDC/USDT and pegged currency pairs such as stETH/WETH. ²The long tail includes all other pairs.

Figures 5 and 6 show that different front ends cater to different user profiles. Telegram bot users’ transactions are smaller, up to $10,000, and are almost exclusively targeting long-tail coins. Aggregators and solver auctions such as 1inch API and 1inch Fusion, Cowswap, and Uniswap

More generally, Figure 6 shows that of the $14B in retail trading volume on Ethereum in November 2023, 50% was trading long-tail token pairs on Ethereum, 23% was trading ETH/BTC token pairs, and 27% Trading pegged token pairs.

Decentralized block construction (centralized MVP)

On October 13, 2023, kyoro.eth used Cowswap to sell HAY , the token Hayden Adams launched five years ago to test Uniswap V1, for 2.7 ETH. 12 Cowswap solvers competed to find the best route, with solver Laertes winning by routing to the aggregator 0x Protocol, which routed transactions through the Uniswap V1, Uniswap V2, and Uniswap V3 HAY-WETH pools. Solver Laertes then submitted the trade to the order flow auction MEV-Blocker, which received 18 bids from searchers in support of the trade. MEV-Blocker sends the backtrace to 7 block builders who compete to merge them, Builder0x69 won the block after merging 4 atomic backtrace, two of which filled the open 1 inch user limit order, and one Signal backtracking from searchers willing to hold HAY stock. Ultimately, Builder0x69 and the Seeker backtrack returned a total of 0.4 ETH (approximately $900 at current market prices) in the form of recaptured MEV to Cowswap’s designated refund address.

Taken apart, this is:

1 solver auction + 12 Cowswap solvers + ≥ 1 aggregator + ≥ 3 decentralized exchanges

+ ≥ 3 HAY-WETH passive liquidity providers + 1 order flow auction

+ ≥ 4 Atomic Searchers + ≥ 1 Signal Searcher + 2 1-inch Limit Order Users + 7 Block Builders

≥ 35 entities participate to help kyoro.eth get preferential prices on transactions!

To understand the complexity of the individual transactions being processed, it is important to understand each of the four consecutive order-by-order auctions involved and how they coordinate a network of professional searchers to drive higher prices for users. We will start with the first auction, which occurs at the intent level before a transaction is created, and ends with the auction of full Ethereum blocks.

Solver Auction

Pioneered by Cowswap and later adopted in different ways by 1inch Fusion and Uniswap X, solver auctions evolved from aggregators that outsourced the work of optimal routing of transactions to competitive markets. The ability to compete and profit simply by optimizing trade routes without having to compete on front-end and liquidity products has spurred the rise of a new class of specialized searchers called “solvers.”

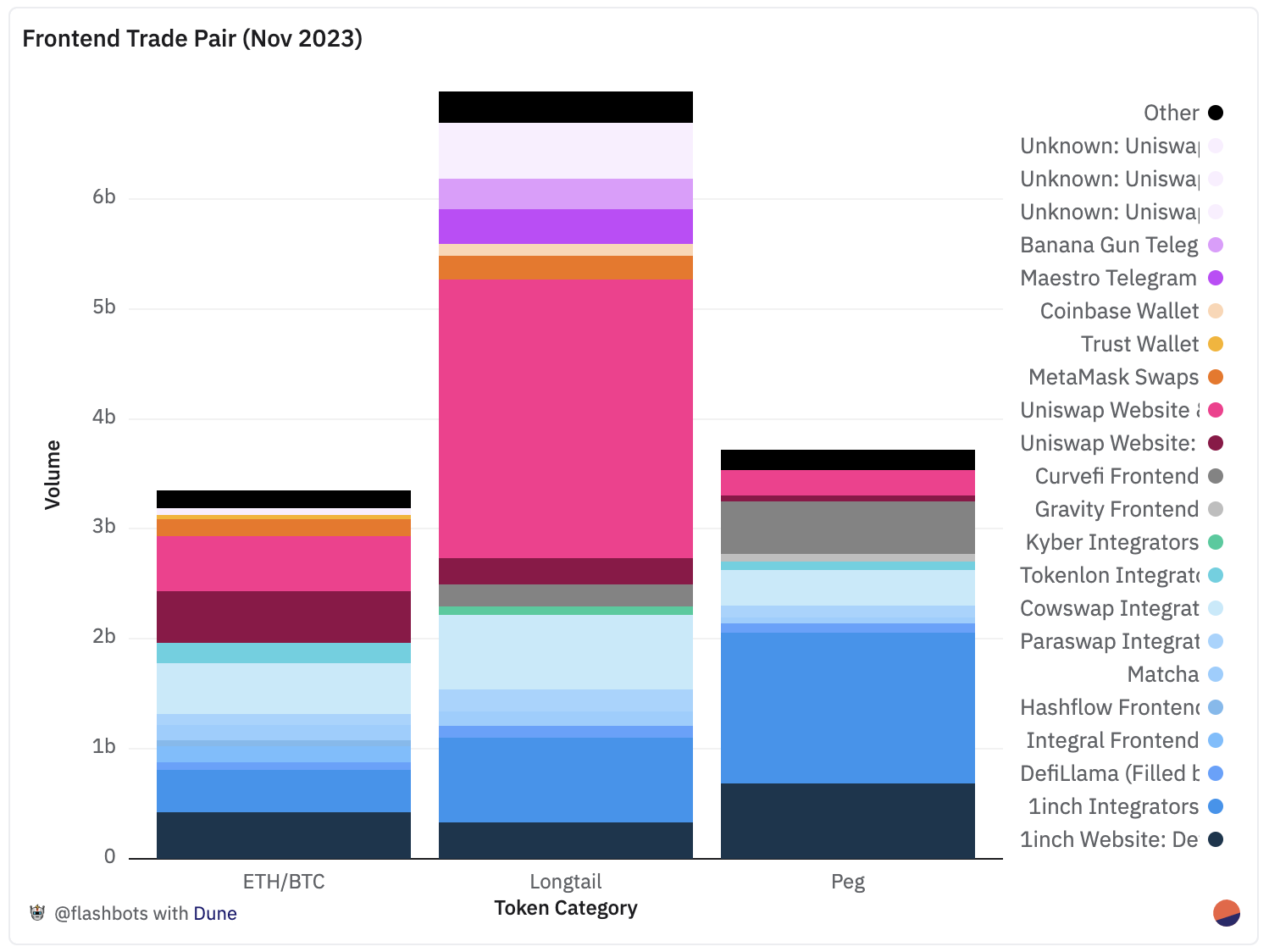

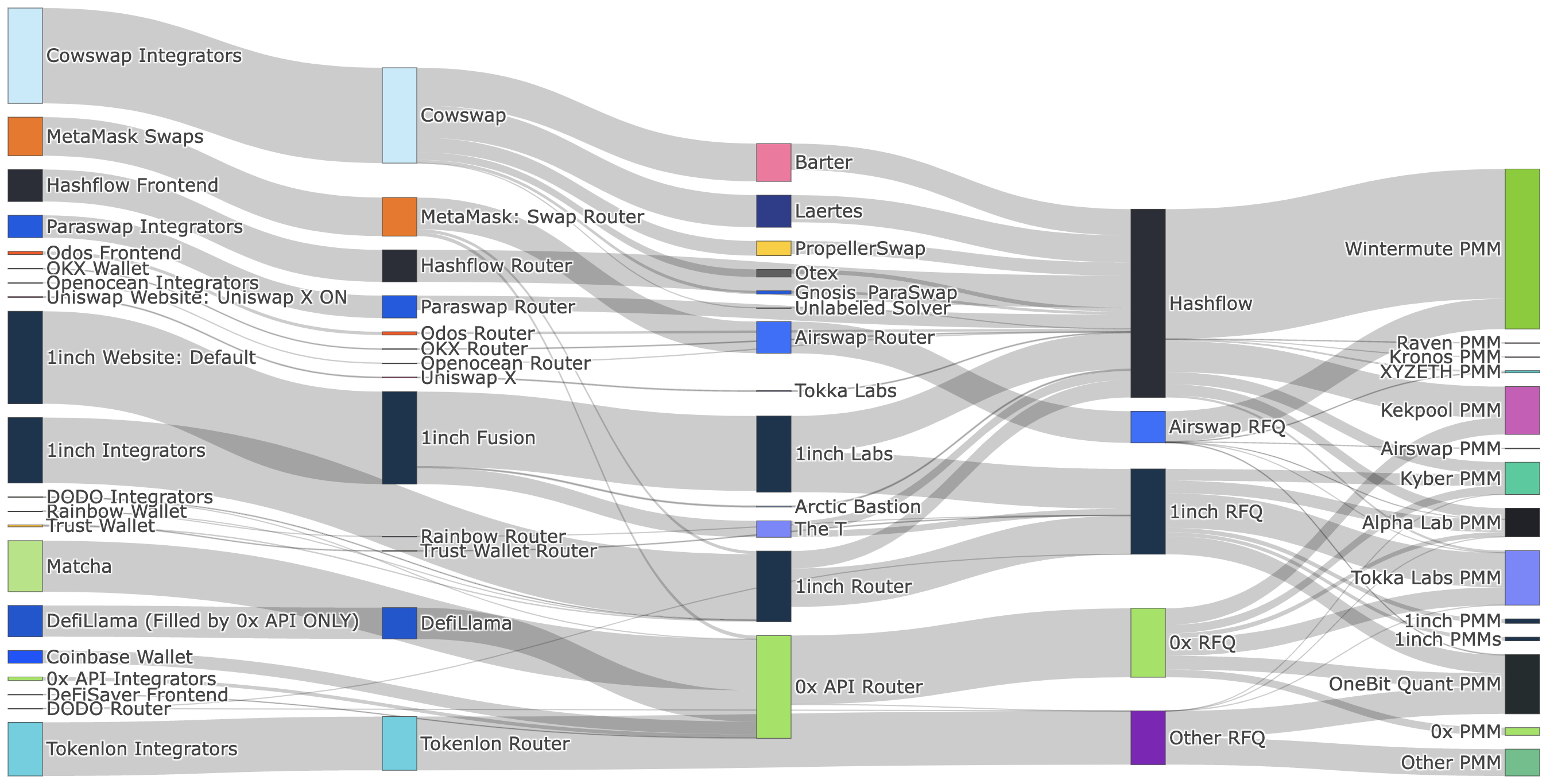

Interact with Sankey diagrams on orderflow.art .

