Author: Luotuo Finance

In the past week, the most anticipated TGE in the market undoubtedly belongs to Pump.fun. This token issuance event began in June, continuously fermenting amid expectations and criticisms, until July 12th, when the token was finally launched. Despite ongoing doubts about its $4 billion valuation, the investor response was evident, with the public offering selling out in just 12 minutes, with some investors even cursing on social media for missing out.

For now, Pump.fun has delivered a relatively satisfactory performance. After launch, the price stabilized and rose, and today, Pump.fun achieved its first token buyback using transaction fees. However, the question of whether the token price can be maintained remains uncertain in many people's minds.

In this bull market's application landscape, Pump.fun, if not the top, is certainly near the top. Without exaggeration, Pump.fun's emergence successfully elevated MEME to a new height. Its fair launch concept and convenient operational form completely broke traditional issuance barriers, with the temptation of creating a token for just $3, which remains highly attractive even in today's declining MEME market.

Mechanically, with no pre-sale or private placement, the entire process is smart contract-priced, and it even includes a graduation mechanism that automatically creates a liquidity pool on DEX when market cap reaches $69,000. This almost fully automated listing process was widely welcomed by the market, making Pump.fun the most powerful money-printing machine in this market cycle.

Since launching in January 2024, Pump.fun has issued a total of 11.44 million tokens, with over 22 million usage addresses, achieving cumulative revenue of nearly $720 million. The highest single-day transaction fee reached $5.43 million, with a single-day revenue peak of an astonishing $15.88 million. It can be basically concluded that this round of MEME market dividends were entirely captured by Pump.fun, further driving Solana ecosystem development.

This MEME-originated project's sudden token issuance sparked widespread market discussion. Pump.fun's token rumors began in February, when Wu Blockchain revealed that Pump.fun planned to list on centralized exchanges, even preparing complete token documentation, but was abandoned due to Trump family's frequent MEME causing liquidity drought. In June, token rumors resurged, with Blockworks citing multiple sources reporting Pump.fun's plan to raise $1 billion through token sales, valuing at $4 billion, with tokens to be sold to public and private investors.

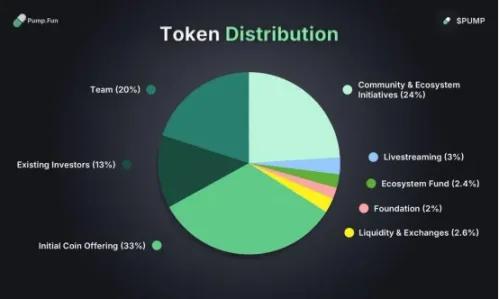

On July 10th, Pump.fun finally announced the official launch of its native PUMP token public sale on July 12th, 2025 at 22:00, with PUMP airdrop imminent. They will issue 150 billion tokens at 0.004 USDT each, representing 15% of total supply (1 trillion tokens). At a $4 billion valuation, they aim to raise $600 million. Due to compliance reasons, UK and US participants are excluded from this sale. In PUMP tokenomics, 33% for public offering, 24% for community and ecosystem incentives, 20% to team, 2.4% for ecosystem fund, 2% to foundation, 13% to existing investors, 3% for livestreaming, and 2.6% for liquidity and exchanges.

Compared to previous expectations, the market collectively doubted the token when it actually launched. Controversies centered on the $4 billion valuation - recall that Circle, the first stablecoin stock to ring the NYSE bell, is valued at only $7 billion. For a so-called "on-chain casino" to claim a $4 billion valuation, even surpassing most current DeFi blue-chip protocols, the market directly accused it of over-extracting liquidity.

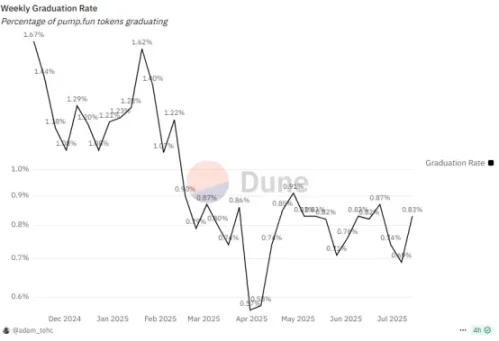

More critically, times have changed. Looking at the current crypto market, except for the recent dragon's rise, most altcoins and MEME coins are experiencing low trends. This can be glimpsed from trading volumes. According to Dune, after reaching a peak of $5.44 million on January 23rd, 2025, Pump.fun's trading volume has essentially cliff-dropped, recently stabilizing within $700,000 daily, an 87.2% drop from its peak. Token creation has halved from a 70,000 peak to 30,000, with graduation rates shockingly low - from 1.6% in 2024 to under 1% now. This clearly shows the diminishing benefit effect, with the MEME market turning "cold" and user enthusiasm rapidly fading.

