summary

The perpetual contract DEX sector experienced explosive growth in 2025, with its market share soaring from 5% at the beginning of the year to 20-26%, and quarterly trading volume exceeding $1.8 trillion. Hyperliquid continued to lead with a $4.78 billion TVL and robust on-chain order book technology, but faced fierce competition from emerging platforms such as Aster and Lighter. Zero-fee models and aggressive airdrop strategies reshaped the competitive landscape, but their sustainability remains questionable. Technological innovation (ZK-Rollup, application chains) and business model innovation (permissionless listings, yield-based collateral) are progressing in parallel, which will, in the long run, build a more open and transparent derivatives trading ecosystem.

I. Industry Background and Development Status

1.1 Structural migration from CEX to DEX

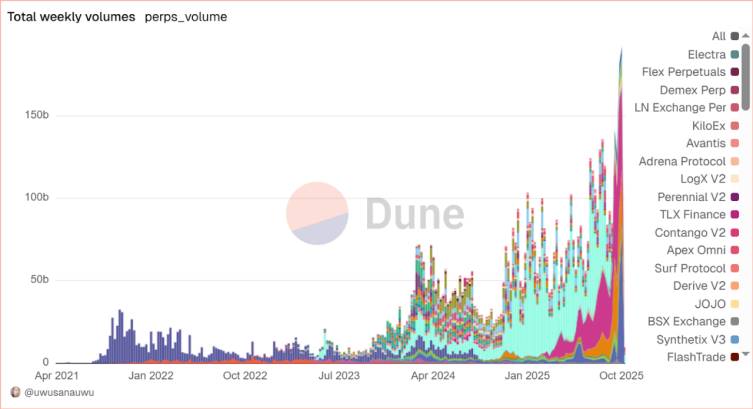

2025 marks a watershed moment for Perp DEX's development. According to the latest data, DEX's share of the perpetual contract market has surged from approximately 5% at the beginning of 2024 to 20-26%, with Q3 trading volume reaching a record $1.8 trillion, a staggering 87% increase from Q2's $964.5 billion. Q3 DEX spot trading volume reached $1.43 trillion, marking the strongest quarterly performance on record and signifying a structural shift in cryptocurrency market pricing. Behind this growth lies a fundamental breakthrough in technological architecture and a rebuilding of user trust.

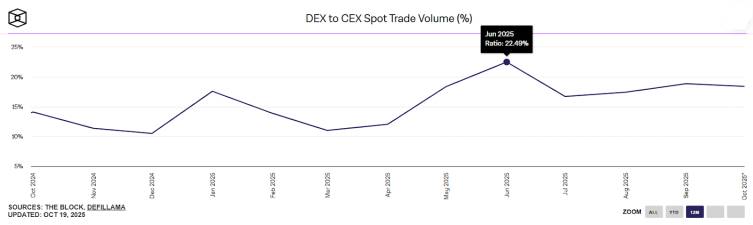

The FTX collapse and the Binance token de-pegging incident on October 11th have completely changed users' perceptions of centralized custody. "Not Your Keys, Not Your Coins" is no longer just a slogan, but a bloody lesson. The DEX-to-CEX futures trading volume ratio hit a record high of 0.23 in Q2 (equivalent to 23% of the CEX volume), a figure that was less than 2% two years ago.

