Compiled by Will Awang

"Small currencies, exchange-strapped countries" are often synonymous with African countries. For companies planning to enter the African market, the complexity of the local financial environment—banking system restrictions, exchange rate fluctuations, and regulatory uncertainty—is often daunting. These obstacles not only hinder daily operations but also deter potential investors. Consequently, the search for alternatives has become essential, and in recent years, blockchain-based encrypted funding channels have been increasingly adopted by companies.

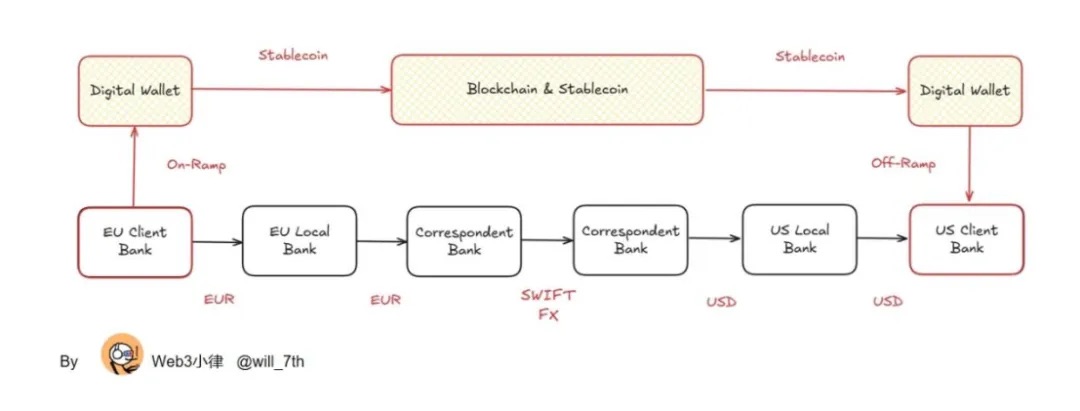

As discussed in our previous article, "Stablecoin Payments and Global Capital Flow Models," while stablecoins fully demonstrate blockchain's core capability of "instantly transferring funds and value," payments are far more than just peer-to-peer transfers. Just like in the stablecoin sandwich, while blockchain replaces traditional payment channels for horizontal value/fund transfers, both ends still rely on the legacy financial payment system, ultimately requiring a return to the bank account system in the target market.

Therefore, crypto over-the-counter (OTC) trading has become a core component of stablecoin payment companies, especially for African countries with small currencies and limited exchange rates. The lack of local financial infrastructure and the inaccessibility of traditional channels have driven the rapid growth of the crypto OTC market. Its efficient deposit and withdrawal services allow companies to transfer funds between fiat currencies and stablecoins securely and quickly.

As Africa and the world accelerate their embrace of digital innovation, crypto/stablecoin payment channels provide opportunities for businesses to expand in a rapidly changing market.

To this end, we compiled a report titled "The Rise of OTC and Stablecoins: Africa's Quite FX Revolution ," from Quidax, a stablecoin payment company (also known as a local OTC service provider in Africa). The report provides a strategic overview of how global firms can leverage crypto over-the-counter (OTC) transactions to streamline settlement, access liquidity, and confidently expand into the African market. Based on regional insights, market trends, and operational realities, the report is designed for decision-makers, financial executives, and treasury teams to help them navigate Africa's evolving cryptocurrency landscape with compliance and clarity. The report also features interviews with several leading figures in the African crypto industry.

Executive Summary

Over-the-counter (OTC) cryptocurrency trading is rapidly becoming a key enabler for global businesses to seamlessly participate in Africa's digital financial ecosystem. By conducting large-scale, peer-to-peer crypto transactions outside of traditional exchanges, the OTC model addresses the structural shortcomings of the traditional banking system and provides a secure and compliant new path for institutional-level settlement. In 2024, global OTC crypto trading volume increased by 106% year-over-year, with stablecoin activity growing by as much as 147%. This has driven African platforms like Quidax and Busha to leverage this model for efficient, large-scale trading. These services help businesses meet liquidity needs with minimal market disruption, achieve real-time fiat settlement, and streamline regulatory compliance onboarding in high-growth markets such as Nigeria, South Africa, and Ethiopia.

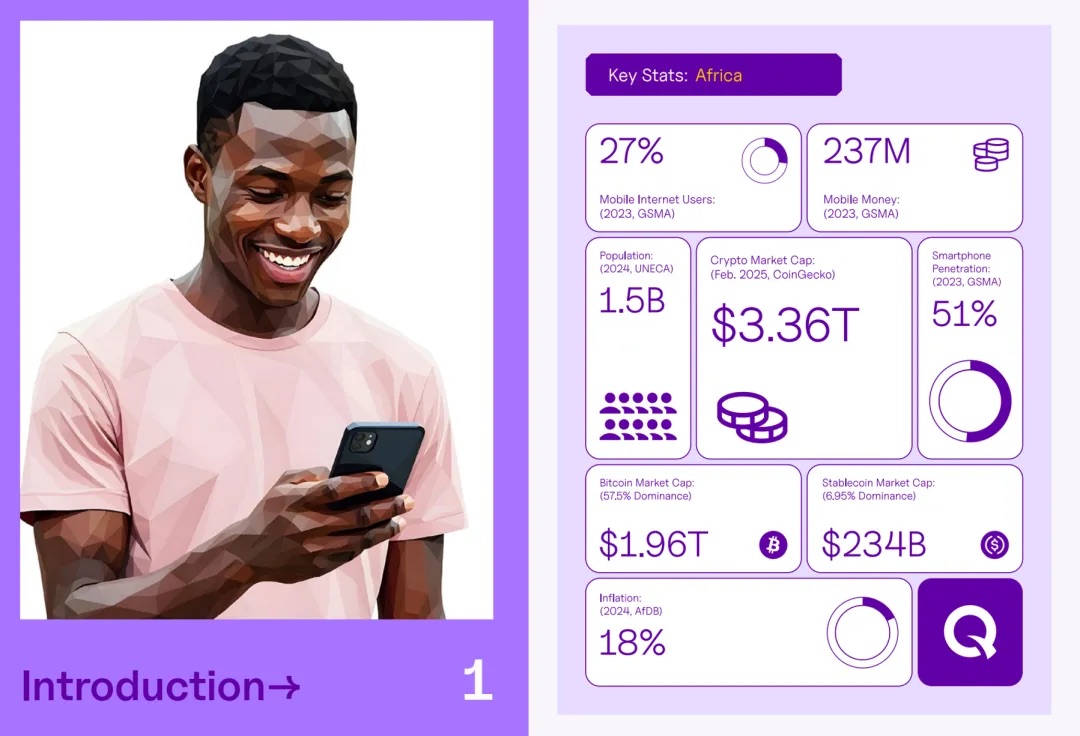

Africa's overall crypto landscape is undergoing rapid transformation: with a median age of just 19.2 and over 60% of the population unbanked, this creates a unique "demographic + economic" dual engine driving digital financial solutions. Cryptocurrencies have evolved from retail speculation to practical applications, particularly in cross-border payments and as a hedge against inflation. Nigeria processed approximately $59 billion in cryptocurrencies last year, ranking second globally after India. South Africa and Kenya are also showing strong momentum, driven by mobile wallet integration and relatively crypto-friendly policies.

Stablecoins have become the dominant asset for settlements, accounting for 43% of all crypto transactions in Sub-Saharan Africa (SSA). Their popularity stems from their price stability, real-time settlement, and transparent auditability. Nigeria alone accounts for over 40% of SSA's stablecoin inflows, while Ethiopia and Zambia both see annual growth rates exceeding 100%. Businesses are using stablecoins like USDT and USDC to hedge against foreign exchange fluctuations, streamline import processes, and accelerate cross-border settlements. Stablecoin trading volume has surpassed Bitcoin in most African regions.

