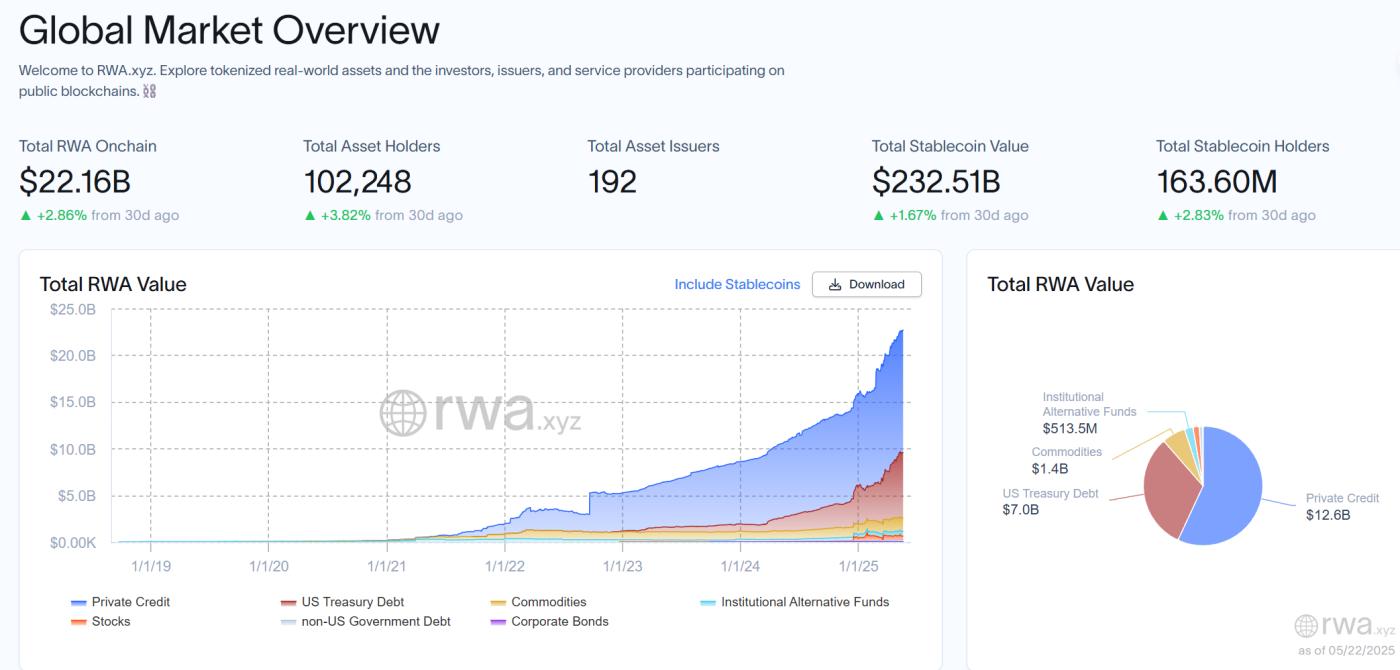

The global asset tokenization process is showing an accelerating development trend. According to RWA.xyz platform data, the total value of global on-chain RWA assets has exceeded $22 billion as of April 2025. Meanwhile, Deloitte predicts in a research report that the tokenized real estate market size will reach $4 trillion by 2035.

In this wave of financial innovation, Hong Kong, leveraging its unique institutional advantages, has quickly become a pioneer in compliant RWA development - from Longnew Group's charging pile asset tokenization project to Huaxia Fund's first compliant tokenized fund in Asia. The successful implementation of multiple benchmark cases confirms the application potential of this innovative financing method in the physical asset domain.

What exactly is RWA?

Why choose RWA, and what are its advantages?

How does Hong Kong regulate RWA?

What compliance points should mainland enterprises pay attention to when conducting RWA in Hong Kong?

