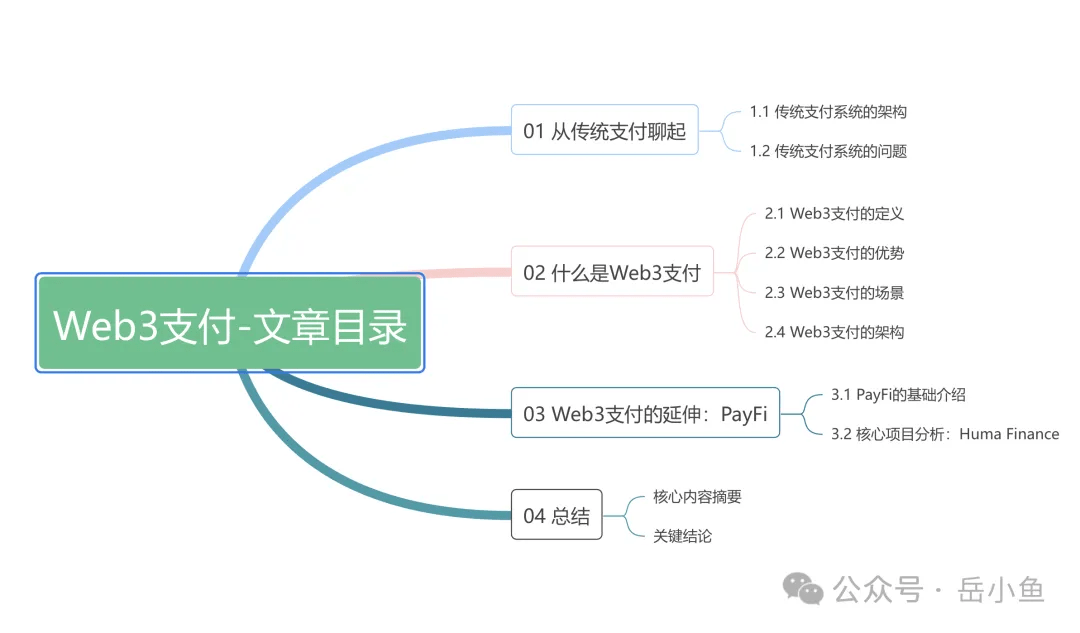

Ten thousand words long article sorting out the Web3 payment system

Author: Yue Xiaoyu

After more than a decade of development of blockchain, the market's focus has once again returned to the vision of Bitcoin when it was first created: payment.

Today, Bitcoin’s value storage properties have been widely recognized, but due to its price volatility, its transaction intermediary properties cannot yet meet payment needs well.

Payment is a high-frequency use scenario. Whether individuals or enterprises, electronic payment is indispensable in modern economic life, so the payment track is a huge market. However, the problem of payment scenarios has not been well solved. With the maturity of blockchain infrastructure and the improvement of user acceptance of blockchain, the solution to the payment problem has been put on the agenda again.

Therefore, this article will deeply analyze the Web3 payment track, starting from the traditional payment system, to the disassembly of Web3 payment, and then expanding to derivative financial services such as PayFi, so that we can fully see the panoramic view of the Web3 payment track.

01 Let’s start with traditional payment

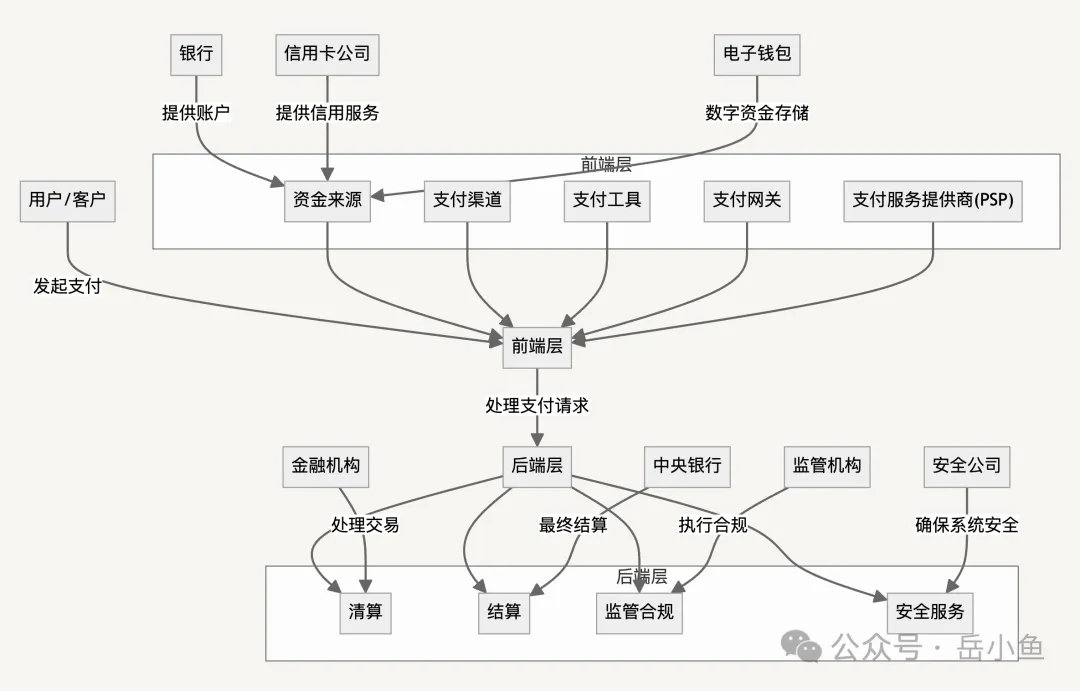

1.1 Architecture of Traditional Payment System

The overall architecture of the traditional payment system can be divided into two layers: front-end and back-end.

The front end focuses on how users initiate payments, including confirmation of the source of funds, selection of payment channels, and use of payment tools. This part focuses on user experience and security.

The back end handles the actual execution of payments, including clearing and settlement, which involves confirming the legitimacy of transactions, the actual transfer of funds, and ensuring that the entire payment process complies with the legal and financial systems.