1.2 The Perp DEX market is highly competitive.

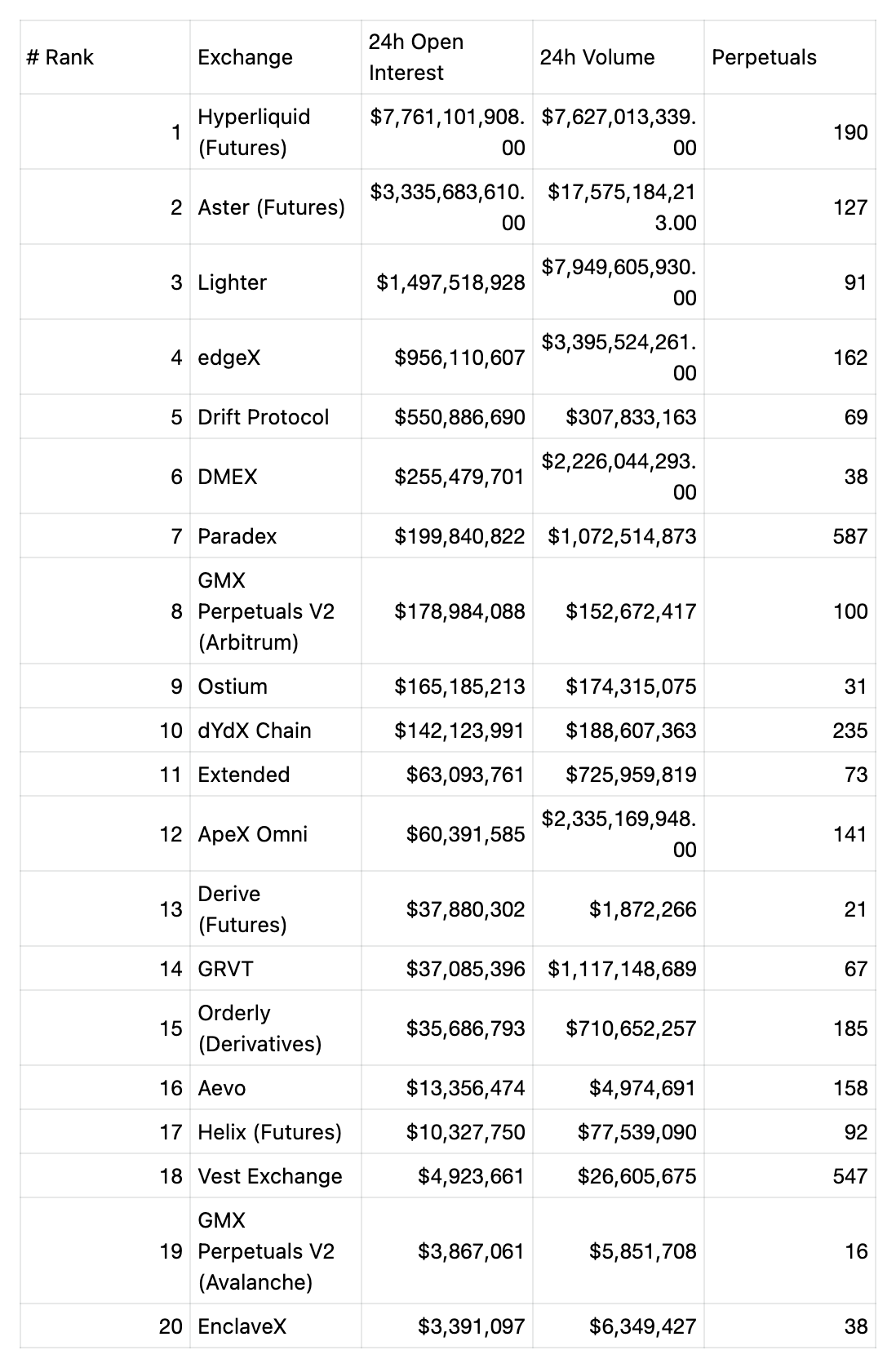

Based on data from October 21, 2025, the current Perp DEX market exhibits a clear head effect.

In 2024, Hyperliquid rapidly rose to become the leader in the decentralized derivatives (DeD) sector, at one point accounting for over 65% of the market share in trading volume, significantly ahead of competitors such as Jupiter and dYdX. However, with increased market attention on DeD and the strong performance of the HYPE token, the field quickly attracted a large influx of new competitors.

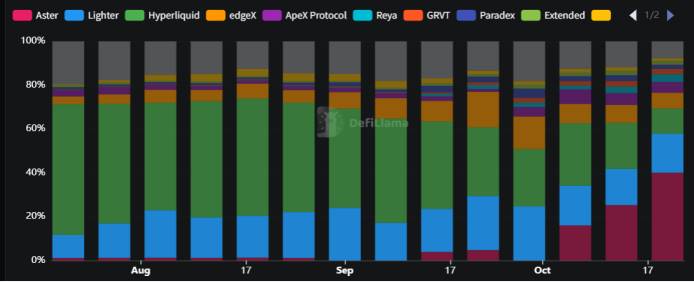

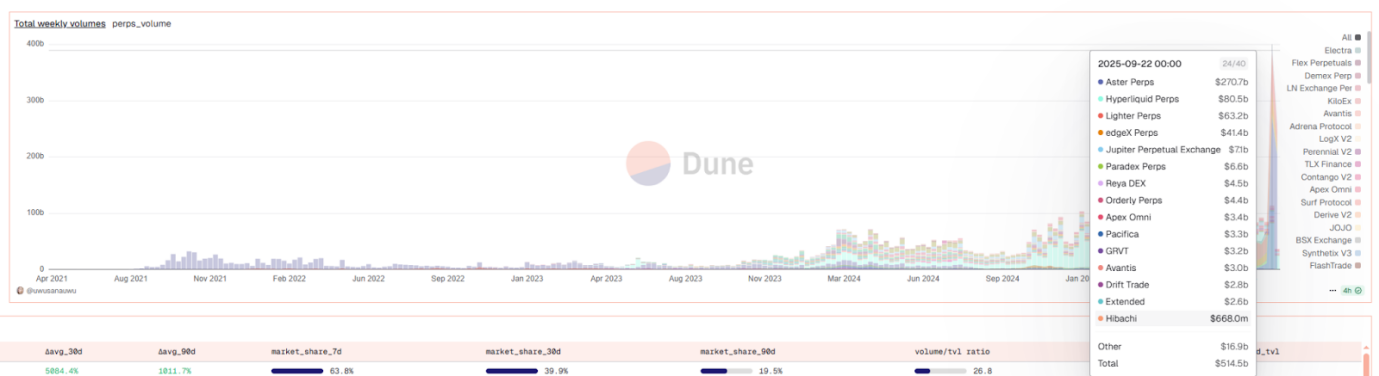

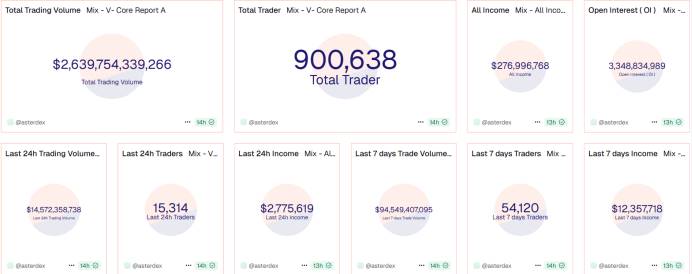

Aster stands out, quickly overtaking Hyperliquid to become the leading platform for decentralized derivatives trading volume, with its current daily trading volume reaching approximately three times that of the latter. Back in July, Hyperliquid still held about 65% of the trading share in this sector, a leading position it has maintained since its mainnet launch at the end of 2024. However, according to data from October 20, 2025, in the past week, Aster accounted for 40% of the perpetual contract trading volume among the top ten protocols, Lighter approximately 17%, while Hyperliquid's share dropped to 7.67%.

