This article is from: Danning, data analyst at Flashbots

Compiled | Odaily (Twitter: @OdailyChina); Translator | Azuma (Twitter: @azuma_eth)

How much profit can MEV arbitrage Bots actually earn from CEX-DEX arbitrage?

Previously, no one could answer this question, but we are excited to announce that a new paper using formal measurement methods has finally emerged (paper link: https://arxiv.org/abs/2507.13023), and I will outline all the core findings of this paper through a series of images and explanations.

Super Condensed Version

Profits? Considerable, but not as much as you might think;

Bot strategies vary, but top traders' excess returns mostly decay within 0.5 ~ 2 seconds;

Market concentration is intensifying, including in the block builder domain;

However, as blockchain builder competition increases, CEX-DEX arbitrage profit margins are shrinking year by year;

Bots are deeply integrating into the block construction process in various ways;

The deeper the connection with block builders, the thinner the "surface" profits (actually transferred to associated parties);

The smaller the market share of block builders, the higher the actual profit rate retained by their associated arbitrageurs;

Even among the top two in the industry, block construction remains a tough business (profits as thin as paper).

Relatively Detailed Version

In the 1 year and 7 months of data we collected, the performance of 19 top CEX-DEX arbitrage Bots is as follows:

Total trading volume reached $241 billion;

Extracted $233.8 million in profits;

Only retained $90.1 million in net income (paid $143.7 million in shares to block builders);

Overall, the average profit rate for CEX-DEX arbitrage is 38.5%.

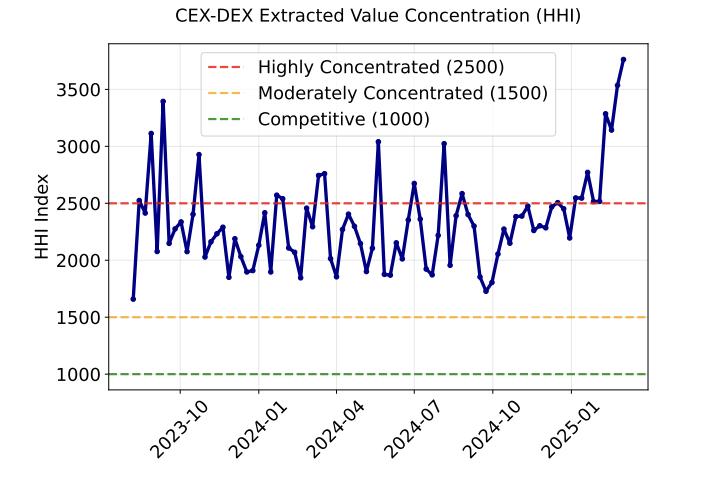

Based on market share analysis of arbitrageurs, we confirm that the CEX-DEX MEV market concentration has reached a "highly monopolistic" level.

