Grayscale Research analyzes the current situation of Ethereum from various aspects and believes that the launch of spot ETF is very helpful in making the public better understand the "smart contract public chain". Although the current valuation of ETH is compared with the launch of Bitcoin ETF in January Higher (the upside potential may be limited), Grayscale is still optimistic about the prospects of both, but Grayscale also specifically named Solana, believing that SOL is the most likely to capture the Ethereum market share.

Table of contents

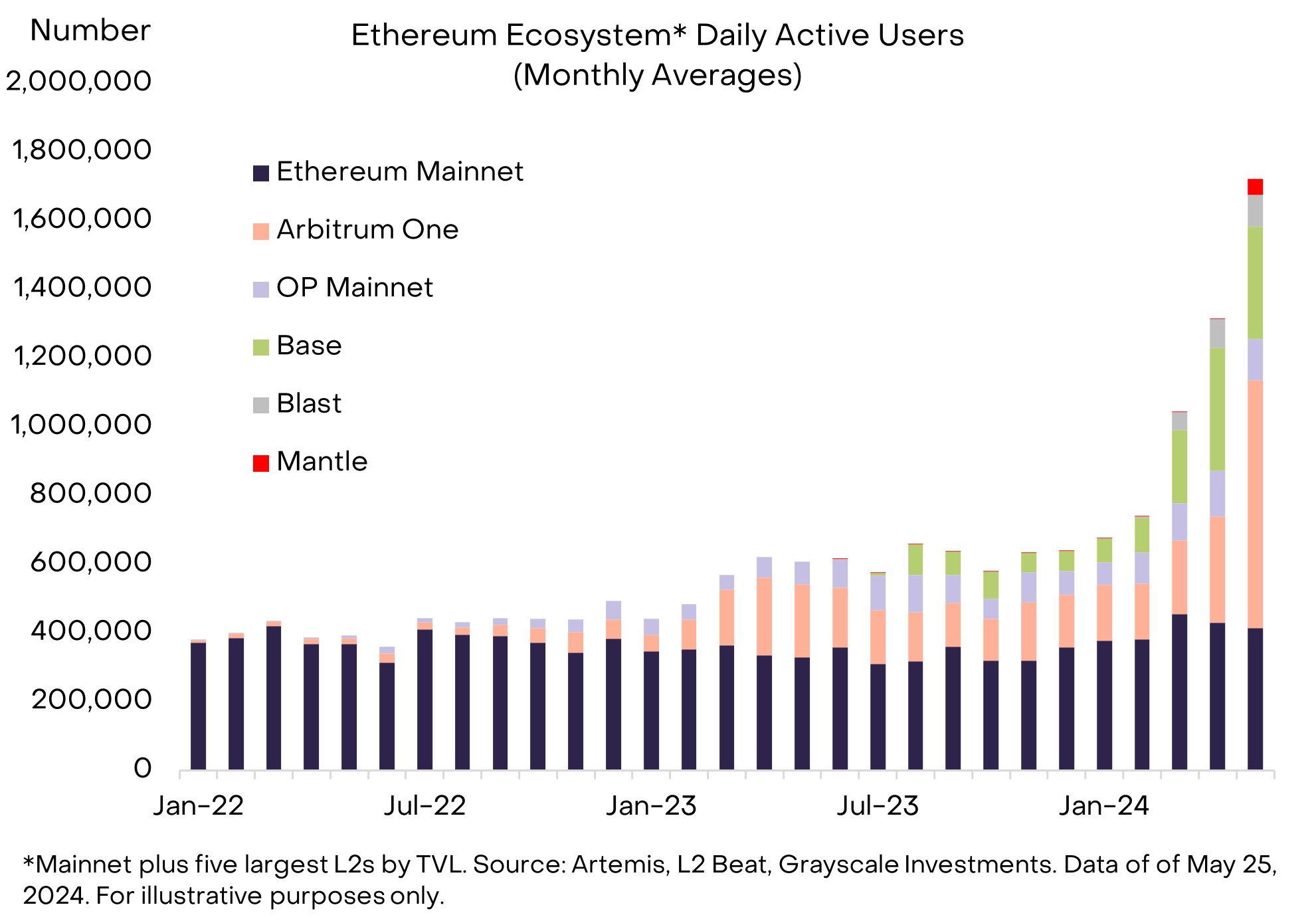

ToggleL2 active users account for 2/3 of total activity

After a major upgrade in March, Ethereum is promoting the transition to a modular network architecture. Through modular design, different types of on-chain infrastructure are designed to work together to provide end-user experience. And as time goes by, more activity is expected to occur on Ethereum L2.

