1. Introduction

On November 26, 2024, Hashkey Group's token HSK was launched. As of press time, the price of HSK has performed well, climbing to about $1.5, with a total market value of $1.5 billion. HashKey Group has attracted much attention for its compliant exchanges, after all, compliance is a controversial track in the crypto industry. This has led to mixed opinions on the prospects of HSK in the market.

To be clear, from the perspective of the token economic model, HSK tokens have long-term sustainable development potential. Under the short-term oriented economic model design of many "VC coins" this year, the price of many projects has fallen after TGE, while HSK "has long-term development potential", which is already a high evaluation. This article will combine the macro background and conduct an in-depth analysis of HSK's economic model based on the systematic token economic model evaluation criteria, not only staying on the surface information such as the distribution mechanism and supply, but further explore how to judge the deep advantages and disadvantages of a token economic model.

2. Macro Background Analysis: Compliance and Coin Issuance

Before analyzing the token economic model, let us first briefly understand the positioning of HashKey in the current macro environment of the crypto market.

Exchanges play a sensitive and important role in the crypto industry chain due to their special nature of being directly related to asset security, and their compliance issues have long been controversial in the market. On the one hand, compliance can significantly enhance the credibility of exchanges, attract a wider user base and gain regulatory recognition; on the other hand, compliance may also weaken user privacy protection and even be considered contrary to the decentralized spirit of the crypto industry.

In fact, from the perspective of historical laws, the development of any industry is difficult to deviate from the inevitable trajectory of "from wild growth to legal compliance". No matter how free or chaotic it is in the early stage, when the industry reaches a certain size, legal compliance will become the only way for further development. Therefore, compliance is an inevitable trend for the Web3 industry to mature. As for decentralization, although it may conflict with compliance, in the long run, the two may also tend to balance in the game and achieve a symbiotic state, so the spirit of decentralization may not be weakened by compliance.

In this context, HashKey's positioning is particularly unique. As the first licensed exchange to issue tokens, HashKey not only carries the decentralized genes of the crypto industry, but also actively explores the development path of compliance. At the same time, "issuing tokens" and "licensing" are the concrete embodiment of this balance.

Therefore, from the macro-law of industry development, if you agree that compliance is an inevitable trend as the industry scale expands, then HashKey is undoubtedly worthy of attention; if you think that decentralization and compliance are irreconcilable, then HashKey is not suitable for your concept. However, as the classic saying goes, "Opportunities are always born out of differences."

3. Real business income: the premise of a sustainable token economic model

Now let’s formally analyze the HSK token economic model. First of all, having real business income is the core prerequisite for the sustainable development of the token economic model .

Real business income refers to the income that users pay for the use value of a project without relying on the sale of any investment products such as tokens, NFTs , and game equipment. Take Arweave as an example. It earns income by providing decentralized permanent storage services, and the fees paid by users are directly linked to their demand for data storage. This source of income is entirely based on the use value of the service itself, rather than relying on token speculation. The funds paid by users are used for long-term storage of data and maintenance of the network, forming a real business income model.

Some GameFi projects are negative examples. For example, the main revenue of some blockchain games comes from the sales of NFT characters and game equipment. These projects often attract users to buy NFTs or tokens through initial hype, but the actual gameplay and experience value in the game are low, and the fees paid by users are more based on speculation rather than the use value of the service itself. Once the market heat decreases, the project will be difficult to sustain.

So why is real business income a prerequisite for the sustainable development of the token economy model? There are two reasons:

First of all, there are two main sources of profit for any crypto project: one is based on real business income, and the other is through market manipulation, such as pulling the price to attract users with FOMO emotions to buy and then sell them for cash. If a project lacks real business income and can only rely on the latter, this model is often unsustainable.

Secondly, a truly excellent token economic model must design a certain mechanism to organically combine with the real business income of the project. This combination can return the project's income to token holders through various mechanisms, thereby enhancing the long-term value of the token. This question sounds simple, but in fact it is quite complicated. The relevant content is discussed in detail in "The Incentive Misalignment Problem in the Crypto Market and the Evaluation Criteria for Sustainable Token Economic Models".

It should be emphasized that HSK is not just the platform currency of HashKey Exchange, but the core token covering the entire HashKey Group ecosystem. This positioning makes it more extensive and in-depth in application scenarios and empowerment mechanisms.

Then, HashKey Group's main business income sources include the following aspects:

- Revenue of HashKey Exchange and HashKey Global Exchange : Compared with the first-tier exchanges, their daily trading volume is basically one to two orders of magnitude lower, but this is quite considerable compared with most on-chain projects.