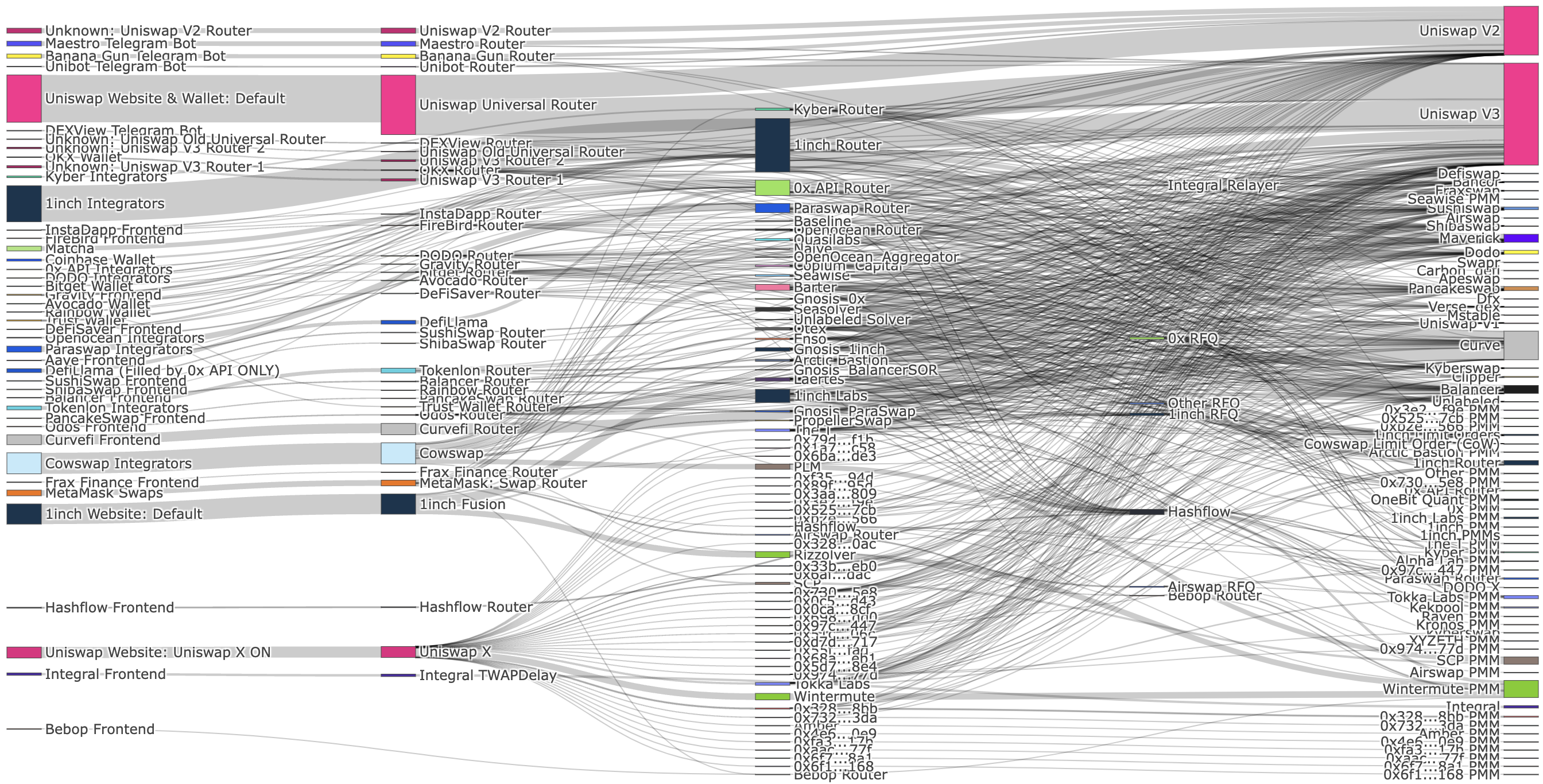

Figure 7. Sankey diagram illustrating where solvers obtain liquidity for transactions sent to solver auctions Cowswap, 1inch Fusion, and Uniswap X. Entity height reflects the transaction volume of landed transactions through each entity in November 2023. Transaction process: Frontend → Solver Auction → Solver → Liquidity Aggregator → Liquidity Source.

Competition in routing trades involves integrating many liquidity sources and optimally allocating trade amounts among these liquidity sources. Figure 7 shows the three solver auctions with a total of 22 solvers accessing over 33 liquidity sources. Figure 7 also shows solvers accessing liquidity through automated market makers (AMMs) (notably Uniswap V3) and private market makers (PMMs) (notably Wintermute and SCP).

Unlike tradfi's NBBO's requirements for price improvements, which fail to consider optimal transaction paths and miss out on private liquidity, the NBBO in the Defi version of the solver auction is maintained by a competitive market of 22 solvers , the market optimizes trade paths for hundreds of sources of public and private liquidity .

Figure 7 also shows that in November 2023, in landing transactions, $14 million of Cowswap user orders matched 1-inch user limit orders. To win the solver auction, 1-inch limit orders must offer better prices than private market makers, supporting the SEC's proposed Rule 615 to expand market access to fill retail order flow can lead to better user outcomes.

Figure 8. Retail transaction volume by front-end category over the past 3 years: DEX front-ends, Telegram bots, in-app wallet exchanges, aggregator API integrators, and solver auctions. Solver auctions include Cowswap, 1inch Fusion and Uniswap X.

Figure 8 shows the growth over time in the percentage of order traffic auctioned through the solver. In November 2023, $3.67B (26.3%) of retail transaction volume was conducted through one of the three main solver auctions.

The growing popularity of solver auctions and increasing competition in the solver market also lower barriers to the adoption of innovative liquidity projects. Solvers are directly incentivized to integrate as many liquidity sources as possible to provide more competitive quotes and win solver auctions. Therefore, for the upcoming wave of Uniswap V4 pegs, developers will only need to integrate one of the 13 Cowswap solvers to compete to fill $1.5B in trading volume (10.5% of Ethereum retail order flow in Figure 2 ). As solvers become more complex over time, defi will also be able to support higher complexity caps on liquidity mechanisms that today's routers cannot support.

Next, we will focus on advances that lower the barrier to market entry for retail order flow, a key source of liquidity that drives competitive pricing for highly liquid token pairs.

market maker auction

Previously, the primary way to access market maker liquidity was through ask-quotes constructed through aggregators such as 1inch and 0x. However, this also comes with the limitation that only the aggregator’s own routing algorithm can access the liquidity of its integrated market maker. Restricting order flow access to RFQ increases the barrier to entry for market makers, who must spend resources integrating each RFQ API to access each project's order flow. Hashflow then developed an ask that allows any project or solver to leverage the liquidity of its market maker.

Interact with Sankey diagrams on orderflow.art .

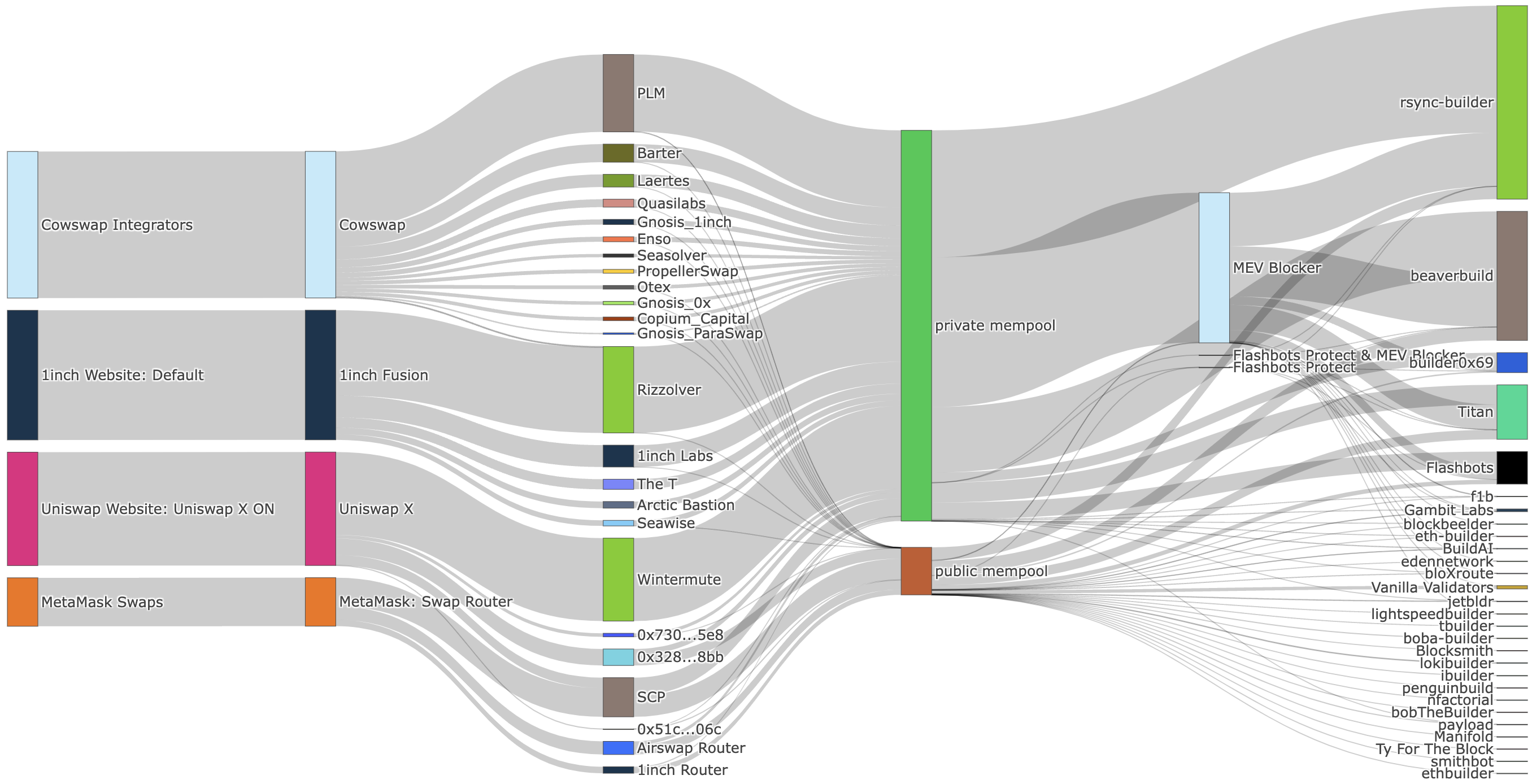

Figure 9. Sankey diagram showing the distribution of the number of projects that obtained liquidity from RFQ and Hashflow and their integrated private market makers (PMM) in November 2023.

