The Fed's situation has undoubtedly become more difficult.

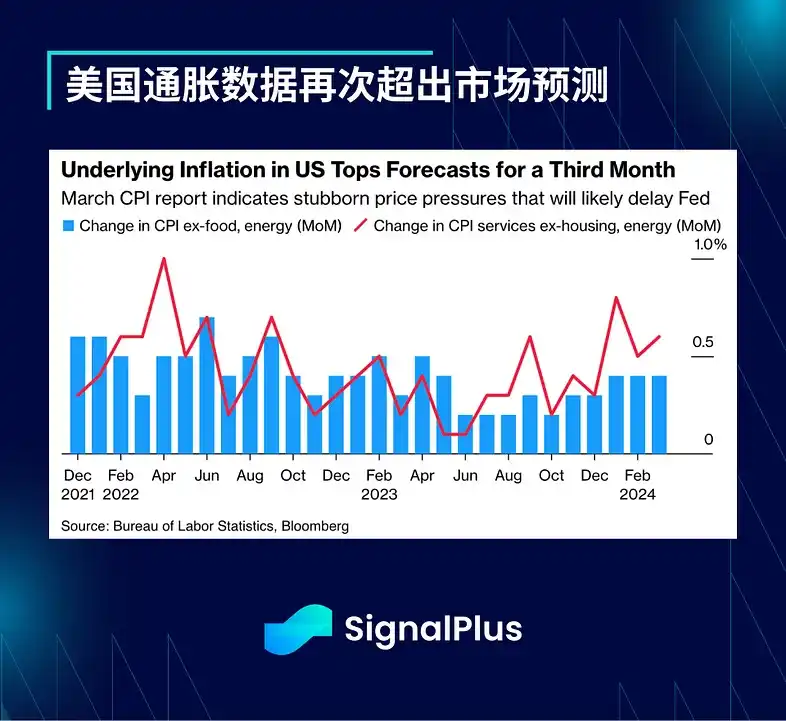

The market is facing unfriendly inflation data, especially the CPI on Wednesday. Core prices are moving in an unwelcome direction. In March, both the overall CPI and the core CPI rose by 0.4% month-on-month. The annual CPI growth rate rose to 3.5% from 3.2% last month. The annual core CPI growth rate remained at 3.8%, with energy growing by 1.1%, services growing by 0.5%, and rents growing by 0.4%. The super core CPI rose again by 0.65% month-on-month.

This is the third time in a row that the core CPI has exceeded expectations, making the "gradual slowing inflation" narrative used by the Fed to justify the three rate cuts in its dot plot almost untenable. As the market (outside of stocks) basically cast a vote of no confidence in Powell's dovish turn, the 1 y 1 y rate jumped +45bps in the past few trading days, the probability of a rate cut in June plummeted to about 22%, and the dollar rebounded against most currencies.

Fortunately for risk markets, yesterday's PPI data was relatively mild, with both headline and core PPI rising 0.2% month-on-month in March, following increases of 0.6% and 0.3% respectively in February. However, although the overall year-on-year growth rate has fallen sharply from 11.7% in March 2022, the year-on-year growth rate of 2.1% in March is still moving in the wrong direction compared to 1.6% in February, posing some challenges to the narrative of slowing inflation.