Despite remaining cautious, many African governments are shifting from prohibition to participation. Nigeria's issuance of crypto licenses in 2024 was seen as a turning point, sparking a new wave of business interest. Countries like Ghana, South Africa, and Kenya have also launched central bank digital currencies (CBDCs) and regulatory sandboxes, providing a clear path to compliance. Executives from companies like Busha and Xago, interviewed for the report, called for a hybrid model that prioritizes innovation, governance, and risk management.

OTC trading has achieved product-market fit across multiple industries: banks and payment providers are integrating stablecoin corridors into their capital flows; manufacturers and importers are using OTC swaps to mitigate slippage and bank fees; and digital businesses are leveraging crypto corridors for rapid user deposits and real-time settlement. Quidax's expansion into South African Rand (ZAR) and Ethiopian Birr (ETB) corridors demonstrates industry momentum. Infrastructure provider Kotani Pay is integrating API-based stablecoin-fiat currency exchange directly into the mobile wallet ecosystem.

The regulatory stance is shifting from a blanket ban to a licensing and sandbox model. In 2024, the Nigerian SEC issued operating licenses to several virtual asset service providers; the South African FSCA has also issued dozens of crypto asset licenses. However, the regulatory frameworks of more than 15 African countries vary, creating compliance complexities for cross-regional players. Despite caution, many governments are shifting from bans to regulations. Nigeria's 2024 licensing system marked a watershed moment, reigniting business enthusiasm. CBDC and sandbox initiatives in Ghana, South Africa, and Kenya are paving the way for compliance. Industry leaders such as Busha and Xago called for a hybrid model that prioritizes innovation, governance, and risk control.

Looking ahead, programmable stablecoin channels and API-driven OTC platforms will recede into the background, becoming the "invisible infrastructure" of enterprise ERP and fintech applications, alongside frameworks like the African Continental Free Trade Area (AfCFTA) to support cross-border trade in Africa. Institutional-grade crypto asset reserves and CBDC pilots in multiple West and East African countries will further blur the boundaries between fiat and crypto settlements, ushering in a new era of "24/7, USD-equivalent" liquidity in Africa.

1. Overview of the African Crypto Market

The rise of cryptocurrency in Africa mirrors the global evolution of fintech and digital currencies, both closely tied to the mobile phone revolution that swept the continent in the early 2000s. The rapid adoption of mobile and internet technologies over the past three decades has laid the foundation for digital transformation across all industries. This shift, fueled by a young, tech-savvy population, has also provided fertile ground for the adoption of blockchain, the underlying technology of cryptocurrency.

In Africa, where more than 60% of the population does not have bank accounts, blockchain has quickly become popular in the financial sector, providing a fast and low-threshold solution for cross-border payments and digital asset transactions.

Initially, crypto assets were embraced as a means of storing value for individuals and as payment gateways for businesses, driven by a desire to hedge against inflation and circumvent capital controls. Today, this trend continues: over-the-counter (OTC) cryptocurrency trading is providing global businesses with a seamless capital flow experience, bypassing the traditional banking system's numerous obstacles, including foreign exchange volatility, settlement delays, and complex cross-border compliance. With the growing popularity of Bitcoin, Ethereum, Tether, and other stablecoins, African businesses are viewing cryptocurrencies not just as tools but as a reliable, fast, and transparent financial infrastructure capable of replacing outdated legacy systems.

1.1 The Evolution of Cryptocurrency in Africa

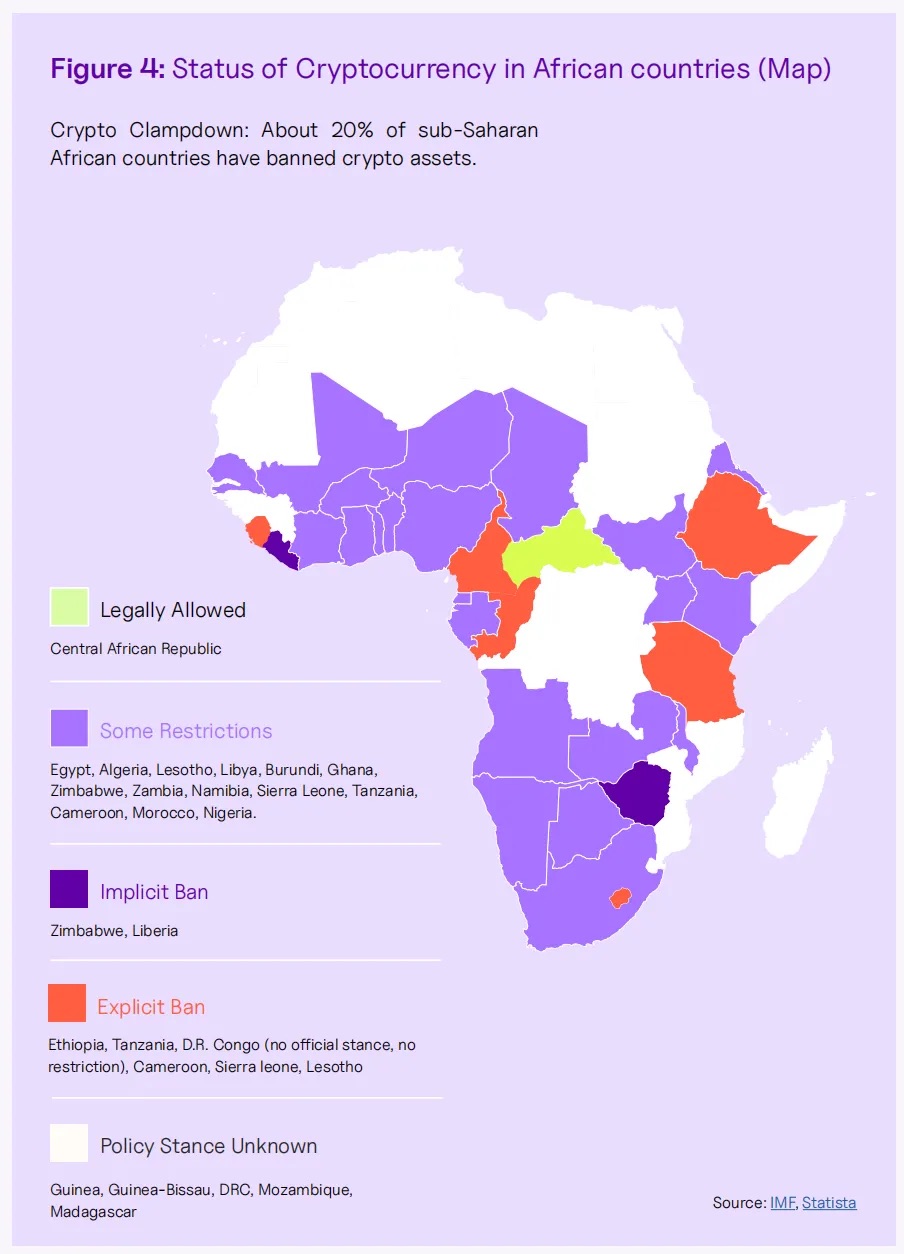

The decentralized and unregulated nature of cryptocurrencies is seen as a potential threat to the status of legal tender, thereby undermining the role of monetary authorities. Governments are also concerned that digital assets could be used for unregulated, illegal transactions. In many African countries, central banks and financial regulators initially reacted with caution. Consequently, countries such as Nigeria, Tunisia, Egypt, Lesotho, and Algeria have successively banned the use of cryptocurrencies in official transactions. However, due to the decentralized nature of cryptocurrencies, no single government can completely ban them, and underground transactions remain active.