Figure 9 shows the order flow sources for RFQ built by aggregators 1inch, 0x, and Airswap are limited to their own frontends and aggregation API integrators. Hashflow’s order flow sources, on the other hand, include solvers on Cowswap, 1inch Fusion, and Uniswap X, wallets like OKX, meta aggregators like Defillama , Odos, and OpenOcean, and even solvers on 1inch Labs. Fusion and 1inch API.

In November 2023, eight market makers competed to fill over $1.45B ( 45% in Figure 6) of ETH/BTC trading on Ethereum via Cowswap, 1inch Fusion and API integrators, and Paraswap through an API integration with Hashflow quantity. Of the realized market maker fills, Figure 9 shows that Hashflow market makers filled $374 million, more than double the 0x and 1inch RFQ market maker fills.

Market makers integrated with solvers via Hashflow have two additional benefits:

- Bypassing solver staking requirements: To become a solver, Cowswap requires solvers to stake 750,000 , 1.5 million COW tokens (currently priced around $415,000) and 500,000 cUSDC. 1inch Fusion requires resolvers to have at least 5% "unicorn power," which is about 1 million 1inch tokens (current price of about $435,000) locked for two years. Integration with solvers enables market makers to bypass the staking requirements of Cowswap and 1inch Fusion to compete for $3 billion in trading volume in November 2023 ( Figure 2 ).

- Access more trades: Without implementing a routing algorithm, market makers can only respond to user quotes if the request matches the set of token pairs they reference. Outsourcing routing to a competitive solver market increases the opportunity surface area for currency pairs that market makers can quote. In this transaction , Cowswap users are trading 2.1M wstETH → USDT, solver Barter splits the transaction into 2.1M wstETH → WETH on Kyberswap, and then 1.6M WETH → USDC and 500k WETH → USDT through Hashflow with Wintermute, and then It is USDC → USDT on 1.6M Maverick.

Enabling market makers to quote more currency pairs on more order flow sources increases competition and drives higher prices for users.

Order flow auction

Solver and market maker auctions are designed to provide the most competitive offers for users to sign. Once an end-user signs a transaction, the entity responsible for transaction inclusion (such as a wallet or resolver) can choose to send the transaction to an order flow auction.

Last year, order flow auctions were introduced as a feature on top of private RPC as the use of sandwich and recovery protection increased. In November 2023, 2 million (41%) retail order flow transactions flowed through private RPC endpoints, with transaction volume reaching $6.3B (45%).

Prior to the order flow auction, competition among searchers increased in the bundle auction , increasing the percentage of profit that searchers had to bid to validators. Atomic searchers and signal searchers respectively profit from backend trades when trade paths are not ideal or price signals are not taken into account. By introducing another auction before the bundle auction, the order flow auction redirects the profits previously earned by validators to users. This is accomplished by auctioning transaction slots behind user transactions to searchers who want to best capture the opportunity for backtracking.

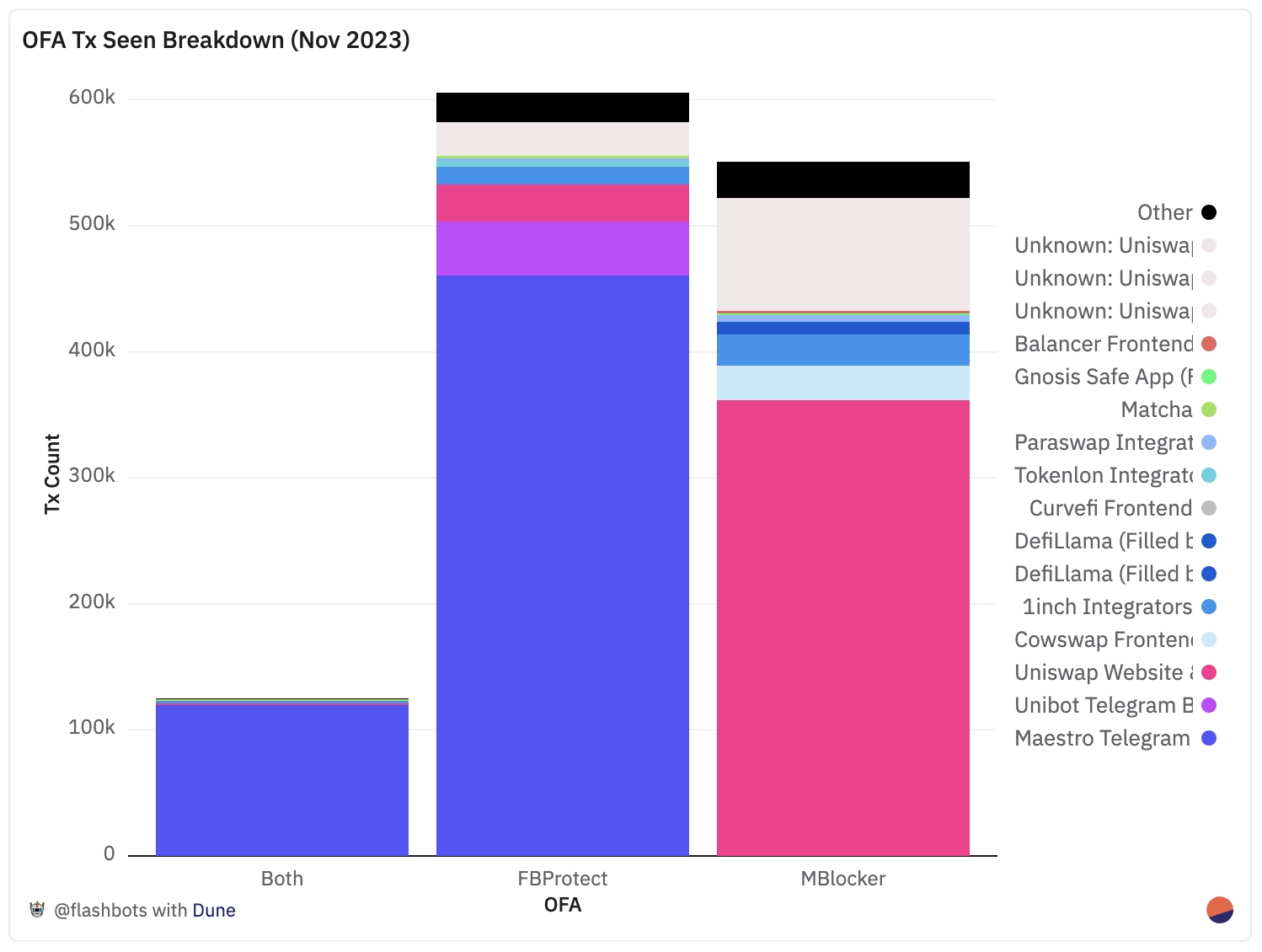

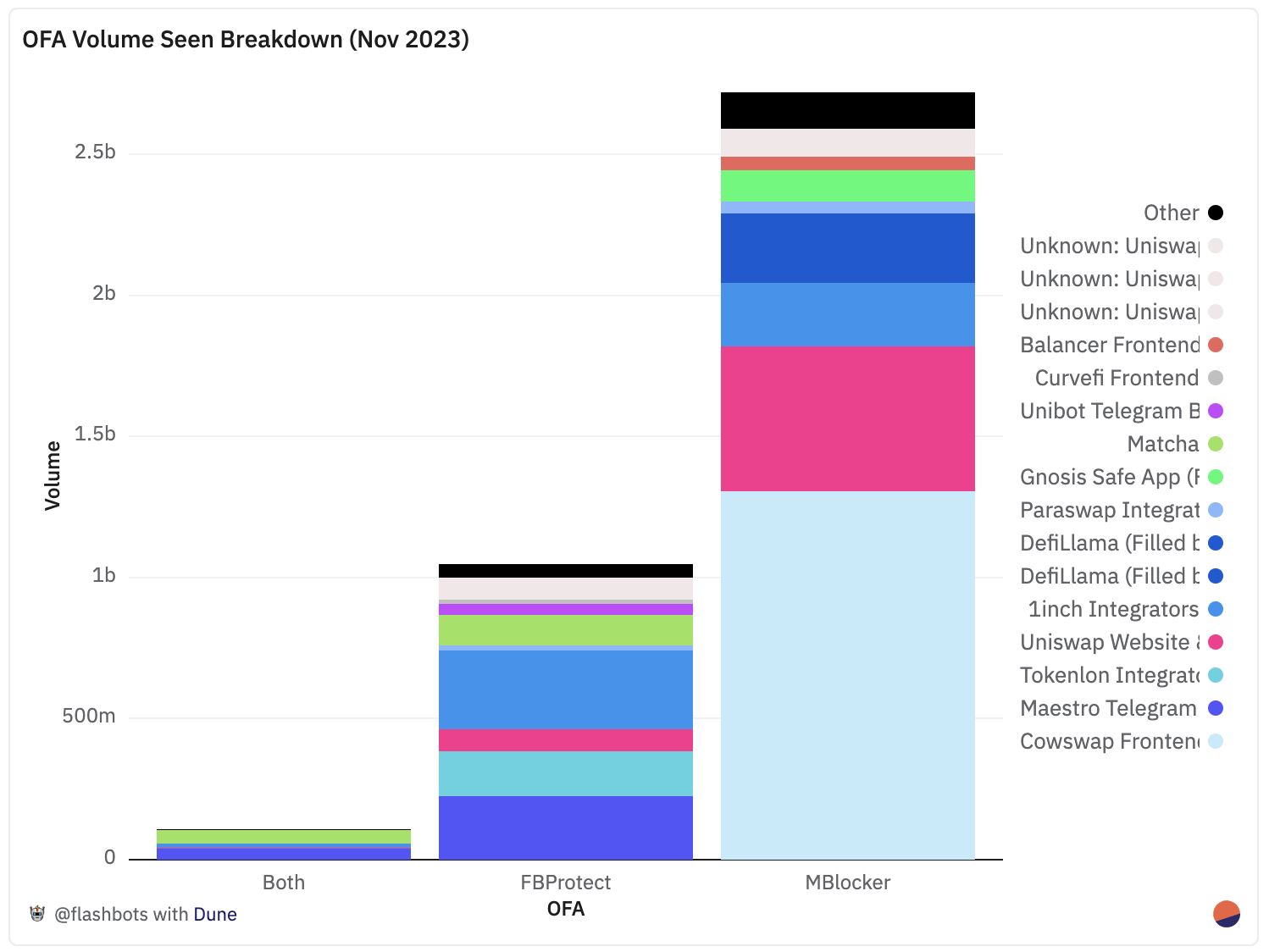

OFAs MEV-Blocker and Flashbots Protect (running the MEV-Share OFA protocol) have published transactions seen on their RPC endpoints on Dune , which allows us to observe who the main users of OFA are and assess the competitiveness of their offers .

