Since the last cycle, platform coins are no longer just “handling fee discount coupons”. From destruction mechanisms, revenue participation, on-chain staking to governance attributes, major centralized exchanges (CEX) are constantly reconstructing the value support logic of their platform coins.

As the industry enters a new round of adjustment cycle, users' expectations for platform coins have also changed significantly - from "how much will it increase" to "what will it increase on". Simple marketing drive is no longer sustainable, and it is replaced by more basic factors such as whether the deflation mechanism is truly effective, whether the usage scenarios are continuously active, and whether the platform's own growth is healthy.

Recently, Binance and Bitget announced the completion of their destruction plans. BNB destroyed about 1.579 million coins in its 31st destruction, accounting for about 1.1% of the total supply; and BGB destroyed 30 million coins in its first quarter, accounting for about 2.5% of the total supply. The platform coin track is moving from "having a mechanism" to "redeem mechanism", and the strategic differences between new and old platforms on the deflation path are becoming more and more obvious.

This article will focus on the following core dimensions to compare the structural design and implementation performance of current mainstream platform coins:

The actual strength of the deflation mechanism

● Total volume structure and risk release

● Actual usage scenarios and ecological binding degree

● The growth capacity of the trading platform

● Market performance and value anchor logic

Through a series of horizontal data, structural charts and qualitative observations, we help users clarify the differences and advantages of mainstream platform coins in mechanism design and implementation results.

1. Comparison of deflation intensity: Who is really destroying? Who is still telling stories?

The deflation design of platform coins is the primary dimension for users to judge their long-term value. However, "having a destruction mechanism" does not mean "actually implementing deflation". The key lies in two issues:

● Is the destruction frequency stable?

● Is the destruction ratio stressful enough?

There are obvious differences in the performance of several mainstream platform coins in terms of deflation mechanisms. The following is an overview of the currently verifiable mechanisms and execution rhythms:

BGB's first quarterly destruction in Q1 2025 reached 2.5% , which is higher than the historical record of BNB.

After completing this destruction, BNB has destroyed a total of 1,579,207 BNB, equivalent to approximately US$916 million, accounting for approximately 1.13% of its total supply. This destruction action continues its mature deflation mechanism and once again reflects Binance's long-term investment in platform currency value management.

However, if we look at it from the perspective of “this round of destruction amount vs current market value”, BGB’s market resilience is even more prominent:

It can be seen that although the amount of funds destroyed by BNB in this round is as high as US$900 million, which is about 6.9 times that of BGB , the market value of BNB is 16.5 times that of BGB .

This means that in terms of the “relative pressure” between the platform coin destruction funds and its market value, BGB is much higher than BNB.

This structural asymmetry sends a key signal: BGB's current valuation is still in the "undervalued" stage, and its market value basis has not yet fully reflected Bitget's platform growth, deflationary execution and ecological binding results.

In other words, for the same volume of deflationary behavior, the price impact is more direct and the value revaluation elasticity is stronger on mid- to early-stage assets such as BGB. This is why this round of BGB destruction is not only the node of mechanism realization, but also the starting point of "structural value upward shift".

Comparative comments:

● BNB has a relatively mature deflation mechanism, adopting a dual-track model of BEP-95 automatic destruction + quarterly manual destruction, with a clear rhythm and stable mechanism. The latest quarterly destruction amount reached US$916 million, and its deflation execution is still one of the strongest among mainstream platform coins. However, its single-round destruction ratio has been maintained at around 1% for a long time, and the marginal price pressure has been significantly reduced due to the huge market value, which is more reflected in "robust compression" rather than price drive.

● BGB shows the structural characteristics of "light market value and high deflationary pressure". The first quarterly destruction reached 2.5%. Although the destruction amount is much smaller than BNB, its market value is nearly 3 times that of the latter, forming a stronger supply reduction effect. Combined with its execution mechanism of using hooks on the chain and its market value volume that is still undervalued, BGB's deflationary behavior has a more significant marginal impact on the price, and it has the typical characteristics of a high-growth platform currency.