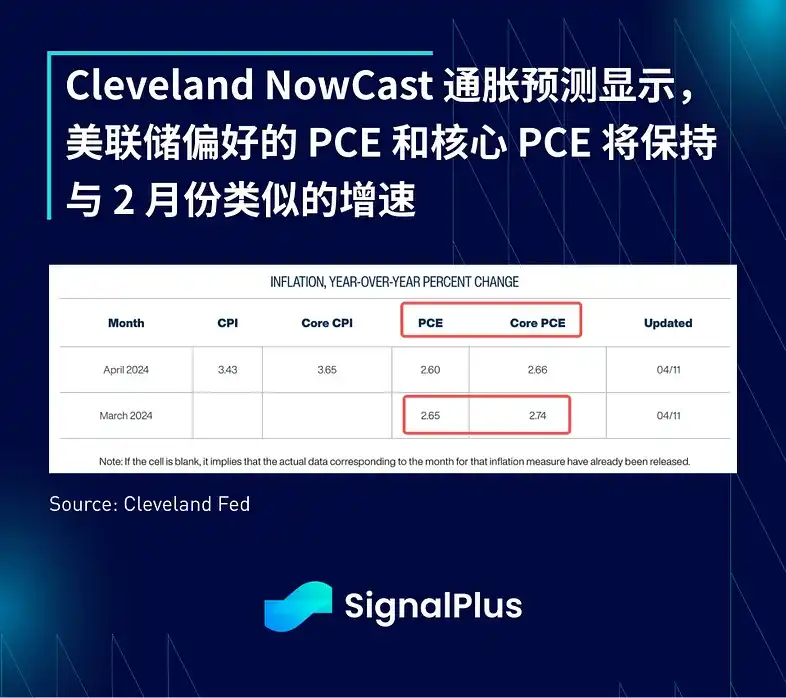

Citi and Cleveland estimate that based on the elements of CPI/PPI, the Fed's preferred core PCE indicator will increase by 0.26% month-on-month in March, similar to the growth rate in February. Due to the base effect and index composition, the annual growth rate is still expected to decline from 2.8% to 2.7%. Core services excluding housing are expected to increase by 0.29% month-on-month, while the super core CPI is expected to maintain a month-on-month increase of 0.65%.

As expected, Fed officials were busy walking back earlier comments about slowing inflation, with Boston Fed's Collins saying it "may take more time than expected" and saying "first quarter CPI was higher than I expected."

Richmond Fed’s Barkin said he wants to see more “signs of a broader slowdown in inflation, not just in goods inflation,” after super-core services inflation significantly exceeded expectations in the first quarter. Finally, New York Fed’s Williams said in a Q&A that “rate cuts don’t seem imminent,” suggesting that “there are certainly scenarios where we need higher rates, but that’s not what I think is the base case.”

The probability of a rate cut in June has fallen to 22.5%, and pricing reflects less than 2 rate cuts for the full year. In addition, considering the timing of the Fed's meetings for the rest of the year, things become more complicated.

June: Low probability of rate cut

July: No Summary of Economic Projections (less important meeting, likely to follow the same cadence as June)

September: Last meeting before elections

November: A few days after the US election

As we can see, if the Fed skips a rate cut in June (currently only 22% chance of a rate cut), they are unlikely to cut in July (32% chance), because the July meeting does not release a summary of economic projections, which is generally less important unless the data moves significantly in a favorable direction within a month. The next meeting will be in September, when the US presidential election is in full swing, and the Fed will be under great political pressure not to act too favorably towards any candidate. In addition, the base effect in the second half of this year is less friendly than in the second half of 2023, and inflation may face greater challenges. The last thing left is the November meeting, which will be held a few days after the election. Imagine how the media and conspiracy theorists will discuss if the Fed does not do anything all year, but decides to cut interest rates two days after the election (with the chance that Trump wins). There is no doubt that the Fed has been caught in a dilemma.

The bond market also expressed itself more intensely, with the 2-year yield rapidly approaching 5% and the 10-year yield also exceeding 4.50%. Wednesday's 10-year Treasury auction was very poor, with a tail of 3.1 basis points and a bid-to-cover ratio of only 2.34x. The subscription ratio of direct bids also reached the lowest level in 2.5 years at only 14.2%, while the proportion of dealers was much larger.

Yesterday's 30-year auction improved slightly, but still performed poorly, with a tail of 1 basis point, weak bid multiples and direct bid participation, and dealers were allocated 17%, higher than the average of 14%.

Bonds have been falling year-to-date, with the RSI indicator beginning to enter oversold (price) territory, but given high inflation and a troubled Fed, it is understandable that investors are less optimistic about duration risk exposure.

Despite the gloomy outlook, there is one asset class that has always managed to take it in stride and keep making a comeback. While the stock market was initially disappointed with the rate cut expectations, attention quickly returned to “good news is good news” and stock prices recovered nearly all of the losses after the data was released.

The SPX’s outperformance, which has outperformed nearly every asset class (except perhaps cryptocurrencies), has put its implied yield relative to U.S. Treasuries at its lowest level in nearly 20 years, but this has not stopped equity investors from piling into the well-performing stocks, and there are currently no signs of any systemic risk.