Perps Volume Market Share——top 10 protocol

In terms of user scale, Aster also demonstrates a significant advantage, leveraging the robust ecosystem of BNB to reach over 4.6 million users. In contrast, Hyperliquid, after a year of development, has only 750,000 users, showing a significantly slower growth rate. Besides Aster, competitors such as Lighter and edgeX have also shown strong performance recently, making Hyperliquid face increasingly fierce market competition.

However, this shift in market share didn't occur within an existing market. Hyperliquid's trading volume didn't actually change much, and even saw some growth. With Aster joining the competition, trading incentives brought significant incremental growth to the entire market. For example, in the week of September 22nd to 29th, Hyperliquid's trading volume reached $80 billion, still at a high level since its launch. However, this pales in comparison to Aster's staggering $270 billion trading volume during the same period.

II. Analysis of Core Projects in the Perp DEX Track

2.1 Hyperliquid: The Moat and Hidden Dangers of the Performance King

Hyperliquid is a high-performance Layer 1 blockchain focused on derivatives trading, aiming to build a fully on-chain open financial system. Its TVL steadily increased from $4.02B in July to a peak of $6.35B in September, and although it recently corrected to $4.78B, it still maintains its leading position in the industry. Its HIP-3 proposal has ushered in a new era of permissionless asset listings, making perpetual contracts for traditional assets such as stocks and commodities possible.

Technological Advantages: Hyperliquid implements a true on-chain Centralized Limit Order Book (CLOB) through the HyperBFT consensus mechanism. With its on-chain order book technology at its core, it provides users with a trading experience comparable to centralized exchanges (confirmation time less than 1 second) and a processing capacity of up to 200,000 orders per second. The platform derives most of its trading volume from derivatives such as perpetual contracts, and has achieved rapid growth without seeking traditional venture capital through a unique economic model that includes airdropping its token HYPE to the community and using platform revenue for buybacks.

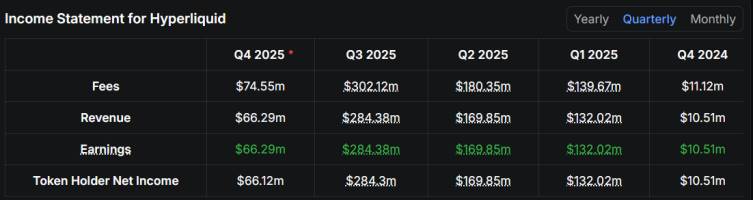

Revenue Model: Hyperliquid employs a highly sustainable token economy model, and its financial data strongly demonstrates the effectiveness of this model—the platform converts almost all of its transaction fees (as shown in the chart, a staggering $302 million in fees in Q3 2025) into "net income for token holders" ($284 million in the same period), which is explicitly used for the buyback and burn of $HYPE tokens. This deflationary mechanism, which directly links the platform's success to the token's value, not only enables explosive wealth growth during bull markets (such as a more than 27-fold increase in income within a year), but also provides solid support for the token price through continuous buybacks during bear markets, making it extremely attractive.

Potential Risks: The protocol faces significant selling pressure from the large-scale unlocking of SHYPE tokens. According to its token unlocking schedule, approximately 19.83 million SHYPE tokens (5.3% of the circulating supply) will be unlocked in Q4 2025, marking just the beginning of prolonged selling pressure. A more severe challenge begins at the end of November 2025, when a total of 238 million core contributor tokens will begin linear unlocking, projecting daily selling pressure of approximately $17 million between 2027 and 2028. This scale far exceeds the current daily buyback capacity of approximately $2 million from the "assistance fund," representing about 8.6 times the buyback capacity, constituting substantial structural resistance. Furthermore, the protocol's relatively centralized governance structure (secured by only 24 validator nodes) contrasts with more decentralized networks like Ethereum, potentially creating a single point of failure risk.

2.2 Aster: A Double-Edged Sword of Aggressive Growth

Aster is arguably the most controversial project of 2025. Its TVL saw a staggering sixfold increase in late September (from 367M to 2.27B), with daily trading volume exceeding $27 billion at one point, but this "rocket-like" growth has also raised questions.

Technological Innovation: Aster demonstrates a deep understanding of user needs. Its product design goes beyond simple feature aggregation; it builds a dual-mode platform serving both professional traders and retail investors. Currently deployed primarily on the BNB Chain, it employs a hybrid "order book + vAMM" model. The order book is used for accurate pricing of mainstream cryptocurrencies, while the vAMM supports high-leverage (e.g., 1001x) long-tail asset trading. It innovatively introduces interest-bearing assets as margin, allowing users to trade using liquidity-staking tokens like asBNB or the native yield stablecoin USDF, significantly improving capital efficiency and enabling "trading to earn interest." For institutional users, Aster focuses on introducing a "hidden order book" feature. This privacy-first design effectively prevents MEV attacks and protects large order strategies. Early integration with the Binance ecosystem not only secured a large initial user base and liquidity but also enhanced market trust through public endorsement, laying a solid foundation for future development.