As major economies around the world (such as the United Kingdom, the United States, and Canada) have successively enacted laws and gradually accepted cryptocurrencies and digital assets, more and more multinational companies - Microsoft, Tesla, PayPal, KFC, etc. - have also begun to accept cryptocurrencies represented by Bitcoin for payment.

As a result, global acceptance of cryptocurrencies has gradually permeated Africa, bolstering local users' confidence that cryptocurrencies are the currency of the future. As trading volumes continue to expand, some African countries have begun to relax their bans—Nigeria, Tunisia, Senegal, Sierra Leone, and Ghana, among others—or have begun researching central bank digital currencies (CBDCs) as regulated alternatives to crypto. These include Nigeria, Egypt, Morocco, Algeria, and Kenya. In April 2022, the Central African Republic (CAR) went a step further, passing a bill designating Bitcoin as legal tender alongside the CFA franc; the bill was subsequently suspended pending approval from the Bank of Central African States (BEACS). In February 2025, CAR launched a meme coin.

1.2 Cryptocurrency in the African Business Landscape

Today, Africa's crypto ecosystem continues to evolve as more governments embrace the vast potential of cryptocurrencies—value creation, smart transactions, and tax revenue. However, as in other parts of the world, African businesses are taking the initiative and daring to be first.

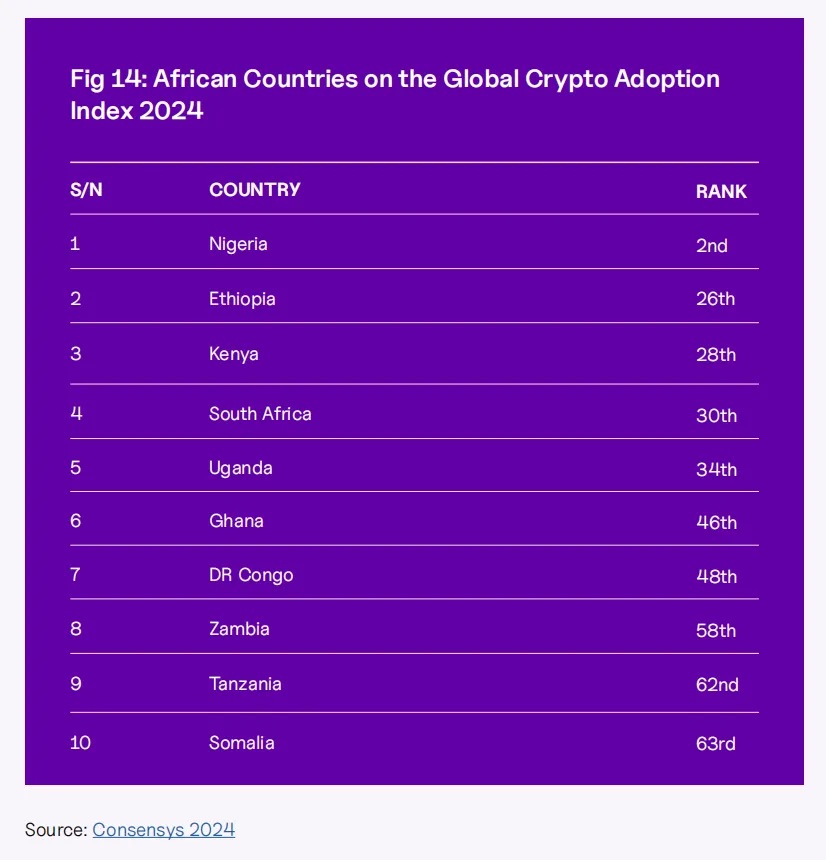

Although Sub-Saharan Africa (SSA) only accounts for $4.8 trillion in crypto transactions, representing 2.7% of global transactions (compared to 7.5% in the Middle East and North Africa (MENA) region), local businesses are already using cryptocurrencies for everyday payments, inflation protection, and more frequent, smaller (retail-level) transfers. According to Chainanalytics' 2024 Global Cryptocurrency Geography Report, stablecoins already account for 43% of transaction volume in Sub-Saharan Africa (SSA). Nigeria ranks second globally in crypto adoption (after India), with Ethiopia (26th), Kenya (28th), and South Africa (30th) also ranking in the top 30.

The report also shows that SSA leads the world in decentralized finance (DeFi) adoption, likely due in part to the region's urgent need for accessible financial services: World Bank data shows that as of 2021, only 49% of adults in the region had a bank account. Companies are also using stablecoins to hedge foreign exchange risks.

Faced with this trend, African central banks remain generally cautious, but still leave a "policy observation window" to reserve possible compliance space for crypto assets.

The 2020 COVID-19 pandemic, the 2021 Russia-Ukraine conflict, and efforts to promote regional integration have all been key turning points in Africa's cryptocurrency adoption process. The African Union's High-Level Panel of Experts on Emerging Technologies (APET) encourages the development of alternative payment methods, such as blockchain and cryptocurrencies, to facilitate cross-border transactions, increase financial inclusion, and reduce transaction costs.

2. Crypto OTC Trading in Africa

Over-the-counter (OTC) trading is rapidly becoming an alternative channel for acquiring cryptocurrencies in Africa.

Financial markets are generally organized in two ways: exchanges and over-the-counter (OTC) trading. Exchanges (such as stock exchanges or various cryptocurrency exchanges) publicly match buyers and sellers. All trades are completed on the exchange, and all traders can see the transaction price of all assets, regardless of whether they participated in the transaction.

Over-the-counter (OTC) transactions, on the other hand, take place directly between two parties, one of whom is typically a "trading desk." A trading desk is a commercial entity that specializes in buying and selling a specific type of asset. In OTC transactions, the two parties agree on a price before the trade is executed; only the two parties know the transaction volume and price.

In the context of cryptocurrencies, OTC trading, unlike exchange-based trading, involves privately matching buyers and sellers outside of regular exchanges. This allows for large-scale, direct transactions of crypto assets to avoid impacting market prices. However, OTC trading often carries higher counterparty risk than exchanges.

As trading scales up, OTC trading is rapidly becoming an important alternative way to acquire cryptocurrencies in Africa.

There are two types of OTC trading counters: principal desk and agency desk.

Principal trading desks use their own funds to buy and sell crypto assets for clients, assuming the risk of price fluctuations during the trading window. For example, if a client requests to purchase 500 BTC, the principal trading desk will first purchase the 500 BTC with its own funds and then deliver it to the client at the agreed-upon price. Even if the market price rises during this period, the desk will bear the price difference.

Brokerage desks act solely as matchmakers between buyers and sellers, using no capital. If the price moves unfavorably before a transaction is completed, the client must adjust their quote and assume market risk. Brokerage desks charge a matching service fee.

2.1 Global Cryptocurrency Over-the-Counter (OTC) Trading

Finery Markets data shows that driven by institutional capital inflows and positive macroeconomic conditions, the global cryptocurrency OTC market experienced significant expansion in 2024, primarily driven by surging demand for stablecoins and increased crypto-to-crypto trading. Bitcoin accounted for 22% of total OTC trading volume, with OTC market turnover increasing by 106% year-over-year, and stablecoin trading volume by 147%, highlighting an active year for institutional and large-scale digital asset trading.

Key events behind this growth include:

Spot ETF launch: The approval of Bitcoin (BTC) and Ethereum (ETH) spot ETFs provides institutional investors with a compliant and convenient entry channel.

Regulatory benefits: The pro-crypto stance shown by the Trump administration after taking office has significantly boosted the scale of spot trading in the fourth quarter of 2024, brought greater regulatory certainty, and further stimulated institutional participation.

Both prices and stablecoins are high: In December, Bitcoin broke through $100,000 and set a new record high; at the same time, stablecoins consolidated their market dominance as the main bridge between traditional finance and digital finance.

Geographical distribution: Europe leads institutional spot OTC demand with a share of 38.5%, while North America, Asia and the Middle East each account for 15.4%.

