Author: tomas

Translated by: TechFlow

On Twitter, discussions about @pumpdotfun's planned ICO are filled with complex emotions, but with almost no concrete evidence to support these views. Therefore, it's worth delving into its fundamentals to assess two questions: 1) Is the $4 billion ICO valuation reasonable? 2) What are the potential returns or risks of this investment?

This article is not a comprehensive analysis, but a series of key observations that I believe are necessary to form a complete judgment. I also need to declare that I have no conflict of interest with @pumpdotfun, and this analysis will also help me decide how to trade this ICO.

To answer the two questions I raised, I believe the following points need further exploration:

How does @pumpdotfun compete in the meme coin field?

How is @pumpdotfun performing in the entire ecosystem?

Is @pumpdotfun's user attraction and development momentum rising or falling?

Let's analyze them one by one.

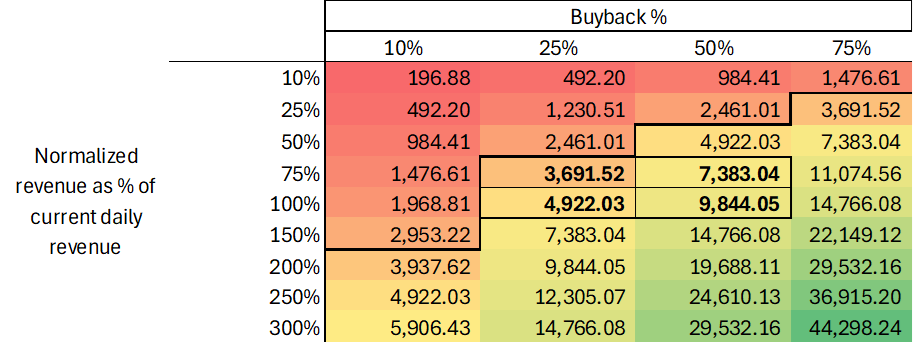

[The rest of the translation follows the same approach, maintaining the original structure and translating all text while preserving the original links and formatting.]Based on the "valuation of dataset B" sensitivity analysis, the results are as follows:

My basic assumption is that Pump.fun can maintain 75%-100% of its current income (daily revenue of $1.5 million), and use 25%-50% of its income for buybacks. This will place its valuation between $3.7 billion and $9.8 billion. If revenue continues to grow, there will be significant room for valuation increase, making a $4 billion valuation seem reasonable or even underestimated.