Author: Simon

Compiled by: TechFlow TechFlow

Original title: Will Pump.fun be able to tell a new story next year?

The following content is excerpted from Delphi's upcoming "2026 Application Outlook Report," focusing on Pump(.)fun—one of the consumer applications we are most interested in next year.

Many things have changed since we published our initial Pump report (before its funding round). Many of our predictions have come true, but there have also been areas where we've fallen short, disappointing users and investors. However, the core challenges facing Pump remain the same.

To realize Pump's grand vision, the team needs to find a balance between the short-term profit-driven nature of the crypto industry and its long-term vision for the platform. It's worth noting that once a project launches its token, its operating environment changes; the token itself becomes a separate product, inherently reflexive, and continuously influences user expectations—Pump is no exception.

Since securing funding, the Pump team has been increasing its investment in encrypted native streaming, but development in this area has not been as smooth as we expected, and it has not yet reached the ideal state.

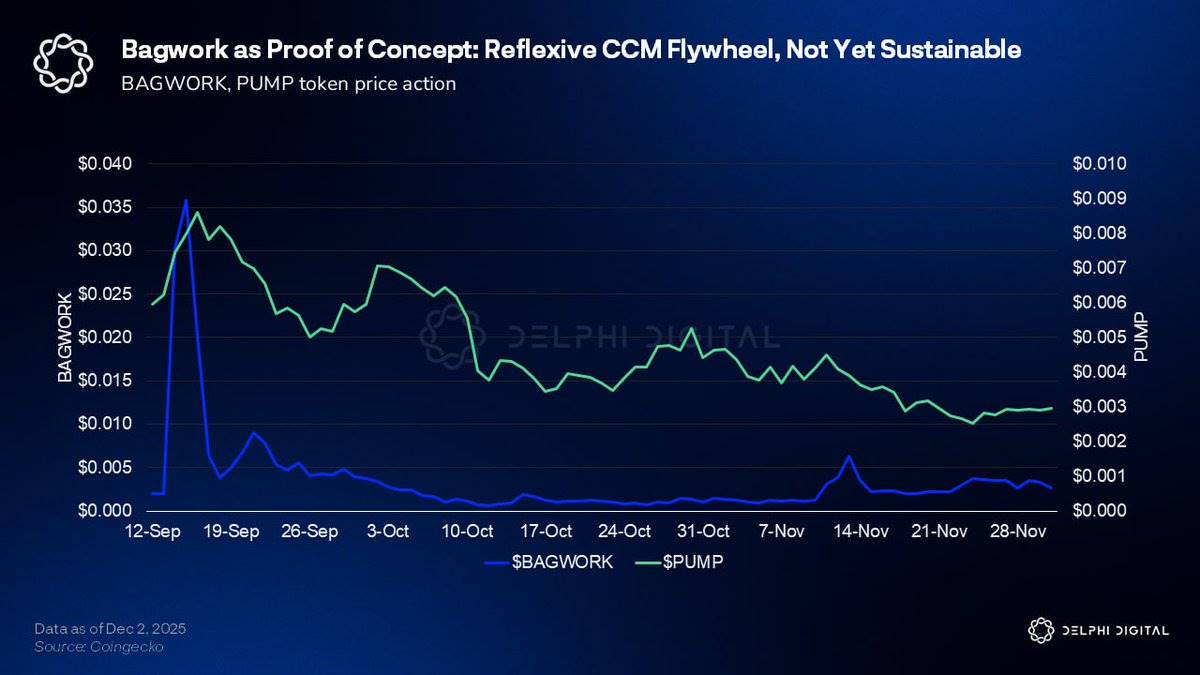

Pump has yet to successfully attract core creators outside the crypto ecosystem, and the CCM metaverse that emerged on the Pump platform has been short-lived. The most notable moment came with the "Bagwork" event, which not only showcased the potential of creator-driven tokens but also revealed the structural problems hindering the development of this model.

This phenomenal outburst was spearheaded by a group of teenagers who, with part of Pump's support, carried out a series of controversial incidents: stealing Bradley Martyn's hat, storming the Dodgers' court, rushing onto the Knicks' court, and even getting Pumpfun and Bagwork tattoos.