Front-end: Processing the information flow of payment transactions

1. Source of Funding

- Concept: refers to the starting point or source of funds, which can be a personal account, corporate account, government account, etc.

- Process: Users provide funding sources through bank accounts, credit cards, e-wallets, etc., and identity verification is usually required.

- Challenge: Ensure the legitimacy of the source of funds and prevent fund laundering or illegal activities.

- Role:

- Bank: Provide a bank account as a source of funds.

- Credit card companies (such as Visa, Mastercard): provide credit payment solutions.

- E-wallet services (such as PayPal, Alipay): act as custodian of user funds and payment intermediary.

2. Service channels for initiating payment

- Concept: This is the way for users or merchants to initiate payments, such as bank online payment systems, mobile application POS terminals, etc.

- Process: The user selects a payment method and initiates a payment request through a specific channel (such as a bank app, payment platform website, etc.).

- Challenge: Provide secure and convenient payment channels while addressing technical security risks such as DDoS attacks and data leaks.

- Role:

- Fintech companies: Develop payment applications or online payment platforms.

- Bank: Provides online banking and mobile banking services.

- Retailers: Offer POS or online payment options in physical stores.

3. Payment Instruments

- Concept: Specific payment methods or tools, such as credit cards, debit cards, e-wallets, Alipay, WeChat Pay, etc.

- Process: The user selects a payment tool and enters payment details (such as card number, password, payment amount, etc.).

- Challenges: Ensure the security and user experience of payment tools, and deal with compatibility and fee differences between different payment tools.

- Role:

- Payment networks (such as Visa, Mastercard, UnionPay): provide payment card services and networks.

- Mobile payment providers (such as Apple Pay, Google Pay): provide mobile payment services.

4. Payment Gateway

- Concept: In e-commerce, a payment gateway is responsible for encrypting and transmitting payment data from merchants to payment processors.

- How it works: The user enters payment information on the merchant's website or app, and the payment gateway receives and encrypts the information and transmits it securely to the payment processing company.

- Challenge: Protect the security of payment data and ensure that payment information is not tampered with or stolen during transmission.

- Role:

- Payment gateway service providers (such as Stripe, Square).

5. Payment Service Provider (PSP)

- Concept: Provide access to multiple payment methods for companies that process online payments.

- Process: PSP interfaces with multiple payment methods (such as credit cards, e-wallets, bank transfers, etc.) to process payment transactions between merchants and customers.

- Challenge: Integrate the technical differences of different payment methods to ensure high efficiency and low risk of payment.

- Role:

- Payment service providers (e.g. Adyen, Worldpay).

Backend: Processing the flow of funds for payment transactions

1. Clearing

- Concept: Clearing refers to the transmission, confirmation and reconciliation of payment instructions (transaction information). The clearing process usually involves confirming the validity of transactions, checking account balances, processing returns or cancellations, etc.

- Process: The payment request is sent to the clearing system, which verifies the transaction and then reconciles the transaction to ensure that the account information of both parties is correct and the transaction is legal.

- Challenge: The clearing system needs to be efficient, reliable, and handle a large number of transactions while complying with various payment protocols and international standards.

- Role:

- Payment processing companies (e.g. Fiserv, First Data): handle the clearing of payment transactions.

- Clearing houses (such as CHIPS, Fedwire): handle the clearing of large transactions.

- Networks (such as SWIFT): used for the transmission of international interbank payment information.

2. Settlement

- Concept: Settlement is the actual process of fund transfer, which completes the fund delivery between the two parties of the transaction and releases the payment obligations between the two parties.

- Process: Based on the clearing results, the systems between banks or payment institutions execute the actual fund transfer, which may involve the exchange of different currencies, cross-border payments, etc.

- Challenges: The settlement process needs to consider factors such as time (such as T+1 settlement), fees, and cross-border regulatory differences to ensure that funds reach the other party's account safely and in a timely manner.

- Role:

- Central banks (such as the Federal Reserve): Responsible for final financial settlement at the national level.

- Commercial banks: perform internal settlements among their customers and participate in central bank or interbank settlement systems.

- The Bank for International Settlements (BIS) and cross-border payment networks such as SWIFT: handle the settlement of cross-border payments.

3. Regulatory bodies

- Concept: Supervise the legitimacy and stability of the payment system.

- Process: Formulate and enforce financial regulations, oversee the operation of payment systems, deal with violations, and protect the safety of consumers and markets.

- Challenge: Maintaining regulatory effectiveness without compromising innovation and efficiency in the payment system.

- Role:

- Financial regulators (such as the OCC in the US, the FCA in the UK).

4. Compliance and Security Services

- Concept: Ensure payment systems comply with legal requirements and security standards.

- Process: Provide compliance consulting, security audits, risk management and other services to help payment systems comply with regulations and security standards.

- Challenge: Provide timely compliance and security solutions in response to the ever-changing legal environment and technological threats.

- Role:

- Compliance consulting firms: Help payment companies understand and comply with relevant regulations.

- Security audit firms: Assess the security of payment systems to identify and fix vulnerabilities.

