Read the public information of this article: https://sk6xgpp38n.feishu.cn/docx/PLA0dmrKrop0ihxUljccUoh5nSc?from=from_copylink

Continuing from the previous text, the logic of the interest-bearing stablecoin (YBS) is to mimic the banking industry, which is just a surface appearance. It still needs to solve many problems such as where users' income comes from, how it is issued, and how to maintain the long-term operation of the project. The collapse of DeFi projects is a daily occurrence in the financial industry. SBF going to prison is fine, but the Silicon Valley Bank represents a systemic risk embryo that requires immediate action from the Federal Reserve.

The Era of Excessive Leverage

Seeking profit is a product mindset, and its financial expression is speculation. Large price differences are the source of arbitrage, and long-term volatility requires risk hedging.

Contrary to the way, after introducing computer technology, the financial industry has gone through three stages of quantitative speculation:

• Portfolio Insurance: Diversifying investment targets for preservation, quantifying risk levels and pricing them;

• Leverage (LTCM): Accumulating sand into a tower, where small trading profits can be amplified by borrowing money;

• Credit Default Swaps: CDS is not a demon, but derivative risk control failure has degraded it into pure gambling;

In the current financial world, spatial price differences have disappeared, and daily, small-scale, and decentralized approaches are the norm. On-chain MEV and off-chain CEX are Web3's imitation of TradFi.

Long-term value preservation is no longer mainstream. Leveraging, extremization, and speculation are the goals, with hedging becoming an end in itself, and long-term risks are something that will never come.

In this context, YBS project parties basically face a dilemma: If APY/APR is not high enough, it's difficult to attract funds to boost TVL; but if promised too high, it will inevitably become a Ponzi scheme, ultimately exploding at any stage such as TGE, financing, farming, point farming, VC, or exchange.

Hedging is essentially arbitrage, and momentum cannot be avoided.