The Crypto Salad legal team has been deeply involved in the cryptocurrency industry for many years, possessing rich experience in RWA project architecture design and complex cross-border compliance issues. They will use their latest RWA project experience and industry research to systematically answer these questions from a professional legal perspective.

(The above image is the global on-chain RWA asset dashboard compiled by RWA.xyz)

I. What exactly is RWA?

RWA, the full English name for "Real World Assets", refers to the tokenization of real-world assets, which is an innovative financial model based on blockchain technology. It maps physical or financial assets onto the chain through blockchain technology, transforming them into highly liquid and divisible digital tokens. This conversion process not only achieves the digital representation of assets but also endows these real-world assets with unprecedented transparency and traceability through blockchain technology.

Although we can elaborate on the connotation and extension of the RWA concept at a theoretical level, it is difficult for all parties to reach a complete consensus when it comes to specific project practices.

"What is a true RWA? Which projects should be considered RWA projects" - for these questions, professionals, regulatory agencies, and project parties all have their own perspectives and viewpoints. The Crypto Salad team, combining project experience and research findings, offers their view from a legal compliance perspective: "RWA is actually a broad concept with no standard answer. Any process of asset tokenization through blockchain technology can be called RWA." For an in-depth analysis of the RWA concept, see: 《Web3 Lawyer Decrypts: What RWA Do People Understand?》