- HashKey Capital : As an important investment institution in the blockchain field, HashKey Capital manages funds of up to US$1 billion and has invested in more than 600 blockchain projects.

- HashKey Cloud : Focuses on providing professional, stable and secure blockchain services to global customers. Its node verification services cover more than 80 mainstream public chains, and the scale of assets under management reaches 1.2 million ETH.

In addition, HashKey Group also plans to launch the EVM L2 public chain - HashKey Chain. This layout is quite similar to Coinbase's "exchange + L2 public chain + other services" business structure, adding more possibilities to its ecosystem.

In summary, if HashKey Group is compared with other Web3 projects, its business revenue performance can be ranked at the "second-tier" level. However, considering that most projects do not even have real income, this performance is already quite good. This also fully demonstrates that HSK has good business income and the sustainable development potential of its token economic model has a solid premise foundation. Next, we will specifically analyze the design and performance of its economic model.

4. Analysis of Token Economic Model

If we divide the token economic model into two parts: basic information and in-depth research, then almost all articles on economic models currently only focus on the introduction of basic information. This part of the content is certainly important, but it is obviously not enough to try to judge whether a token economic model is healthy and has long-term development potential based on basic information alone. To truly see its value, we must also deeply analyze the specific mechanism of the token economic model.

Basic Information

| Overview | Hashkey Group Coin |

| Total Supply | 1B |

| Release public chain | Ethereum (ERC-20) |

| Other annotations | Incentive-based fair distribution to ecosystem users and contributors, no private or public sales to raise funds |

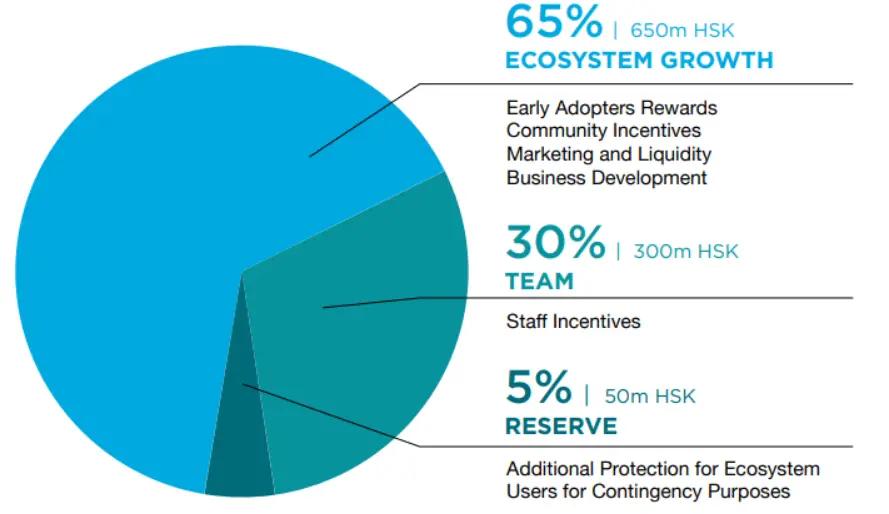

The allocation mechanism is as follows

The basic mechanism of HSK token economy is generally reasonable. We will not spend too much time on it. There are two main points to note here:

- The high ratio of 30% for team incentives may cause some market concerns, especially in the absence of clear lock-up and release rules. However, considering that the team portion will be unlocked after 3 months and divided into 36 months, this release mechanism avoids the team's selling pressure to a certain extent, prevents the team from inaction, and achieves consistency between the team and the project goals.

- Despite the 5% reserve as a risk buffer, in extreme cases, this amount of funds may still be insufficient to cope with greater market pressure.

Next, we will focus on analyzing the in-depth mechanism design of the HSK token and its long-term development potential.

Further research

Not only should there be real income, but it should also be distributed to the holders of the currency

Let’s talk about the most important thing first. The core mechanism in the HSK token economic model is that Hashkey Group will use 20% of the total profit to regularly repurchase HSK tokens and burn them.

Image source: HSK Token White Paper

This is a great design, and it is the core mechanism that makes HSK tokens have long-term development potential. If we simply understand it as "a mechanism that ties the issuance of tokens to the actual operating conditions of the company", it would be a bit superficial. We have said before that "a truly good sustainable token economic model must be organically combined with business revenue." What does it mean specifically? Let's analyze it.

First of all, it should be explained that the repurchase and burning mechanism of HSK is essentially a disguised way of distributing business income to coin holders. This is very intuitive: when HashKey uses profits to repurchase HSK, the circulation in the market decreases, while the total market value (circulation × coin price) remains unchanged. The reduction in circulation will naturally drive up the coin price. In other words, this is equivalent to HashKey indirectly giving back part of its business income to coin holders in the form of rising coin prices.