● OKB is currently still in a state of "having a destruction commitment but lacking execution disclosure". Although the white paper clearly states that there is a deflation mechanism, the actual destruction rhythm is not transparent, the amount is not public, and the path is unverifiable. It is difficult for users to establish stable expectations, and the support for the currency price and market feedback are also relatively mild.

2. Total volume structure and releasing pressure: Whose supply is clearer?

To judge the deflation potential of a platform currency, we should not only look at the destruction ratio, but also whether its supply structure is clear:

● Is the total supply capped?

● Is there still a large proportion of team or foundation shares to be released?

● What is the proportion of circulating supply? Is there any hidden danger of "possible market crash in the future"?

The following is a comparison of the supply structure of the current mainstream platform coins (data comes from official white papers, on-chain information and market platform disclosures):

Comparative comments:

● Although the total target of BNB is 200 million and the supply is continuously reduced through the automatic destruction mechanism, there are still a small number of historical reserved shares that have not been unlocked. Its supply structure is relatively stable, but it will take time to be completely closed.

● BGB is one of the few platform coins that have been "fully released". At the end of 2024, Bitget officially destroyed 800 million BGBs originally belonging to the team at one time , directly reducing the total supply from 2 billion to 1.2 billion, and announced that it is currently in a 100% full circulation state, and there is no subsequent unlocking impact or distribution risk.

● There is a certain degree of uncertainty in the supply structure of OKB , and there may be team holdings and undisclosed unlocking plans. This type of platform currency has a large "future supply elasticity", and users may not be able to accurately assess whether the deflationary effect can be maintained in the long term.

In the value assessment of platform coins, capped supply + full circulation status is the basic foundation for building "scarcity expectations". BGB's approach is to completely eliminate supply-side uncertainty , and by locking the total amount and release rhythm in advance, it directs market attention to the main logic of "actual use drives value".

3. Actual usage scenarios: It’s not who has the most uses, but who is used most frequently

The more usage scenarios of platform coins, the stronger their value support is in theory. But in reality, "usable" ≠ "commonly used" and "nominal support" ≠ "users are really using it".

What is really worth paying attention to is which platform coins appear frequently in product participation entrances and continue to form a positive cycle of "lock-up-deflation-value feedback" through use.

The following is a comparison of the usage coverage of the current mainstream platform coins in the two dimensions of platform (CeFi) and on-chain (DeFi) :

Comparative comments:

● As an established platform currency in the industry, BNB still leads in product usage breadth and ecological maturity. As the core Gas asset of BSC (now BNB Chain), it is naturally embedded in a large number of on-chain DeFi scenarios. However, due to the large user base, the average participation income per user has decreased, which has weakened BNB's motivation to participate to a certain extent.

● The use scenarios of BGB have expanded rapidly in recent years. It is not only frequently used in the core products of Bitget Exchange (such as Launchpool, Launchpad, PoolX), but also bound to the financial management area, Earn strategy combination, fee deduction and other paths. Moreover, most of these products require staking or locking BGB to participate , forming a stable "holding currency-locking-benefiting" chain in actual operation.

● OKB functionally supports participation in project issuance, fee discounts, etc., but its on-chain usage capabilities are weak and the pace of new product launches is slow , resulting in low user usage frequency and insufficient binding stickiness.

Taking Bitget's Launch series of products as an example, BGB is the ticket currency for almost all new projects, and many activities attract hundreds of thousands of users. At the same time, BGB provides gas payment, on-chain staking and other functions in the Bitget Wallet ecosystem, and plans to expand to Web3 scenarios such as NFT casting and DAO governance. These layouts show that BGB is not only used frequently at the CeFi level, but is also gradually building a closed loop of on-chain applications , strengthening its potential as an ecological "central asset".

In comparison, the use of BNB has entered a stable period. Although its functional coverage is wide, the marginal benefits of users are weakening; while BGB is still in the early stages of "function unlocking + user expansion". With the launch of functions such as on-chain DAO governance and NFT purchase rights, its usage closed loop may be further expanded.

