Original: Liu Jiaolian

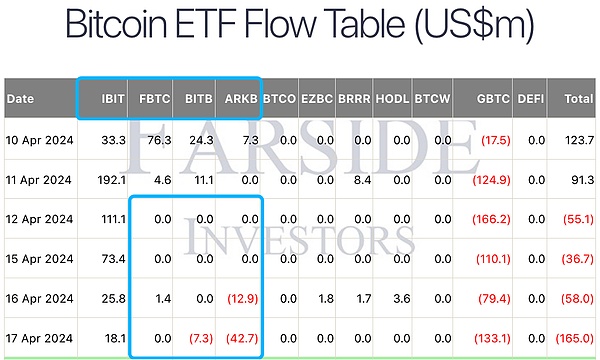

It can be said that most retail investors, even some institutions, chase the rise and sell the fall. This can be seen from the inflow data of spot Bitcoin ETF. BTC (Bitcoin) has fallen continuously in recent days. In just 10 days, it has dropped from 72k to 62k by 10,000 dollars, and once broke through the 60,000 dollar mark. With the downward trend of prices, three of the "four major" spot Bitcoin ETFs have directly stalled, and BITB and ARKB have even reversed to net outflows. Only one cylinder of this four-cylinder engine, BlackRock, is still working hard, so the power is naturally much weaker.

To be honest, the current position of around 60,000 is really safe. Going through 2025 and reaching the end of 2026, even if the "previous high" is broken as at the end of 2022 in more than two years, the lowest price will be 70,000 dollars. In other words, 70,000 dollars at the end of 2026 is equivalent to 16,000 dollars at the end of 2022. This also means that if your funds can remain unchanged for three years (both subjectively and objectively), then even if you do not carry out the so-called "escape from the top" and hold BTC until the end of 2026, you will most likely not lose money.

Know the bottom line of your position. Know that the bottom line will not cause losses. This will give you the foundation and capital to pursue higher returns. Many people blindly pursue high returns and get rich quickly because they don't understand the bottom line, and end up losing everything.

Buffett said that the most important thing in investing is not to lose money.

Zhang San and Li Si both started with a capital of 1 million. Zhang San steadily increased his capital by 40% every year. Li Si made a huge profit of 200% one year and a loss of 60% the next year, and the cycle continued. After 10 years, how big is the gap between the two?

Zhang 30 years later: 1 million x (1 + 40%)^10 = 28.92 million

Li 40 years later: 1 million x (1 + 200%)^5 x (1 - 60%)^5 = 2.49 million

Answer: The difference in their net worth is 10 times.

So what if the time is extended to 30 years? The numbers may surprise you.

Zhang San 30 years: 1 million x (1 + 40%)^30 = 24.2 billion

Li Si 30 years: 1 million x (1 + 200%)^15 x (1 - 60%)^15 = 15.4 million

Now the two of them were no longer in the same wealth class. It was meaningless to compare the difference in their net worth.

And if you compare how the two of them spent the past 10 or 30 years, you might feel even more emotional.

In the past 10 to 30 years, Zhang San has hoarded BTC and held it. He has spent time educating his children, accompanying his family, doing what he likes, traveling, maintaining his health, exercising, writing books, etc.

In the past 10 to 30 years, Li Si has: sold high and bought low, added leverage, and nervously watched the market at all times, closely followed new coins and projects, rushed into on-chain meme, took advantage of airdrops, and took advantage of the situation; his positions were liquidated, his coins were stolen, and he was PUA'd by the project parties; he had no time to pay attention to his children's studies, his spouse's relationship, or his aging parents; he had no time or mood to exercise, and his health was getting worse and worse; he was numb and no longer knew what hobbies he had besides speculating in coins, and he had no interest in doing any down-to-earth work to earn money; he kept watching the market even when he traveled, and his mind could not be cleared, and his body and mind could not relax; and so on.

My son has to read extracurricular books in primary school, so I gave him a book called "38 Letters from Rockefeller to His Son" for him to read. He reads it every day during breaks after class and shares his thoughts with me after school. Yesterday he told me that the latest article he read said that people should be the masters of money, not the slaves of money.

Yes. Investing is a personal practice. Investing is nothing more than a part of one's life. Before answering the question of what kind of investment we should make, we must first think clearly about what kind of life we want to live. Otherwise, we will forget our original intention and become slaves to money.

