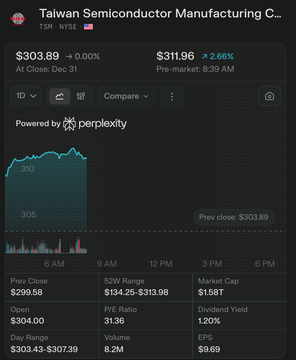

Bernstein: TSMC Is Our Top Pick'

In light of its quality, risk and undemanding valuation; With no meaningful challenger in sight, TSMC is the de facto producer of XPUs, and hence one of the primary beneficiaries of AI growth.

We project AI and TSMC’s leadership in advanced technologies broadly to propel TSMC to expand its revenue (in US$) by 23% in 2026 and 20% in 2027.

More benign FX and better cost control will also alleviate the cost burden from oversea production and we thus model TSMC’s EPS at 20% CAGR in the same period, just a tad slower than revenue CAGR."