The crux of the controversy: On October 5th, DefiLlama removed Aster from the market due to data anomalies, primarily caused by an abnormal ratio of trading volume to open interest (reaching 27 times), far exceeding normal levels. Although the official explanation was that it was due to market maker activities and points incentives, accusations of "volume manipulation" persist.

2.3 Lighter: A Pioneer in the Zero-Cost Revolution

Lighter represents a completely different business model – attracting users with zero transaction fees and profiting through paid APIs and spreads, similar to the "order flow payment" model in traditional finance. Its TVL has achieved a robust 6-fold growth (from 186M to 1.10B), demonstrating a linear and continuous development trajectory.

Technological Innovation: Its high-performance trading engine, built on ZK-Rollup, achieves ultra-fast transaction latency of less than 5 milliseconds through a verifiable off-chain matching mechanism, while ensuring the ultimate transparency and security of on-chain settlement. This technology lays a solid foundation for its "zero-fee" model and, by providing an LLP liquidity vault with up to 63% APY, has successfully attracted capital, building a vibrant trading ecosystem.

Challenge: Lighter's low user retention rate indicates that its user engagement needs to be strengthened. Similar to Aster, Lighter's trading volume to OI ratio is much higher than competitors like Hyperliquid. The high turnover rate may indicate a large number of short-term, speculative behaviors on the platform, rather than long-term retained actual trading users. Therefore, Lighter's long-term profitability is currently questionable, and it needs to convert the huge traffic attracted by zero fees and airdrop expectations into real users with long-term engagement.

2.3 EdgeX: A Differentiated Competitor with Stable Operations

Incubated by the well-known market maker Amber Group, EdgeX is a relatively small but distinctive player in the current Perp DEX market, holding approximately 5.5% market share. EdgeX has not adopted extreme strategies in performance or incentives, but rather leverages its risk control capabilities stemming from its market-making background and its deep cultivation in specific regions to secure a stable niche. It represents another path in the Perp DEX market that emphasizes steady and sustainable growth.

Market Strategy: EdgeX's users are primarily concentrated in the Asian market (China, Japan, South Korea, and Taiwan). It employs a conservative operational strategy, incentivizing users through a multi-dimensional points program, but its fee structure is not competitive. Its OI/Volume ratio is approximately 0.27, significantly lower than Hyperliquid but considerably higher than Aster and Lighter, indicating relatively less "volume manipulation" in its trading volume and more genuine and sustainable user behavior. While its Liquidity Vault (eLP) size ($147 million) is the smallest among the four, it achieved profitability during the "1011" market crash, similar to HLP, demonstrating robust risk resilience.

2.5 Emerging Forces and Competitors in Niche Markets

● dYdX : As a pioneer of the order book model, it has migrated to an independent application chain, aiming to create a fully decentralized, high-performance derivatives exchange.

● GMX : It pioneered the multi-asset shared liquidity pool (GLP) model, featuring no slippage trading and "real yield," which is highly favored by retail investors.

● Paradex (incubated by Paradigm): Focuses on unified margin accounts and institutional-grade services.

● Orderly Network : As infrastructure, it provides derivatives trading capabilities for other applications.

● Drift Protocol : Plays an important role in the Solana ecosystem, providing a one-stop cross-margin trading experience.

The current Perp DEX market is fiercely competitive, exhibiting diverse development models such as high-performance on-chain order books, high-leverage incentives, zero fees, and institutional-grade services. From a long-term development and market resilience perspective, Hyperliquid demonstrates the strongest overall competitiveness thanks to its robust technical architecture (self-developed L1 on-chain order book), superior performance, and highly transparent and sustainable token economic model (revenue directly used for buybacks and burns). Its deflationary mechanism, which successfully links the platform to token value, captures value in bull markets and supports token prices through continuous buybacks in bear markets, building a strong competitive advantage. In contrast, Aster's aggressive growth has been accompanied by controversies surrounding wash trading, Lighter's zero-fee model faces challenges in user retention and profitability, and EdgeX is limited by its relatively niche market positioning. The Perp DEX model will continue to evolve, but its core competitiveness will increasingly focus on a combination of technological innovation, a sustainable economic model, and genuine user engagement, rather than simply short-term incentives.

III. Technological Breakthroughs: Solutions to Architectural Evolution and Performance Bottlenecks

3.1. Evolution of Scalable Technology Paths

The current mainstream technical architectures can be divided into three paths, each with its own advantages and disadvantages, and suitable for different strategic goals:

1. App-Chain Paradigm : Represented by Hyperliquid, this paradigm provides exchange applications with maximum performance customization and sovereignty by building dedicated L1 blockchains (such as HyperBFT consensus). Advantages include extreme performance (high TPS, low latency) and a gas-free experience; disadvantages include extremely high development difficulty and the need to maintain a validator network and security measures independently. Although customized Layer 1 blockchains have multiple validator nodes, theoretically decentralizing the system, the actual degree of decentralization is limited due to the small number of nodes and their complete team control.