2.2 Advantages of OTC Trading

Over-the-counter (OTC) crypto settlement has become a vital complement to the exchange market, particularly suited for businesses requiring large-scale, fast, and compliant digital asset settlement. The following five core advantages warrant the attention of global businesses:

Deep Liquidity

OTC desks aggregate large buy and sell orders outside of exchanges, enabling businesses to complete large-scale crypto asset or stablecoin trades in one go, without splitting up their order books. Trades are fully executed at the negotiated price, avoiding the partial fills and slippage common on public exchanges.

Compliance and transparency

Well-known OTC platforms (such as Quidax) implement comprehensive KYC/AML, whitelist counterparties and wallet addresses, provide auditable transaction links at any time, and hold local licenses (such as the Nigerian SEC and the South African FSCA), providing sufficient protection for financial and compliance teams.

Fast settlement

Unlike traditional banking channels with clearing cycles of several days, OTC crypto settlements (especially stablecoins) are usually completed within minutes, significantly reducing settlement risks and accelerating working capital turnover.

Easily accommodate large transactions

The OTC counter focuses on single transactions with a six-digit or even seven-digit USD volume, which can be completed within a single order, avoiding large orders that impact the open market and cause drastic price fluctuations, thereby ensuring price stability.

Personalized service and bargaining space

OTC counters offer customized quotes, flexible settlement methods (fiat currency or stablecoins like USDT/USDC), and direct negotiation, allowing businesses to flexibly design transaction structures based on their cash flow needs, hedging strategies, and treasury policies. OTC transactions are conducted privately, outside of exchanges, making them particularly suitable for large-value transactions, ensuring that transaction details remain private.

2.3 How OTC transactions can solve the pain points of global companies in Africa

Over-the-counter (OTC) crypto counters, with their unique positioning, can precisely address the challenges multinational companies have long faced when operating in Africa. The following sections will map these pain points and OTC solutions, supplemented by mini-scenario illustrations.

Foreign exchange fluctuations

Pain point: The local currency exchange rate changes rapidly, and banks' large-scale foreign exchange settlements can easily erode profits.

OTC solution: Settle in USD-anchored stablecoins (USDT/USDC) or mainstream crypto assets, lock in the exchange rate during transactions, and hedge intraday FX risks in real time.

Scenario: A Nigerian importer enters into a 30-day USDT contract with an OTC counter to pay a major supplier, successfully avoiding the mid-month NGN/USD exchange rate jump.

Cross-border payments are complex

Pain point: Multi-step correspondent bank transfers bring delays, fees, and operational complexity.

OTC solution: On one end, the local currency is exchanged for a stable currency, which is transferred instantly on the chain, and on the other end, it is directly exchanged for the recipient's fiat currency. A single transaction can close the loop.

Scenario: A Ghanaian NGO disburses funding to its Kenyan partner in USDT through the Quidax OTC counter, which is then converted into KES within minutes.

Exchange slippage

Pain point: Large orders impact the market, resulting in slippage and hidden costs.

OTC solution: The OTC completes large-scale transactions at pre-agreed prices using its own liquidity or bilateral matching, with minimal market impact.

Scenario: An African fintech company needs to purchase 5 BTC for its reserves and trades it over the counter at a fixed price to avoid 2% slippage.

Comply with local currency regulations

Pain point: Currency controls and AML/KYC requirements vary from country to country, making implementation cumbersome.

OTC solutions: Licensed OTC service providers (such as Quidax) provide one-stop KYC/AML access and customize settlement paths based on the legal currency channels and legal frameworks of various countries.

Scenario: A European exporter completed the entire process of SEC-VASP compliance, local beneficiary bank declaration, and Euro to Naira stablecoin to partner bank account through Quidax's Nigeria OTC counter, all in one go, with auditable documentation.

Optimize supplier/partner payment process

Pain points: Manual foreign exchange purchases and multiple bank transfers tie up working capital, and the approval process is lengthy.

OTC Solutions: A dedicated account manager can negotiate billing terms, issue settlement instructions, and automate recurring payments via API or scheduled calls.

Scenario: A pan-African agricultural group sets up weekly OTC swaps to convert its USD cash position into NGN stablecoins, allowing it to pay multiple suppliers in Lagos directly without requiring repeated bank approvals.

Platform users make batch payments

Pain points: In high-frequency issuance scenarios such as the gig economy and gaming platforms, banks have slow approval processes and high fees.

OTC solutions: Over-the-counter (OTC) solutions can execute stablecoin issuance or direct crypto transfers in batches, reaching end users in areas with weak banking infrastructure.

Scenario: A Nigerian digital platform makes instant, low-fee payments in USDT to tournament winners via OTC, allowing players to withdraw funds immediately to their personal wallets.

2.4 African OTC Company Quidax

Quidax is a licensed and regulated cryptocurrency exchange founded by an African team, making it easy for anyone to buy, sell, store, and transfer crypto assets. Its core expertise lies in over-the-counter (OTC) trading. Quidax provides businesses and fintech companies with a dedicated crypto API, seamlessly integrating high-volume, compliant settlement into existing platforms.

Quidax operates under dual licenses, holding both Canadian MSB and Nigerian Securities and Exchange Commission (SEC) VASP licenses. Since its official launch in 2018, Quidax has served users in over 70 countries and has localized teams in key African markets. The platform offers direct fiat currency access, supporting multiple African currencies, including the Nigerian Naira (NGN), South African Rand (ZAR), and Ethiopian Birr (ETB). The Quidax OTC counter allows for single transactions exceeding $100,000 USD, with instant settlement in fiat currency or USDT, providing a seamless corporate payment experience.

2.5 How can key African industries leverage over-the-counter (OTC) trading?

OTC business use cases at a glance:

Use Case 1: Cross-border Trade and Commerce

Pain point: International brands and distributors face high costs and lengthy payment cycles when settling accounts with local partners in multiple African markets.

Solution: Through OTC stablecoin transactions, companies can purchase digital dollars (USDC, USDT, etc.) at preferential exchange rates, and then use Quidax OTC to instantly convert them into local fiat currency, achieving fast and compliant settlement.

Results: Settlement time reduced from days to hours; foreign exchange fees significantly reduced; cash flow and supplier relationships improved simultaneously.

Use Case 2: Digital Platforms and Consumer Applications

Pain point: Large global digital platforms targeting users on the African continent need to quickly pay local partners and service providers while strictly controlling operating costs.

Solution: The platform purchases stablecoins in bulk through the Quidax OTC counter and instantly converts them into local fiat currency, completing efficient and reliable account splitting.

Results: Partners' payment processing time was significantly reduced; transaction and foreign exchange fees were reduced; and OTC processes were embedded in automated treasury workflows.

Use Case 3: Institutional and Fund Operations

Pain Point: Financial institutions, corporate groups, and investment groups urgently need reliable, compliant, and scalable solutions to transfer large amounts of value into or out of African countries.

Solution: Quidax OTC trading supports large single transactions, guarantees execution, provides local fiat currency channels, and complies with regulatory requirements.

Results: Improved fund management capabilities; increased confidence in regulatory compliance; and frictionless expansion of cross-border business.

Case Study I: Simplifying Cross-Border E-Commerce Settlements in Africa

NevaCommerce is a global digital commerce services company headquartered in Europe. Through its partnership network in emerging markets, NevaCommerce helps international brands connect with distributors and end customers in Nigeria, South Africa, Kenya and other regions.

Challenges

When using traditional banking channels to settle large payments to partners in local currency, fees are high and payment processing is slow.

Exchange rate fluctuations and high exchange costs erode profits.

The regulatory complexity of cross-border transactions creates operational challenges.

Solution

Cooperate with Quidax OTC counter to adopt stablecoins for cross-border settlement.