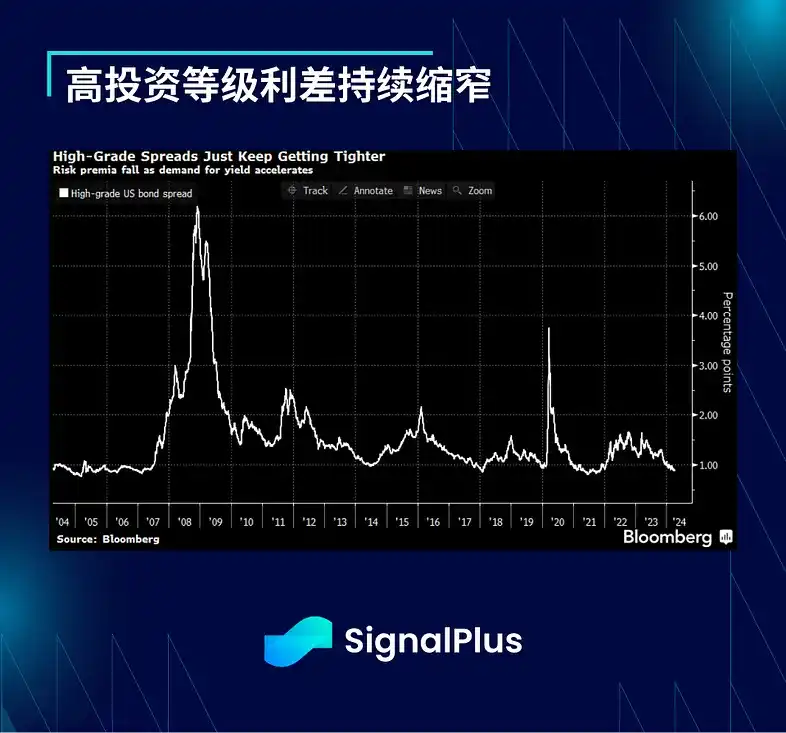

A similar phenomenon has occurred in corporate bonds, where expectations of slower quantitative tightening (slower balance sheet reduction) have led to more buying of corporate bonds, keeping high investment grade bond spreads at historic lows.

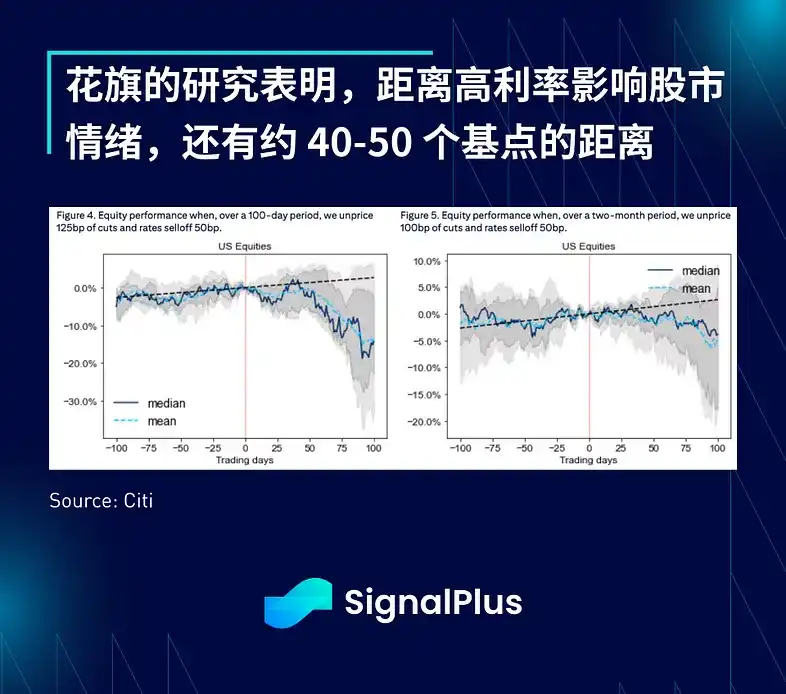

On the important question of when interest rates will impact stocks, Citigroup has done an analysis where they looked at previous “hawkish” scenarios and concluded that we are still some distance away (~40–50bps) from the current rate changes having a negative impact on the stock market. Investors also view this scenario as highly unlikely, as they are certain that the Fed will remain dovish amid strong growth and inflation, and therefore cannot imagine them completely ruling out all implied rate cuts, so investors choose to continue to focus on corporate earnings (coming soon), economic growth (strong), and friendly comments from the Fed to support continued higher stock market sentiment. As it stands, an actual rate cut is nothing more than an additional tailwind as long as the current economic trajectory remains unchanged.

In terms of cryptocurrencies, BTC prices have been hovering around 70,000, and some bulls have hedged and taken profits as major currencies have failed to break out significantly. With the arrival of the halving, ETF inflows have slowed down, and market sentiment is also relatively depressed. More consolidation is expected.

Welcome to BlockBeats the BlockBeats official community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Twitter Official Account: https://twitter.com/BlockBeatsAsia