2. General L2 Rollup Paradigm : Represented by Lighter, this is a ZK-Rollup built on Ethereum. Its advantages include natural integration into Ethereum's vast ecosystem and security, benefiting from its network effects, and strong asset composability (e.g., LLP tokens can easily connect to mainnet DeFi protocols). With Ethereum upgrades such as Danksharding, its cost advantage will become increasingly apparent. While, as a Rollup, only a single Sequencer handles matching, resulting in centralized execution, verifying ZK proofs consumes very few resources and can be done by lightweight nodes, making the verification process highly decentralized and compensating for the shortcomings of centralized execution. Furthermore, the asset ledger resides on the Ethereum mainnet, meaning that even if the Lighter team disappears, users can still retrieve their funds independently, ensuring full asset security.

3. Hybrid Architecture : Aster employs a hybrid architecture combining order book and ZK-Rollup, ensuring accurate pricing through CLOB and supporting perpetual contract trading with leverage up to 1001x on the ZK L1 chain, effectively improving capital efficiency. Its overall architectural strategy presents a clear phased plan. Currently, Aster cleverly leverages the BNB Chain, utilizing its mature ecosystem resources to quickly launch the market and aggregate liquidity. This "Trojan horse" strategy avoids the cold start challenges of building a self-sufficient ecosystem. Through a series of ecosystem collaborations, the project has deeply integrated on-chain credit and popular tracks like Memes, building a strong community and distribution network. Looking ahead, Aster plans to migrate to its self-developed ZK L1 chain—Aster Chain. This crucial leap aims to completely resolve performance and privacy bottlenecks. At that time, with the economic incentives of large-scale airdrops, Aster expects to smoothly guide the users and liquidity accumulated on the BNB Chain to its sovereign chain, ultimately forming a one-stop trading ecosystem with high performance, strong privacy, and cross-chain interoperability.

3.2 A Revolution in Order Matching Mechanisms: From AMM to On-Chain CLOB

The core of the development of perpetual DEXs is the continuous evolution of the order matching mechanism, which aims to balance decentralization and performance efficiency.

1. Oracle Pricing Model: Represented by GMX. This model relies entirely on external oracles to provide prices, and transactions are executed directly at those prices. Its advantage is zero slippage, but the cost is giving up on-chain price discovery; traders are essentially "price takers."

2. vAMM Model: Represented by the early Perpetual Protocol. This model introduces virtual automated market makers, simulating liquidity pools through mathematical formulas for trading and pricing. It achieves on-chain price discovery, but often suffers from high slippage due to liquidity virtualization, resulting in a poor user experience.

3. Off-chain order book + on-chain settlement: Represented by dYdX v3. This is a key breakthrough in hybrid models. Order matching and processing are completed on high-performance off-chain servers, with only the final transaction settlement results uploaded to the blockchain. This approach significantly improved transaction speed and user experience in the early stages, representing an important step towards a CEX-like experience.

4. Full-on-chain order book: This is the next frontier in evolution, represented by Hyperliquid. With the emergence of high-performance blockchains such as Solana and Monad, as well as dedicated application chains, it has become possible to place the entire order book on-chain. This model restores the full transparency and composability of on-chain transactions and strives to solve problems such as latency and front-end attacks through the optimization of the underlying infrastructure, representing the ultimate form of decentralized transactions.

This evolutionary path clearly demonstrates the industry's shift from imitation to innovation, ultimately aiming to provide a trading experience comparable to centralized platforms while maintaining the core advantages of decentralization.

3.3. Capital Pool Model: A Core Innovation for Improving Capital and Risk Efficiency

The DEX liquidity pool model significantly improves capital efficiency and reduces trading slippage through innovative liquidity aggregation and risk management mechanisms.

1. Hyperliquid HLP Model: HLP acts as a protocol treasury, participating in market making and clearing processes and earning a share of transaction fees. This model employs an active liquidity strategy, enabling it to dynamically respond to market changes, but it carries the complexity of hedging failure and liquidation risks.

2. Aster ALP and USDF Combination: Aster employs a hybrid liquidity setup, using ALP (Automated Liquidity Pool) in on-chain "Simple Mode" trading. USDF, as a yield-generating stablecoin, is fully backed by a delta-neutral portfolio of crypto assets and short positions. Users can earn up to 20x margin boost by depositing assets such as BNB and USDT into asBNB or USDF.

3. Lighter LLP Shared Risk Model: LLPs collectively bear losses as a single liquidity pool, employing a shared risk structure. This model offers a zero-fee option and achieves verifiable order matching and clearing through ZK circuits. LLP revenue comes from counterparty profits and losses, funding fees, and clearing fees.

4. Jupiter Liquidity Aggregation Model: As a leading DEX aggregator for Solana, Jupiter aggregates liquidity from 50+ DEXs using the Metis v1 engine, handling over 50% of Solana's trading volume. Its liquidity aggregation model provides deep liquidity access and minimizes slippage. The newly launched Jupiter Lend protocol employs a custom liquidation engine and dynamic risk isolation limits.