Gain competitive large-scale liquidity and exchange rates through OTC transactions.

With Quidax OTC, stablecoins can be seamlessly converted into local fiat currency, allowing for quick and compliant payments to partners.

Results

Settlement time has been reduced from up to 5 days to less than 1 hour.

Save up to 2% on forex spreads and fees per trade.

Faster, more reliable payment methods strengthen local partnerships.

The key difference OTC brings

Customized quotations and single large-amount processing capabilities.

Private, secure, and compliant trade execution.

Support local currencies and meet regulatory requirements, so you don’t have to worry about compliance.

“For the first time, our finance and operations teams can quickly and cost-effectively settle transactions in Africa – OTC has completely transformed our business.” — NevaCommerce, CFO

Case Study II: Simplifying Localized Partner Settlement in Africa

Global Platform Co. is a fast-growing international digital platform with millions of users and partners in African markets including Nigeria, South Africa, and Ghana.

Challenges

Settlement with local partners and service providers is slow and costly.

Market pressure requires shortening payment cycles to improve user experience and partner satisfaction.

Traditional payment methods have poor flexibility and high transaction fees.

Solution

Integrate Quidax OTC counter and use stablecoins for batch settlement.

Get deep liquidity and the best exchange rates through OTC transactions.

Instantly convert stablecoins into local fiat currency and make payments to African partners quickly and compliantly.

Results

Partner settlement time has been reduced from 48 hours to less than 4 hours.

Operating expenses are reduced and capital efficiency is improved.

OTC transactions have been embedded in the daily global settlement process.

The key difference OTC brings

Provide stable and locked-in quotes on high-value transactions.

Seamless integration via API for automated settlement.

Leverage Quidax license and local expertise to ensure compliance coverage.

“With Quidax OTC, our treasury team has the flexibility, speed, and regulatory compliance required to seamlessly serve the African market.” — CFO of Global Platform Co.

3. Payment Trends of Stablecoins in Africa

As with other regions globally, Africa's stablecoin market has matured, surpassing Bitcoin as a preferred asset for daily transactions. With the exception of North America, where stablecoin trading only slightly outpaces Bitcoin, stablecoin trading volumes in all regions exceed Bitcoin by more than double.

In Africa, high inflation and currency depreciation have eroded people's wealth, so stablecoins are used as a hedge against currency instability, providing a more reliable means of trading and preserving value.

Foreign exchange fluctuations led to retail and small-to-medium-value stablecoin transfers accounting for as much as 43% of all crypto transactions last year.

Currently, the growth of stablecoins in Africa is primarily driven by small transfers under $1 million—retail and non-institutional transfers. Sub-Saharan Africa (SSA) is the fastest-growing region for both retail and professional stablecoin transfers, with annual growth exceeding 40%. Last year, stablecoins accounted for 43% of all cryptocurrency trading volume in SSA.

3.1 Stablecoin adoption in Africa continues to heat up

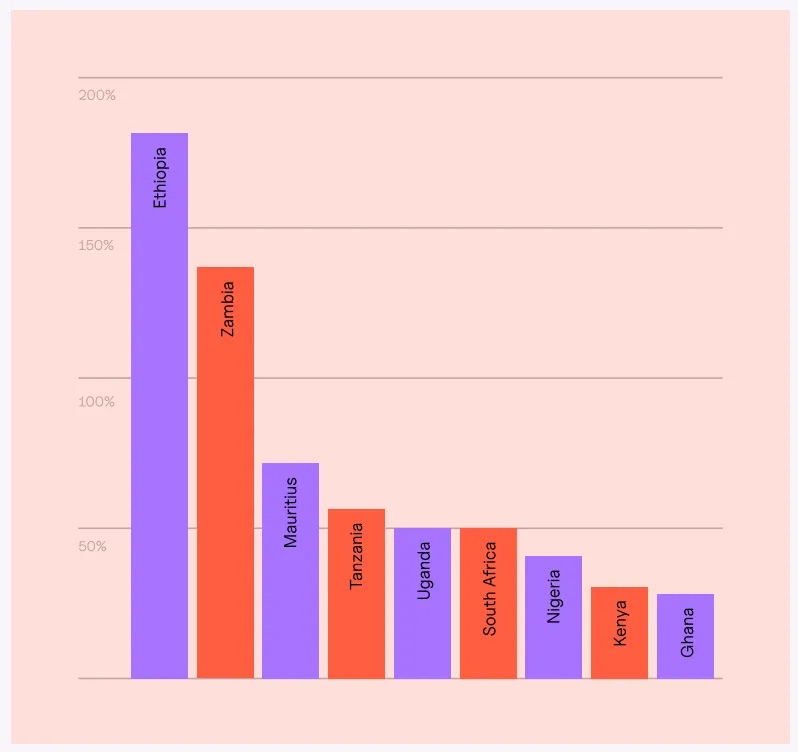

While Nigeria and South Africa lead stablecoin adoption, countries like Ethiopia, Zambia, Mauritius, Kenya, and Ghana are also rapidly increasing their use. The chart below shows the year-over-year growth in retail-level (less than $10,000 per transaction) stablecoin transactions in Sub-Saharan Africa (July 2022–June 2023 vs. July 2023–June 2024).

Ethiopia and Zambia both saw annual stablecoin growth exceeding 100% over the past year. Ethiopia was the fastest-growing market for retail stablecoin transfers, with an annual growth rate of 180%. The Ethiopian birr (ETB) depreciated by 30% in July after the government relaxed currency controls to secure a $10.7 billion IMF and World Bank loan. This loss in value is expected to further fuel demand for stablecoins. Crypto activity in Nigeria is primarily driven by small retail and professional transactions, with approximately 85% of transactions occurring in amounts below $1 million. Nigeria has received over $20 billion in stablecoin inflows in Sub-Saharan Africa, representing over 40% of all transactions.

Meanwhile, alongside the growing prominence of stablecoins, decentralized finance (DeFi) is also experiencing a significant moment in Nigeria, echoing the broader trend of Sub-Saharan Africa leading the world in DeFi adoption.

3.2 The role of stablecoins in mitigating cryptocurrency price fluctuations

Stablecoins play a key role in the crypto ecosystem by addressing one of the most vexing issues in the crypto space: price volatility. Cryptocurrencies like Bitcoin and Ethereum can experience dramatic fluctuations in value over short periods of time, making them difficult to use as a medium for daily transactions or as a reliable store of value.

According to S&P Global Ratings, stablecoins enable near-instant final settlement within minutes during over-the-counter (OTC) transactions, compared to days typically required by traditional methods. Slippage is minimal (typically less than 1%, a significant advantage compared to foreign exchange fees of 5–10%). Furthermore, the immutable blockchain record enhances Know Your Customer (KYC)/Anti-Money Laundering (AML) transparency and compliance. As a programmable, 24/7 "dollar rail," stablecoins enable African businesses, fintech companies, and telecom-finance ecosystem partners to expand cross-border payment corridors without the need for new banking infrastructure.

3.3 Related Data

Although Sub-Saharan Africa (SSA) accounts for a small portion of global crypto trading volume, several indicators show that the region has promising prospects in the cryptocurrency field.

YouGov 2024 Survey Data:

93% of respondents worldwide said they had heard of cryptocurrencies, with 51% saying they had "some knowledge" about them.

Sub-Saharan Africa (SSA) accounts for only 2.7% of global trade volume.

Nigeria is projected to receive approximately $59 billion worth of cryptocurrency in 2024, ranking second (after India) in the Global Crypto Adoption Index.

The "willingness to invest in crypto in the future" among African respondents is as high as 87%, higher than other regions in the world.

In terms of "understanding" of encryption, Nigeria (77%), South Africa (65%), South Korea (61%) and India (60%) are at the top of the list.

