Author | Jeffery, Chief Analyst, HashKey Group

Stablecoins have always been an integral part of the cryptocurrency ecosystem.

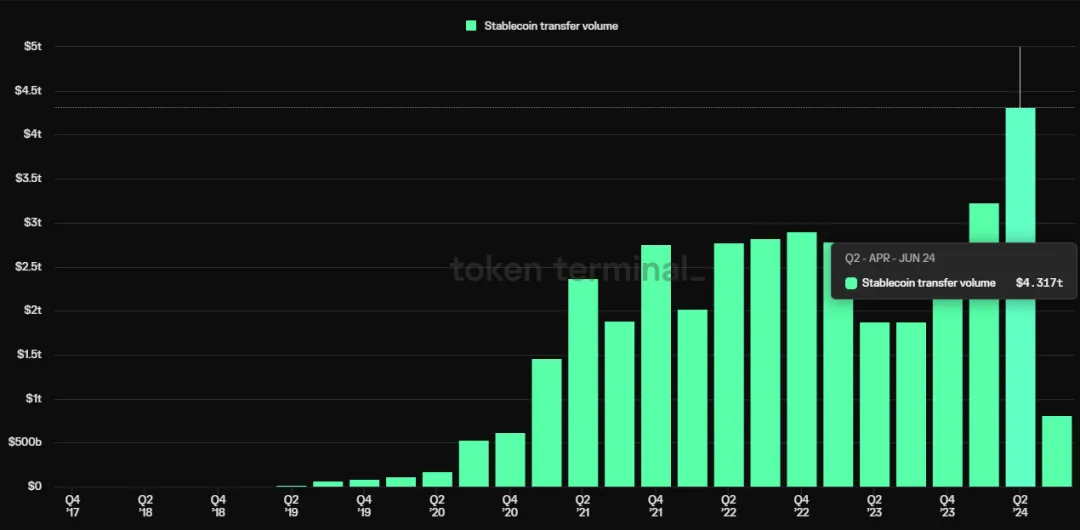

Data show that over the past four years, quarterly stablecoin transfer volume has increased seventeen times, from US$17.4 billion in the second quarter to US$4 trillion. On July 17, 2024, the total trading volume of the entire meta currency market was US$94.8 billion, and stablecoins accounted for 91.7% of the trading volume of the entire cryptocurrency market, reaching US$87 billion, of which the largest was USDT, reaching 83.3 %.

However, due to the lack of endorsement by large financial institutions, it is difficult for stable coins to become truly "stable" coins for users. The era of compliance has arrived. At present, governments in Hong Kong, Europe, Singapore, the United States and other places have begun to issue local stablecoins, and the stablecoin market structure may usher in changes. This article will discuss how the Hong Kong stablecoin market structure will be reshaped in the era of compliance, as well as the possibilities for future development.

Hong Kong will become the first region in the world to allow banks to issue stablecoins

The Hong Kong government has recently actively promoted the establishment of a stable currency regulatory system to maintain financial stability and protect consumer rights. Following the virtual asset service provider licensing system that came into effect in June last year, the Treasury Bureau and the Hong Kong Monetary Authority consulted the public on the proposed regulatory system for stablecoin issuers in Hong Kong at the end of last year, and will soon publish a consultation conclusion. We can have an overview of Hong Kong’s stablecoins. Regulatory policy orientation.

At present, it seems that Hong Kong has a strict regulatory system for fiat currency stablecoin issuers, which mainly includes reserve management and stabilization mechanisms, requiring issuers to ensure that fiat currency stablecoins are fully supported by high-quality and highly liquid reserve assets; redemption requirements; regulatory requirements.

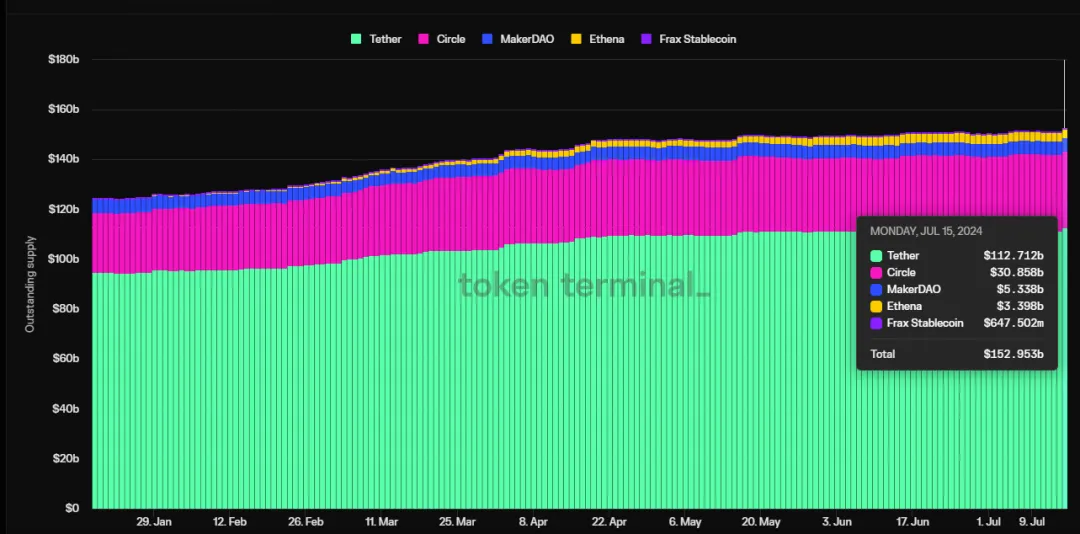

In terms of stablecoin suppliers, only licensed fiat stablecoin issuers, authorized institutions, licensed corporations and licensed virtual asset trading platforms can provide stablecoins. The issuer may involve exchanges, banks, and licensed investors such as USDT, USDC, etc.