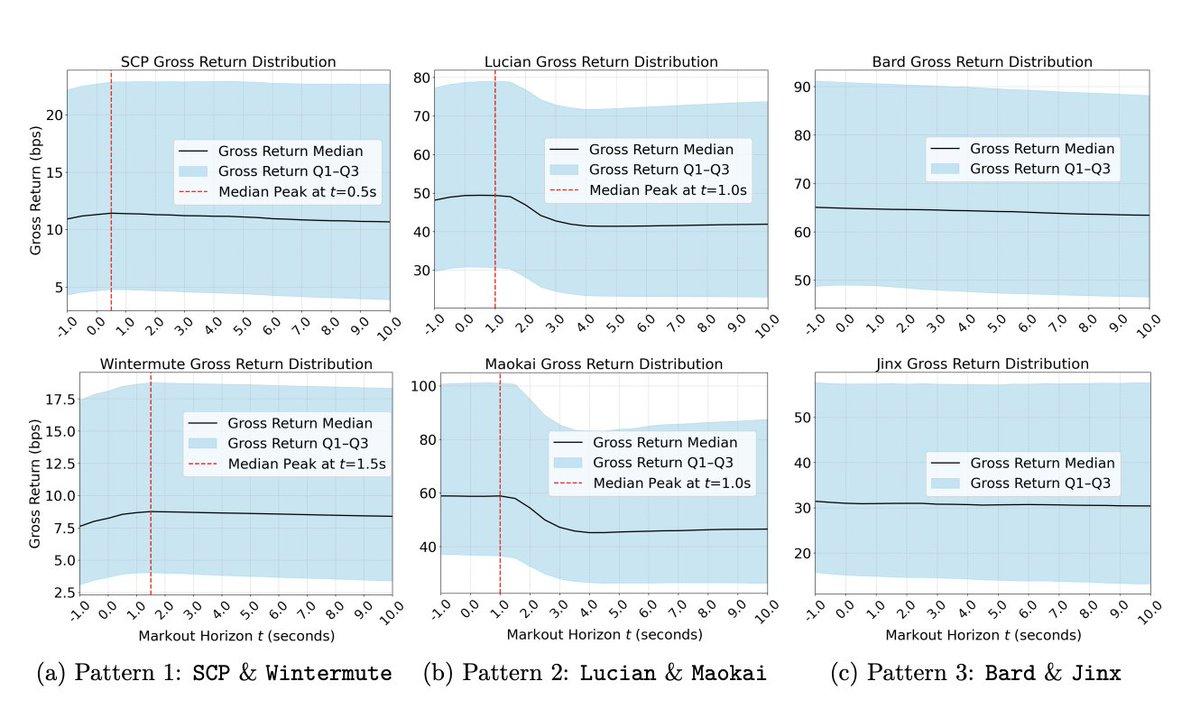

Using the "League of Legends" tier label system proposed by @0x Rezin, we calculated the Binance mark-out prices of arbitrage Bots, using a weighted average to define their "total income" before hedging.

The data shows that most CEX-DEX arbitrage signals rapidly disappear within seconds. Through median distribution, we can observe the income peak - the best hedging opportunity appears in the 0.5-1.5 second interval.

After deducting the share paid to block builders, we obtained an upper limit estimate of Bot profits.

So, how are the current top three block builders' earnings after incorporating arbitrageur profit corrections?

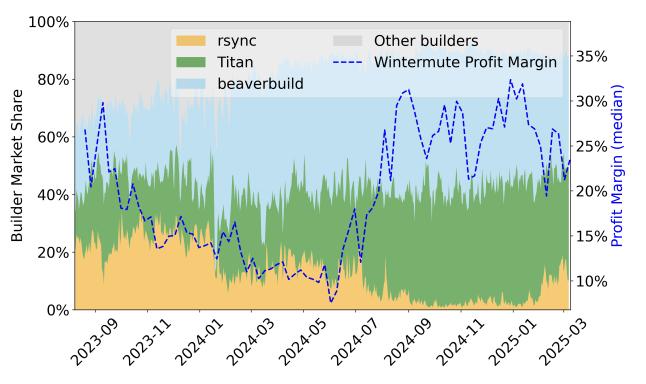

Since rsync (currently ranked third) abandoned the "order flow war" last mid-year, its market share has significantly dropped, but what went unnoticed is that its profit rate has rapidly rebounded from 5% to over 25%, bringing its comprehensive profit rate (arbitrage + block construction) to around 27%.

However, the top two block builders' profitability is very limited.

In the 18-month data cycle, beaverbuild (currently ranked first) has a comprehensive profit rate of only 7.92% (including arbitrage revenue), while Titan (currently ranked second) without self-operated arbitrage has a profit rate of only 5.85%.

Clearly, the opaque "order flow" trading makes this situation even more difficult to explain.