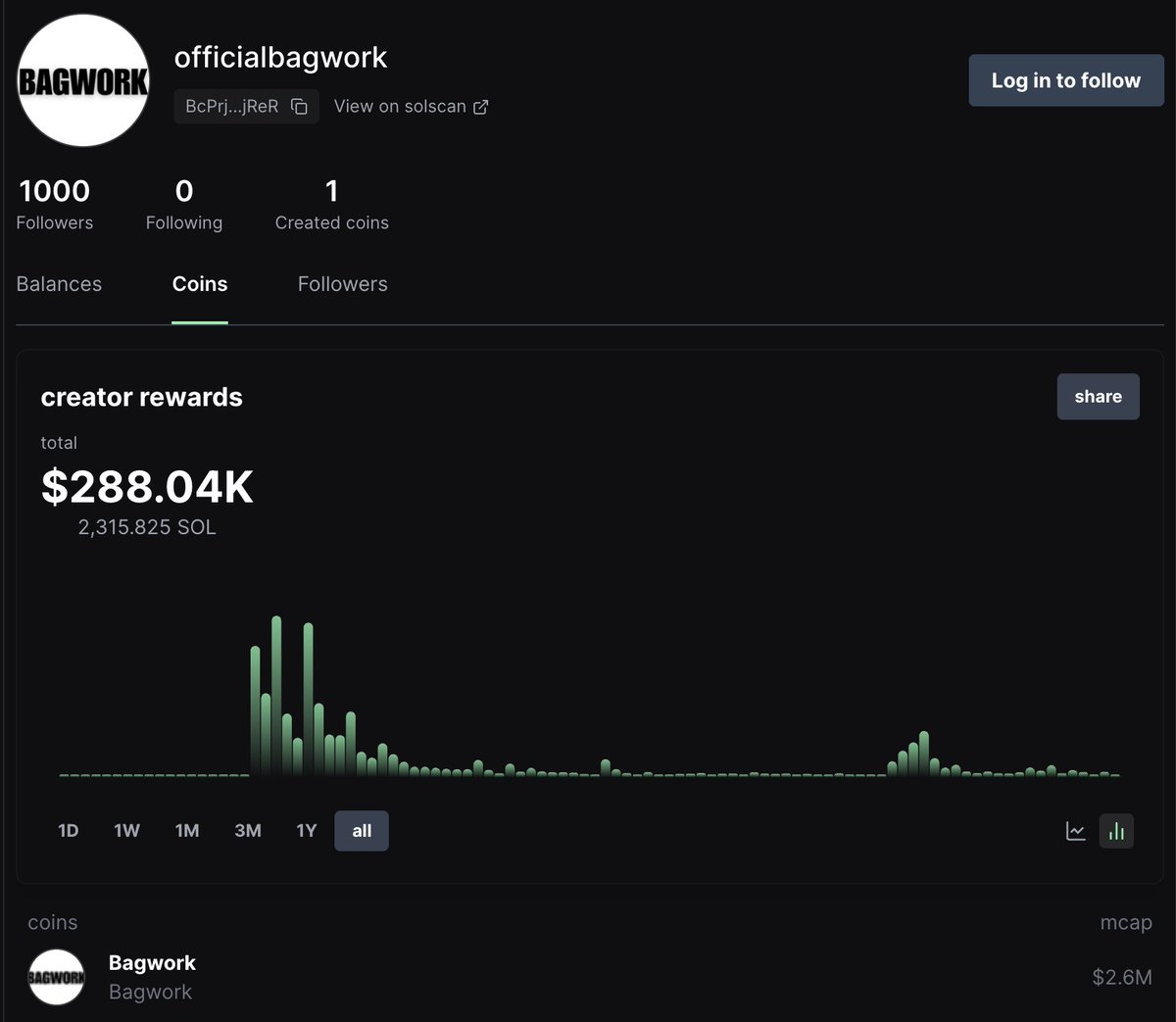

@onlybagwork 's rise almost perfectly coincided with Pump.fun's peak of popularity in mid-September. At that time, $PUMP's fully diluted valuation (FDV) reached approximately $8.5 billion, while Bagwork's market capitalization briefly surpassed $50 million.