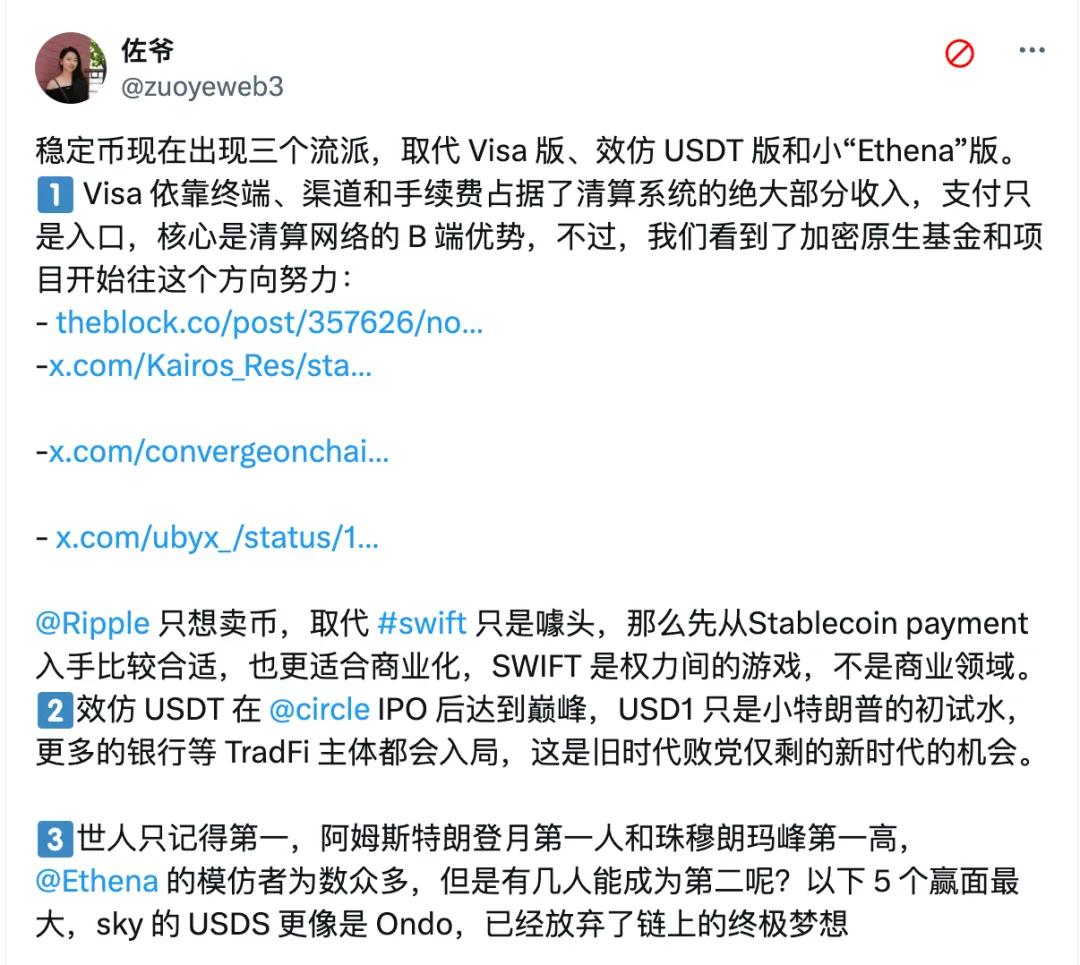

Image description: Stablecoin faction image source: https://x.com/zuoyeweb3/status/1935242935634903275

First, let's extract YBS from the stablecoin market, which currently has three branches:

• The first is for institutions, mainly clearing networks, used for cross-border, cross-industry, and cross-entity transactions, aiming to supplement and replace existing products like Visa and SWIFT, such as JD.com or JP Morgan;

• The second is a product similar to USDT promoted by TradiFi, which can be divided into USD-pegged and non-USD stablecoins, and alternative attempts by large financial institutions, such as USD1;

• The third is competitors of Ethena, such as Resolv, which is the main subject of this article.

The market always has an "impulse" to surge when it can rise and continue to explore the bottom when expected, known as momentum. YBS fits this perfectly. Many projects will compete with Ethena on the same stage, pulling APY to the highest, then clearing the market, leaving the track's king. Hedging will ultimately converge highly with arbitrage, becoming indistinguishable.

(Translation continues in the same manner for the rest of the text)III. Yield Sources

Based on underlying assets and minting mechanisms, we consider two dimensions of yield sources: interest-generating mechanisms and stability, to construct the complete process of minting, interest generation, and redemption of interest-bearing stablecoins.

Taking Ethena as an example, the delta mechanism consists of ETH spot and short position hedging, where hedging itself is the mechanism to ensure USDe's 1:1 dollar anchoring, and the funding rate arbitrage of short positions is the yield source, used to pay returns to sUSDe holders.

Image description: Yield source image source: @zuoyeweb3

Ethena also chooses stETH and other ETH versions with built-in staking yields to enhance yield capture capabilities. The above describes the minting process of sUSDe and USDe, and the redemption process also needs to be considered.

1. sUSDe can be converted back to USDe, with a 7-day cooling period after unstaking before entering the withdrawal process, or directly exchanged in real-time on DEX;

2. USDe can be converted back to ETH with a T+7 restriction. Of course, USDe itself is a stablecoin that can be directly exchanged for any asset on CEX or DEX, though this is not the official asset redemption function.

Beyond Ethena, the remaining YBS projects are merely interest-bearing scenarios with improved asset value stability mechanisms. Avalon's liquidation mechanism is slightly different, more similar to traditional lending products, used to control stablecoin price stability.

Facing the public, involving deposit-taking and lending has always been a social and political event, both in the East and West. Based on this, we delve into the internal workings of YBS, elaborating on the fundamental characteristics of a healthy project from the perspective of the project team. Entrepreneurship is challenging - how many out of 100 YBS projects can survive?