1.2 Problems with Traditional Payment Systems

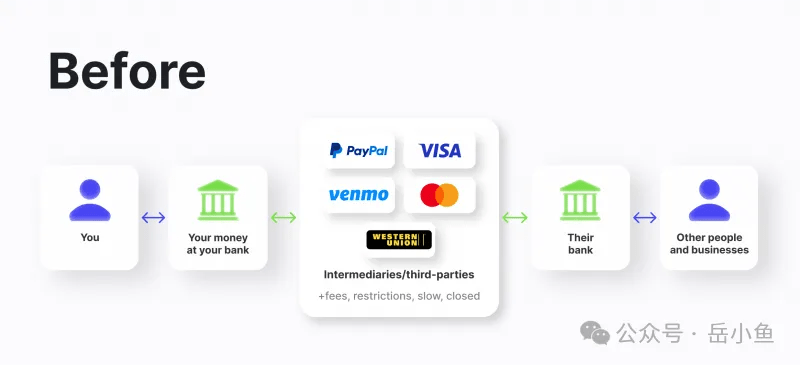

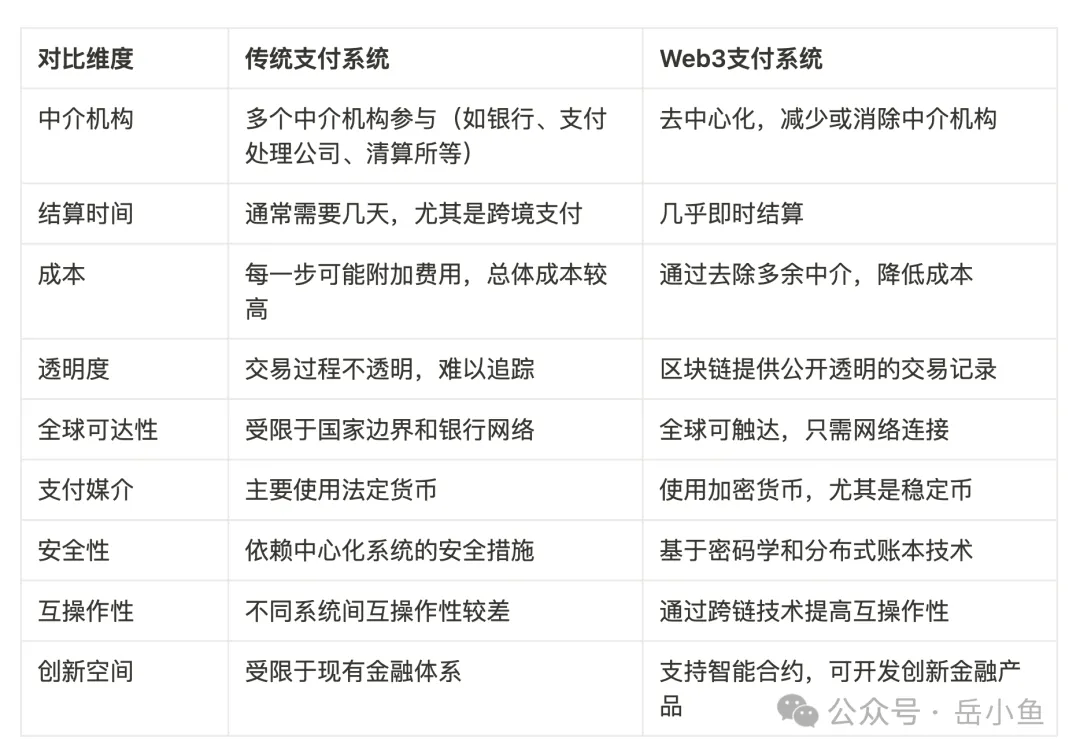

From the perspective of the architecture of traditional payment systems, there are many participants overall, and users only perceive various payment channels. However, the system behind it is very complicated and involves a long process of cash flow processing. Especially in cross-border payment scenarios, the financial and time costs will be very high.

1. Multiple intermediaries: Each intermediary may add a layer of fees and time delays, which not only reduces efficiency but also brings the risk of information transmission errors. Intermediaries exist to provide security, credit checks and compliance, but this also leads to redundancy in the system.

2. Lack of standardized processes and formats: Different payment systems and countries have their own standards and data formats, which makes cross-system operations difficult and increases the complexity of international payments. This also limits the interoperability of payment systems and hinders the process of global financial integration.

3. Manual closed processing: Processes that rely on manual input and confirmation are not only slow but also prone to errors, reducing the reliability of the payment system. Lack of integration with the latest technologies (such as AI) makes it impossible to achieve optimization and predictive maintenance of payment processes.

4. Lack of transparency: Every step of a transaction may not be fully understood by the user or merchant, which can erode trust, especially in cross-border payments when funds are transferred between different systems. Lack of transparency also makes it more difficult to track payment progress and resolve disputes.

5. High costs and long settlement cycles: The high costs of cross-border payments and the long settlement cycles of several days are not conducive to small-amount high-frequency transactions, especially affecting small and medium-sized enterprises and individuals. Cross-border payments usually take up to 5 working days to settle, with an average fee of 6.25%.

02 What is Web3 Payment

2.1 Definition of Web3 Payment

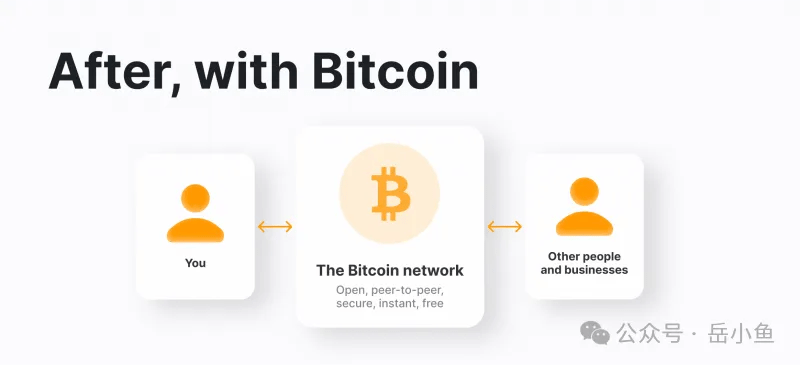

Web3 payment refers to a system that uses blockchain technology and smart contracts to process payment transactions, aiming to build a decentralized, transparent and user-autonomous payment network. Unlike traditional payment systems, Web3 payment does not rely on central banks or financial institutions as intermediaries, but uses peer-to-peer networks to directly transfer funds.

The operation of Web3 payment relies on the following technical modules:

1. Blockchain as payment infrastructure:

- Concept: All transactions are recorded in a distributed, transparent and tamper-proof ledger. Blockchain provides the underlying technical support for payment, including account management, transaction verification and recording.

- Process: The user initiates payment through the wallet on the blockchain network. The transaction is broadcast to the network, added to the block after verification, and finally confirmed by all participating nodes.