Figure 10. Number of retail order flow transactions received by MEV-Blocker and Flashbots Protect RPC endpoints by item. Both represent transactions received by two OFAs.

Figure 11. Retail order traffic received by MEV-Blocker and Flashbots Protect RPC endpoints by item. Both represent the amounts received by the two OFAs.

Figure 10 shows that MEV Blocker’s largest source of order flow in terms of number of transactions is Uniswap’s mobile wallet . Although Cowswap’s transaction volume is not high, Figure 11 shows that Cowswap accounts for $1.5B (59%) of the transaction volume flowing through MEV-Blocker. Figure 10 also shows that Flashbots Protect’s largest source of exclusive order flow by number of transactions is the Telegram bot Unibot. Figure 11 shows that imToken wallet is the largest transaction volume contributor to Flashbots Protect, sending $159 million (15%) of transaction volume.

Telegram bot users mainly trade liquid tokens on Uniswap V2. However, sometimes the tokens being traded have liquidity elsewhere. When the Telegram Bot Router misses these sources of liquidity, arbitrage opportunities arise. On December 22, 2023, the highest refund received by Unibot telegram bot users was 0.255 ETH (then $592) . User 0xc3f7 swapped 0.8 ETH ($1800) for Omnicat tokens and backtracked on atomic arbitrage of OmniCat tokens to the Uniswap V2 < > V3 pool. From July to December 2023, Unibot telegram bot users received 3.6 ETH in 230 tracebacks, with an average refund of 0.016 ETH (approximately $35 at current prices).

Figure 7 , on the other hand, shows that Cowswap has 13 solvers competing to access 33 liquidity sources and optimally distribute user transactions among these sources. However, since their launch in April 2023, their solver transactions have still been returned 7,700 times , with a cumulative refund of 376 ETH ($845,000 at current prices).

Solver transactions may still expose background running opportunities for the following reasons:

- Price signals not previously considered, as some signal seekers (usually the same group of market-making entities) not included in the earlier auctions may still want to buy at the final AMM price.

- Sources of liquidity for PMM and AMM liquidity were not previously considered.

- Transactions are not ideally distributed among the liquidity sources considered.

As solver complexity increases, the opportunities for reverse runs due to reasons (2) and (3) should decrease over time.

Order flow auction refunds are also another source of monetization for solvers, frontends, wallets, and users. Cowswap protocol rewards are the primary source of monetization for Cowswap solvers who are not market makers. However, from May 2023 to December 2023, Cowswap issued 388 ETH in solver rewards, which is almost the same as the 376 ETH in MEV-Blocker refunds during the same period. Everyone from solvers, frontends, wallets, to users who didn’t send an order flow auction today could be left with a ton of money! cube

OFA Searcher Competition

Searcher integration with MEV-Blocker and MEV-Share is permissionless, making OFA the lowest barrier to entry point in the entire order flow network, and therefore potentially the most competitive.

MEV-Blocker and MEV-Share enable permissionless integration by using privacy-based mechanisms to protect user transaction execution and prevent searcher misconduct. Integration at any other point in the order flow network requires stake, KYC, or trust relationships to inhibit inappropriate behavior. MEV-Blocker enables transaction privacy by removing transaction signatures and issuing additional fake transactions to backend searchers. MEV-Share enables programmable privacy , such as only revealing to backend searchers the pool a user is trading in (e.g. USDC-WETH Uniswap V3), but not the limit price or trade direction.

