Editor's Note: Currently, RWA perpetual products (such as Ostium) have seen a surge in usage, but the GLP liquidity model is unsustainable due to high funding rates, zero-sum game between traders and LPs, and lack of hedging mechanisms, which limit platform expansion. In comparison, HyperLiquid performs better with a more flexible HLP model. In the future, Ostium may achieve long-term healthy development only by shifting to an order book model, reducing fees, and improving market efficiency.

Below is the original content (slightly edited for readability):

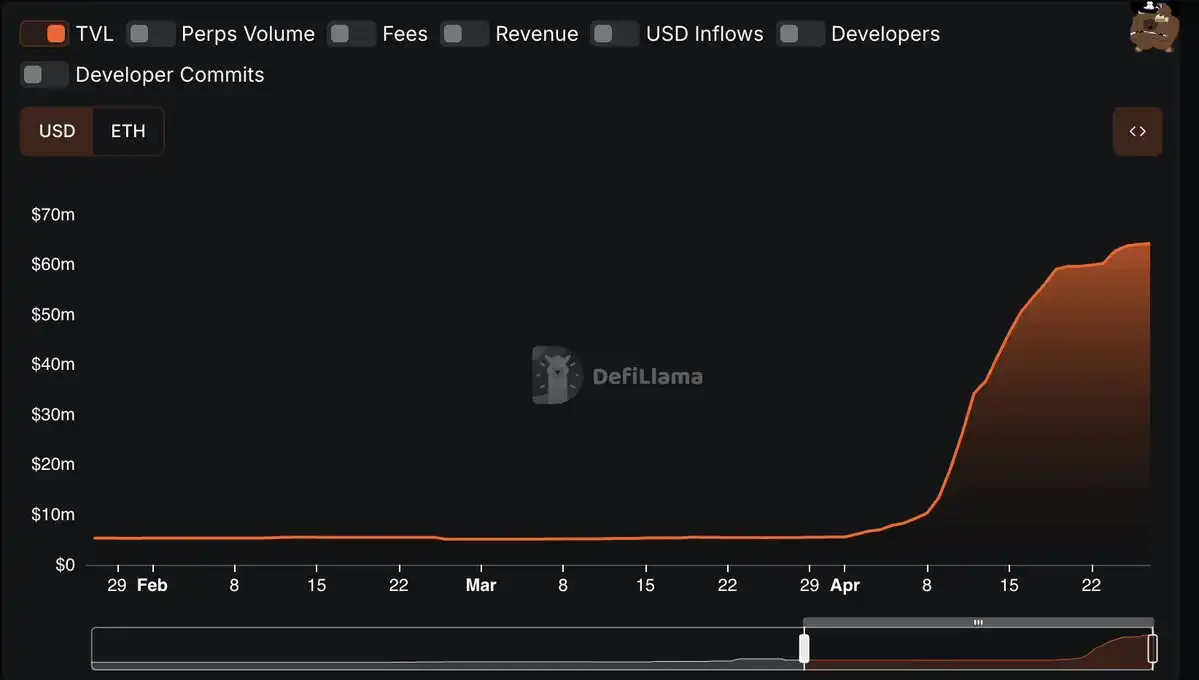

Over the past month, with tariff crises approaching, monetary market volatility, and stock markets fluctuating like an electrocardiogram, the usage of RWA perpetual contracts has seen a surprising growth. @OstiumLabs' total deposits surged from a stable less than $6 million to over $60 million in just one month. Trading volume has also significantly increased. HyperLiquid has also launched a @Paxos PAXG perpetual contract market.

The demand for long or short RWA derivatives is already very apparent. The question is whether the current solutions are good enough, and if not, how they can be improved.

Why these solutions might not be good?

At the beginning, I mentioned two seemingly contradictory points: on one hand, traders are indeed using RWA products; on the other hand, I question whether the existing solutions are good enough.

Some might think that since users are choosing these platforms, it indicates that current RWA perpetual contracts are already sufficient. But that's not the case. Let me explain with some data.

Looking at the funding rates on Ostium, we can see that the gold trading pair (XAU/USD) once had a funding rate as high as 30%, and is still around 13%.

In comparison, the current BTC funding rate on Bybit is about half of Ostium's, while on Binance and OKX, it's only about a quarter of Ostium's. Some might think this is because gold is performing better, but that's not necessarily true.

Gold has risen about 50% this year, and Bitcoin's rise is similar.

When comparing the crypto market with traditional financial markets (like CME), the difference becomes even more apparent. If you go long on gold on CME and roll your position, the annualized cost is around 6%, only half of Ostium's lowest funding rate, a difference of 600 basis points.

Seeing such a large price difference, delta neutral traders might think there's a huge arbitrage opportunity: for example, shorting on Ostium to collect a 13% funding rate while going long on CME with a 6% annualized cost. But it's not that simple.

Because Ostium uses a GLP-like (GMX's liquidity pool) model, if you short on Ostium, you actually have to pay a 13% funding rate.

This means that neither delta neutral traders nor market makers have an incentive to provide liquidity. And this is not a coincidence, but a fundamental design issue with Ostium.

The Unsustainability of the GLP Model

The GLP model used by Ostium and @GainsNetwork_io is, simply put, not scalable.

The GLP model essentially means all traders are betting against the protocol's liquidity pool. First introduced by GMX with their GLP pool, Ostium calls it OLP, and on Gains, it's various g(asset) vaults.

It's important to note that the GLP/OLP model is very different from @HyperliquidX's HLP model. HLP's pricing model is hidden and dynamic, while GLP's pricing is fixed and static.

This means that while HyperLiquid also has base liquidity providers, they are not the only counterparty, and the funding rate mechanism continues to incentivize the market towards greater efficiency. In Ostium's OLP model, traders must lose for OLP liquidity providers to make money. It's a pure zero-sum game.

Unlike the HLP model, which can partially hedge exposure on-chain, the OLP model lacks a stable mechanism to hedge RWA risk exposure.

While the OLP model helped Ostium quickly build liquidity early on, it now becomes an obstacle to further growth. Just as HyperLiquid eventually had to release the absolute counterparty control of HLP to users, Ostium will also need to unbind OLP's pricing dominance to achieve greater expansion.

A warning case has already emerged: in terms of market share in gold, Ostium currently has only $4 million in gold market positions, while HyperLiquid's newly opened PAXG market has already reached $15 million (with lower funding rates and opening costs).

Moreover, Ostium's current total locked value is $65 million, of which $57 million, or 86%, is concentrated in OLP. While HyperLiquid is also high, its proportion is around 60%, which is relatively healthier.

To sum up in one sentence: this model is unsustainable.

Possible Future Directions

Although these problems would be serious if left unchecked, theoretically, they can all be solved by changing the model.

If Ostium can shift to an order book model, it could reduce fees, and funding rates would decrease due to improved market efficiency, while the platform can still profit from trading fees.

OLP could continue to exist but should operate in a more dynamic and flexible manner.

In my personal view, as someone who loves the RWA perpetual concept, this is the only sustainable long-term model for RWA perpetual products, not just for Ostium, but for Gains and all related projects.

The GLP/"casino-style" model can only be used in the cold start phase, and long-term development is unrealistic, which has been verified multiple times.