To realize this mechanism, two key elements need to be met: first, the project itself has real business income; second, a mechanism is designed to distribute business income to coin holders. Only when both of these are met can a token economic model with long-term investment value be built.

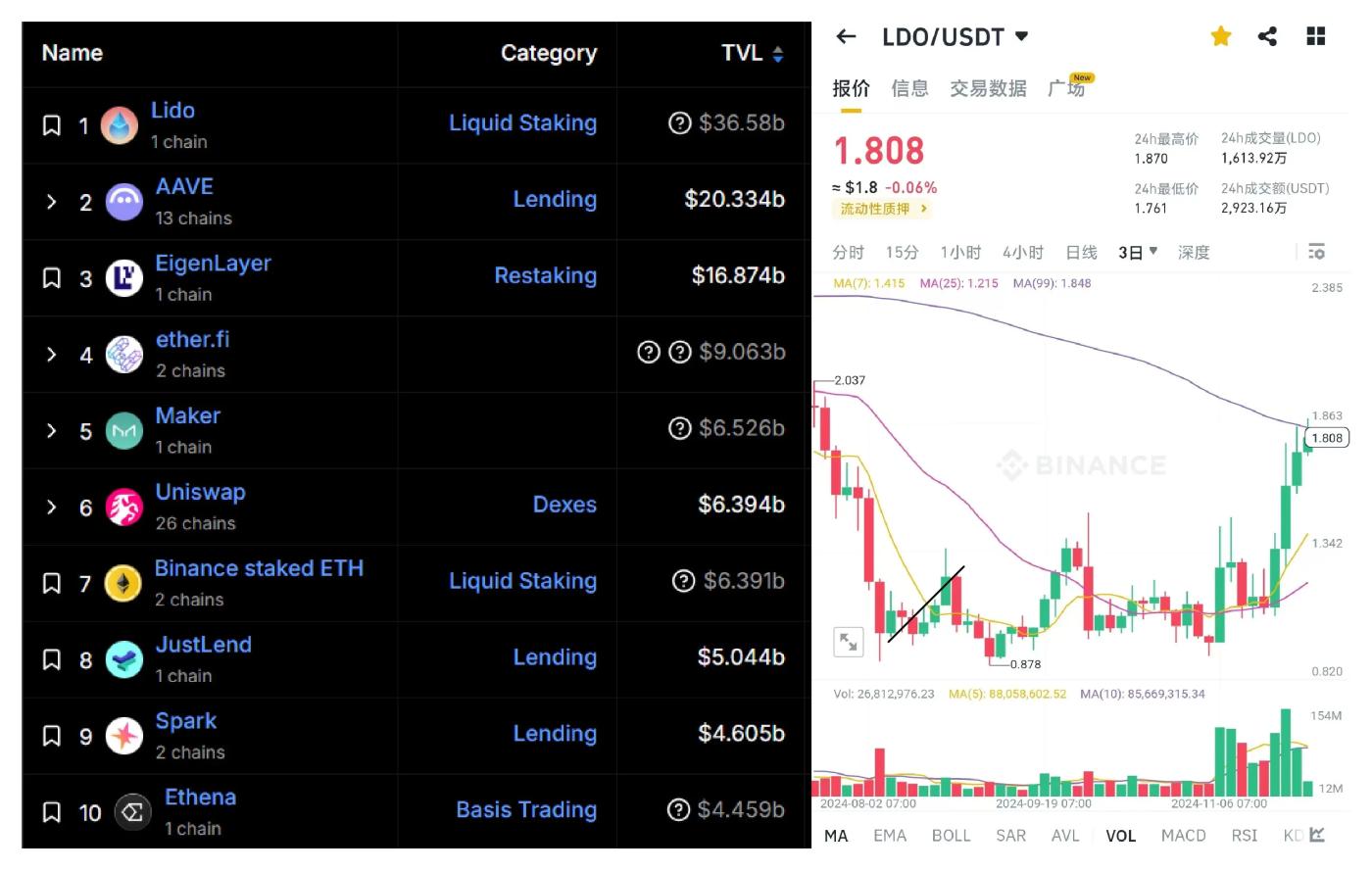

Why do you say that? Because even for high-quality projects with real business income, their token economic models may not be attractive for long-term investment. For example, Lido is a leading project in the DeFi track. It provides services for Ethereum staking by aggregating liquidity, and its business income is the best in the entire Web3 field. But the problem is that Lido's token LDO does not have a mechanism to distribute business income to holders. No matter how considerable Lido's income is, users holding LDO cannot benefit from it. This directly leads to the long-term fluctuation of LDO's coin price in a range, lacking strong performance.