2. Decentralization and ownership confirmation:

- Concept: The Web3 payment system operates through a decentralized network, users have direct control over their assets, and payment transactions do not rely on any centralized institution.

- Process: Users sign transactions with their private keys to ensure the authorization and security of transactions. The payment process does not go through a centralized processing agency, but rather confirms transactions through network consensus.

3. Smart Contracts:

- Concept: A smart contract is a pre-set code stored on the blockchain that automatically executes transaction or payment conditions.

- Process: When payment conditions are met (for example, payment at a specific time or payment after a specific commodity transaction), the smart contract automatically executes the fund transfer without human intervention.

4. Cross-chain payments and interoperability:

- Concept: Due to the existence of multiple blockchain networks, Web3 payments may involve cross-chain technology to ensure the transfer of assets between different blockchains.

- Process: Through cross-chain bridges or interoperability protocols, users can transfer assets between different blockchains, thereby achieving a wider payment network.

5. Deposit and Withdrawal Services:

- Concept: In order to connect real-world fiat currencies with cryptocurrency payment systems, Web3 payment systems usually include fiat currency deposit and withdrawal services.

- Process: Users exchange fiat currency into cryptocurrencies (deposit) or cryptocurrencies back into fiat currency (withdrawal) through an exchange or payment gateway.

6. Payment and asset transfer:

- Concept: Once funds are converted into crypto assets, users can use them to purchase goods, pay for services, or invest in assets.

- Process: Payments can be direct peer-to-peer transactions, or more complex financial operations such as lending, staking, or generating stablecoins can be performed through DeFi protocols.

2.2 Advantages of Web3 Payment

1. Instant Settlement

- Traditional payment systems, especially cross-border payments, can take days to settle due to the need to go through multiple intermediaries, clearing systems, and comply with financial regulations in various countries.

- Web3 payments, leveraging blockchain technology, allow for nearly instant settlement because once a transaction is added to the blockchain and verified, the funds transfer is complete.

- Instant settlement not only improves the liquidity of funds, but also greatly reduces counterparty risk because there is no need to wait for changes in financial conditions that may occur during the settlement period.

2. Reduce costs

- Each step in the traditional payment system may have additional fees, including bank fees, cross-remittance fees, currency exchange fees, etc.

- Web3 payments reduce these additional costs by removing redundant intermediaries. Smart contracts automatically execute transactions, further saving on manual and administrative costs.

- For merchants, reduced transaction costs can translate into lower prices for goods or services, thereby attracting more consumers. For individual users, cross-border transfers are no longer an expensive option.

3. Openness and transparency

- The essence of blockchain is a public distributed ledger where all transactions are transparent and verifiable. This increases trust because anyone can view the transaction history, but at the same time, through encryption technology, the user's true identity can remain anonymous.

- This transparency promotes trust in the payment system, especially when audits or dispute resolution are needed. Transparency also provides the possibility for regulation, although a balance needs to be found between privacy and transparency.

4. Global reach

- Web3 payment systems are not limited by national borders or banking networks. This means that anyone anywhere with an internet connection can make payments or receive funds, without the need for a bank account.

- For developing countries or areas where banking services are not widely available, Web3 payments provide opportunities for financial inclusion. People can participate in global economic activities without being constrained by local banking infrastructure. This is particularly valuable for freelancers, multinational businesses, and aid organizations.

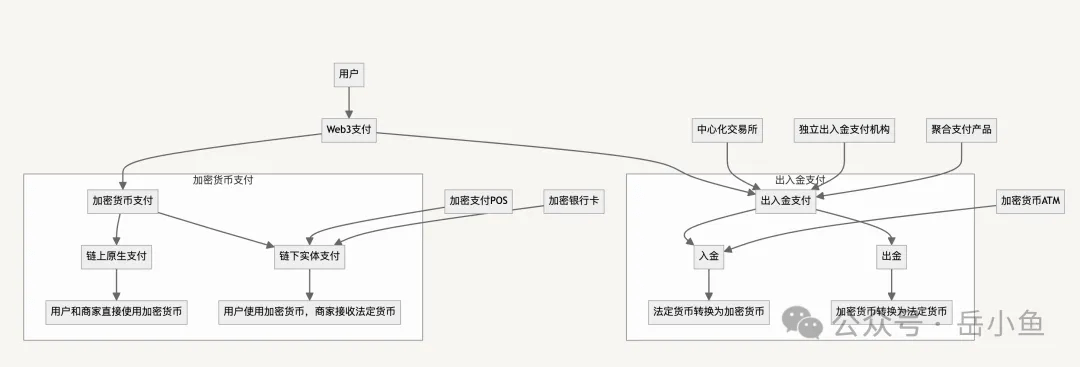

2.3 Web3 Payment Scenarios

Web3 payments can be divided into two major scenarios: deposit and withdrawal payments and cryptocurrency payments.

Deposit and withdrawal payment solves the problem of conversion between cryptocurrency and legal tender, while cryptocurrency payment further explores its application in commercial transactions. These two aspects jointly promote the transformation of cryptocurrency from an investment tool to a daily payment method.

1. Deposit and Withdrawal (On Ramp & Off Ramp)

Deposit and Withdrawal Payment Process

- On Ramp: The process of converting fiat currency into cryptocurrency. Here, third-party payment institutions and liquidity providers play a key role. Users pay fiat currency to these providers, and the providers send the corresponding cryptocurrency to the user's encrypted address through the blockchain. These liquidity providers are usually large centralized exchanges or stablecoin issuers.

- Off Ramp: The reverse process, where users exchange cryptocurrencies back to fiat currencies. In this process, payment institutions convert cryptocurrencies into fiat currencies and pay them to merchants or users.

Main deposit and withdrawal payment methods

- Centralized exchanges: Directly provide deposit and withdrawal services, and users can use bank cards or transfers to purchase cryptocurrencies. However, in strictly regulated areas, they need to cooperate with independent payment institutions such as MoonPay or Paypal.