In terms of the proportion of people who "have or currently hold crypto assets", more than half are in Nigeria (73%), South Africa (68%), the Philippines (54%), Vietnam (54%) and India (52%).

Chainalysis' 2024 Global Crypto Geography Report

Sub-Saharan Africa (SSA) still accounts for the smallest share of global deal volume, at 2.7%.

Stablecoins already account for approximately 43% of the region’s total trading volume.

Nigeria is expected to receive approximately $59 billion worth of cryptocurrencies in 2024, ranking second in the global adoption index.

3.4 Interview with Buchi Okoro, CEO of Quidax

Q: What key consumer behavior changes have you observed in Africa regarding cryptocurrency adoption over the past two years?

A: The most obvious shift is from "speculation" to "real-world application." Early on, most users viewed crypto assets as investment tools. Today, we're seeing a significant increase in their use in everyday transactions—more and more consumers are using cryptocurrencies for cross-border payments and even directly for e-commerce purchases.

Q: In your opinion, what structural or fundamental barriers are preventing the large-scale adoption of cryptocurrencies for commercial transactions in Africa? And can these barriers be changed or improved?

A: Lack of regulation is one of the biggest obstacles, making many businesses in the African market hesitant to use cryptocurrencies. But this can be changed. We are seeing some positive signs: countries like Nigeria have introduced regulatory frameworks, including digital asset exchange licenses, which have greatly boosted market confidence and given consumers a greater sense of security. If this model can be replicated in more African countries, it will create an environment where businesses can seamlessly embrace crypto. What is needed is balanced regulation—regulators working together with compliant crypto businesses to maintain appropriate oversight while encouraging innovation and protecting users.

Q: Looking ahead to the next 2–3 years, how do you see the African cryptocurrency market evolving? What changes are likely to occur in the short and long term?

A: In the short term, more African countries will introduce regulatory frameworks, ushering in a "wave of regulation" for the industry. This will create a structural order, legalize cryptocurrencies in various countries, and provide consumer protection. In the long term, cooperation between traditional financial institutions and crypto companies will become increasingly close. Central banks in some countries will also launch central bank digital currencies (CBDCs) in response to the growing crypto ecosystem.

Q: Which key markets are worth focusing on? What are the core factors driving cryptocurrency adoption in these African markets?

A: Nigeria, Ghana, Kenya, Rwanda, Tanzania, and South Africa. Large and young consumer groups, relatively well-developed financial infrastructure, and forward-looking technology policies will become the three major engines of growth in these markets.

Q: How will OTC trading desks evolve in Africa? Is full decentralization realistic, given fraud cases and corporate governance issues?

A: Over the next few years, as the regulatory framework matures, the OTC market will see a more pronounced trend toward institutionalization. Over-the-counter (OTC) trading platforms will adopt more standardized operating procedures, focusing on more rigorous risk management and compliance practices. Technology will also be upgraded: more automated systems, enhanced custody and escrow capabilities, and more will be introduced.

Q: How are African businesses currently exploring OTC platforms? What are some interesting use cases, key players, and industries or sectors? Which areas are showing the fastest growth and greatest opportunities?

A: The use cases are diverse: cross-border trade settlement for importers and exporters, payment channels for international suppliers, and hedging against local currency fluctuations through OTC transactions. The import/export, technology, and e-commerce sectors are actively capitalizing on the opportunities presented by OTC transactions.

Q: How can regulators effectively collaborate with industry participants to promote the growth of the crypto industry? Is it possible to achieve pan-African crypto regulatory cooperation based on the African Continental Free Trade Area (AfCFTA) model?

A: Regulatory sandboxes are an excellent approach—allowing industry players to experiment first in a controlled environment. Regular public-private dialogue is also crucial, enabling regulators and industry players to understand each other and jointly develop rules. The Nigerian Securities and Exchange Commission (SEC)'s engagement with crypto stakeholders is exemplary. As for pan-African cooperation, it's entirely feasible: in the future, it could promote unified consumer protection policies and achieve mutual recognition of licensed institutions.

Q: Looking ahead to the next 2-3 years, how do you foresee the regulatory landscape for cryptocurrency in Africa evolving?

A: I believe that regulation will become more segmented, with clear distinctions between different types of crypto activities—trading, payments, asset tokenization, fundraising—and tailored rules for each type of activity.

3.5 Interview with Moyo Sodipo, Co-founder of Busha

Busha is a licensed cryptocurrency exchange and payment platform headquartered in Nigeria and serving the African market. It was founded in 2018 and obtained the first batch of digital asset temporary licenses issued by the Nigerian Securities and Exchange Commission (SEC) in 2023, becoming one of the first compliant crypto exchage in Nigeria.

Q: In your opinion, what structural or fundamental barriers are hindering the widespread adoption of cryptocurrencies in commercial transactions in Africa? Can these barriers be changed or improved?

A: Lack of regulatory clarity has always been a significant stumbling block. Nigeria has no clear regulatory framework for cryptocurrencies until August 2024, which means many individuals and businesses that might otherwise be interested in crypto and digital assets are taking a wait-and-see approach to our industry. Consequently, we've had to put a lot of effort into persuading and explaining things before people actually start using cryptocurrencies. Thankfully, the Nigerian government, under the leadership of the new SEC Director-General, has decided to begin regulating cryptocurrencies, which offers a glimmer of hope.

Q: What key consumer behavior changes have you observed in Africa regarding cryptocurrency adoption over the past two years?

A: The biggest change I've seen is people's growing awareness of the importance of cryptocurrency settlements. Looking back at Nigeria, crypto first gained widespread attention during the 2017 bull market. Prior to that, the MMM Ponzi scheme was prevalent in Nigeria, and many people confused Bitcoin with MMM. That was the first wave of public exposure to cryptocurrency that I can recall. The second wave came when forex trading became popular—due to limited access to foreign exchange in Nigeria, people used cryptocurrency to fund their trading accounts, a trend that continues to this day. Overall, crypto has evolved from a simple tool for speculation to a payment method that can be integrated into daily life. Today, we're seeing increasing discussion about the adoption of stablecoins in various scenarios.

While cryptocurrencies haven't yet gained full acceptance in Nigeria, globally, the use cases for stablecoins are expanding, demonstrating how they can transform intercontinental remittances. With the implementation of Nigeria's licensing system, we'll see more businesses accepting not only cryptocurrencies but also stablecoins as a means of payment in the coming years. Imagine buying a plane ticket and being offered the option to "pay with a stablecoin" at checkout—the possibilities are endless. I believe we're experiencing a shift from a "get rich quick" narrative to a "practical payment tool" narrative.

Q: Looking ahead to the next two to three years, how do you see the cryptocurrency settlement landscape evolving in Africa? What short-term and long-term changes might we see?

A: Cryptocurrency acceptance and adoption will inevitably increase. I believe within two to three years, we'll see crypto being used for everyday consumption. Once African countries launch stablecoins pegged to their national currencies, cross-border transactions will become much simpler. Imagine a Kenyan Shilling (CKS) and a Nigerian Naira (CNGN) stablecoin. I wouldn't need to have a bank account in Kenya to trade between Nigeria and Kenya. This is the future I envision—digital versions of national currencies running on a blockchain, enabling intra-African trade without the need for physical US dollars. In the coming years, stablecoins in different currencies will be widely traded, boosting intra-African trade without relying on physical US dollars.

Q: Looking ahead to 2025, what is the overall outlook for cryptocurrencies and OTC trading in Africa?

A: The outlook is very positive. This year, in particular, it's been very positive: as we look across African jurisdictions and market participants, we're seeing a growing willingness to use stablecoins for a variety of purposes—whether it's storing value, sending money across borders, or paying suppliers directly. The discussion is much more intense than last year. It's clear there's a genuine interest in exploring this new technology to ensure faster, smoother, and more efficient business operations.

