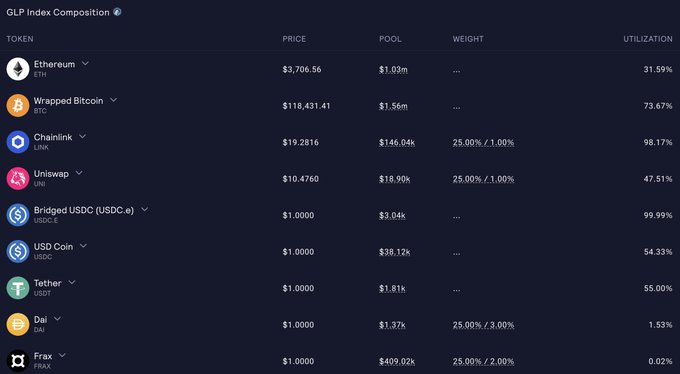

《GLP/JLP/HLP: Everyone can be a banker》 In early 2022, an on-chain perpetual contract exchange called GMX was born. Once the product was launched, it was almost unrivaled and firmly sat on the top of the list. In just one year, the monthly trading volume reached a maximum of 10 billion US dollars, and the Arbitrum chain dominated the list with an average TVL of 500 million US dollars. To date, it has processed a total transaction volume of nearly 300 billion US dollars. The reason behind the gorgeous data is a new liquidity provision mechanism called "GLP" launched by the team. "GLP" achieves one thing: "Allowing anyone to be the banker on the chain and act as the counterparty of the gambler." Since then, the liquidity provision method similar to GLP has been passed down to the present. Looking at the current on-chain perpetual contract exchange track, you can see similar product design concepts in almost all related protocols: HLP, JLP, MLP... Although GMX itself is no longer as glorious as it was in the past, understanding similar "banking models" can help you be more relaxed in using various derivatives protocols. "Perpetual Contract LP: Retail Investors' Counterparties" In traditional finance and early DeFi, market making has always been a game for professional players: the capital threshold is high and the risk control requirements are extremely strong, making it impossible for ordinary users to play. The perpetual contract LP model breaks all of this. It simplifies "market making" into a betting-style liquidity participation mechanism - users no longer need to predict the market, they only need to deposit money into a shared pool and enjoy the fees and losses brought by traders. This design of "you pay the money and the protocol is the banker" not only greatly reduces the threshold for market making, but also becomes a new way for DeFi protocols to generate their own blood. So you will find that more and more perpetual exchanges are starting to launch their own GLP, HLP, JLP... In essence, they are all playing the same game. Let's take GLP, the pioneer of this mechanism, as an example to reveal the underlying operating logic. GLP is the liquidity pool of GMX, which is the counterparty of all perpetual contract transactions on the entire platform. When users open a long or short position on GMX, they are not facing another user, but the entire GLP fund pool. As a GLP holder, you are one of the people who bet with others, but you don’t need to do anything, just wait for the result. GLP's revenue mainly comes from two parts: - First, commission income: All transactions will generate commissions, which are distributed proportionally to GLP holders. - The second is the loss of the trading counterparty: the losses caused by others' high leverage margin calls and misjudgment will eventually be absorbed by the GLP pool and go into your pocket. The whole process does not require market prediction or monitoring. You only need to put money in and you can passively collect money like an "algorithm-driven banker". The more frequent the transactions and the more people lose, the more GLP earns. So what's in the pool? From the above picture, we can see that GLP is not a "single asset pool", it is more like an "asset portfolio" or "index fund". The funds in it are mainly composed of three types of assets: - Mainstream assets such as ETH and WBTC; - Stablecoins such as USDC/USDT/DAI; - Large-cap Altcoin such as LINK/UNI. The asset allocation of the pool will be dynamically adjusted according to the market trading direction. For example, if the proportion of ETH in the pool is too high relative to the target weight, the cost of minting GLP with ETH will be higher, while the cost of minting with other assets will be lower to help the pool rebalance. In other words, the agreement will dynamically adjust positions based on "counterparty pressure" to ensure that GLP will not be easily crushed in extreme market conditions. But what are the risks of GLP? Will GLP lose money? Of course, after all, you are trading against traders across the market. There are three main sources of risk in GLP: 1. The market is unilaterally strong and traders collectively make profits: For example, in a strong bull market, a large number of users open long positions and make money, then GLP, as the counterparty, will lose money; 2. The underlying assets fall: GLP is essentially an asset pool. If the ETH or BTC you deposited falls sharply, the market value of your holdings will naturally shrink; 3. Shrinking transaction volume: If the platform activity decreases, the fee income will decrease, and GLP's income will also decrease. So although GLP is "brainless participation, automatic profit", it is by no means a risk-free product. Its profit and risk actually depend on two factors: "market conditions" and "trader behavior". "The evolution of perpetual contract LPs, what are they earning?" Initially, the peer-to-pool model of GLP was the core operating mechanism of GMX, an on-chain perpetual exchange. However, as competition in the on-chain perpetual contract exchange sector becomes increasingly fierce, protocols continue to evolve and innovate on this basis, and the perpetual contract LP mechanism has gradually evolved from the initial "passive market maker" to a more diverse and sophisticated form. > Diversification of asset structure When GLP was first created, the assets were mainly ETH, BTC and stablecoins. This design is not only convenient for risk control, but also in line with the mainstream asset preferences of the on-chain perpetual contract market. However, as the on-chain ecosystem continues to expand, more and more public chains and protocols are beginning to try to support more risky assets. For example, GMX V2 attempts to support more long-tail asset transactions by introducing an asset isolation pool (GM Pool). In other words, in V2, each trading pair has an independent market-making fund pool and no longer shares risks, which provides