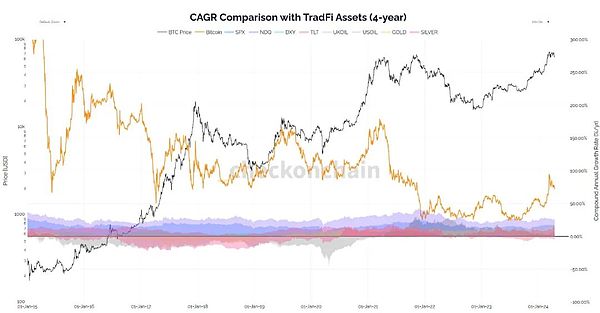

So, the technical question is, is it difficult to achieve a 40% annual return by hoarding BTC? The following chart shows the CAGR (compound annual growth rate) of Bitcoin over a 4-year period, as well as a comparison with some other traditional assets.

The orange curve in the figure is the 4-year CAGR of BTC, and the corresponding value can be seen on the right Y-axis. It can be seen that except for the two years from January 2022 to January 2024, the 4-year CAGR is between 25-50%, and the rest of the time is above 50%. Since March this year, as BTC has risen to 60,000-70,000 dollars, the 4-year CAGR has risen back to more than 72%.

However, most people make money while investing, so they will continue to increase their positions at different points in time during the four years. In this case of fixed investment, the advantage is that it will smooth out some volatility, but the disadvantage is that the actual CAGR of the position will be much lower than the CAGR of the one-time investment at the starting point. It is about half lower. In this way, if the 4-year growth of BTC is equivalent to a CAGR of 80%, then the CAGR of fixed investment can reach about 40%, which is very good.

Now, as BTC retreats, if the 4-year CAGR is equivalent to 72%, the fixed investment CAGR is about 35%.

Teaching chain real disk, in the past 6 years from 2018 to now, the eight-character formula insists on fixed investment and adding positions when the market falls, and the CAGR is about 28%. There are three reasons for the low value: First, in 2018, the investment was tentative and there was no heavy position, but it was still counted as 1 year, which lowered the value; second, the bull market in 2021 was over, and the investment was increased in the high range, resulting in top-heavy; third, the increase in funds in 2023 was restricted by objective factors, and the investment amount was low. In short, the theory is full, and the reality is very skinny. In actual operation, it is difficult to be perfect if you have to persevere subjectively for many years and objectively not drag your feet (such as not losing your job, not reducing your salary, not getting sick, and not spending a lot of money).

Many people have no idea about the compounding power of CAGR.

In 2021, Jiaolian said that it would be great if BTC could achieve a CAGR of 40% in the past two cycles. This goal is not impressive, but it is relatively possible to achieve.

Two cycles are 8 years. With a CAGR of 40% in 8 years, 1 million will become 1 million x (1 + 40%)^8 = 14.75 million.

On the other hand, if you earn 13.75 million in 8 years, that is 140,000 per month, or 1.7 million per year. With a monthly salary of 140,000 and an annual income of 1.7 million, even in first-tier cities, you can be considered a high-income group, right?

Considering that the actual operation will not be so ideal and the growth rate will certainly decline, it is better to use a CAGR of 20%. This is roughly equivalent to the level of Mr. Buffett.

8-year CAGR 20%, 1 million x (1 + 20%)^8 = 4.3 million.

This translates to a monthly salary of 34,000 yuan, or an annual income of 410,000 yuan, which is the income level of white-collar workers in first-tier cities.

Just think of it as a kind of savings. Or like paying insurance premiums every year. Saving BTC is like taking out an insurance policy for your life.

Soon, the power of compound interest will be apparent.

In addition to BTC, do you think there are other coins that have the ability to generate long-term compound interest? To be honest, I really can’t see it. “Depositing money” in those things is simply “giving away money” and “burning money”.

There is an old saying that making a little money is something anyone can do with hard work, but making big money depends on luck.

But in this market, many people are unwilling to make a few tens of millions of dollars a year, and they have to gamble their lives in an attempt to win big. If you win, you will be financially free, but if you lose, you will be heavily in debt. From the perspective of probability and the law of nature, 99.99% of people are destined not to get rich overnight.

If it is destined to be yours, you will get it eventually. If it is not destined to be yours, don’t force it. The result of forcing yourself to get rich quickly is usually not a good one.