4. Platform support: The stronger the platform, the more valuable the coin

Image data source: CoinGecko, April 14, 2025

The value of platform coins, in the final analysis, is still the "platform credit". The deflation mechanism determines scarcity, and the usage scenario determines the intensity of demand, but the final valuation anchor still depends on the actual size, ecological layout and development trend of the exchange behind it.

In other words: the medium- and long-term value of platform coins depends on the platform's real growth ability, rather than conceptual stimulation.

The following is a comparison of some key data of mainstream platforms (data source: CoinGecko, April 14, 2025):

Next, based on TokenInsight 's "Crypto Exchange 2024 Annual Report" , a comparative analysis of the development of the three major exchanges over the past 24 years is conducted:

● Binance: Market share leader, but growth is slowing down. As the world's most influential crypto exchage, Binance still ranks first in terms of spot, derivatives and user volume. As of 2024, its spot share is as high as 48.2%, which means that its platform currency BNB has a strong user coverage and ecological foundation. However, Binance's annual total market share has dropped from 42.2% to 32.7%, and it has begun to show a marginal slowdown in terms of user growth and share stability.

● Bitget: A typical high-growth platform with an impressive leap forward. Bitget is the "second-tier leader" with the most outstanding performance in the past year. As of 2024, its spot share increased by 8.06%, its total market share for the whole year increased by 5.2 percentage points, and its derivatives share was close to 12%. BTC, ETH and other mainstream currencies were traded actively, with a total 24-hour trading volume of more than $3.6B. It is particularly noteworthy that Bitget's growth did not rely on a single explosive point, but was promoted in multiple points around contracts, copy trading, financial management, and wallet ecology, gradually forming a trinity structure of exchange + wallet + product platform, which also constitutes the value foundation of BGB.

● OKX: Stable share, deep product line but limited breakthroughs. OKX is a traditional strong platform, especially in derivatives, it has maintained a certain market presence (15% share). However, the spot share is slightly passive under the impact of emerging platforms, and the market share in 2024 has dropped from 16.6% to 11.8%, and the BTC/ETH liquidity index is also lower than Bitget. OKB's usage logic within the platform is relatively conservative, and its ecological binding is not as good as BNB and BGB, which also affects its valuation ceiling to a certain extent.

The strength of the platform is the underlying anchor point of the platform currency value. From the current situation:

● Binance represents “asset security” and “breadth of circulation”;

● Bitget represents “growth potential” and “mechanism evolution”;

● OKX Relatively conservative , the support for platform coins needs to be further released.

From this perspective, BGB’s current price structure is still in the valuation discount stage of “high-growth platform currency” and has realistic soil for repricing.

5. Market performance review: trends, liquidity, and valuation elasticity in the past year

The structure and mechanism of platform coins are certainly important, but how the market ultimately views them still depends on three indicators:

● Price trend (whether it can reflect structural value)

● Trading activity (average daily liquidity and participation intensity)

● Valuation rationality (current pricing vs potential space)

The following is a comparison of the market performance of the three major platform coins from April 14, 2024 to April 13, 2025 in the past year (data source: CoinMarketCap):

Note: V/MC = average daily trading volume ÷ market value, used to measure activity and liquidity.

Comparative comments:

● BNB performed steadily, rising slightly, and continued to maintain its characteristics as the leading asset in the crypto market. The relatively low turnover reflects its "value storage" positioning.

● BGB has increased by more than 260% in the past year and is currently one of the strongest performing platform coins. V/MC is relatively high, indicating that it may still be undervalued by the market and has great potential for growth.

● OKB’s market capitalization and trading volume are relatively neutral and lack obvious driving force.

