Japan truly has many seemingly unremarkable companies that produce small components that become monopolistic products, capable of holding the global AI industry hostage.

Recently, Musashi Seimitsu (7220.T), a precision component manufacturer from Aichi Prefecture, Japan, unexpectedly rode this wave, with its stock price surging over 250% in a year, pushing its market capitalization above 490 billion yen.

Founded in 1938, Musashi has been manufacturing automotive parts for nearly 70 years and is Honda's largest supplier of transmission gears.

The real turning point came in 2020 when it acquired JM Energy, a small company specializing in hybrid supercapacitors (HSCs), for approximately 3 billion yen. Four years later, this acquisition became Musashi's most valuable asset.

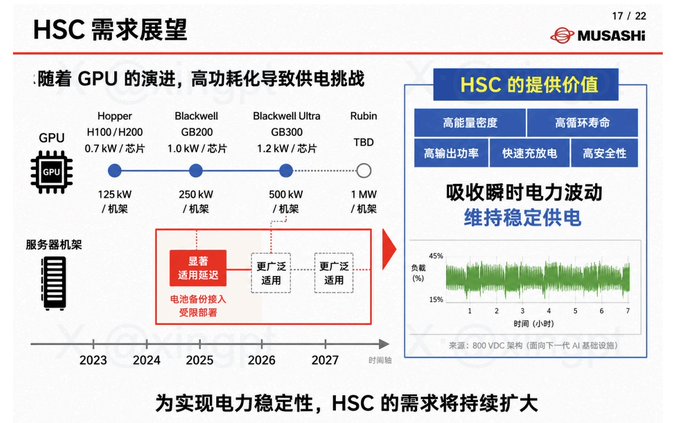

HSCs fall between traditional capacitors and lithium batteries, offering millisecond-level charge and discharge capabilities, over 1 million cycles, and inherent safety.

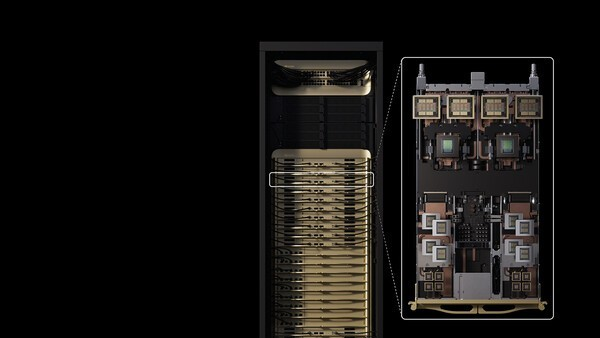

When NVIDIA's GB300 racks push single-rack power to 155kW and GPU loads fluctuate wildly, traditional batteries simply cannot keep up; HSCs become the only solution.

GB300 standard changes supercapacitors from an "optional" to a "standard" requirement, necessitating over 300 units per rack. Global demand is projected to exceed 15 million units by 2026, while Musashi's capacity is only 6.5 million units, leaving a significant gap.

Financially, HSC currently accounts for only about 3% of revenue, but management is aggressively expanding production, building a new Southern Alps plant that will increase capacity 32-fold within three years.

Analysts predict a 41% CAGR for EPS over the next three years. Short-term FY2026 profitability will remain under pressure, as traditional automotive parts sales are shrinking and depreciation at the new plant is ramping up.

If 800VDC architecture becomes the standard for next-generation data centers, this company could transform from a ¥350 billion annual revenue parts manufacturer into an indispensable part of AI infrastructure.