However, since then, no creator token has come close to this organic potential or reached a similar valuation peak.

The Knicks arena incident occurred much more recently, long past its initial hype, and Bagwork's current market value is just over $2 million.

Bagwork is one of the few examples of Pump's streaming experiment that truly works as expected. The Bagwork team has earned over 2,300 SOL in creator revenue (approximately $300,000 at current prices) through transaction fees.

It's worth noting that none of this required the team to sell their holdings. The viral event directly translated into increased attention, trading volume, and fee revenue, creating Pump's closest example to a true creator token flywheel effect to date.

However, aside from Bagwork, Pump continues to struggle to realize its streaming vision. Creator tokens have consistently failed to maintain their value. This phenomenon can be traced back to a fundamental problem: the tokens themselves are part of the product.

Currently, the economic rationale for owning or backing a particular streamer token remains unclear. Bagwork's early success quickly faded, and since then, every major streamer token has failed to gain similar attention, eventually tending towards zero.

Creators can gain short-term benefits through CCM's fee structure, but the reputational risk associated with crash tokens makes this model unattractive to bigger, more established creators who could have helped the platform attract a wider audience. From a trader's perspective, these tokens remain a zero-sum game environment, not a genuine community.

This is the most important problem Pump needs to solve as it heads into 2026.

Currently, the team has not made any meaningful attempts at deeper creator incentive mechanisms, and airdrop distribution remains untouched. Aside from the informal support provided during the Bagwork craze, Pump has not taken any coordinated measures, such as targeted airdrops, creator rewards, or other incentive mechanisms, that could have been used to launch early activities, create more PvE (player versus environment) incentives, and provide creators with room to experiment without immediately disrupting its community ecosystem.

The good news is that this provides the pump with tremendous flexibility.