6. Who has the long-term value logic?

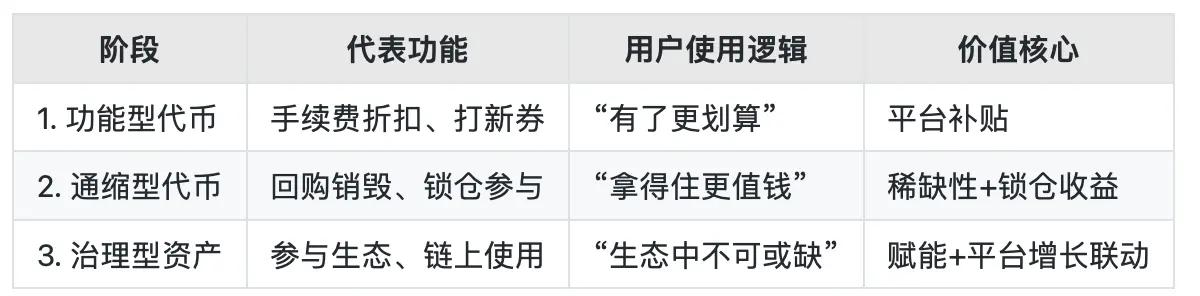

The positioning of platform coins is undergoing an evolution from "tool type" to "asset type" .

In the early stages, the role of most platform coins was very simple - to deduct handling fees, participate in new listings, and earn a small spread . In essence, they were the platform's "user incentive tokens" and were not scarce or had independent value logic. The market's pricing of them was more dependent on sentiment and market trends.

However, starting from 2021, especially after the leading platforms built their own ecosystems and promoted on-chain expansion, platform coins have gradually assumed three deeper roles:

1. Deflation Anchor: Binding Platform Business Growth

● BNB : Linking destruction to on-chain transaction fees through BEP-95;

● BGB : Based on on-chain usage fee + fixed destruction amount, a two-way destruction path is realized;

This means: the richer the usage scenarios → the more destruction → the higher the value of the platform currency , forming a closed loop.

2. Ecosystem participation certificate: becoming a "product ticket"

● Staking BGB/BNB allows you to participate in Launchpad, Launchpool and other products;

● Locking platform coins can enjoy higher financial management interest rates, priority qualifications, and whitelist channels;

Users do not "hold coins for the purpose of speculating on them", but "must hold them to participate in the ecosystem", and platform coins have become part of the ecosystem access mechanism .

3. On-chain governance assets: from platform to chain

● BNB has participated in on-chain governance proposals, gas payments, and staking mining;

● BGB supports on-chain staking in Bitget Wallet, and plans to expand DAO, NFT voting and other functions;

● OKB has also proposed an on-chain governance plan, but it has not yet been fully implemented.

Platform coins are trying to complete the "value out-of-circle" from CeFi internal incentives → DeFi external empowerment, and become the benchmark asset for ecological governance.

Currently, BNB is between stage 2.5 and 3, BGB is transitioning from stage 2 to stage 3, and OKB remains between 1.5-2 .

Through the comparison of deflation mechanism, supply structure, usage scenarios, platform support and market performance, we can see that although platform coins belong to the same category, the logic behind them has gradually differentiated into two categories:

● One type is platform coins with clear mechanisms, tight structures, and positive platform growth , such as BGB and BNB;

● The other type is platform coins with unclear mechanisms, unclear circulation, and weak sense of participation in use , which lack long-term value support.

Based on the current data, we can re-summarize the long-term value potential of mainstream platform coins from the following core dimensions:

By comparison, we can see:

● If users value the long-term deflationary pressure of platform coins + clear use of closed loop + growth platform support , BGB is the "new type of practical platform coin" with the most complete structure and the greatest potential space at the current stage.

● If you value stability and safety margin more, BNB is still the asset with the most fundamental support in the crypto industry.

● OKB may have swing opportunities, but lacks structural clarity and sustainable ecological binding. Holding it requires a higher level of speculative tolerance and timing ability.

So, which users are suitable to pay attention to platform coins? In what scenarios can they consider configuration?

● For users who frequently participate in exchange products and are used to Launchpad, BGB/BNB has a high frequency of participation and can actually benefit;

● For medium-term holders who want "low valuation + long-term potential", BGB's structure is early-stage and more flexible;

● If you prefer swing trading and are willing to short-term speculation, you can pay attention to platform coins such as OKB.

The next round of revaluation of platform coins will no longer rely on stories, but on cashing out. Platform coins that truly have long-term value must be assets that outperform in four aspects: clear mechanisms, clean supply, real scenarios, and continuous platform expansion.

The competition in the future will not just be about “who can grow” but “who can continue to grow”.