- Independent deposit and withdrawal payment institutions: such as MoonPay, which provides multiple payment methods to enter the crypto market and simplifies the process of users purchasing cryptocurrencies. Paypal has entered this field by launching the PYUSD stablecoin.

- Aggregate payment products: such as MetaMask, which integrates multiple payment methods to provide convenience for users.

- Cryptocurrency ATM: Allows users to purchase cryptocurrencies with cash and is an important method of offline payment.

2. Cryptocurrency Payment

Payment for native scenarios on the chain

- Definition: Cryptocurrency transactions conducted directly on the blockchain, with both users and merchants using cryptocurrencies. This requires payment institutions to solve trust issues and integrate with existing blockchain settlement systems to ensure transaction security and confirmation. Similar to e-commerce shopping, a third-party payment platform is required to guarantee payment.

Payments with off-chain traditional entities

- Definition: Users pay with cryptocurrency, but merchants ultimately receive fiat currency. In this process, third-party payment institutions are crucial, as they are responsible for converting cryptocurrency into fiat currency.

- Crypto bank cards: This is an important tool to promote the daily use of cryptocurrencies. Through cooperation with traditional card organizations, such as Visa or Mastercard, users can hold cryptocurrencies and actually pay with legal currency when spending. This approach not only improves convenience, but also enhances the practicality of cryptocurrencies.

- Crypto Payment POS: Allows merchants to accept cryptocurrencies and pay with fiat currency, helping to realize the offline use of cryptocurrencies.

- Merchant acceptance: Data from 2022 shows that up to 85% of large retailers have begun to accept cryptocurrency payments, mainly through platforms such as PayPal and Venmo. Although these platforms are not crypto-native, they provide convenience for merchants to accept cryptocurrencies.

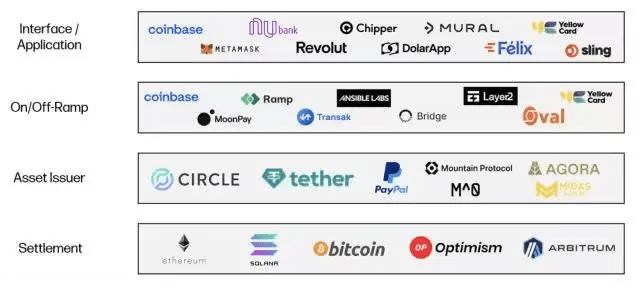

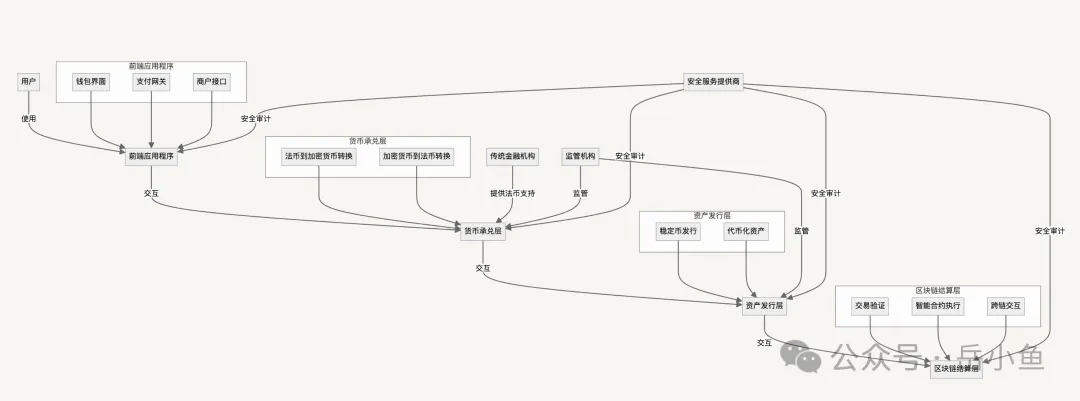

2.4 Web3 Payment Architecture

The technical architecture of Web3 payment is a multi-layer system, from the front-end that interacts directly with users, to the middle layer that handles the exchange of fiat currency and crypto assets, to the issuance and management of assets, and finally to the bottom layer for final settlement on the blockchain.

1. Front-end application

- Definition: The front-end application is the main interface for users to interact with the Web3 payment system. It needs to provide an intuitive user experience that makes it simple and easy to operate crypto assets and payments.

- Business Model:

- Platform Fee: A service fee charged to users, which may be part of the transaction fee or a subscription model.

- Traffic fee: the fee paid by the payment channel to obtain user traffic.

- Technical points:

- Security: Front-end applications need to strengthen security measures, such as two-factor authentication (2FA), biometrics, etc., to protect users’ assets.

- Compatibility: Multiple wallet formats and blockchain standards are needed to provide wider service coverage.

- Typical projects: Metamask, Trust Wallet, Phantom, etc.

2. Currency Acceptance (Deposit and Withdrawal)

- Definition: This layer is responsible for the conversion between fiat currency and cryptocurrency and is the bridge of the Web3 payment system.

- Business Model:

- Trading Commission: A fee charged on each conversion, which may be a fixed fee or a percentage of the transaction amount.

- Technical points:

- Compliance: Need to comply with KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations in various countries.

- Liquidity management: ensuring sufficient liquidity to process transactions while managing exchange rate risks between different currencies.

- Typical projects: MoonPay, Ramp, Transak, etc.

3. Asset Issuer

- Definition: These entities issue and manage digital assets, such as stablecoins, which are used as a medium of payment in Web3 payments.

- Business Model:

- Interest rate spread income: Earn income by investing in safe assets such as government bonds. At the same time, the issued stablecoin serves as a liability, and the interest rate spread becomes the main source of income.

- Technical points:

- Transparency and Auditing: Regularly publish audit reports of reserves to maintain user trust.

- Stabilization mechanism: Use algorithms or collateral to maintain the stability of the currency value.

- Typical projects: Circle, Tether, PayPal, etc.

4. Blockchain Settlement Layer

- Definition: This is the underlying technology for payment settlement, ensuring the final consistency and immutability of transactions.