users with more flexible choices. Suppose you think now: "The altcoin season is coming soon, ETH will soar, and BTC may not have much room for growth", and at the same time you want to make some financial strategies around GMX. In V1, only participating in GLP may cause GLP to lose money due to the crazy unilateral market of ETH, but in V2 you can choose the market where the underlying asset only exists in "BTC+USD", so you only have BTC risk exposure. In addition, when we look at all the public chains, almost every chain cannot avoid the three old DeFi items: "DEX, lending, and Perp". In addition to the fact that we have proven that users have a rigid demand for these applications, from the asset side, the development of a public chain is inseparable from governance tokens. In order to allow governance tokens to have actual demand and value capture, the GLP-like model is one of the important ways to accumulate funds. The most representative one is "JLP" on Solana. "JLP" is a replica of "GLP" launched by Jupiter on Solana. With the rebirth of $SOL, "JLP" has become the core basic asset of Solana DeFi, and its shadow can be found in almost all mainstream DeFi protocols. > Diversification of income structure With the great success of the GLP model in peer-to-pool perpetual exchanges, the concept of perpetual contract LP has also begun to spread to more complex market structures. Nowadays, even in contract exchanges with order books as the core mechanism, we can see that designs similar to "liquidity providers connecting to traders at a loss" are quietly emerging. Take Hyperliquid's HLP as an example: it is a community-driven liquidity sharing pool. After users deposit USDC, the protocol automatically places buy and sell orders in its on-chain order book and earns the buy and sell spread, transaction fees, funding fees, and liquidation fees when trading is active. The key difference from traditional perpetual contract LPs (such as GLP) is that: - Market making method: from passive "point-to-pool" betting to active order matching on the order book; - Revenue structure: Added bid-ask spread and other fees; - Strategy initiative: Introduce algorithmic market making and strategy adjustment. In order to expand product revenue, more and more protocols will choose to introduce some active strategies "operated by the protocol", which is actually very different from the original GLP model. For such "black box strategy" products, users should be more cautious and always pay attention to changes in revenue. "It's not easy to be a banker, be careful of getting hit hard" When we do perpetual contract LP, in most cases we are the counterparty of the trader. The source of the trader's profit comes from the LP, so theoretically we don't want to see extreme one-sided market conditions, because this situation can easily lead to traders making profits. But in fact, Crypto market transactions are relatively irrational, so in the long run, GLP is basically difficult to lose money. The risk that deserves our attention is that when we are "famous dealers", it means "the enemy is in the dark, we are in the light". The trading market is a PVP game. When we are in a passive market-making situation, there will be a smart "scientist" in the market who will stare at our strategy and implement "targeted attacks". Once the loopholes designed by the exchange are discovered by smart players, it will be a devastating blow to any liquidity provider. It is difficult to achieve absolute security in DeFi. For example, an old protocol like GMX that has been running for many years still allowed attackers to find a logical vulnerability in GMX V1 in July 2025. The attacker took advantage of a small loophole in the system's steps of updating prices and balances when calculating the price of GLP tokens. By establishing a large number of "short positions", the attacker achieved the effect of raising the price of GLP, and then redeemed the pre-deposited GLP to make a profit through the price difference. High-end attacks often use the most common means. In March 2025, a low-liquidity currency price manipulation incident occurred on our "version child" HyperLiquid: a trader used high leverage to open a short order of about four million US dollars on HyperLiquid; then used another address to dump the spot to make the short order profitable; after making a profit, a large amount of margin was raised, causing the short order to be forcibly closed; due to insufficient liquidity, the huge short order was taken over by HLP; this trader then bought a large amount of spot to increase the price, causing a huge loss in the HLP vault. When the situation was out of control, HyperLiquid officials chose to intervene centrally, rolling back the price and ultimately helping the providers of the HLP vault to stop losses. 「End」 As on-chain perpetual contract exchanges gradually become a "red ocean" track, the perpetual contract LP model has become more and more common, and the mechanism has also changed. In the bull market, trading behavior becomes extremely active, and the handling fees and counterparty income surge, providing LPs with considerable profit opportunities. Oracle attacks and contract vulnerability attacks are indeed difficult to avoid, so for retail investors, "selecting the leader" may be the simplest solution. Disclaimer: The content of this article is for knowledge popularization and educational purposes only and does not constitute any investment advice or financial advice; DeFi protocols are subject to high market risks and technical risks, and digital asset prices and yields fluctuate greatly. Participating in digital asset investment and DeFi protocols may result in the loss of all investment amounts; readers are requested to understand and comply with local laws and regulations before participating in any DeFi protocol, conduct risk assessment and due diligence, and make prudent decisions.

This article is machine translated

Show original

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content