L2 settles and publishes transaction records to L1, benefiting from the security and decentralization of the mainnet, which Grayscale Research points out is in sharp contrast to blockchains with a holistic design concept, such as Solana, where all key operations (execution, Settlement, consensus, and data availability) all occur on a single L1.

From an on-chain activity perspective, the upgrade was successful, with the number of active addresses on L2 increasing significantly and now accounting for approximately two-thirds of the total activity in the Ethereum ecosystem.

L2 leads to decline in Ethereum mainnet revenue

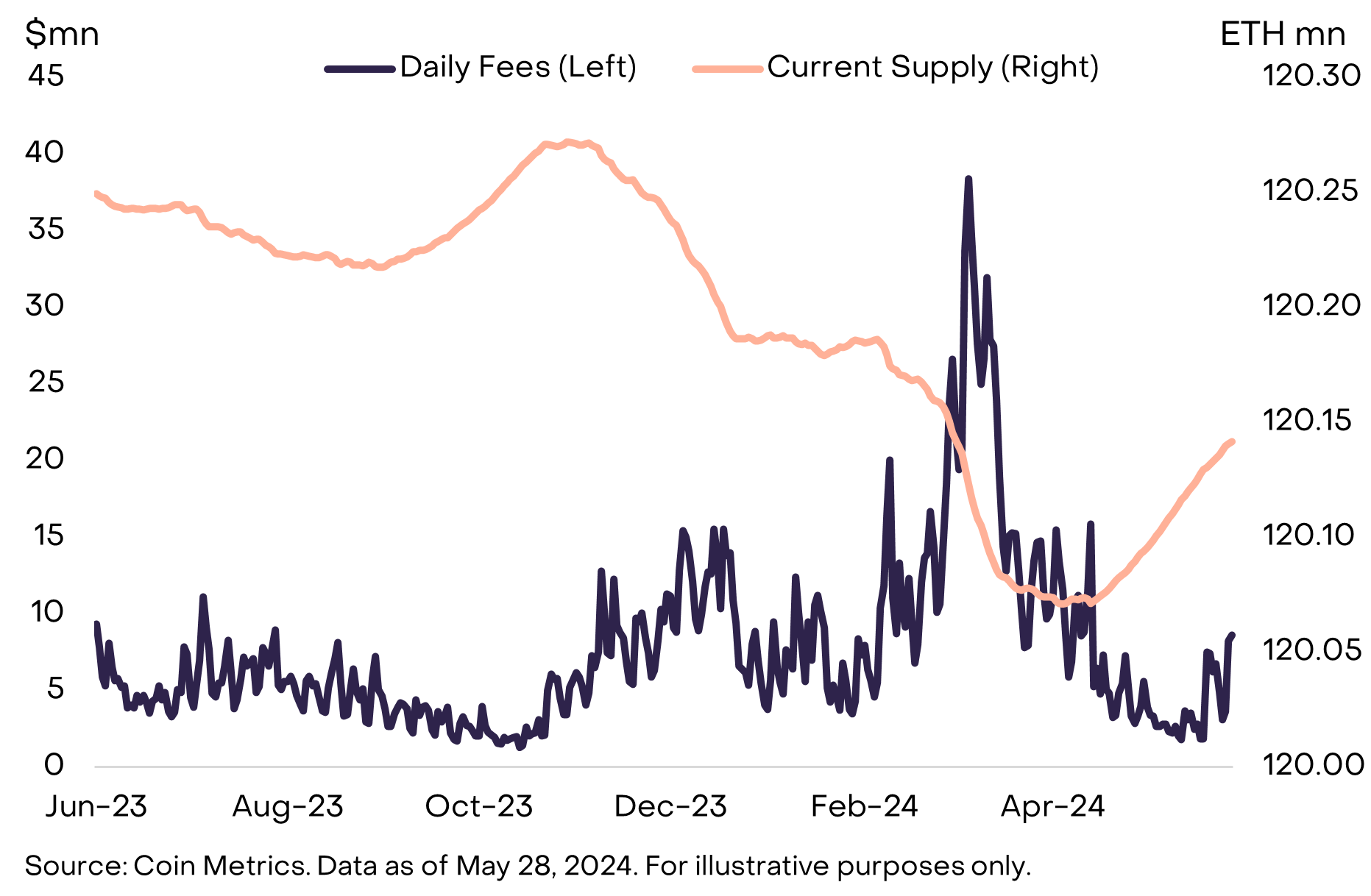

However, the shift of on-chain activity to L2 also affects Ethereum’s token economy.

When Ethereum's on-chain revenue is high, the number of tokens burned tends to exceed the rate of new coins being issued, and the total ETH supply tends to decline. However, as on-chain activity transitioned to L2, fee revenue on the Ethereum mainnet declined, and ETH supply began to increase again.

Although L2 still needs to pay a fee to publish data to L1 (so-called "blob fee" and other transaction fees), the amount is often relatively low.

( Vitalik discusses the impact of multi-dimensional Gas pricing to improve Ethereum tariff standards )

Ethereum mainnet revenue needs to increase

Grayscale Research believes that in order for ETH to rise over time, the Ethereum mainnet will likely need to see fee revenue rise. This works through:

Moderate growth in L1 activity, paying higher transaction costs,

Significant growth in L2 activity, achieved by paying lower transaction costs.

Grayscale Research predicts that both L1 and L2 on-chain activities need to continue to grow to benefit Ethereum, which may be a combination similar to L1 (low-frequency, high-value transactions) and L2 (high-frequency, low-value transactions).