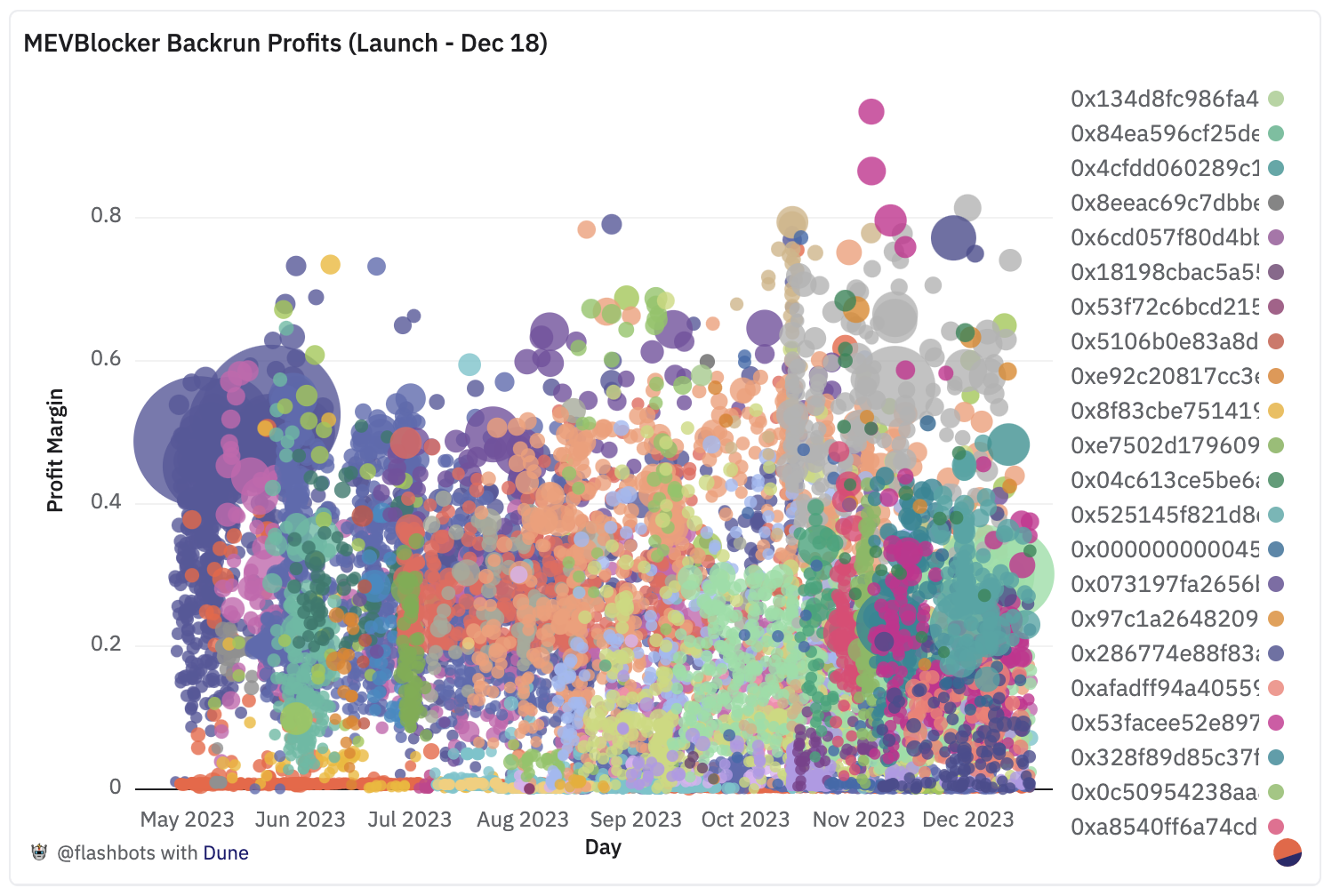

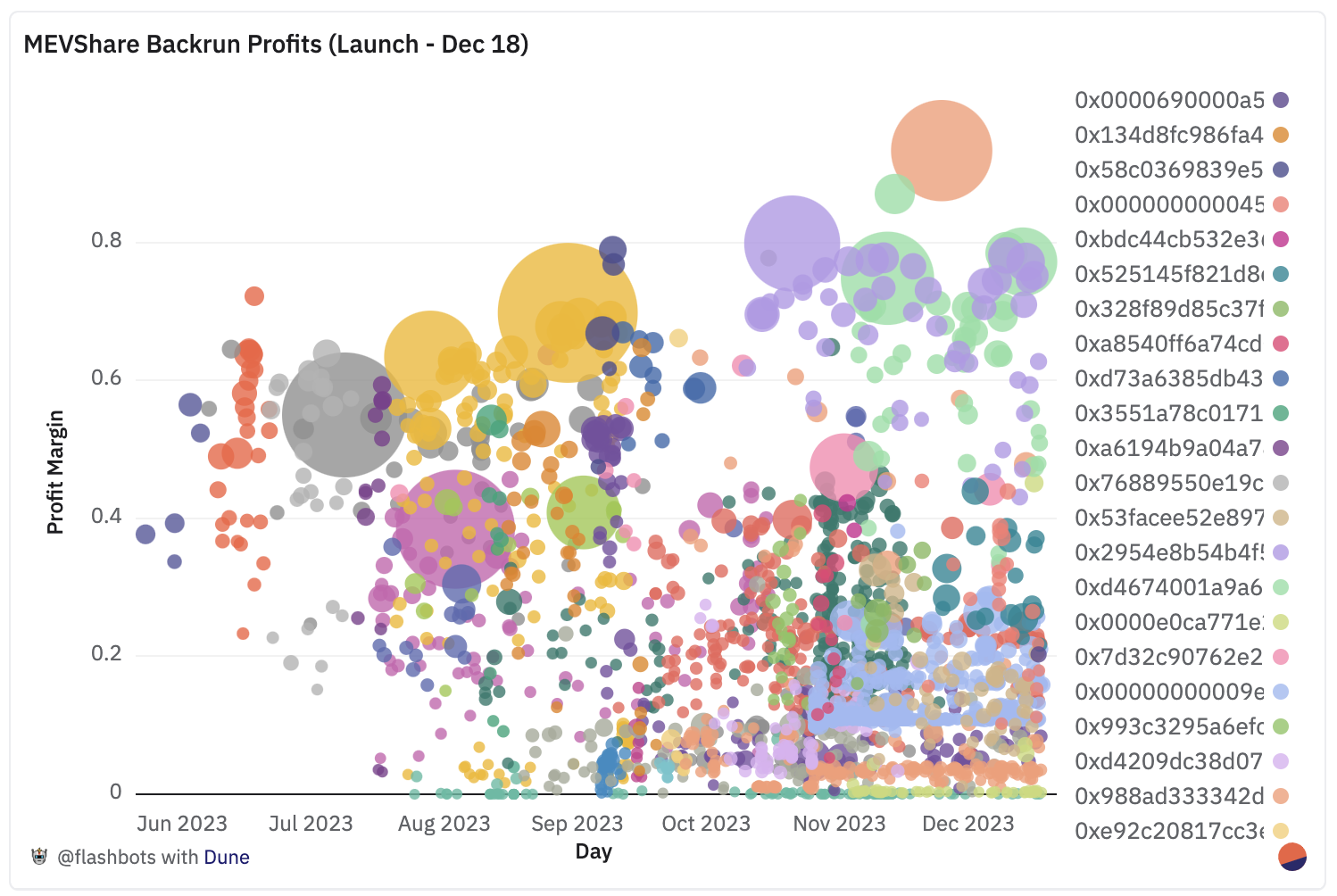

Order flow auctions rely on searchers competing to find more arbitrage opportunities and bidding users a higher profit percentage. We will focus on atomic arbitrage because calculating searcher profits using on-chain data is deterministic. Using LibMEV ’s Atomic Arbitrage Profit API, we observed that since launch in May 2023, 52 atomic searchers have made 207 ETH on 15,000 backtracks on MEV-Blocker, and 38 atomic searchers have made 207 ETH on MEV-Share Performed 2,700 backtracements and earned 63 ETH.

Figures 12 and 13 show searcher profit margins over time for MEV-Blocker (top) and MEV-Share (bottom). A profit margin of 0.4 means that if atomic arbitrage yields a profit of 2 ETH, the searcher keeps 0.8 ETH after tipping and paying gas. The size of the circle represents the profit the searcher made in ETH.

Figures 12 and 13 show that searcher profit margins tend to zero over time in both order flow auctions. This further supports observations over the past few years that searcher margins in the atomic arbitrage market are approaching zero as opportunities arise and competition intensifies.

collective auction

As we saw in the opening example , block builder Builder0x69 is able to provide five MEV-Blocker tracebacks for users exchanging HAY for ETH: two 1inch Limit Order < > Uniswap V3 Atomic Arbitrage, two Uniswap V3 < > Uniswap V1 atomic arbitrage, and 1 signal arbitrage total refund 0.4 ETH.

Results for retail users are consistent across auctions, requiring that transactions sent to builders via order flow auctions be included only when 90% of searcher bids are returned to the specified address. Another 10% of searcher bids are transferred to builders to incentivize builders to include as many returning users as possible.

More broadly, we can think of block auctions (also known as mev-boost auctions ) as a competition among block builders to quickly incorporate non-conflicting searcher preferences. A year ago, Flashbots open-sourced our production module builder to lower the barrier to entry and drive competition toward faster bundle merging and simulation. Currently, a total of 41 builders are actively participating in collective auctions.

Decentralization and competition

We have shown how each of these four auctions lowers barriers to entry, democratizes access to retail order flows, and increases competition. Four consecutive make-to-order auctions together create a market structure in which:

- Anyone with economically meaningful information can express it into the block building process before user transactions are executed.

- Searchers are becoming more specialized, collaborating on routing, providing liquidity, and bundling mergers to produce blocks, rather than having a few large entities do more.

- Competition among this network of professional searchers is effectively exploited to increase prices for users on an order-by-order basis.

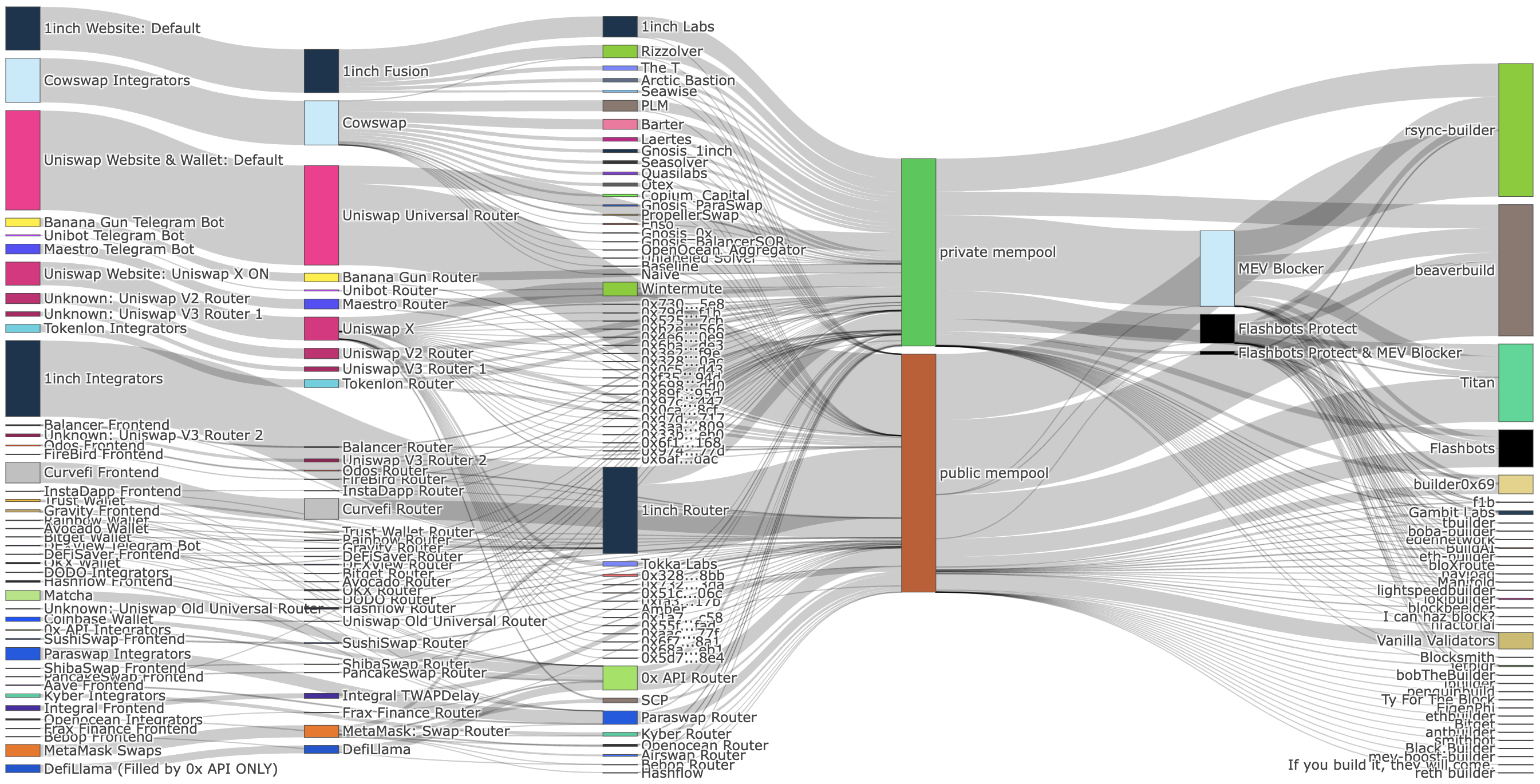

Ultimately, successive sequential auctions demonstrate the decentralized and collaborative process of reaching global consensus on financial conditions. We use a Sankey diagram to visualize this process through November 2023.

Interact with Sankey diagrams on orderflow.art .

Figure 14. Sankey diagram of retail trade volumes, showing trade flow from frontend, solver auction, solver, order flow auction, and ultimately builder to inclusion in November 2023. ⁴

Interact with Sankey diagrams on orderflow.art .

Figure 15. Sankey diagram of retail liquidity impact, focusing on liquidity per user order source in November 2023. ⁴

Figures 14 and 15 show that 33 solvers, 12 market makers, 90 OFA backend operators, and 41 block builders are involved in facilitating and optimizing user transactions for 12,000 token pairs . The scale of Defi and the number of tokens traded demonstrates the extent of global user desire, while a handful of players in a handful of trust zones are unable or unwilling to serve. The quality of Defi's execution shows the desire, effectiveness, and diversity of searchers, and when you build systems that allow them to do so, they will show up to satisfy such user preferences.

Ultimately, Figures 14 and 15 show that global, competitive, and cooperative systems are possible in a highly financialized environment, and that they can be very beneficial to users.

There is more work to be done.

As the volume of orders flowing through solver auctions increases, it is important to consider the impact of the solver mechanisms we design on the structure of the DeFi market. A front-end controlling a large volume of order flow can quickly and significantly change the market structure, thereby altering the decentralization of the network.

Fight the inertia of centralization.

In contrast to atomic arbitrage, which has become more competitive and decentralized over time ( Figures 12 and 13 ), market makers have historically been an active centralizing force in tradfi and defi. The natural power of concentration is to dominate other markets from existing markets in which it operates due to economies of scale and the transferability of its advantages (e.g. in delayed infrastructure and asset pricing models).

Sankey diagrams are available on orderflow.art .