3.6 Interview with Jurgen Kuhnel, Xago CEO

Xago Technologies (Pty) Ltd is a South African fintech company founded in 2016 and headquartered in South Africa. Leveraging the speed and scalability of the XRP Ledger, the company provides efficient and secure digital payment and crypto asset trading services.

Q: As a frontline practitioner, what key changes have you observed in the adoption of cryptocurrency by African consumers over the past two years?

A: It's difficult to talk about the overall crypto evolution in the African consumer market, as our business scenarios are very focused. However, we've seen a surge in stablecoin growth in Africa—explosion is an understatement. The use of USDT and USDC has skyrocketed, with USDT being the most widely accepted. I often say that a few years ago, everyone was talking about M-Pesa in Kenya: mobile money emerged out of nowhere, and with some kind of government support, it now controls approximately 55% of Kenya's GDP. USDT is like the "unannounced M-Pesa," sweeping Africa.

I mean, when you talk to the average person in Africa, they don't really care if USDT is 100% backed by dollars, if it's on Tron or Ethereum, if it's at a premium or a discount—they know exactly how to use it. I think this virality is going to catch a lot of people off guard.

Q: Looking ahead to the next two to three years, how do you see the African cryptocurrency market evolving? What changes are likely to occur in the short and long term?

A: From our perspective, the trend is very clear. As the regulatory framework gradually takes shape, more and more "big players" are entering the market. Take the US: giants like BlackRock are launching Bitcoin ETFs on the stock market; governments are also beginning to use Bitcoin as a hedge for their own currencies and foreign exchange reserves. Even a tweet from Trump can influence the price of Bitcoin. Over a dozen US states have already introduced bills, and Trump recently signed an executive order. Once the US takes this step, the rest of the world will quickly follow.

Major American companies have already accumulated significant amounts of Bitcoin. Some argue that "cryptocurrency is still in its infancy" and "will explode," but the reality is that it has already exploded—it's already ubiquitous. I personally haven't met anyone who hasn't heard of Bitcoin, but perhaps there are one or two who are truly "isolated."

Now, look at my 16- and 17-year-old children. In ten years, they'll be the primary consumers and will have no psychological barriers to cryptocurrency. In ten years, crypto will be as commonplace as mobile payments are today. Back to our roots: We invested in crypto because we needed an alternative. For example, if I wanted to send money to the UK, I'd traditionally have to use SWIFT; now I can buy cryptocurrency and send it directly across borders. For the world's major banks and payment giants, transitioning to this new paradigm will take time, but ultimately, crypto will become a parallel clearing platform.

Q: Which key markets in Africa are worth watching? What specific factors will drive crypto adoption in these markets?

A: Some ATMs in South Africa already allow direct cryptocurrency purchases and withdrawals. Some exchanges have also integrated with retailers, allowing purchases with cryptocurrencies. The South African market is already very mature.

Key markets are always those with the largest populations and economies: Nigeria and South Africa. They also have the highest adoption rates. Namibia is actively introducing licensed exchanges; in liquidity-constrained countries like Mozambique, cryptocurrencies can play a vital role. Generally speaking, African users prefer stablecoins over Bitcoin or XRP—they simply want to exchange their local currencies for stable assets like the US dollar. For Americans, the US dollar is depreciating; for Africans, it's the "hard currency" that anchors everything.

Q: You mentioned over-the-counter (OTC) crypto trading earlier. Can you elaborate on how companies are currently using OTC in practice?

A: OTC isn't typically used by individuals, but by businesses with urgent needs. For example, a company might be holding a large amount of Angolan currency but struggling to convert it to US dollars through a local bank. Since most African countries require US dollars to import goods and services, they turn to OTC. Another example is a South African-based company with operations in Angola that needs to remit funds back to South Africa. Traditional channels are impractical, so they might use crypto OTC.

Of course, this doesn't mean cryptocurrencies are "more reliable"; it simply offers an alternative. If traditional foreign exchange channels are smooth, bank endorsements are complete, and the CFO sign-off process is clear, companies will still prefer to stick with them. Only when traditional channels become blocked, particularly when liquidity issues arise, will companies try cryptocurrencies.

Q: Looking ahead, do you think cross-border payments in Africa will be driven extensively by cryptocurrency platforms and OTC counters, similar to how trade integration under the AfCFTA (African Continental Free Trade Area) has been?

A: I'm certainly optimistic about this scenario, but end users may not be aware that encryption is running in the background. As regulatory frameworks and reporting systems improve, cross-border settlement companies in South Africa, for example, will be able to legally use encryption. Currently, there are still obstacles, so encryption is only a backup option. In the future, encrypted settlement will run alongside traditional methods like SWIFT and Western Union and be integrated into existing networks. Open your bank app and you'll see: Should I use SWIFT or an encrypted channel to complete this transaction?

The more stablecoins (USDT/USDC) are used, the smoother their implementation will be. We already have a partner working on integration: users pay with their mobile wallets, and the final payment is USDC or USDT. A very successful company in Kenya is operating this mobile payment system.

4. Africa’s Crypto Regulatory Framework

For international companies entering Africa's burgeoning commercial landscape, the vastly different regulations, licensing systems, and compliance requirements often create a maze; any misstep could lead to frozen funds, hefty fines, and even brand damage. African regulators are increasingly stringent with their Know Your Customer (KYC)/Anti-Money Laundering (AML) requirements for large transactions. Partnering with unlicensed counterparties or anonymous P2P platforms exposes companies to significant legal action and fund recovery. The onboarding process for crypto OTC platforms like Quidax includes:

Automated global sanctions list screening;

Continuous transaction monitoring;

Complete customer due diligence.

Ultimately, an institutional-level compliance framework will be formed that is fully aligned with the highest global standards, ensuring that every dollar or stablecoin in circulation has an immutable audit trail on the chain, which is available for internal and external review at any time.

Many African countries implement strict foreign exchange controls and repatriation regulations, often leading to regulatory deadlocks in cross-border settlements. Quidax fully complies with the guidance of central banks and securities regulators worldwide through direct fiat currency access and stablecoin trading pairs pegged to local fiat currencies—the Nigerian Naira (NGN), the South African Rand (ZAR), and the Ethiopian Birr (ETB). This pan-African licensing model ensures that corporate funds settlements are not interrupted by unexpected freezes or detentions.

4.1 Treating Cryptocurrencies as Digital Assets Requiring Regulation

The general regulatory trend is to treat cryptocurrencies as "virtual or digital assets" (similar to real estate) and tax them accordingly. This is the case in the United States, the United Kingdom, and Canada: the US Internal Revenue Service (IRS) has declared that the same general tax principles that apply to real estate apply to crypto assets. South Africa and Nigeria have also proposed similar frameworks under their Virtual Asset Service Provider (VASP) regulations.

However, faced with a highly volatile and decentralized system, most governments are still seeking a balance between "controlling risks" and "promoting innovation." Data shows that only a quarter of countries in sub-Saharan Africa have formally regulated cryptocurrencies.

Although the pace is slow, African countries are shifting away from a hardline stance on cryptocurrencies. Currently, around 70% of African countries still have a “neutral” or “uncertain” policy stance on cryptocurrencies.

Nigeria

As one of the African countries with the highest crypto-asset holdings, Nigeria's regulatory environment has long been uncertain. In 2017 and again in 2021, the Central Bank of Nigeria (CBN) banned formal financial institutions from participating in crypto trading (which gave rise to peer-to-peer trading). Meanwhile, the Securities and Exchange Commission (SEC) of Nigeria continued to research the market, launching the Regulatory Incubation Program (SRIP) in 2021 and issuing the Digital Asset Rules in 2022. In 2023, the CBN issued the Virtual Asset Service Provider (VASP) Guidelines, which, while continuing to prohibit financial institutions from directly trading crypto assets, allowed them to provide settlement channels for crypto transactions. In 2024, the SEC released the Accelerated Regulatory Incubation Program (ARIP) framework and issued "Approval-in-Principle" to Quidax and Busha.