Currently, about 70% of tokenized U.S. Treasury bonds are on the Ethereum chain (picture below). Relatively high-value NFTs may also remain on the Ethereum mainnet because they benefit from its high security and decentralization, and Relatively little changes hands (for similar reasons, Bitcoin NFTs are expected to continue to grow).

Ethereum Spot ETF

Ethereum spot ETF helps increase the demand and price of ETH.

Grayscale compares BTC and ETH exchange-traded products (ETPs) outside the United States. Ethereum ETP accounts for about 25%-30% of Bitcoin ETP. Therefore, it is also expected that the net inflow of Ethereum spot ETF will be Bitcoin’s since Net inflows since January are 25%-30% of US$13.7 billion.

Although ETH futures only account for about 5% of underlying BTC futures in the US market, Grayscale Research believes that this does not represent the possible relative demand for Ethereum spot ETFs.

50% of ETH supply is locked in long term

Grayscale lists that about 50% of ETH circulation is in a long-term locked state:

27%: Pledge.

11% are locked in multiple smart contracts.

6%: Not transferred for more than five years.

3%: held in the form of ETH ETP.

0.7%: held by the Ethereum Foundation, Mantle, and Golem vaults.

Grayscale Research says:

The above limits the available supply of Ethereum spot ETFs. Future net purchases of ETH will come from the remaining circulating supply, so any increase in demand may have a greater impact on the price.

Solana will capture Ethereum market share

At the end of the report, two points that are less conducive to the price of ETH are listed.

Grayscale quoted the MVRV-Z indicator, which showed that when the Bitcoin spot ETF was launched in January, its MVRV-Z score was relatively low, indicating that the valuation was moderate and there may be greater room for growth; while ETH was overvalued, and the ETF The potential for upside after approval is likely to be smaller.

