Author: Zach Pandl, Michael Zhao

Translator: Luffy, Foresight News

Historically, the cryptocurrency market has followed a clear four-year cycle, with prices experiencing consecutive upward and downward phases. Grayscale Research believes that investors can monitor various blockchain-based metrics and other indicators to track the crypto cycle and inform their risk management decisions.

Cryptocurrencies are an increasingly mature asset class: new spot Bitcoin and Ethereum ETFs have expanded market access, while the incoming Trump administration may bring greater regulatory transparency for the crypto industry. For these reasons, the cryptocurrency market valuation could break new historical highs.

Grayscale Research believes the current market is in the mid-stage of a new crypto cycle. As long as the fundamentals (such as application adoption and macroeconomic conditions) are sound, the bull market may continue until 2025 or even longer.

Like many physical commodities, the price of Bitcoin does not strictly follow a "random walk" model. Instead, Bitcoin price movements exhibit statistical momentum characteristics: uptrends tend to follow uptrends, and downtrends tend to follow downtrends. While Bitcoin may experience short-term ups and downs, its price has shown a significant upward cyclical trend in the long run (Figure 1).

Figure 1: Bitcoin's price has fluctuated but overall shown an upward trend

Each past price cycle has had its unique drivers, and future price movements may not entirely follow past experiences. Furthermore, as Bitcoin matures and is more widely adopted by traditional investors, and as the impact of the four-year halving event on supply diminishes, the cyclical patterns of Bitcoin price changes may be reshaped or disappear altogether. Nevertheless, studying past cycles can still provide investors with some guidance on Bitcoin's typical statistical behavior, which can inform their risk management decisions.

Observations on Bitcoin's Historical Cycles

Figure 2 shows Bitcoin's price performance during the uptrend phase of each previous cycle. Prices are indexed to 100 at the cycle low (the start of the uptrend phase) and tracked to the peak (the end of the uptrend phase). Figure 3 presents the same information in tabular form.

Bitcoin's first price cycle was relatively short and volatile: the first cycle lasted less than a year, and the second cycle lasted about two years. In these two cycles, Bitcoin's price rose over 500-fold from the lows. The subsequent two cycles each lasted less than three years. In the cycle from January 2015 to December 2017, Bitcoin's price rose over 100-fold, while in the cycle from December 2018 to November 2021, Bitcoin's price rose about 20-fold.

Figure 2: Bitcoin's price movements have been similar in the past two market cycles

After reaching a peak in November 2021, Bitcoin's price fell to around $16,000, a cyclical low, in November 2022. The current price uptrend phase has been ongoing for over two years since then. As shown in Figure 2, the latest price uptrend is relatively close to the previous two Bitcoin cycles, both of which lasted around three years before reaching their peaks. In terms of the magnitude of the uptrend, Bitcoin's current cycle has seen a roughly 6-fold increase, which, while quite substantial, is notably lower than the returns achieved in the past four cycles. In summary, while we cannot be certain that future price returns will resemble past cycles, Bitcoin's history suggests that the latest bull market can continue in both duration and magnitude.

Figure 3: Four distinct Bitcoin price cycles in history

On-Chain Metrics

In addition to observing past cycle price performance, investors can also apply various blockchain-based metrics to gauge the maturity of the Bitcoin bull market. Common indicators include the profitability of Bitcoin buyers, the inflow of new capital into Bitcoin, and price levels related to Bitcoin miner revenues.

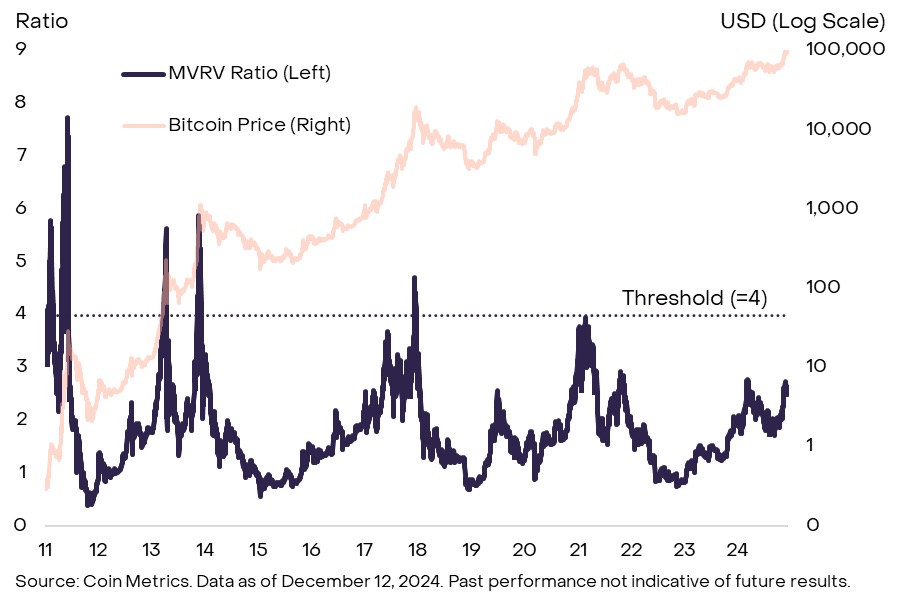

A particularly popular metric is the calculation of Bitcoin's market value (MV) (circulating supply * current market price) relative to its realized value (RV) (the sum of the last on-chain transfer price for each Bitcoin). This ratio, known as the MVRV ratio, can be seen as the degree to which Bitcoin's market value exceeds its cost basis. In the past four cycles, the MVRV ratio has reached at least (Figure 4). Currently, the MVRV ratio is 2.6, suggesting the latest cycle may have further to run. However, the peak MVRV ratio has been declining in past cycles, so this metric may never reach 4 this time around.