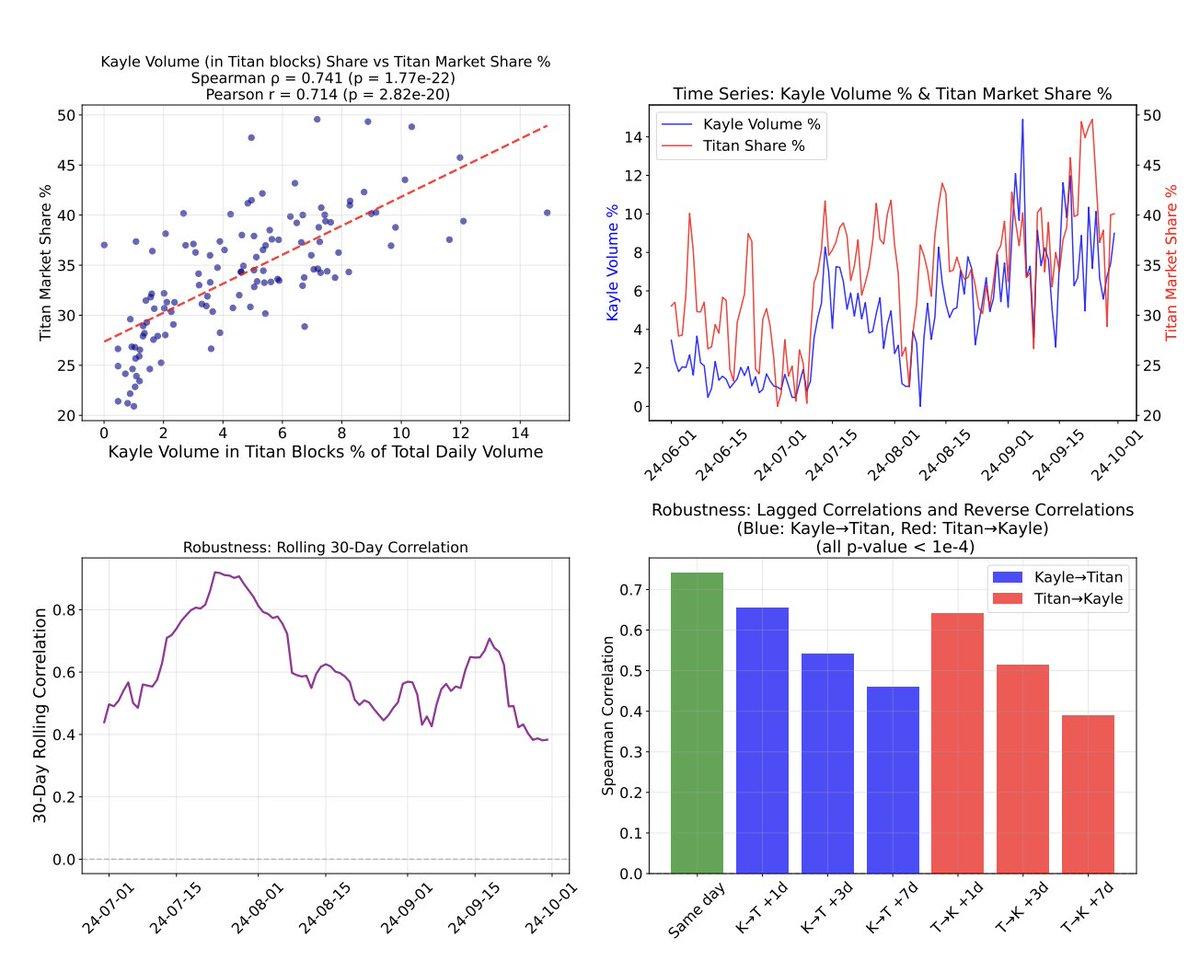

Besides the known combinations like beaverbuild + SCP and rsync + Wintermute, correlation analysis reveals another significant exclusive cooperation case. Observing the 30-day rolling correlation between "Kayle's transaction volume share in Titan's block construction" and "Titan's market share" reveals some insights.

Our core conclusion is that block construction is a low-profit business, and without holding extremely high MEV value order flows, there is no market entry opportunity today.

Additionally, the current block auction mechanism has serious inefficiency issues. On one hand, the subsidy mechanism will squeeze block builders' profits; on the other hand, exclusive cooperation will fragment order flows and extend transaction on-chain waiting times.

However, the current situation is not unchangeable. Flashbots' newly launched BuilderNet may be able to break the deadlock and improve block builders' earnings.