- Business Model:

- Selling block space: Profits are made through network transaction fees (Gas Fees) or other forms of block rewards, mainly by selling block space to the market.

- Technical points:

- Scalability solutions: such as Layer 2 technology (Optimistic Rollups, ZK-Rollups), sharding, etc., to improve transaction processing capabilities.

- Cross-chain interoperability: enabling the exchange of assets and information between different blockchains, such as Polkadot and Cosmos technologies.

- Typical projects: Bitcoin, Ethereum, Solana and other blockchains.

03 Extension of Web3 Payment: PayFi

3.1 Basic Introduction of PayFi

PayFi, or Payment Finance, is a new narrative proposed by the Solana Foundation. The core of PayFi is to create a new financial market around the time value of money.

Money has a time value. This is a fundamental concept in economics and finance that refers to the fact that a unit of money today is worth more than the same unit of money in the future. This is because money today can be invested and earn a return, generating appreciation. In addition, there is the factor of inflation, which makes the purchasing power of money decrease over time.

PayFi obtains the time value of money mainly through three aspects:

- Instant Settlement: In traditional financial markets, settlement may take several days, but blockchain technology can achieve almost instant transaction settlement, immediately releasing the value of funds.

- Liquidity and instant asset utilization: By tokenizing physical assets (such as real estate), PayFi can make the value of these assets more flexibly utilized and traded in financial markets, reducing the value loss caused by the time it takes to liquidate assets.

- Innovative financial products: Based on smart contracts, PayFi can automatically execute financial contracts involving time value, such as instant loans, payment financing, etc., which are based on the calculation and utilization of the present value of future cash flows.

To sum up, PayFi is a fintech solution that combines payment, DeFi (decentralized finance) and RWA (Real World Assets).

The development from the basic function of Web3 payment to PayFi can be seen as an expansion and deepening of the application scenarios of Web3 payment. PayFi not only handles payments, but also handles payment-related financial derivative services, such as instant loans, supply chain financing, etc.

PayFi is built on Web3 payment technology, especially the smart contract function of blockchain, which enables seamless integration of payments and more complex financial operations. PayFi integrates the infrastructure of Web3 payments to build a broader financial ecosystem. This includes payment, financing, asset custody, and docking with real-world assets.

PayFi currently has the following three application scenarios:

- Cross-border payments and international settlements: PayFi uses blockchain technology to achieve instant, low-cost cross-border payments, solving the problems of long settlement time and high costs in traditional payment systems. Paypal launched the PYUSD stablecoin to meet the needs of cross-border payments.

- Supply Chain Finance and Payment Financing: By tokenizing real-world assets (RWA), PayFi provides a new channel for financing in the supply chain. For example, Huma Finance’s work in the field of payment financing allows companies to obtain instant loans by pledging RWA for short-term capital turnover.

- Consumer finance: Provide more immediate and personalized loan services by using consumers’ on-chain activities and assets as part of credit assessment. Through DeFi platforms, users can use their crypto assets as collateral to quickly obtain consumer loans.

3.2 Core Project Analysis: Huma Finance

3.2.1 Basic Introduction

Huma Finance is a typical representative of the PayFi track.

Huma Finance was established to address liquidity issues in the global payment system, especially in the areas of cross-border payments and trade finance. As globalization accelerates, the inefficiency, high costs and reliance on prepaid capital of the traditional payment system have become a bottleneck for business development.

In 2024, Huma Finance merged with Arf to jointly focus on the tokenization of real world assets (RWA). Huma Finance recently received $38 million in investment to expand its RWA-based PayFi platform.

Huma Finance has launched a payment financing network called PayFi, a combined payment and financing service that leverages blockchain technology, specifically the stablecoin USDC, to enable instant payments and financing services.

It mainly provides more efficient and lower-cost financial solutions for companies, especially small and medium-sized enterprises, that require cross-border payments and quick financing.

Huma Finance v1 is an unsecured lending platform for businesses and individuals that focuses on the borrower's future potential income - that is, when a borrower borrows money, it mainly examines the borrower's future income cash flow.

HumaV2 has added a credit line for secured accounts receivable to attract institutional investors. Accounts receivable are customer bonds generated by the sale of goods or provision of services during the business operation, representing the company's future cash flow income.

3.2.2 Project Value

Huma provides three main values:

- Providing a wider range of collateral options: Huma Finance has introduced the tokenization of real world assets (RWA) through its PayFi network, which means that businesses and individuals can use multiple types of assets as collateral for financing.

- Future revenue converted into loanable amounts: Revenue and earnings are the most important factors in underwriting because they are highly predictive of repayment ability. Huma Finance’s platform allows future revenue streams (such as accounts receivable) to be used as a loanable asset. Instead of waiting for customers to pay, companies can immediately convert future revenue into cash for operations, expansion or investment, which solves the problem of intermittent cash flow.

- A full-process solution from financing to payment: from loan application, asset evaluation, funding to final payment, all completed within the same ecosystem. This reduces the complexity and cost of transactions. The use of blockchain and smart contracts allows the entire process from financing to payment to proceed faster without the involvement of intermediaries, reducing time and improving efficiency.