Figure 16. Sankey chart showing ETH/BTC volume flows for Cowswap, 1inch Fusion, Uniswap X and Metamask swaps since November 2023.

Figure 16 shows that market makers SCP (PLM on Cowswap) and Wintermute (Rizzolver on 1inch Fusion) account for more than 75% of the ETH/BTC on the four major order flow sources on Ethereum (Uniswap, 1inch, Metamask and Cowswap) Trading volume. Cowswap is the exception among the four, with SCP's Solver PLM directly filling 40%, which may be due to Cowswap's mechanism design and/or more solver competition.

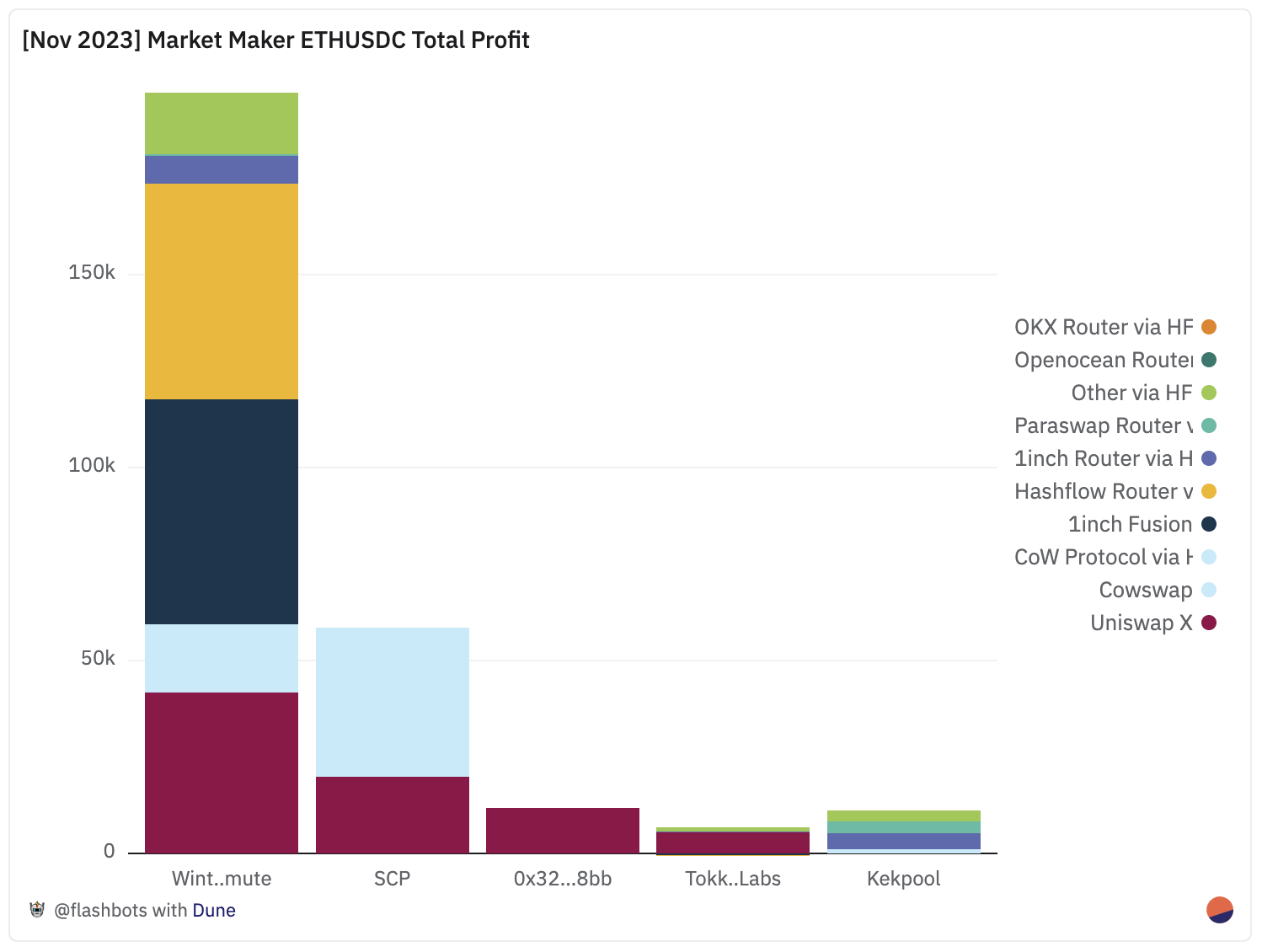

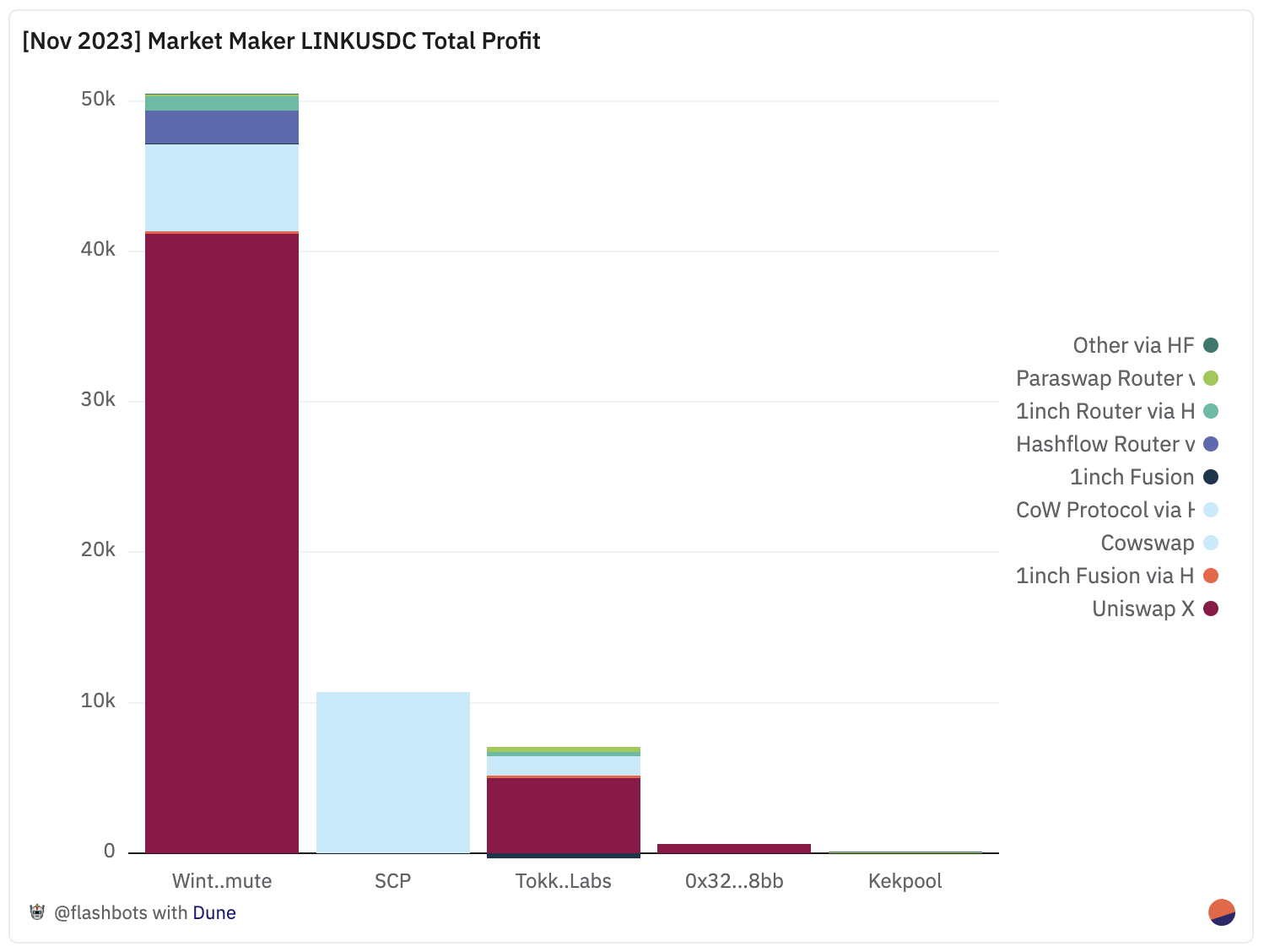

To understand the relationship between trading volume and profits, we estimate the market making profits of solver auctions through direct integration of market makers as solvers and indirect integration through Hashflow. We focus on ETH-USDC, the most popular trading pair on Ethereum, and LINK-USDC, the most popular trading pair outside of ETHBTC and pegged token pairs. Profits are estimated by applying markups against the centralized spot exchange Binance, often considered a price discovery venue for cryptocurrencies, estimating the fair value of highly liquid assets.

Figure 17a. Estimated profits from market making ETH-USDC on Uniswap X, Cowswap, 1inch Fusion, and Hashflow in November 2023⁵ .

Figure 17b. Estimated profits from LINK-USDC market making on Uniswap X, Cowswap, 1inch Fusion and Hashflow in November 2023⁵ .

Figure 17 shows that even among the top five market makers on ETHUSDC and LINKUSDC, profit distribution is top-heavy. Figure 17 also shows that market making profits do not always correlate with trading volume, and the profit-to-volume ratio can vary between token pairs. On Uniswap SCP, on the other hand, made $20,000 from $16 million in ETHUSDC trading volume on Uniswap X, with an estimated profit per dollar of more than double Wintermute.

Cowswap is the only order flow source that compares the profit difference between direct integration and indirect integration, where SCP integrates directly as a solver and Wintermute does the quoting via Hashflow. While it is difficult to draw conclusions due to limited data and imperfect understanding of market making strategies, we strongly encourage market makers to integrate as close to the front end as possible, including:

- To bypass fees charged by intermediaries: Hashflow and RFQ charge market makers "dynamic fees" to populate user transactions through their APIs. The market maker charges a fee per order, such as 30 basis points for risky trades (such as USDC-WETH) and 10 basis points for stable trades (such as USDC-USDT), but if the market maker changes the order path, it will be charged to the market maker. Merchants charge lower fees from purchasing AMM liquidity to PMM liquidity. In fact, the quotations of indirectly integrated market makers must be at least 10-30 basis points higher to compete with directly integrated market makers.