Similarly, the token UNI of Uniswap lacks a profit-sharing mechanism in its economic model, and its price performance is not impressive enough. However, Uniswap has proposed to add a profit-sharing mechanism to its token economics to improve the current situation.

Lido coin price has no correlation with project revenue

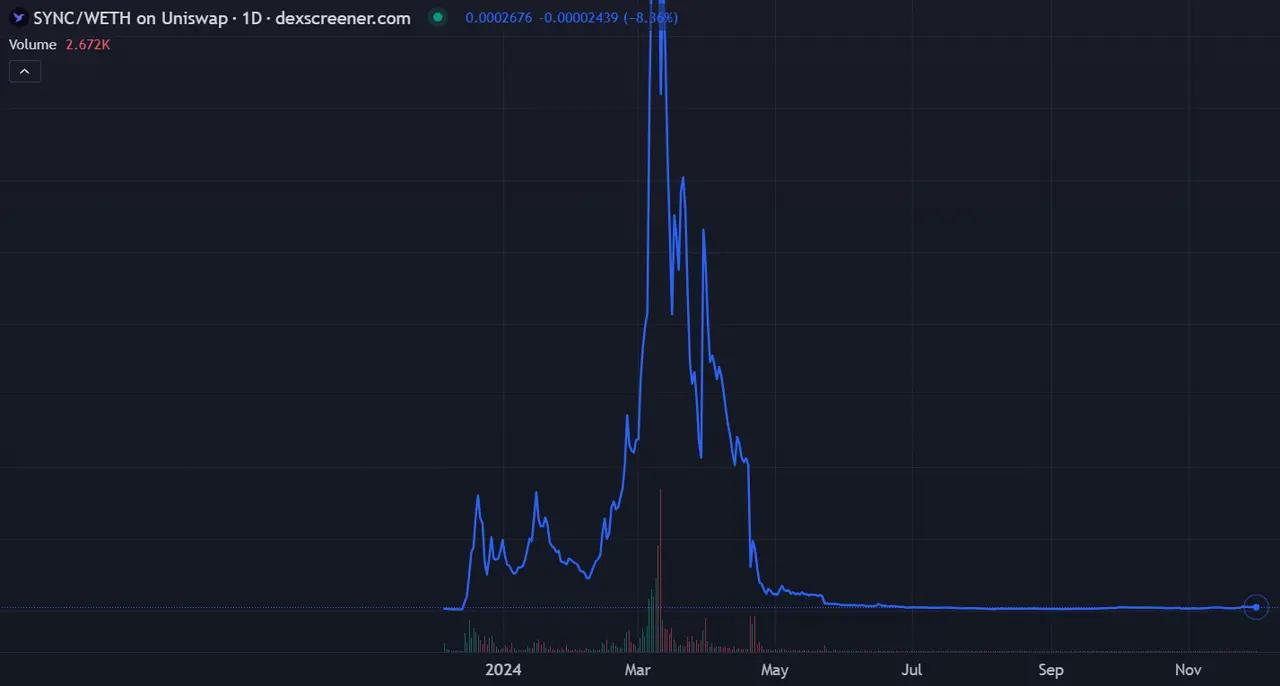

UNI and LDO belong to the categories of “having income but not sharing”, and another type is “sharing, but no income”.

There are many projects of this type, and the price of the coin often rises in the short term and then plummets immediately. The characteristic of this type of project is that there is no business income, and a part of the tokens are often preset in the token economic model to reward the holders. It should be noted that this preset reward is just air, not real money from business income. This type of economic model is a typical short-term explosive rise and fall project, and often does not have long-term investment potential. Due to space limitations, the explanation is expanded here. For detailed analysis, please see "The problem of incentive misalignment in the crypto market and the criteria for judging sustainable token economic models".

The candlestick chart of this typical project SyncusDAO

Therefore, a token economic model with long-term potential must meet the following requirements: a portion of the benefits must be distributed to the token holders, and the distribution must be done with real money from their own business income. The representative of this type of project is Curve, whose economic model design has long become a classic in the Web3 industry. The recent strong price of CRV is essentially because, as one of the leaders of Ethereum DeFi, Curve’s revenue has increased with the recent increase in on-chain transaction volume. Users have long-term confidence in Curve due to CRV’s profit-sharing mechanism. From this perspective, the profit-sharing mechanisms of HSK and CRV are essentially the same.