3.2.3 Operational Mechanism

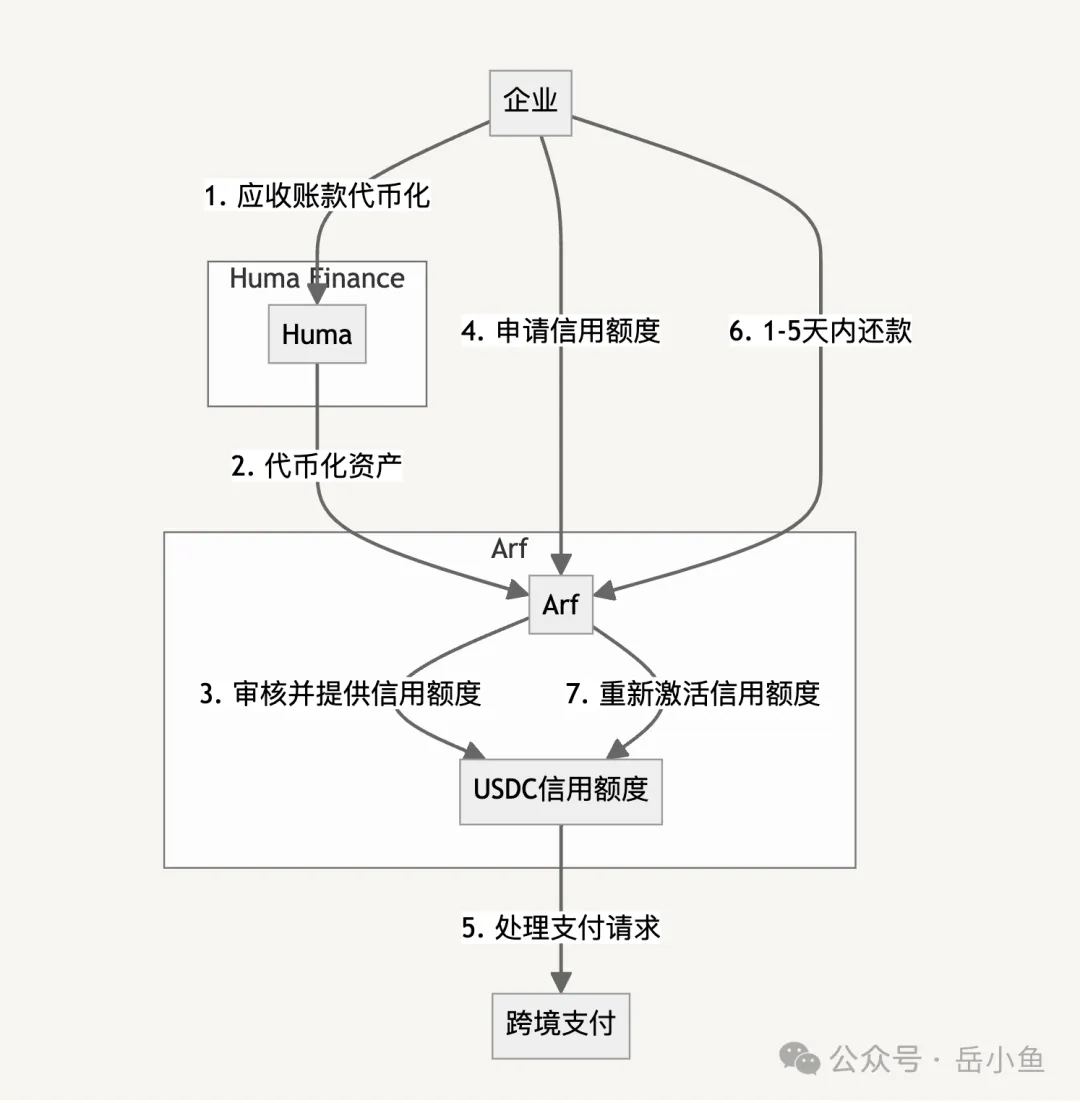

After the merger of Huma Finance and Arf, Huma is responsible for users' deposits, and Arf is responsible for lending to the Web2 world + collecting interest, forming a sustainable cycle.

By combining Huma’s RWA tokenization technology with Arf’s liquidity solution, they have created a cross-border payment system that is fully transparent and traceable on the blockchain.

Through Huma, customers can choose to use their soon-to-be-due receivables as collateral. Huma tokenizes these receivables through its protocol, and these tokens are used as collateral on Arf’s platform, allowing customers to borrow from Arf’s lending pool and obtain a USDC credit line.

The overall process is as follows:

- Asset tokenization: Through Huma’s technology, companies tokenize assets such as accounts receivable. These tokens can not only be used as collateral, but can also circulate on the platform, increasing the liquidity of assets.

- Apply for a credit line: The enterprise applies for a credit line from Arf, which reviews it through its credit assessment system and provides the corresponding USDC credit line.

- Payment processing: When businesses receive cross-border payment requests, they can use the USDC credit line provided by Arf to process the payment. This means that payments can be completed instantly without locking up funds in advance.

- Repayment: The business repays Arf the amount of credit used and any applicable fees within 1 to 5 days. Upon repayment, the credit line is reactivated, allowing the financial institution to continue processing new cross-border payments.

3.2.4 PayFi Stack

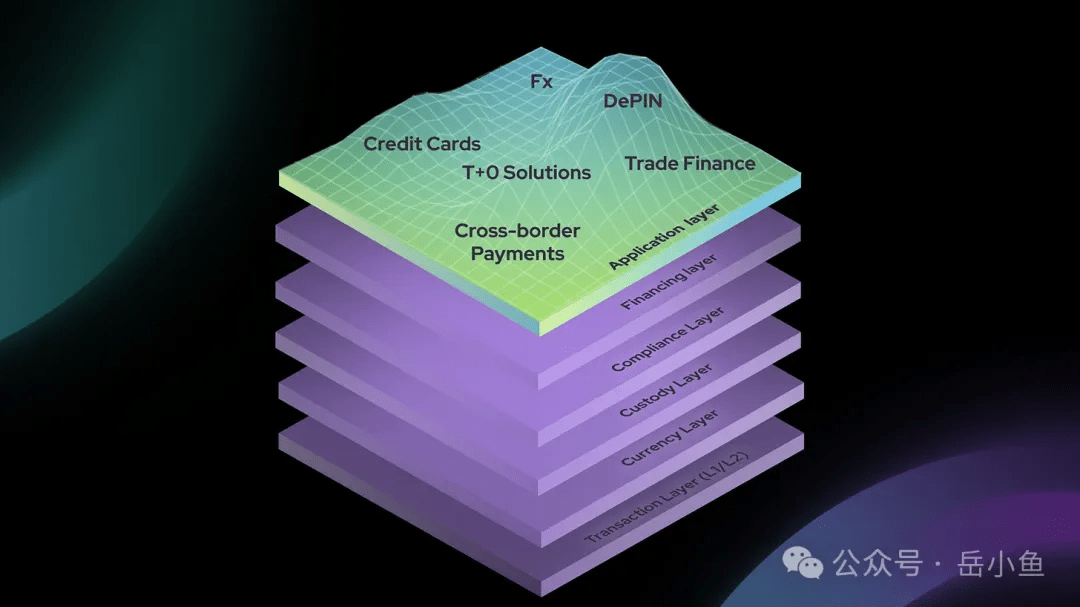

The PayFi Stack proposed by Huma is equivalent to establishing a common framework and standards for the PayFi track.