- To gain control over execution (called last look): In Uniswap X, directly integrated market makers can choose not to execute user orders if the price moves against the user. However, in the case of indirect consolidation, a separate entity controls the execution of trades, forcing market makers to provide a wider range of quotes or less competitive quotes in the event that prices change against them.

The funding and resources required to directly stake and integrate every system to gain this market-making advantage are something only large teams like SCP and Wintermute can afford. Likewise, running the block builder creates market making advantages that only SCP and Wintermute can provide. SCP and Wintermute, named beaverbuild and rsync builder respectively, run the two main block builders on Ethereum, and together they built 61% of MEV-Boost blocks in the first two weeks of January 2024.

The dominance of these two market-making teams across various verticals in the order flow processing network supports tradfi's historical observation of the financial system's tendency to centralize over time and the strength of economies of scale. Decentralization in decentralized finance is far from guaranteed, so we must consciously pay attention to the market structure created by our mechanisms.

Not all mechanisms are created equal.

We previously showed in Figure 16 that Cowswap’s solver market has a greater number of solvers and is less dominated by market makers. Although more order flow theoretically increases the incentive to consolidate, the distribution of power on 1inch Fusion is more concentrated.

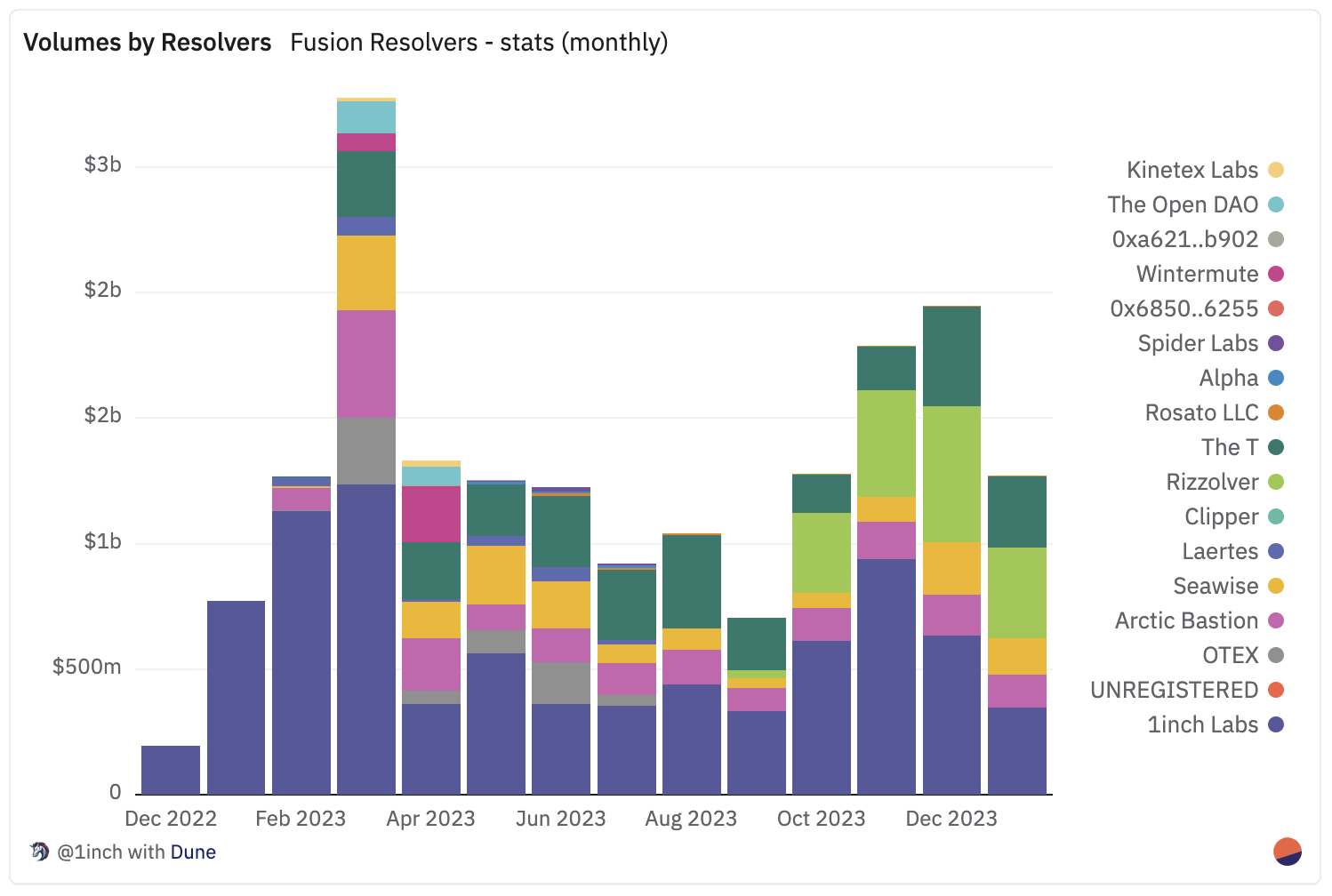

Figure 18. 1inch Fusion Volume grouped by solver since launch in December 2022.

Figure 18 shows that in November 2023, 1inch Labs itself held 50%, and market makers Wintermute (Rizzolver) and Tokka Labs (The T) held 24% and 10% respectively.

Uniswap X data also shows the concentration of power and profits in the hands of a small number of existing market makers.

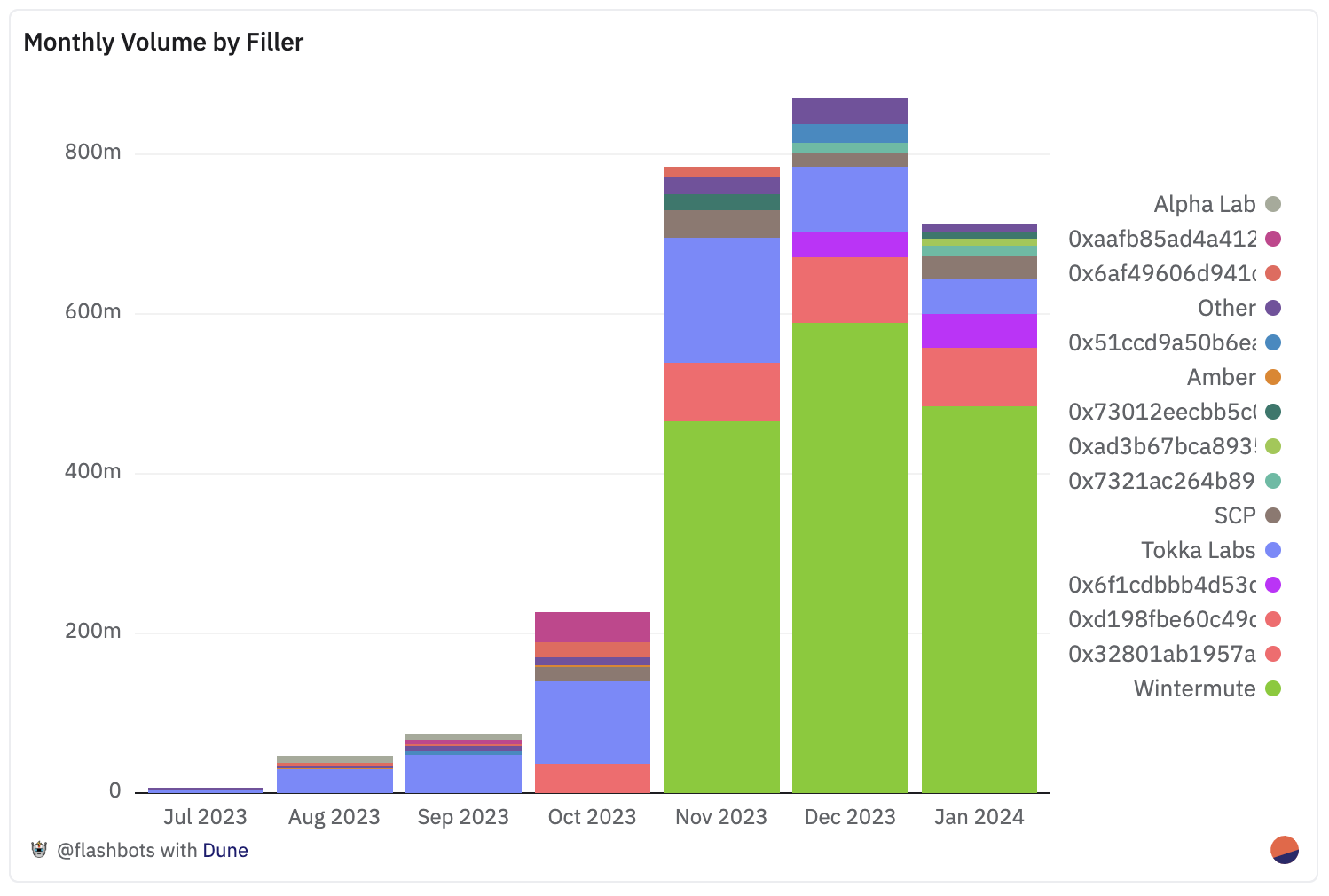

Figure 19. Uniswap X trading volume since launch in July 2023 grouped by solver.

Figure 19 shows that 90% of the trading volume on Uniswap X in November was occupied by four existing market makers, of which Wintermute, the largest market maker, accounted for 60%.

Uniswap's order flow capacity is three times that of Cowswap and 1inch Fusion ( Figure 2), and its design choices are particularly influential. The design of Uniswap This design repeats many of the mistakes of the centralized tradfi market structure we discussed earlier:

- Separate retail traffic from passive liquidity providers and flow directly to a set of licensed market makers. This change actively concentrates power in the hands of a small number of existing market makers and taxes profitability, thereby incentivizing the provision of passive liquidity.

- Mechanisms to police misconduct in general undermine the incentive to provide the best possible price to each user. When the total trading volume is only required to be >90%, the market maker will choose not to close the transaction when the price changes are unfavorable to itself, and increase the proportion through other methods, such as still closing the transaction when the loss is small.