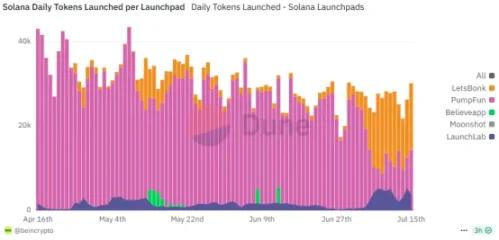

On another front, while the market shrinks, competitors are rising. Pump.fun, once unrivaled, now faces pressure. Recently, letsbonk.fun, centered on BONK, has developed rapidly, often topping token launch numbers and surpassing Pump.fun in market share, though Pump.fun quickly counterattacked, their competition remains intense, and Pump.fun's top position is undeniably threatened.

For these reasons, Pump.fun's $4 billion valuation faced severe questioning. After June's token rumors, it triggered market risk aversion, with popular Solana MEME coins widely pulling back and funds quickly exiting. IOSG Ventures partner jocy directly stated this ICO seems more like a liquidity exit than a long-term development plan. Crypto researcher @rezxbt even pointed out that Pump.fun is staging a complete "harvesting operation".

Interestingly, in March 2024, Pump.fun co-founder alon had stated on social media that every pre-sale is a scam. Coincidentally, Pump.fun is now conducting a pre-sale, ironically contradicting his own statement. Token issuance covers 33% of total supply, with 18% for institutional private rounds and 15% for public rounds, with all tokens fully unlocked on the first day of listing.

From the final result, while industry professionals were skeptical, supporters and institutions clearly thought differently. In the public offering, PUMP tokens completed the $500 million quota in just 12 minutes, with 6 major exchanges including Kraken, Bitget, and Bybit participating. According to Dune panel data, 23,959 wallet addresses completed KYC on Pump.fun's website, with 10,145 successfully purchasing, averaging $44,209 per purchase. 89.7% of PUMP token pre-sale was completed via the official website, with CEXes accounting for only 10.3%. Among pre-sale addresses, small-amount users were the primary group, with 5,758 users purchasing under $1,000 of PUMP, while 202 addresses purchased over $1 million, showing institutional enthusiasm.

The entire process perfectly illustrated the crypto market's unique contradiction. Due to technical issues during exchange public sales causing user purchase difficulties, many users expressed dissatisfaction on social media. At the time, the community had significant disagreements about Pump's subsequent performance - some believing the valuation was too high and would collapse after the spotlight fades, while others argued that as the most representative MEME product, Pump has a complete revenue logic and cognitive foundation and won't easily fail.

From the current stage, the latter seems to have temporarily gained victory. After launching GMGN on July 15, Pump briefly dropped from $0.0065 to $0.0042, but after oscillating, it started an upward trend, currently reporting at $0.0066, rising 55% compared to the $0.004 fundraising price, with FDV price increasing from $4 billion to $6.6 billion, bringing certain wealth effects to subscribers.

Of course, this price increase also has performative elements. According to @EmberCN's on-chain analysis, by 8 am this morning, pump.fun began repurchasing PUMP with transaction fee income. In the past 7 hours, it transferred 187,770 SOL in transaction fees to the 3vkp...3WTi address, purchased PUMP, and then transferred the bought tokens to the G8Cc...kqjm address for storage. Currently, it has used 111,953 SOL (approximately $1.83 million) to buy 3.04 billion PUMP, with an average price of $0.006. Repurchasing can support the price, but it also cannot escape the suspicion of moving money from one hand to another. However, for holders, regardless of the purpose, as long as the price is pulled up, it is ultimately a good thing.

Whether exiting liquidity or simply building for the benefit, the valuation controversy of Pump.fun reflects the current market status. The once liquidity-renowned MEME is collectively entering difficulties, and the explosive attention economy seems to gradually become a false proposition. At this point, even the most representative applications are embarking on token issuance, subtly revealing signals of narrative ending. Where MEME will ultimately go, the token Pump will be a weathervane, and the market's bet on it will be an effective observation of the value judgment of the attention economy. Token price increase at least represents market recognition of its pricing, while token decline will prompt people to consider the true essence of the MEME market, potentially generating more selling emotions. This might also be one of the reasons for Pump's repurchase.

Returning to the title's question, who exactly profited from Pump.fun's token issuance? Undoubtedly, the project side profited, and public and private sale participants have also profited so far, as have short-term long investors. But how long they can profit and to what extent the project can maintain the token price remains a big question mark. Some whales have already started to secure profits. According to Lookonchain monitoring, one whale 8a5nSU spent 5 million USDC through 5 wallets to participate in PUMP public sale, purchasing 1.25 billion PUMP tokens, and sold all at an average price of $0.0067 today, making a profit of $3.416 million.

On the other hand, the current macroeconomic market improvement will also influence MEME to some extent. With a strong Ethereum narrative, mainstream tokens led by Ethereum continue to rise, directly resulting in the outbreak of Ethereum blue-chip Altcoins. Taking ENS as an example, it rose over 18% today, creating a new high since February this year. In the long term, even with current market uncertainty, predictable interest rate cuts are on the way, and the Altcoin market might welcome a small peak. MEME will more likely show a bipolar trend, with quality MEME rising with sector rotation, while remaining MEME liquidity gets absorbed, with most becoming neglected.

If following this path, MEME, similar in nature to lipstick and lottery economies, will continue to exist but will find it difficult to stir up the monetary tide like in 2024.