1. Transaction Layer: This layer involves the selection and application of the underlying blockchain technology, similar to the transport layer in network communications. Huma Finance has chosen high-performance blockchains such as Solana and Scroll as its infrastructure to ensure fast and low-cost transaction processing. This layer determines the basic performance of the network, such as transaction speed, security, and decentralization.

2. Currency Layer: The currency layer focuses on the means of payment, that is, the use of stablecoins. Huma mentioned a variety of stablecoins, including USDC and PYUSD, which reflects the demand for global payment tools. The use of stablecoins can reduce exchange rate risks in cross-border payments and provide more stable and faster means of payment. Stablecoins in different regions (such as EURC, HKDR, etc.) show the importance of localized payment solutions.

3. Custody Layer: Custody services are crucial in finance to ensure the security and compliance of assets. This involves how to safely store and manage digital assets to ensure that only authorized users can trade. The design of the custody layer needs to consider the security of smart contracts, private key management, and the interface with traditional financial systems. There are higher requirements for institutional-level custody, such as multi-party asset control and sophisticated account management. Common custody solutions include Fireblocks, Cobo, Copper, etc.

4. Compliance Layer: Payment and financing services must comply with local laws and regulations. The compliance layer ensures that all transactions and fund flows comply with anti-money laundering (AML), know your customer (KYC) and other regulations. This requires real-time monitoring of transactions, identity verification, and legal adaptation across jurisdictions.

5. Financing Layer: This layer involves how to provide the necessary funds for payments and transactions, including mechanisms such as lending and investment. The funding layer in PayFi Stack needs to solve the liquidity problem, allowing users to obtain instant loans or investments through tokenized assets and improve capital utilization efficiency.

6. Application Layer: Interfaces and services for end users to interact with the PayFi system. This includes various financial products, payment solutions, user interface design, etc. This layer directly affects the user experience and determines the availability and attractiveness of the service. The application layer needs to be flexible enough to adapt to different business models and user needs. For example, from Arf’s cross-border solutions to Zeebu’s telecommunications services, payment needs in different fields are met.

Each layer of the PayFi Stack is designed to solve specific problems in the payment and financing process, from the underlying technology selection and efficient transaction processing to the upper-layer application services and compliance requirements.

By defining these layers, Huma Finance’s PayFi Stack seeks to address the interoperability problem in payment and financing systems, similar to the OSI model or TCP/IP model in computer networks, which aims to enable seamless interaction between different systems and services.

This framework not only promotes innovation in financial technology, but also focuses on practicality, aiming to solve practical payment and financing problems, such as the efficiency and liquidity of cross-border payments.

04 Conclusion

The article is quite long and covers a lot of concepts and underlying principles. Here I will summarize the core content and key conclusions of this article.

Core content:

1. Limitations of traditional payment systems

- The involvement of multiple intermediaries leads to high settlement costs and long settlement times

- Lack of standardized processes and formats limits cross-system operations and global financial integration

- Manual sealing process reduces system reliability and efficiency

2. Analysis of Web3 Payment

- Use blockchain technology to achieve instant settlement and improve capital liquidity

- Mainly divided into deposit and withdrawal payment scenarios and cryptocurrency payment scenarios

- The overall architecture is simpler, and stablecoins are an important payment medium

3. PayFi: Extension of Web3 Payment

- PayFi integrates payments, DeFi, and RWA to create a broader financial ecosystem

- Mainly used in cross-border payment, supply chain finance and consumer finance

- Huma Finance is a typical representative, providing a payment financing network based on RWA

Key conclusions:

- The traditional payment system is very complex. What users perceive are only the various payment channels, but there are many participants and a long processing flow behind it. Especially in cross-border payment scenarios, the financial and time costs of traditional payments will be significantly magnified.

- Specifically, the complexity of the traditional payment system is mainly concentrated in the clearing and settlement link, which can be well solved through blockchain technology. Blockchain is a global ledger with low clearing and settlement costs and fast speed.

- The payment scenarios of Web3 are mainly deposits and withdrawals and cryptocurrency payments. Only when fiat currency and cryptocurrency can be exchanged more freely and conveniently, and the deposit and withdrawal channels are opened up, can cryptocurrency payments truly become popular in daily life.

- In the Web3 payment architecture, stablecoins as a currency medium are very important, because only a medium with stable value can be used as currency. This is also the problem that BTC payment could not be widely popularized before. At the current stage, the price fluctuation of BTC is still too large, and stablecoins are a good payment medium.

- PayFi is a new narrative that combines RWA and Payment, and is a derivative financial service in the payment track. Among them, the current leading representative product is Huma Finance, which supports enterprises to tokenize accounts receivable RWA, thereby obtaining loan amounts for corporate capital turnover. This is a typical supply chain finance. Huma can be said to be very advanced in the field of PayFi.

- Subsequent development of Web3 payment: There are currently three issues that need to be resolved. The first is whether the blockchain performance can support high-frequency application scenarios such as payment, the second is whether the deposit and withdrawal channels can be unobstructed, and the third is how to protect user privacy when the on-chain data is too transparent.

Disclaimer: As a blockchain information platform, the articles published on this site only represent the personal opinions of the author and guests, and have nothing to do with the position of Web3Caff. The information in the article is for reference only and does not constitute any investment advice or offer. Please comply with the relevant laws and regulations of your country or region.

Welcome to join the Web3Caff official community : X (Twitter) account | WeChat reader group | WeChat public account | Telegram subscription group | Telegram exchange group