For sophisticated traders or institutions seeking maximum capital efficiency and leverage, Aster's ALP/USDF model may be more attractive, as it maximizes asset utility through a delta-neutral strategy and margin up to 20x, but also carries higher complexity risk. For risk-averse liquidity providers, Lighter's LLP shared-risk model might be a better choice, offering a clearer profit structure with its zero-fee and risk-sharing mechanism, although losses are collectively borne. Hyperliquid's HLP model resembles a professional, actively managed hedge fund, better suited for users who trust the protocol's active management capabilities and can tolerate potential hedging failures. For most ordinary users, Jupiter's liquidity aggregation model is likely the optimal choice for most everyday trading scenarios, as it provides the best price and lowest slippage by aggregating liquidity across the network without requiring active user management, offering superior ease of use and trading experience.

IV. New Dimensions of Ecosystem Competition: From Traffic Acquisition to Value Creation

With the technical architecture gradually maturing, the competitive focus of Perp DEX has shifted from simple technical performance to a deeper competition in building a broader ecosystem.

4.1 The Double-Edged Sword of Growth Strategies: Aggressive Incentives and Controversies Regarding "Data Inflating"

The most prominent phenomenon in the current ecosystem competition is that emerging platforms have achieved explosive growth through high incentive strategies, but this has also sparked controversy about the authenticity of data.

● Aster's Aggressive Growth : Aster boosted its daily trading volume to over $27 billion and its total user base to over 4.6 million by offering leverage up to 1001x and incentive programs. However, this rocket-like growth was accompanied by skepticism. Its trading volume to open interest (OI) ratio was abnormally high, far exceeding normal levels, raising concerns that a significant portion of its trading volume was being manipulated to obtain airdrop credits through "volume boosting."

● Lighter's Zero-Fee Model Challenges : Lighter's zero-fee model has successfully attracted a large amount of traffic, but its user retention rate is low. Similar to Aster, its trading volume to OI ratio is also much higher than that of industry stalwarts (such as Hyperliquid), indicating that the platform may have short-term speculative behavior with high turnover rates rather than long-term retained real trading users, thus casting doubt on its long-term profitability.

● Benchmarks for Authenticity and Sustainability : In contrast, Hyperliquid's trading volume growth is relatively stable, and its OI/Volume ratio is healthier. While platforms like EdgeX have smaller market shares, their OI/Volume ratios are significantly higher than Aster and Lighter, indicating that their user behavior is more authentic and sustainable.

4.2 The Deep Race of Ecosystem Building: Assets, Liquidity, Business Innovation, and Fee Models

Beyond traffic, project teams are also competing on a deeper, ecosystem-level scale.

● The Race for Asset Diversity : Hyperliquid's HIP-3 proposal pioneered the "permissionless asset listing" model, allowing for the rapid launch of perpetual contracts for traditional assets such as stocks and commodities. This is becoming a new strategy to attract long-tail assets and the community. Aster, however, demonstrates a differentiated understanding of this trend. Its strategy does not simply pursue the quantity of assets, but focuses more on building asset depth and integrating trading scenarios. For example, Aster's 24/7 stock perpetual contracts, featuring highly watched assets such as Tesla and Nvidia, aim to provide crypto-native users with seamless exposure to traditional market risks.

● Liquidity and Yield Model Innovation : Leading protocols are vying for capital through differentiated designs in liquidity and yield model innovation. For example, Hyperliquid's HLP market-making pool allows users to deposit USDC to share in counterparty profits and losses, yielding an annualized return of approximately 6.7%. The protocol also allocates about 93% of its transaction fees to an aid fund for token buybacks, creating a value-return flywheel. Aster, through its ALP liquidity pool, allows users to use interest-bearing assets (such as asBNB or USDF) as collateral, earning staking rewards (asBNB annualized returns of approximately 5-7%) or stablecoin deposit rewards (USDF combined with a high APY of up to 16.7%) while trading, thus improving capital efficiency. Against this backdrop, innovations from other protocols are also noteworthy. For instance, Lighter's LLP liquidity vault attracts capital by offering high APYs, with its returns derived from counterparty profits and losses, funding fees, and liquidation revenue. Whether this model can be sustained under zero transaction fees is attracting considerable attention.

● Business Model Transformation: Hyperliquid and its developer incentive program encourage third parties to build new applications on its infrastructure, while Aster's deep integration with the BNB Chain ecosystem demonstrates a path to rapid launch by leveraging existing traffic. These innovations not only improve capital efficiency but also create network effects, driving the entire ecosystem towards a more sustainable future.