According to the list of participants in the stablecoin issuer sandbox released by the Hong Kong Monetary Authority today, institutions participating in the sandbox include: Yuanbi Innovation Technology Co., Ltd., JD Coin Chain Technology (Hong Kong) Co., Ltd., Yuanbi Innovation Technology Ltd., and Standard Chartered Bank (Hong Kong) Limited, Ansu Group Limited, and Hong Kong Telecommunications (HKT) Limited. During the assessment process, these institutions can demonstrate their true intention and reasonable plans to develop stablecoin issuance business in Hong Kong, and that the proposed operations under the sandbox will be conducted within restrictions and with controllable risks.

Among them, in February this year, Hong Kong's largest licensed exchange Hashkey Exchange, Yuanbi Technology, and Allinpay International issued a cooperation announcement. The three parties relied on their respective business and product advantages to cooperate, including compliant and safe digital currency trading services, extensive and diversified online Under the physical merchant acceptance network, as well as advanced stable currency research and development technology.

But as for USDT and USDC, which currently have the highest adoption rates, whether they can be traded in Hong Kong in the future depends on whether they can make a successful transition. The first problem is that only issuers with physical companies in Hong Kong can apply. Secondly, if we look at the European MiCA stablecoin regulatory policy, perhaps only issuers that support placing their reserves in banks can obtain regulatory recognition in the changing situation. This part will be discussed in detail later.

On the other hand, Hong Kong may also see a "multi-faceted bloom" scenario of stablecoins. For example, banks have their own stablecoins, and exchanges have their own stablecoins. If the bank successfully launches its own stablecoin, Hong Kong will be the first place where a bank launches a stablecoin, and can also be a pioneer for other parts of the world. According to media disclosures, State Street Global, the world’s largest issuer of ETF SPY, is expressing interest in stablecoins and tokenized deposits.

Although Hong Kong's cryptocurrency ecosystem is still developing, for example, ordinary citizens cannot directly use bank money to purchase stablecoins, and there are not enough payment systems and stored value methods to cover stablecoins. In addition, in terms of accounting, there are no complete regulations to determine whether crypto assets can become part of a company's assets. In terms of licenses, you must have a physical company in Hong Kong to apply for it, so USDT and USDC have to consider more, because they need to set up a company in Hong Kong to issue. This move may deter them, and there is no such thing for the time being. Cooperation with other jurisdictions, so these issues are also worth considering later.

Enlightenment from Hong Kong’s Stablecoin Regulatory Policy and European MiCA Regulations

How Hong Kong’s stablecoin policy will move forward may provide some reference from the European stablecoin policy supervision.

At present, Europe's MiCA is very similar to Hong Kong's stablecoin regulations, even more comprehensive, and it is the most comprehensive cryptocurrency regulatory bill in Europe's history.

On April 20, the European Parliament passed MiCA, and the regulation is expected to be fully implemented in early 2025.

Starting in July 2024, the most important legislation has already been implemented, including that stablecoin issuers will be required to maintain sufficient reserves, such as at least one-third of all funds in banks, to meet large-scale withdrawal requests. In addition, transaction limit limits also need to be set.

This is a big challenge for stablecoin issuers. USDT, the US dollar stablecoin issued by Tether, the largest supplier of stablecoins, has no plans to accept the supervision of MiCA regulations in the near future because its CEO Paolo Ardoino expressed some concerns about MiCA's requirements. He believes that stablecoins should be able to convert 100% of Reserves are kept in Treasury bills, rather than placing large reserves in uninsured cash deposits, exposing themselves to the risk of bank failure and damaging their interests, but Tether said it would continue to communicate with relevant institutions to reach a consensus.

Currently, many exchanges will delist unlicensed stablecoins in Europe, and many cryptocurrency exchanges have also taken adjustment measures. For example, OKX delisted Tether's USDT for EU users in March, but continued to support Circle's USDC, a stablecoin issuer that values regulations. However, some companies such as Kraken will continue to list USDT in Europe. They express that they understand that European customers value the use of USDT, so they have no plans to delist it for the time being.

USDC, the U.S. dollar stable currency issued by Circle, may become the biggest beneficiary under the new European digital asset management regulations that will take effect in July. As the first stablecoin under MiCA regulations, its market share in Europe may soon surpass USDT to become the largest stablecoin provider in Europe.

MiCA regulations may have an impact on European users' transactions in the short term, but in the long term, the successful implementation of MiCA may inspire other jurisdictions such as Hong Kong to adopt similar regulatory measures, promoting higher standards of global market integrity and consumer safety .

This harmonization reduces regulatory arbitrage, helps create a more consistent and stable global crypto market, and facilitates cross-border trading and investment. MiCA may enhance international cooperation and standardization of digital asset regulation. Countries observing the benefits of a well-regulated EU stablecoin market may implement similar frameworks to increase the resilience and transparency of the global financial system. This shift to unified regulatory standards attracts institutional investors seeking clarity and stability, further promoting legitimacy and global growth for the crypto industry.