Passive liquidity will decrease due to segmentation of up to 30% of retail order flow on Ethereum, which will:

- Over time, Uniswap traders' user quotes will become less competitive as the trading impact of reduced depth of passive liquidity increases, further reducing the minimum price that market makers must quote.

- Further negatively impacting non-Uniswap traders, such as users not in Uniswap geo-regulated front-end countries, who are unable to trade with whitelisted market makers and face greater exposure to unlicensed passive liquidity pools price impact.

We have shown in previous chapters the role of democratized access to order flow in driving better user outcomes, as well as the scope and diversity of user and searcher risk preferences. We demonstrate the presence of signal traders willing to wrap up low-liquidity token symbols, such as MEV-Blocker Seeker 0xa1c wraps up HAY and jaredfromsubway.eth , the latter of which manages an inventory of over 3,000 low-liquidity tokens with a total value of over 1,000,000. In comparison, the SCP and Wintermute markets produced 75 and 53 tokens respectively.

In designing a mechanism that favors a small number of market makers, Uniswap Instead, Uniswap created a system that was biased towards the risk appetite of existing businesses and ultimately underserved defi and Uniswap’s own core user base, which itself accounted for $2.8 of Ethereum retail long-tail token trading volume in November 2023 B (40% in Figure 6 ).

No, Uniswap, you have to choose decentralization, I'm just giving you a choice so you can feel some sense of control. You have to repair the breach yourself. Source: Barbie Movie

Privacy is powerful. #

Information privacy of transactions is particularly important to maintaining the execution quality of auction-by-deal auctions. Even the market makers themselves have emphasized this point – in Citadel’s comment letter to the SEC’s proposed Rule 615, they listed two issues with transaction privacy in trade-by-trade auctions and described their adverse impact on execution quality:

- Advance Trading: "(Auction news) will include detailed information about the characteristics of the retail order, including the stock, direction (buy or sell) and auction limit price. Therefore, all market participants will know the details of the retail order before the order is actually executed." Relevant characteristics and be free to trade ahead of retail orders based on that information, even if the execution of the retail order is not certain. The proposal therefore creates an effective license and encourages others to trade ahead of retail orders mechanism. Information leakage significantly increases the likelihood of price movements in a direction unfavorable to retail investors, while orders are delayed by 100 to 300 milliseconds in the auction (especially for larger orders and orders for less liquid stocks) .”

- Auction failure: “The auction mechanism may fail to execute, in which case retail orders need to be routed to exchanges or other auctions. If this occurs, we should expect retail investors to receive worse execution quality as the market Be fully aware of auction failures and will take this (and the impact of information leaks and trades on price) into account when determining whether and at what price an order will be executed...Retail orders for less liquid stocks are expected to be received worse execution quality, as failed auctions have a greater impact on these orders.”

Citadel recognizes that front-running and failed auctions disproportionately impact large transactions and long-tail transactions. In DeFi, solver auction frontends are the most popular venue for both user profiles. In November 2023, Uniswap, Cowswap, and 1inch Fusion accounted for $3.8B in Ethereum retail long-tail token trading volume (40%, 10%, and 5% in Figure 6 ). Uniswap, Cowswap and 1inch Fusion and API front-end processing In November 2023, 75% of transactions exceeded $1 million (154, 189 and 752 transactions respectively) ( Figure 5 ).

However, today's solver auction mechanisms are unable to address these significant information deficiencies, which are particularly influential in protecting the execution quality of their core user base.

Cowswap and 1inch Fusion are designed as open limit order books, where anyone can see the token pair, direction (buy or sell), and limit price for user orders. The adverse execution effects of open limit order books on-chain are currently understudied, but the future probabilistic trading described by Citadel is very possible today.

In Uniswap If a market maker wins the exclusive fill period, all other market participants can expect trades to be executed in the next block and can preempt the market maker on both off-chain centralized exchanges and on-chain decentralized exchanges. If the winning market maker chooses not to fill or the auction fails outright, market participants will price in this information when the order is rerouted to the solver or market maker auction, or to subsequent OFA and block auctions, which may Can result in a worse offer than the one originally signed.

Existing solutions for early trades and failed auctions (also known as pre- and post-trade privacy) in Defi involve adding trusted centralized entities to maintain privacy guarantees. This is the case with the aforementioned OFA MEV-Blocker and MEV-Share and block auctions, where the privacy of searcher bundles is maintained through trust in the block builder to facilitate faithful sealed bid auctions and keep failed bundles secret forever . .

Experimentation with permissionless but centralized privacy APIs and investments in privacy infrastructure that will one day decentralize such APIs is one of the most important R&D issues in improving the quality of defi execution and maximizing the competitive potential of bid-by-buck auctions Compared to PFOF wholesale market structure.

Orderflow.art

Today we are releasing this blog post with orderflow.art , a dashboard that uses Sankey diagrams to visualize Ethereum’s order flow processing landscape. Orderflow.art supports filtering by transaction hash, so users can track which items and searchers participated in the execution of a transaction. Filtering by token pairs and entities is also possible, allowing the community to characterize and observe the origin of order flow for entities such as Flashbots Protect and Flashbots Builder.

In clarifying order flow, we seek to educate users and front-end projects about untapped price improvement and monetization opportunities in their trades, simplify the discovery and evaluation process of MEV opportunities for searchers and liquidity projects, and monitor the market as a whole. Decentralized situation.

All data provided in blog posts and dashboards, as well as their query code, are open source and can be accessed on Dune with a direct click on the embed. Sankey methods, code, and data, including project-specific processing, are documented and accessible here .

As the number of centralized off-chain MEV systems increases, trust should come with easy and clear access to the information needed to understand the properties of the mechanism and analyze the data received for the quality of execution. The details of the visualization and in-depth analysis of the off-chain solvers and order flow auctions in this work were only possible through the hard work of the CoW Protocol and 1inch Labs teams in publishing and maintaining the Cowswap, MEV-Blocker and 1inch Fusion datasets.

Meteor Shower: The Potential and Opportunities of Defi

We hold the future of defi in our hands. Don't let its small size fool you—the shooting star looks small, too. From your first trade to your last, defi shines with radiant fruit and bright clarity. Perishable, stay decentralized. Source: Blue Bottle Coffee

After clarifying and comparing the prospects of defi and tradfi, several key points emerge. Defi’s permissionless and decentralized origins create a unique order flow processing environment that has the potential to solve known tradfi market failures. Despite this opportunity, many key challenges remain to realize DeFi's true potential in achieving the goals of robustness and decentralization.

MEV Institutional Designers Want to Disrupt MEV Institutional Designers , think carefully about market conditions and how your actions and products impact that market's ability to reach its full potential.

After several careful iterations, we believe the future of permissionless and decentralized decentralized finance is bright. We urge you to join us in illuminating and building this future.

Special thanks to Phil Daian, Xinyuan Sun, Reid Yager, and the permissionless and decentralized searcher network for discussions and review.

1. Router-based deduplication method: The most common development pattern for exchange interfaces on Ethereum is to call the project’s router contract when signing a transaction on the front end. The router contract tracking the project is the best information available on the chain for estimating which frontend a user transaction originated from.

In this approach, searcher (such as market makers or sandwich) trading volumes are removed since all major searchers interact directly with the pool using their own contracts. We deduplicate volume by only counting the first on-chain entry point, so when Metamask's meta aggregator routes a $100 user order through 1inch, the $100 only counts as user volume for Metamask.

45 frontends identified: Frontends were identified by sending test transactions on well-known frontends and by the Gas used to identify router contracts in the list of top Ethereum contracts.

Estimated details:

- Pink represents Uniswap's universal router volume, which is the default value for transactions originating from the Uniswap website application and wallet. However, transactions originating from other unknown frontends can also use Uniswap's universal router, so the $900 million in transaction volume is not unique to Uniswap's official frontend. Therefore, we expect that for each front end, this number will represent an overestimation of its volume.

- Some 1inch API integrators do not have their own router; their first on-chain entry point is 1inch's aggregation router, so we refer to these sites and wallets collectively as 1inch API integrators (blue).

2. List of popular stablecoins and pegged token pairs tagged from November 2023.

3.OFA reuse:

It appears the optimal decision is to send the transaction to both order flow auctions to maximize searcher coverage and competition for higher refunds. Counter-intuitively, this removes the privacy guarantees of MEV-Blocker and MEV-Share, exposing transactions to a high risk of being caught in the middle, and ultimately leading to worse execution.

4. Sankey methodology:

Retail Transaction Volume: The breadth of traffic shows the transaction volume of successful transactions originating from the frontend on the Ethereum blockchain in November 2023. Volume is deduplicated through on-chain entry points, so when Metamask routes a $100 user order through 1inch, the $100 only counts as user volume for Metamask.

Retail Liquidity Impact: The width of the flow shows the amount of liquidity generated by successful transactions on the Ethereum blockchain in November 2023. When a solver routes trades through multiple liquidity sources, the volume after the solver is vertical is duplicated. For example, when a $100 LINK-USDC transaction is routed first through the LINK-ETH Uniswap V3 pool and then through the ETH-USDC Curve pool, $100 is counted as Uniswap V3's transaction volume and $100 is counted as Curve's Trading volume. Since the volume before the solver vertical is still deduplicated, entities with outflows > inflows can be identified as routing participants executing trades across multiple available liquidity sources.

5. Market making profit methodology:

Market makers' profits are estimated by comparing the trading price on the DEX to the Binance ETHUSDC mid-price, with T0 being the time when their trading block was proposed and the period started. The Binance ETHUSDC mid-price is calculated by dividing the ETHUSDT mid-price by the USDCUSDT mid-price.

DEX Price is calculated using the net entry and exit volumes of a range of maker wallets across major PMM venues: Uniswap X, 1inch Fusion, Cowswap, Metamask, and Hashflow.

- Get deals through top routers

- Connected to the original transfer, filtering single ETH-USDC batches from addresses in the manufacturer's wallet list.

- If the maker is the solver, the gas cost must be calculated. If a solver sells eth, the eth gas fee will be added to the amount sent. If the solver purchases eth, the gas fee for eth is subtracted from the amount received.

The Binance LINK-USDC mid-price is calculated by dividing the LINKUSDT mid-price by the USDCUSDT mid-price.