Figure 4: Historically, the Bitcoin MVRV ratio has peaked

Some on-chain metrics measure the degree of new capital entering the Bitcoin ecosystem. Experienced crypto investors often refer to this framework as HODL Waves. There are various ways to measure this, but Grayscale Research prefers the ratio of the amount of tokens moved on-chain last year relative to Bitcoin's total free-float supply (Figure 5). In the past four cycles, this metric has reached at least 60%, meaning that during the uptrend phase, at least 60% of the free-float supply was transacted on-chain within a year. Currently, this figure is around 54%, suggesting we may see more Bitcoin change hands on-chain before prices reach a peak.

Figure 5: The ratio of active Bitcoin to circulating supply is below 60%

Some cyclical metrics focus on Bitcoin miners, the professional service providers that secure the Bitcoin network. For example, a common measure is the ratio of Miner Capitalization (MC) (the dollar value of all Bitcoin held by miners) to the so-called "thermocap" (TC) (the cumulative value of Bitcoin issued via block rewards and transaction fees to miners). Generally, when the value of miner assets reaches a certain threshold, they may start to realize profits. Historically, when the MC/TC ratio has exceeded 10, prices have subsequently reached a cycle peak within that cycle (Figure 6). Currently, the MC/TC ratio is around 6, suggesting we are still in the mid-stage of the current cycle. However, similar to the MVRV ratio, this metric's peak has been declining in recent cycles, so the price peak may come before the MC/TC ratio reaches 10.

Figure 6: The cyclical peak of the Bitcoin miner metric MCTC has also been declining

There are many other on-chain metrics, and these may differ slightly from indicators derived from other data sources. Additionally, these tools can only provide a rough sense of how the current Bitcoin price uptrend compares to the past, and do not guarantee that the relationship between these metrics and future price returns will be similar to the past. That said, the common indicators of Bitcoin cycles remain below the levels seen when prices peaked in the past. This suggests that, if the fundamentals are sound, the current bull market may have further to run.

Broader Market Indicators Beyond Bitcoin

The cryptocurrency market is not just about Bitcoin, and signals from other industry sectors may also provide guidance on the state of the market cycle. We believe these indicators may be particularly important in the coming year, given the relative performance of Bitcoin and other crypto assets. In the past two market cycles, Bitcoin's dominance (Bitcoin's share of the total crypto market capitalization) peaked around two years into the bull market (Figure 7). Bitcoin's dominance has recently started to decline, around the two-year mark of the current market cycle. If this trend continues, investors should consider monitoring a broader set of metrics to determine if crypto valuations are approaching a cyclical high point.

Figure 7: The dominance of Bitcoin has shown a downward trend in the third year of the past two cycles

For example, investors can monitor the funding rate, which is the cost of holding a long position in perpetual futures contracts. When speculative traders have high demand for leverage, the funding rate tends to rise. Therefore, the overall level of funding rates in the market can indicate the overall positioning of speculative traders. Figure 8 shows the weighted average funding rate of the 10 largest Altcoins after Bitcoin. Currently, the funding rate is clearly positive, indicating the demand of leveraged investors for long positions, although the funding rate has dropped sharply in the recent decline. Moreover, even at the current local high, the funding rate is still lower than the levels seen earlier this year and the highs of the previous cycle. Therefore, we believe the current funding rate level indicates that the speculative nature of the market has not yet reached a peak.

Figure 8: The funding rate indicates that the speculative nature of Altcoins is at a moderate level

In contrast, the open interest (OI) of perpetual futures on Altcoins has reached a relatively high level. Before the major liquidation event on December 9, the open interest of Altcoins on the three major perpetual futures exchanges had reached nearly $54 billion (Figure 9). This indicates that the overall positioning of speculative traders is relatively high. After the large-scale liquidation, the open interest of Altcoins fell by about $10 billion, but it is still at a high level. The high long positions of speculative traders may be consistent with the late stage of the market cycle, so continued monitoring of this indicator may be important.

Figure 9: The open interest of Altcoins was high before the recent liquidation

The bull market will continue

Since the birth of Bitcoin in 2009, the cryptocurrency market has made tremendous progress, and many characteristics of the current crypto bull market are different from the past. Most importantly, the approval of spot Bitcoin and Ethereum ETFs in the US market has brought a net capital inflow of $36.7 billion and helped integrate crypto assets into a broader traditional investment portfolio. Furthermore, we believe that the recent US election may bring more regulatory clarity to the market and help ensure the permanent position of crypto assets in the world's largest economy. This is a significant change compared to the past, when observers repeatedly questioned the long-term prospects of the crypto asset class. For these reasons, the valuations of Bitcoin and other crypto assets may not follow the historical patterns of the early days.

At the same time, Bitcoin and many other crypto assets can be viewed as digital commodities, and like other commodities, they may exhibit a certain degree of price momentum. Therefore, the evaluation of on-chain indicators and Altcoin data may be helpful for investors to make risk management decisions. Grayscale Research believes that the overall set of current indicators suggests that the crypto market is in the mid-stage of a bull market: metrics like MVRV ratio are far above the cycle lows, but have not yet reached the levels that have marked previous market tops. As long as the fundamentals (such as application adoption and macroeconomic conditions) are sound, we believe the crypto bull market will continue until 2025 and beyond.