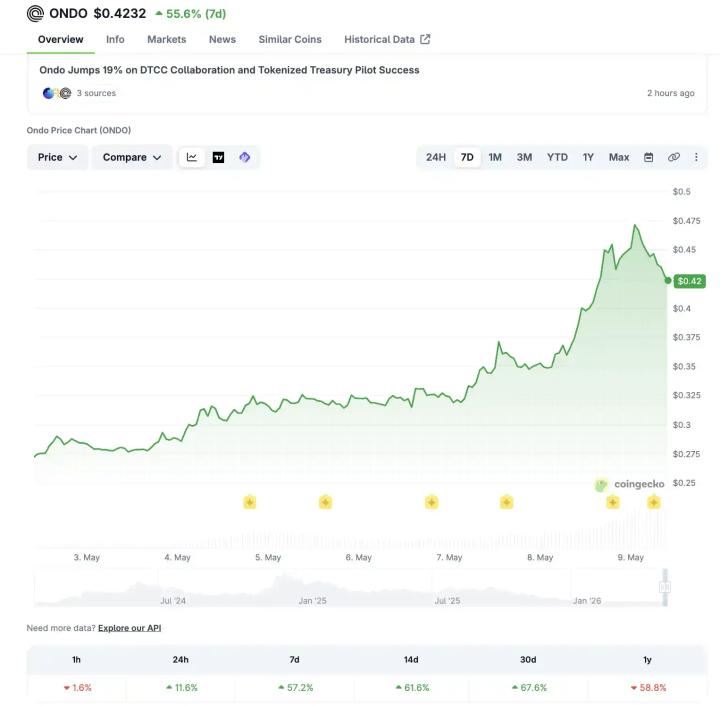

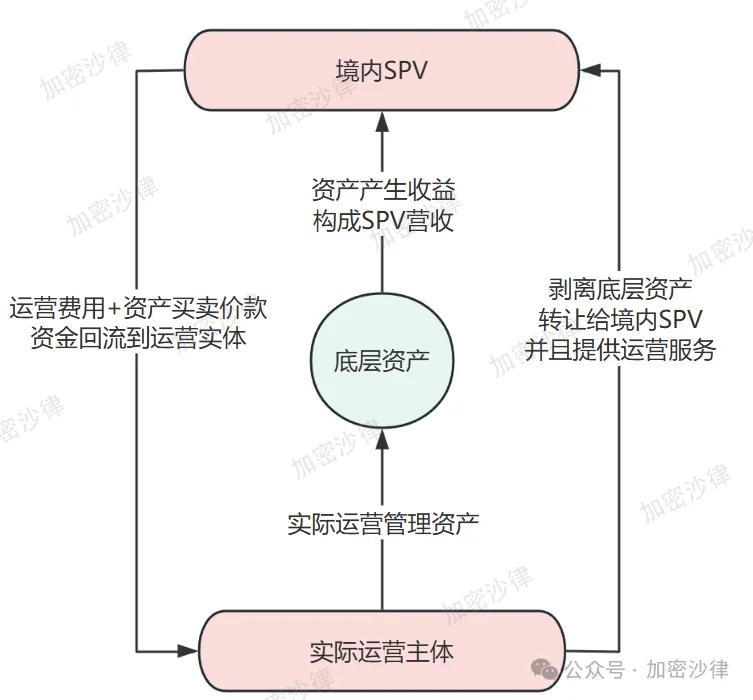

(The translation continues in the same manner for the rest of the text, maintaining the structure and translating all non-tagged content to English.)Here is the English translation: Currently, the market is continuously cultivating and expanding the RWA investor group. In the current RWA track, financial asset tokenization products are leading the way. Due to the high compliance, high standardization, and low data collection difficulty of financial assets, financial asset tokens have inherent advantages and demonstration effects in the RWA track. The wave of financial asset tokenization began with low-risk underlying assets such as US Treasury bonds and money market funds, with a typical case being the BUIDL tokenized investment fund launched by the global top asset management group BlackRock. So far, BUIDL's total market value has reached $2.89 billion. In addition to low-risk financial assets, high-risk financial assets like stocks and ETFs have also recently embarked on the tokenization express lane. On May 22nd and 23rd, Kraken exchange and Ondo Finance respectively announced plans to promote tokenization and on-chain trading of stocks and ETFs. With the rapid landing and development of various tokenized financial assets and stablecoins, the investor scale and liquidity of the RWA market will reach a new height. In the future, more and more different types of RWA products will enter investors' vision, thereby attracting more Web2 users and traditional financial investors into the RWA ecosystem. The entire RWA ecosystem's flywheel will rapidly cycle and develop, bringing new wealth effects and industry opportunities. [Images omitted] [The rest of the document continues in the same translated manner, maintaining the specific translations for technical terms as requested.]Secondly, the actual operating entity transfers the underlying assets to the SPV through buying and selling transactions.

Finally, the SPV will sign an operational service agreement with the project party, with the project party responsible for managing and operating the underlying assets, and the SPV periodically paying corresponding service fees to the project party.

(The above diagram is a schematic design of the asset separation framework, for reference only)

In summary, through this asset separation architecture, the project party can transfer asset ownership to the SPV company, achieving risk isolation while facilitating subsequent asset packaging and issuance. At the same time, although the actual operating entity no longer owns the asset, it can continue to manage and operate the underlying assets through the service agreement.

(II) Data On-Chain Compliance

Due to China's strict supervision of cross-border data transmission and data exchange, most RWA projects will not choose to transmit related data overseas and circulate or disclose it on public chains.

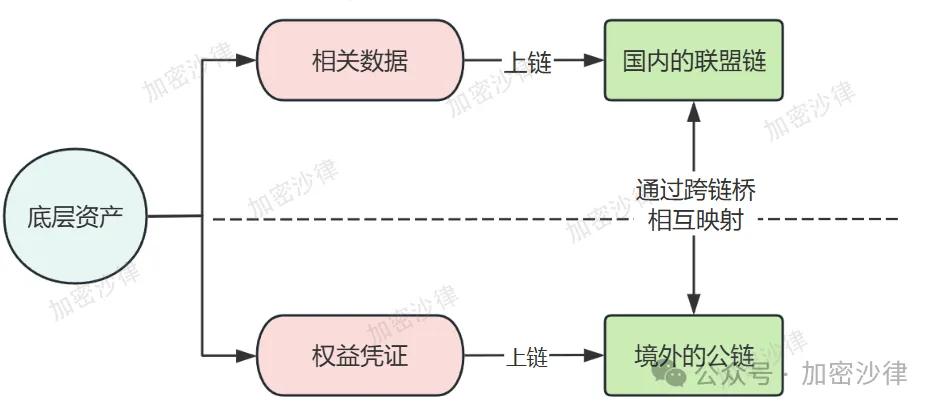

The Encrypted Shalü team discovered during their research that, under the premise of meeting the compliance requirements of China's Data Security Law and Personal Information Protection Law, project parties are more inclined to choose the "Two Chains One Bridge" model to achieve data on-chain.