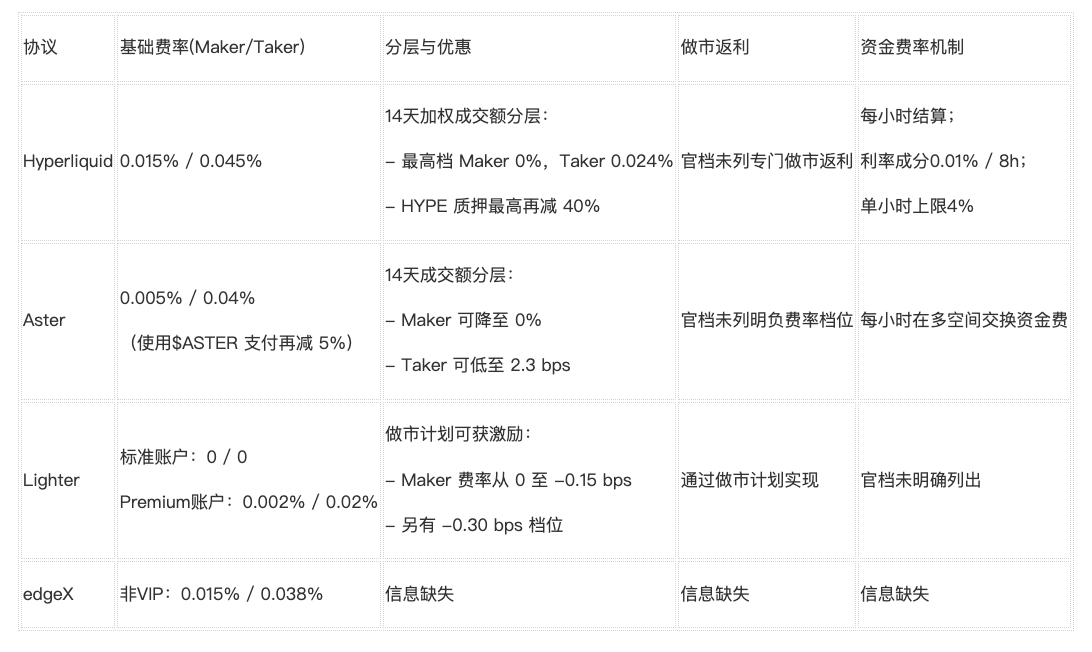

● Fee Comparison: A comprehensive comparison of the fee structures of various perpetual contract DEXs allows for differentiated selection based on user profiles: Lighter's standard account with its zero-fee model is most attractive to retail and low-frequency traders; its Premium account, with its extremely low taker fees, is more suitable for high-frequency traders. For passive market making and large orders, Aster and Hyperliquid are preferred due to their more advantageous tiered mechanisms and market-making rebates. If sensitive to funding rate fluctuations, Aster and Lighter's mechanisms are more suitable. In contrast, EdgeX does not show significant competitiveness in its current fee structure.

V. Compliance Challenges: The Sword of Damocles Hanging Over Our Heads

Perp DEX's rapid growth is facing immense pressure from the accelerating formation of a global regulatory framework, and compliance has become crucial in determining a project's long-term survival.

5.1 Clarification of the Global Regulatory Environment

● United States : In September, the U.S. CFTC and SEC jointly announced a commitment to provide "innovation exemptions" for DeFi venues, explicitly including crypto derivatives such as perpetual contracts in the safe harbor pilot program, and announced a 24-hour roundtable discussion on coordinating market, portfolio margining, and DeFi regulation. This policy signal indicates that regulators are beginning to shift from a purely enforcement stance to constructive framework development.

● EU : While the MiCA regulation only applies to spot crypto assets, any perpetual, swap, or other derivatives offered to EU clients automatically become MiFID II financial instruments. ESMA's final guidance, issued in December 2024, explicitly warns that simply operating an English-language frontend accessible from the EU could undermine the reverse solicitation exemption, and derivatives DEXs must either be geo-blocked or obtain an investment services license.

● Asia Pacific : The regulatory framework in the Asia Pacific region is also rapidly improving. The Monetary Authority of Singapore (MAS) requires any platform offering leveraged crypto products (including DEXs) to hold a license under the Payment Services Act, and if derivatives are involved, it must also obtain "organized market" approval under the Securities and Futures Act. The Hong Kong Securities and Futures Commission's roadmap indicates that digital asset derivatives trading will only be open to "professional investors" and will be subject to strict risk management and off-exchange reporting rules.

5.2 Specific Risks Faced by the Project Owner and Countermeasures

● User Geographical Risk : Platforms like Hyperliquid have a large number of US users, but there is significant uncertainty as to whether their practice of blocking US IP addresses on the front end can withstand the strict scrutiny of the SEC. Furthermore, their business model heavily relies on user loyalty and sustained revenue growth. If future regulations tighten, requiring platforms to implement KYC/AML measures, or if a deteriorating macroeconomic environment leads to lower-than-expected trading revenue, both could impact the sustainable operation of their ecosystem.

● Red line for asset innovation : Products such as perpetual stock contracts explored by various platforms have directly entered the deep waters of traditional securities regulation, which is very likely to trigger a joint crackdown by global regulatory agencies.

● Solution Exploration : The industry is actively developing compliance technologies (RegTech), such as on-chain KYC modules, zero-knowledge proofs, and regulatory sandboxes, in an attempt to find a balance between the ideals of decentralization and regulatory requirements.

VI. Future Outlook: From Traffic Battles to Value Reconstruction - A Final Reflection

In the current battle for traffic within the Perp DEX industry, the market is gradually shifting from disorderly expansion to structural consolidation. This evolution not only reflects the deepening of the competitive landscape but also foreshadows the reshaping of value creation mechanisms. The following discussion explores the potential endgame scenario of the industry from aspects such as long-term competitive consolidation, transformation of growth models, institutionalization paths, regulatory impact, convergence of technical architectures, and value capture mechanisms.

6.1 A Long-Term Competitive Consolidation Landscape Beyond Market Share Competition

The initial stage of the Perp DEX market was dominated by fierce competition driven by traffic, but in the long run, this model will become unsustainable and shift towards oligopoly and ecosystem synergy. Data from 2025 shows that the industry's trading volume has exceeded $1 trillion, with an annual growth rate of over 138%, but the market share of the dominant platforms is rapidly concentrating on a few leading players. It is projected that by 2027, DEX perpetual contract trading volume will account for more than 50% of the overall derivatives market.