HSK’s Token Empowerment

An excellent token economic model must have a clear token empowerment mechanism, which is the key to closely integrating tokens with ecological value. Token empowerment means providing actual benefits or functions to token holders, such as participating in governance, enjoying discounts, unlocking special services, etc., thereby significantly enhancing the intrinsic value and market appeal of tokens.

The exchange's platform token naturally has the potential to empower tokens, because the exchange itself has advantages such as liquidity, transaction fees, and project launch resources, which can be used to motivate users through the use of platform tokens. For example, users holding platform tokens can get transaction fee discounts, participate in token sales of new projects (such as Launchpad), or obtain additional income through staking. These empowerment mechanisms not only expand the application scenarios of tokens, but also enhance user stickiness and promote a virtuous cycle of the ecosystem.

Take BNB as an example, its market value has increased hundreds of times since its launch. In addition to the rapid development of Binance itself, it is also inseparable from the wealth-creating effect brought by waves of Launchpool activities, which provides strong empowerment support for BNB. As a coin with similar platform properties, HSK naturally has the same promising development potential.

Another important enabling scenario is that HSK will be used as gas and transaction fees for the EVM L2 public chain Hashkey Chain released by Hashkey Global. The gas and transaction fees of the public chain are undoubtedly an excellent means of deflation, but in fact, more deeply, it will also add a "underdamping mechanism" with soft landing properties to the token to prevent the price of the currency from falling sharply. (The "underdamping mechanism" of the token is discussed in detail in "The Incentive Misalignment Problem in the Crypto Market and the Evaluation Criteria for Sustainable Token Economic Models")

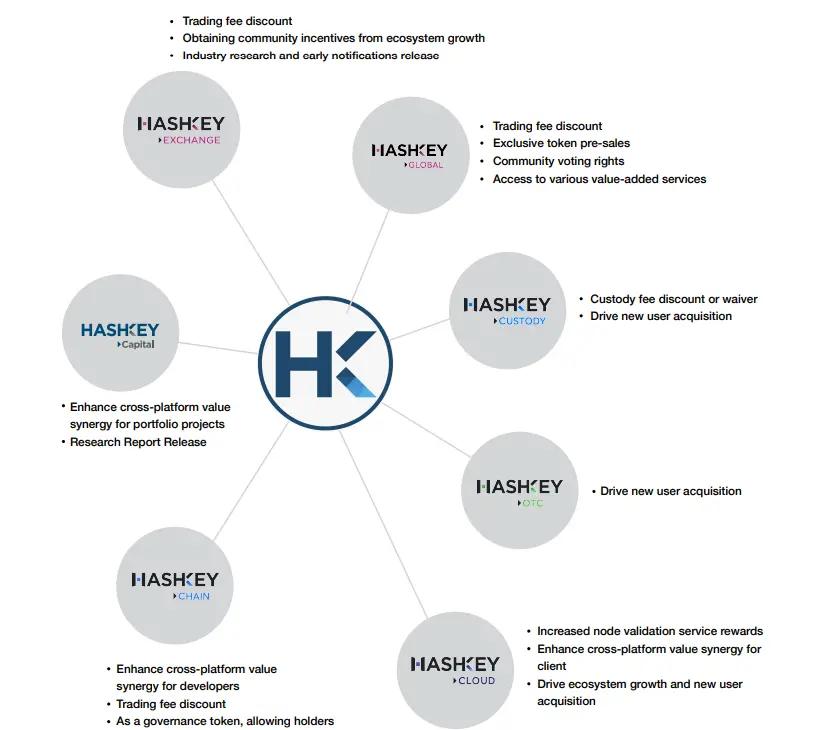

In addition to the platform currency, HSK has diversified application scenarios in different business sectors of the entire Hashkey Group and has sufficient empowerment potential.

Summarize

In summary, the economic model design of the HSK token is quite good in the current crypto market. It not only has real business income support, but also returns income to coin holders through mechanisms such as repurchase and burning. At the same time, it has achieved multi-scenario and multi-functional coverage in the empowerment mechanism, making the HSK token have long-term development potential.

Of course, the improvement of the economic model is only an important part of the success of the project. The future of HSK ultimately depends on the prospects of the compliance track. If you agree that legal compliance is an inevitable trend in the process of Web3 gradually maturing, and believe that this trend is a key step in promoting the integration of the crypto industry with traditional finance and achieving a broader user base, then HSK is undoubtedly a high-quality target worthy of attention. On the contrary, if you insist that Web3 should always adhere to the core spirit of decentralization and non-regulation, and that compliance will restrict the development of the industry, then HSK does not conform to your investment logic.

Opportunities always arise from disagreements in the market. Whether HSK is worth holding for the long term depends not only on the continued development of HashKey Group itself, but also on users’ expectations for the future path of Web3.