South Africa

On October 19, 2022, the Financial Sector Conduct Authority (FSCA) of South Africa officially classified crypto assets as financial products, regulated under Section 1(h) of the Financial Advisory and Intermediary Services Act (FAIS Act). This classification builds on a proposal by the FSCA in November 2020, requiring institutions providing crypto-related services to apply for licenses and report crypto asset transactions. Since June 2023, the FSCA has issued licenses to 59 crypto service providers.

Kenya

Like other countries, Kenya's stance on cryptocurrencies is evolving. In December 2024, the Kenyan Ministry of Finance released the draft National Policy on Virtual Assets and Virtual Asset Service Providers and the draft Virtual Asset Service Providers Bill. The draft policy states, "This policy aims to create a fair, competitive, and stable market for virtual assets (VAs) and virtual asset service providers (VASPs) in Kenya." The document comprehensively outlines the licensing, consumer protection, and cybersecurity regulatory framework for VA activities and VASPs. The government has opened these draft regulations for public comment until January 2025.

Egypt

In 2018, Egypt's top Islamic legislative body issued a religious decree classifying commercial transactions involving Bitcoin as haram, or prohibited under Islamic law. This position was reiterated in January 2021, providing no protection for losses incurred from crypto transactions.

The Central Bank and Banking System Law (Law No. 194 of 2020) explicitly prohibits the issuance, trading, or promotion of cryptocurrencies without prior approval from the Central Bank of Egypt (CBE). Article 206 of the law provides for severe penalties, including fines and imprisonment, for any unauthorized crypto-related activities.

Central African Republic

On April 22, 2022, the Central African Republic’s parliament passed a law establishing cryptocurrency as legal tender in the country. The law stipulates that cryptocurrencies coexist alongside the Central African Financial Cooperation Franc (FCFA), the current legal tender of the Central African Economic and Monetary Community (CEMAC).

However, CAR is a member of CEMAC, and currency issuance rights belong to the Bank of Central African States (BEAC). The BEAC Governor subsequently issued a statement declaring the new cryptocurrency law passed by CAR "null and void," claiming it violated the regional bloc's terms. In February 2025, CAR launched a meme coin as a countermeasure.

Other countries

While the Ethiopian government is gradually opening its economy to competition and digital technology, it remains cautious about crypto assets. High mining activity and rising adoption are forcing the state to reconsider its hardline stance. Tunisia, Senegal, and Sierra Leone have remained silent or neutral, and have yet to introduce legislation on cryptocurrency use. In Tunisia, the finance minister has stated that the current position criminalizing cryptocurrency traders needs to be reviewed. North African restrictions are even stricter: Egypt, Algeria, and Libya have already completely banned cryptocurrency use. In 2024, Morocco and Ghana released draft guidelines for cryptocurrency regulation.

4.2 Regulatory Challenges and Opportunities in the African Crypto Ecosystem

challenge

Regulatory uncertainty: Many African countries lack regulations permitting cryptocurrencies. While countries like Nigeria, Kenya, and South Africa are developing strategies around virtual asset service providers (VASPs), the ultimate direction remains unclear. Crypto assets are still viewed as a potential threat to monetary policy institutions.

The decentralized and unregulated nature of cryptocurrencies makes it difficult for governments to effectively regulate them. While attempts at central bank digital currencies (CBDCs) have not been particularly successful, regulated blockchains still hold potential.

Illicit Financial Flows: As mentioned above, cryptocurrencies provide opportunities for illicit financing; this is particularly problematic in Africa, where fraud and terrorist financing are increasingly rampant.

Price volatility: Cryptocurrencies, such as Bitcoin, are prone to significant market fluctuations, which can have devastating effects on household and business finances.

opportunity:

Improve financial inclusion: If regulators approve cryptocurrencies, it will facilitate collaboration between VASPs and traditional financial institutions, thereby enriching financial services and products.

Promoting cross-border trade within Africa: Through regulatory coordination at the continental level, cryptocurrencies have the potential to boost intra-African trade.

Improving payment efficiency: Cryptocurrencies, represented by stablecoins, have great potential to reduce transfer and settlement costs in Africa.

Hedging against inflation: Stablecoins are increasingly seen as a hedge against inflation and currency devaluation, helping to preserve the value of household assets.

4.3 Interview with Michael Kioneki, Founder of Blockchain Association of Kenya

Q: Please introduce the background of the Kenya Blockchain Association, its core mission, and the role it plays in the Kenyan blockchain ecosystem.

A: I am the founder and president of the Kenya Blockchain Association, established in 2015. I entered the industry in 2014, when the ecosystem was vastly different from what it is today, and I've witnessed its transformation. Until recently, I was the Head of Growth and responsible for business development at a startup called Fonbnk. Since 2014, I have worked with numerous crypto and fintech startups and was one of the earliest thought leaders to actively promote blockchain/crypto as fintech infrastructure. For the past decade, I have focused on educating the public and building the community. In 2023, we worked with the Association and a group of stakeholders to draft the Virtual Asset Service Providers (VASP) Bill and submit it to Parliament. My core goal has always been to promote the ethical adoption of blockchain in Kenya, the region, and Africa as a whole. This has already influenced numerous organizations outside of Kenya and foreign investors interested in this market.

Over the past decade, there have always been different key obstacles at different stages. Only by breaking through these obstacles can the ecology be pushed to new heights.

Q: Looking ahead to the next two years, how do you see the African crypto market evolving? What changes are likely to occur in the short and long term?

A: Overall, I believe the industry will move toward formalization. Countries like Kenya and South Africa have already passed or are in the process of implementing relevant legislation. The Nigerian government is also imposing taxes and requiring compliance on giants like Binance. Kenya is also pursuing tax reimbursements. Therefore, the core trend is formalization: companies will apply for licenses, open bank accounts, and pay taxes formally. This will make customer acquisition more transparent, and the industry will no longer be "gray." Crypto companies will need to obtain government "birth certificates," just like fintech companies.

The biggest question mark will be which services will be permitted. For example, once Binance obtains licenses in various countries, users will be able to speculate legally on the exchange. Blockchain-driven fintech will leverage this technology to improve cross-border payments (as Yellowcard and Binance Pay are already doing). Online payment scenarios will also emerge—users can pay merchants with their local currency through cryptocurrencies, with stablecoins being a key enabler. Furthermore, tokenization will emerge in the capital markets—companies may raise funds through tokenized securities.

The premise of all this is "formalization": regulators must be able to manage systemic risks of technology and enterprises as well as consumer risks.

Q: How do African businesses currently participate in over-the-counter (OTC) crypto settlements?

A: This has actually already begun. Companies like Quidax and Yellowcard are doing this—they connect with different banking partners in different markets to complete cross-border settlements, but they don't advertise it publicly. There are also some purely B2B companies that don't face consumers, but provide backend settlement support for fintech or crypto companies. Nigerian companies are particularly adept at this. BitPesa (now AZA) is a prime example.

Q: How will OTC trading evolve? Given the issues of fraud and corporate governance, is full decentralization realistic?

A: I foresee a more formalized OTC settlement. In the future, OTC settlement will increasingly take the form of fintech or bank partnerships, but funds will ultimately return to the banking system because banks want to keep the flow of funds within their own systems. Banks and regulators are both trying to curb decentralization—it weakens their power and creates systemic risks, so they won't allow it to happen. This isn't just a Kenyan or African phenomenon; it's a global phenomenon (in Hong Kong, Singapore, the US); stablecoin settlement will ultimately become a regulated "intra-financial systemic tool."

High-growth regions are also high-capital flow regions: any trade or cross-border remittance corr