This consolidation is not a simple merger or acquisition, but rather achieved through network effects and liquidity aggregation: leading platforms will form a "winner-takes-all" landscape through cross-chain bridging and protocol interoperability. A few platforms will dominate more than 80% of the liquidity, while peripheral participants will be marginalized or integrated into the ecosystem alliance. This process is similar to the oligopolization of traditional financial markets, driving the industry to transform from fragmented competition to large-scale collaboration, avoiding resource waste and improving overall efficiency.

6.2. Evolution from Incentive-Driven Growth to a Sustainable Organic Model

Currently, Perp DEX's expansion heavily relies on airdrops, tokens, and short-term incentives. While these mechanisms can quickly attract traffic, they are prone to bubbles and user churn. In the future, the industry will gradually shift towards an organic growth model based on real yield, with protocol fee buybacks and burning becoming core pillars. For example, some platforms have already allocated 99% of their revenue to token buybacks, achieving a shift from speculative incentives to value-anchored rewards.

This evolution will rely on the stable generation of transaction fees and long-term incentives for liquidity providers. It is projected that by 2028, the organic user retention rate will increase from the current 40% to over 70%. By reducing emissions dependence and strengthening the sustainable mechanism of fee sharing, Perp DEX will shift from a "traffic game" to a "value cycle," thereby resisting market cycle fluctuations and achieving endogenous expansion.

6.3 Institutional Adoption Trajectory and Market Maturity Indicators

Perp DEX is currently primarily driven by retail and quantitative traders, but institutional adoption will be a key catalyst for market maturity. Data from 2025 shows that institutional funds flowing into DEXs have increased from 10% to 25%, thanks to improved risk management and compliance tools on the platforms.

The future trajectory will be a gradual progression: initially attracting hedge funds and asset management institutions through permissioned access (such as KYC/AML options), and in the medium term achieving large-scale integration through standardized APIs and custody solutions. Maturity indicators include open interest (OI) consistently exceeding $100 billion, institutional trading accounting for over 40%, and an optimized TVL to trading volume ratio (currently around 0.3, approaching 0.5). This transformation will mark Perp DEX's leap from a "retail paradise" to "institutional infrastructure," driving market depth and stability.

6.4 The Reshaping of Business Models by Regulatory Frameworks

The evolving regulatory environment will reshape the Perp DEX business model. Currently, regulatory uncertainty has led to the postponement of launches for some platforms (such as OKX's DEX project), but in the long run, a clearer framework will foster a hybrid model: platforms will need to incorporate TradFi elements, such as permissioned compliance and risk disclosure, in exchange for institutional access.

It is projected that by 2027, major global jurisdictions (such as the EU's MiCA and the US CFTC rules) will require DEXs to implement optional KYC and anti-money laundering mechanisms. This will reshape revenue structures—shifting from pure fee-based models to compliant service fees. Simultaneously, regulation will curb high-risk leveraged products, pushing platforms towards lower-risk, transparent derivatives. Overall, this reshaping will eliminate non-compliant participants but provide a legitimacy basis for sustainable models, promoting the industry's integration from the "grey area" into mainstream finance.

6.5 The trend of convergence in technical architecture

Perp DEX's technical architecture will evolve from diversified experimentation to standardized convergence to address the issues of liquidity fragmentation and execution delays. Currently, the CLOB (Centralized Limit Order Book) model has become mainstream, and in the future, it will further integrate the Intent Layer and ZK proofs to achieve unified cross-chain liquidity and privacy protection.

It is projected that by 2026, 80% of platforms will adopt a multi-chain aggregation architecture, combined with a HyperEVM-like EVM-compatible layer, to improve composability and settlement speed (from seconds to milliseconds). This convergence will reduce bridging risks, drive the transformation from "on-chain silos" to a "unified execution layer," and support the processing of trillions of dollars in transaction volume.

6.6 The Ultimate Value Capture Mechanism That Determines Long-Term Winners

The long-term winners of Perp DEX will be determined by an efficient value capture mechanism, rather than simply trading volume. The core lies in the closed-loop design of fee sharing: leading platforms achieve token value anchoring and user loyalty through 99% revenue buyback and burning, the ve (voting custody) governance model, and PnL sharing in the Liquidity Vault (HLP). In the future, value capture will emphasize an ecosystem closed loop—integrating lending, staking, and derivatives to achieve compound returns, driving the industry from "traffic capture" to the ultimate goal of "value reconstruction."

in conclusion

The Perp DEX sector has successfully moved beyond the technology validation phase and entered a new stage of competition based on ecosystem and business model. While companies like Aster and Lighter have demonstrated the power of short-term growth through aggressive strategies, their data integrity and model sustainability face challenges. Hyperliquid, on the other hand, showcases the advantages of combining technological performance with a sustainable economic model. The future winners will undoubtedly be those ecosystems that can establish comprehensive advantages in technology, user experience, economic models, asset innovation, and compliance. Despite the challenges ahead, the trend of Perp DEX driving finance towards greater openness and transparency is irreversible, and its long-term value is solid and full of potential.