Specifically, RWA asset data is selected to be on-chain and completed on a domestic alliance chain, while the corresponding RWA Token is deployed on a high-performance public chain overseas. The RWA Token circulating overseas and the data on-chain domestically are mapped and bound through a cross-chain bridge.

This architectural design solves the on-chain evidence problem of RWA underlying asset-related data, ensures the transparency and traceability of asset data, and avoids crossing the compliance red line of cross-border data transmission.

(The above diagram is a schematic of the "Two Chains One Bridge" model, for reference only)

In addition to the "Two Chains One Bridge" model, RWA projects can also rely on the Hainan Free Trade Port Cross-Border Data Flow Experimental Zone (hereinafter referred to as "Hainan Free Trade Data Port") to complete cross-border data on-chain and circulation. Based on the disclosed information, the Encrypted Shalü team summarizes that the current core framework of the Hainan Free Trade Port data export scheme is as follows:

The regulatory agency actively classifies and grades data;

Establish a data whitelist, where data listed on the whitelist can be directly exported without approval;

If data is not listed on the whitelist, the regulatory agency will apply corresponding supervision procedures based on different data types: personal information protection certification, data export security assessment, personal information export standard contract filing, etc.

The Encrypted Shalü team discovered in the actual project promotion process that in addition to compliance requirements in the data circulation link, there are also some key compliance points and administrative supervision requirements in the data collection, preservation, desensitization, and packaging stages of RWA underlying assets. Due to the length of this article, this will not be discussed in detail.

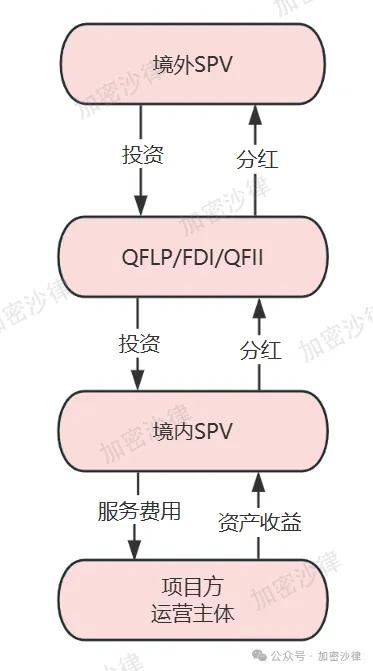

(III) Capital Circulation Compliance

Due to China's strict foreign exchange control, funds raised from RWA issuance overseas cannot be directly transferred to the actual operating entity domestically and require a specialized compliance team to design an overseas fund aggregation and circulation framework and path.

Based on the project experience of the Encrypted Shalü team, after RWA projects complete financing through token issuance overseas, the funds will generally be collected through a capital channel to the overseas SPV and ultimately transferred to the actual operating entity. There are three choices for the capital channel in this framework:

QFLP (Qualified Foreign Limited Partner)

FDI (Foreign Direct Investment Enterprise)

QFII (Qualified Foreign Institutional Investor)

When designing the capital circulation framework, the compliance team generally needs to comprehensively consider factors such as tax burden, entry threshold, procedural requirements, and compliance costs. In the actual project implementation process, the project team must also prioritize compliance. The preparation of application materials, window opinion responses, and corresponding framework adjustments and improvements for different capital channel entities all require full support from a professional legal team.

(The above diagram is a schematic of RWA project capital channels, for reference only)

This represents only the author's personal opinion and does not constitute legal consultation or legal advice for specific matters.