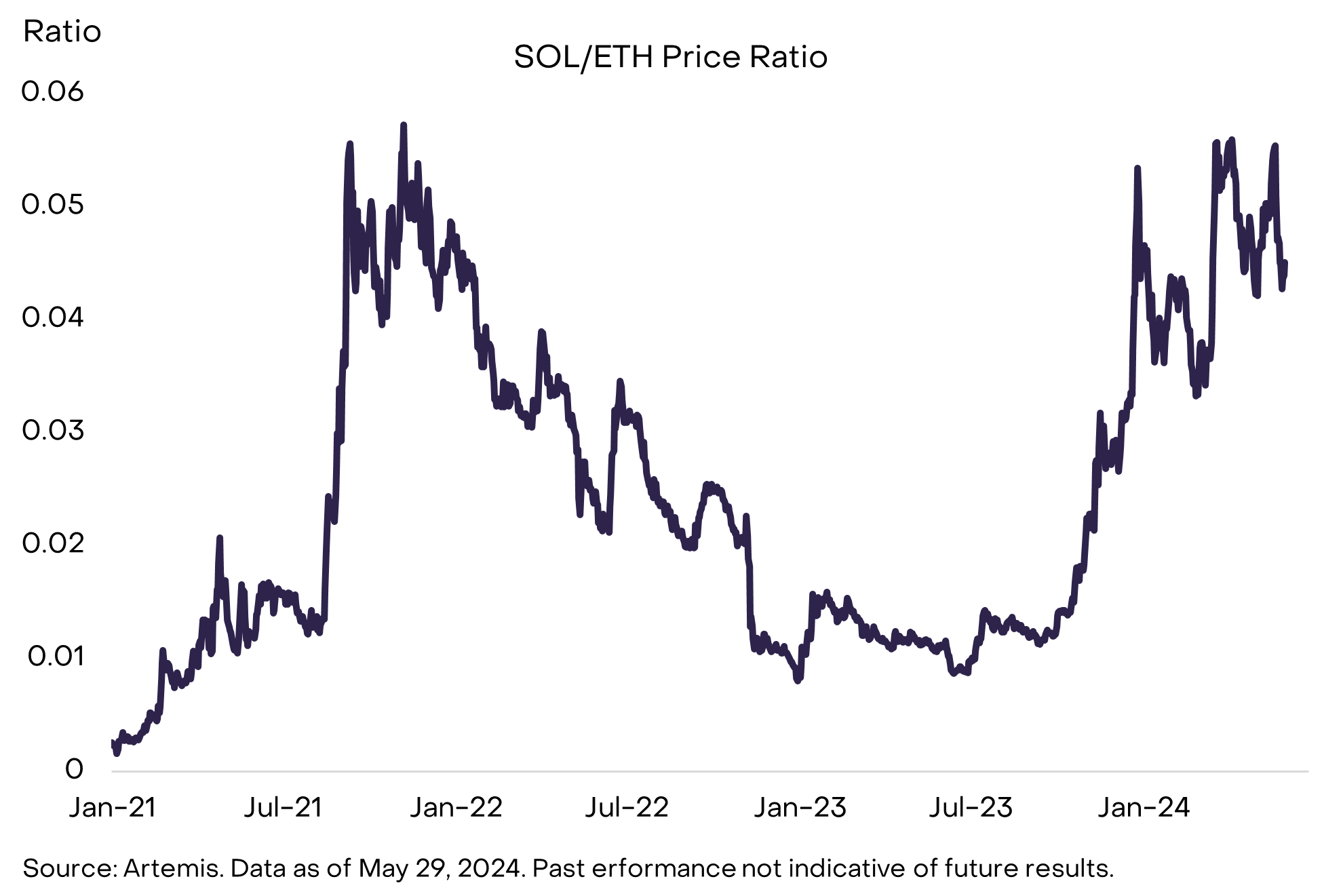

Grayscale Research finally mentioned that crypto investors may be more concerned about the competition between ETH and other smart contract public chains, especially the SOL/ETH exchange rate. Considering that Solana is the second largest project in the market, Grayscale It is believed that SOL has the best chance to capture market share from Ethereum in the long term.

Last year, SOL performed significantly better than ETH, and the SOL/ETH price ratio is now close to the previous high. In the short term, Grayscale expects the SOL/ETH exchange rate to stabilize, and the Ethereum spot ETF will support the price of ETH, but in the long term It seems that the SOL/ETH exchange rate will depend on the growth of the two’s on-chain income.