Written by: Yue Xiaoyu

Let's directly look at Huma platform's overall business process to get a comprehensive understanding:

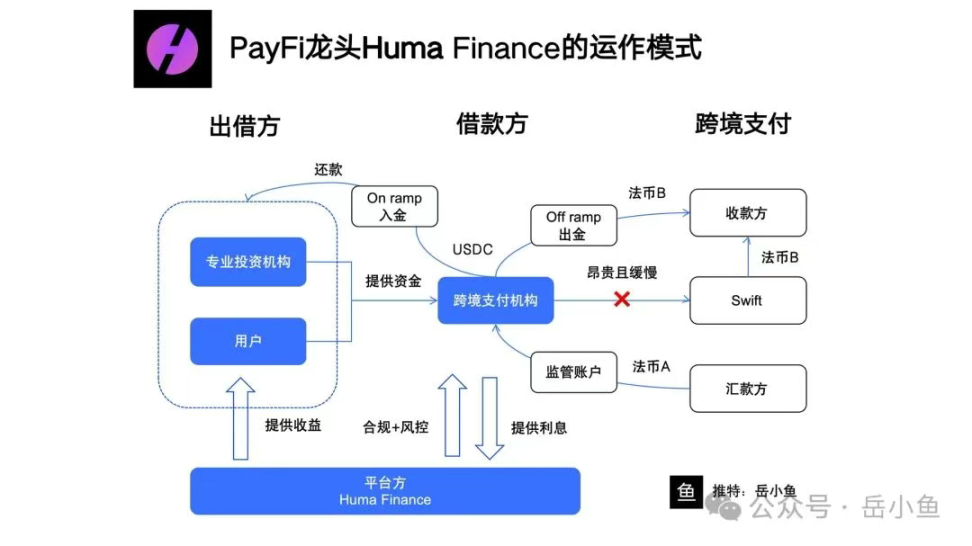

1. User Lending Funds:

(1) Ordinary users (on-chain lenders) deposit stablecoins (USDC) through Huma's decentralized platform

(2) No KYC required, funds are locked through smart contracts, earning fixed returns

(3) Funds enter Huma's lending pool for borrowers to use.

2. Cross-border Payment Institutions Submit Borrowing Needs:

(1) Compliant cross-border payment institutions (such as payment service providers with financial licenses) register on the Huma platform and submit loan applications;

(2) Loan purpose: Provide fast cross-border payment services for remitters (customers).

(3) Loan amount: Usually short-term advance funding (3-5 days), matching remittance scale.

3. Collateral Custody:

(1) Payment institutions must provide equivalent fiat currency collateral, i.e., fiat currency A paid by the remitter (such as euros);

(2) Custody the fiat currency in Huma's designated regulatory account (managed by Arf, a licensed institution acquired by Huma).

4. Borrow USDC and Execute Payment:

(1) Huma issues USDC loans to payment institutions through smart contracts;

(2) Payment institutions use USDC as an intermediary currency, transferring funds to Country B via blockchain (Solana).

(3) In Country B, payment institutions exchange USDC for local currency B (such as US dollars) through local partners (exchanges or OTC service providers) and pay the recipient.

5. Loan Repayment:

(1) Within 3-5 days (credit period), payment institutions use the custodied fiat currency A (collateral) or subsequent funds from the remitter to exchange for USDC and repay Huma's loan principal and interest.

(2) Huma returns the principal and earnings to lenders, deducting platform fees (interest spread, i.e., the difference between borrowing and lending rates).

6. Income Distribution:

(1) Lenders receive stable returns (assuming 10% annual).

(2) Huma earns interest spread (e.g., 15% borrowing rate - 10% lending yield = 5%).

(3) Payment institutions earn customer transaction fees through fast payment services (lower than Swift's 1%-3%) and cover loan interest costs.

Roles and positioning of each party in the entire business process:

We can see that Huma has built a lending platform where ordinary users are lenders providing funding sources, and cross-border payment institutions are borrowers;

In cross-border payment scenarios, the remitter pays local currency A in Country A. If using the traditional Swift settlement system, it would take 3-6 working days with very high fees, involving exchange rate differences and currency conversion fees, typically 1%-3%.

Instead of directly using Swift, cross-border payment institutions receiving remitter payments use USDC as an intermediary currency, borrowing stablecoins on the Huma platform, and then directly converting USDC to local currency B in the target Country B, completing the payment process on the same day.

Throughout the process, Huma provides short-term advance funding for cross-border payment institutions in the form of USDC, with payment institutions requiring one withdrawal and one deposit.

Huma's borrowing end consists of compliant cross-border payment institutions that must provide equivalent fiat currency collateral (such as the remitter's local currency) and custody funds in a regulatory account to ensure risk control.

The lending end participates through on-chain smart contracts, requiring no KYC, and directly depositing stablecoins.

The platform controls the qualifications and loan applications of borrowing-end enterprises, earning interest spread (borrowing rate higher than lending yield).

Let's highlight Arf, the company acquired by Huma Finance:

Arf is a financial institution registered in Switzerland that can provide stablecoin-based settlement services for licensed payment institutions globally.

So after Huma acquired Arf, it directly solved licensing and compliance issues, using this entity to conduct business.

It's worth knowing that the most complicated and biggest barrier in financial business is compliance.

Huma cleverly solved compliance issues by acquiring a licensed institution, simultaneously establishing its competitive barriers.

To summarize:

Huma's operational process and business model are quite clear, but the off-chain part remains a black box with many operational possibilities.

Therefore, Huma's core method of gaining community trust is to potentially put this information on-chain in the future, or directly disclose some borrower information to ensure full traceability of funds.

What needs further attention is that Huma is not just doing cross-border payment advance funding; this business is just an important entry point. In the future, it will expand to more businesses:

Cross-border payments are a $4 trillion market, credit cards are a $16 trillion market, and it can also expand to the broader Trade Finance market.

Overall, Huma is building a PayFi platform and PayFi ecosystem, which can be considered a combination of practical and narrative-driven projects, worthy of long-term attention.