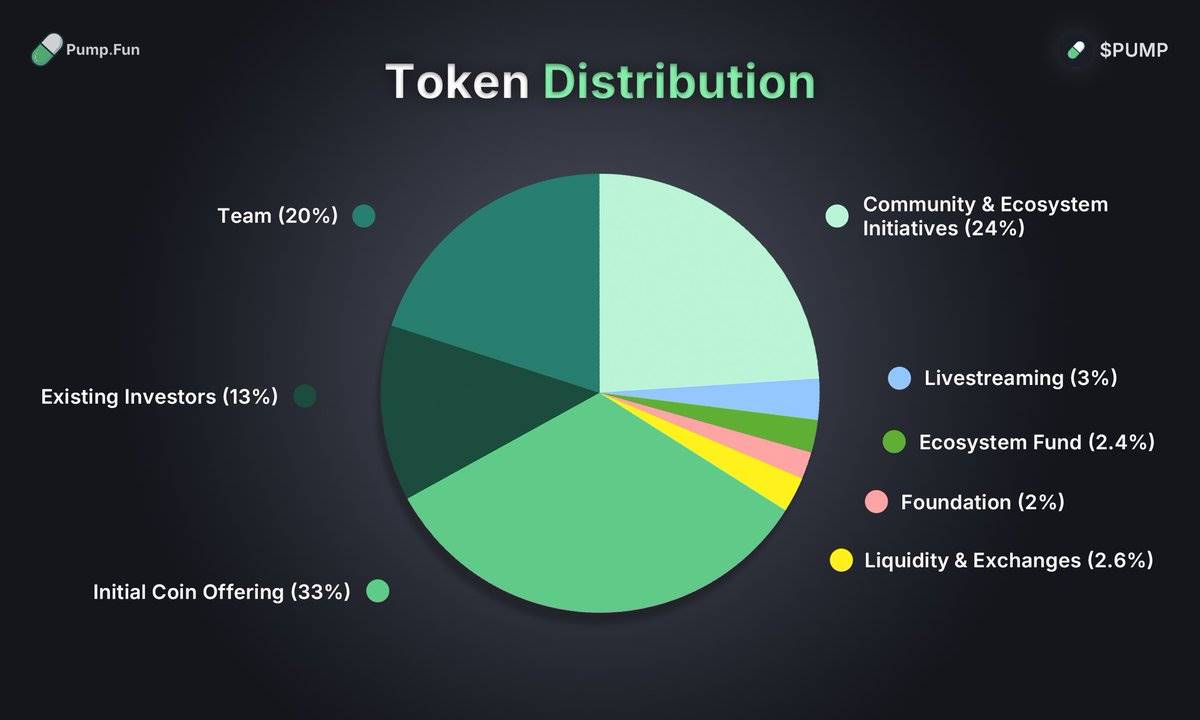

The untapped Community & Ecosystem Initiatives fund remains a crucial lever for the team to utilize as the model matures. If Pump can design a sustainable creator token incentive structure, it will open up a whole new economic category for creators looking to monetize and expand their audience using crypto mechanisms.

Despite the potentially substantial gains, streaming will continue to behave as a series of short-lived booms rather than a sustainable and repeatable vertical until then.

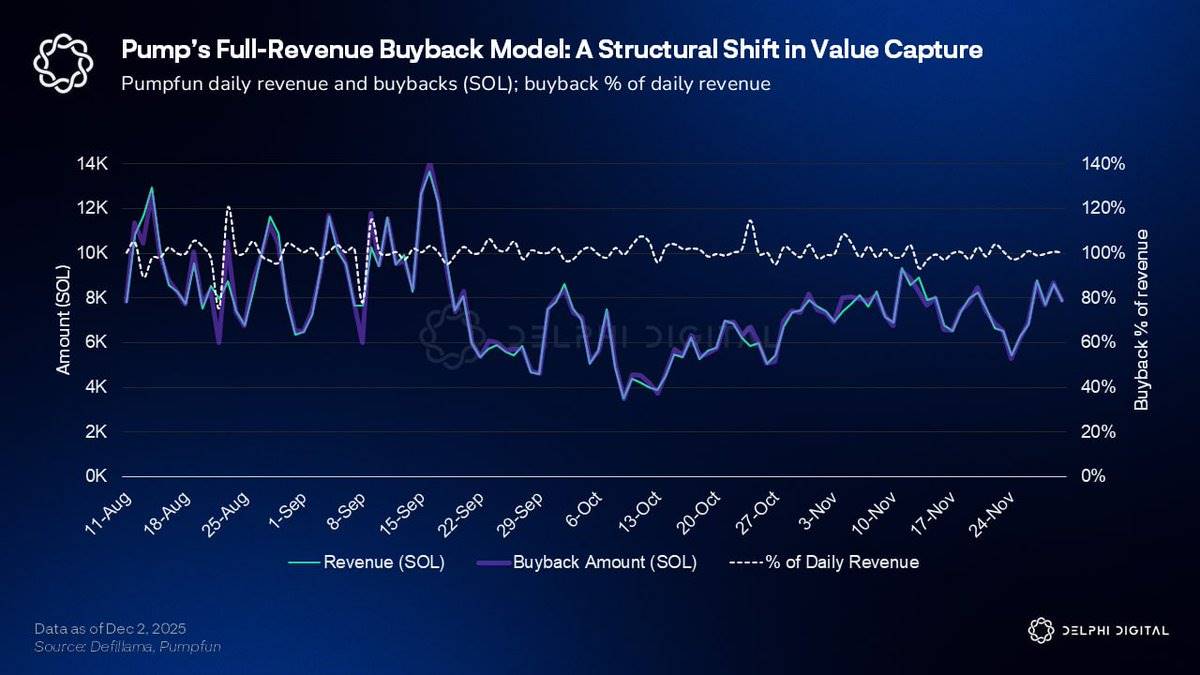

Regarding the token, the main catalyst that drove $PUMP up from approximately 0.025 to 0.085 was the team's decision to use 100% of its net proceeds for buybacks.

Pump shifted from initially planning to allocate about a quarter of its revenue to buybacks to adopting a buyback model almost entirely in the style of Hyperliquid. This change came after the market made it clear that a partial buyback model would not be well-received. This shift ignited one of the strongest large-cap token rallies this year in the illiquid and challenging Altcoin market.

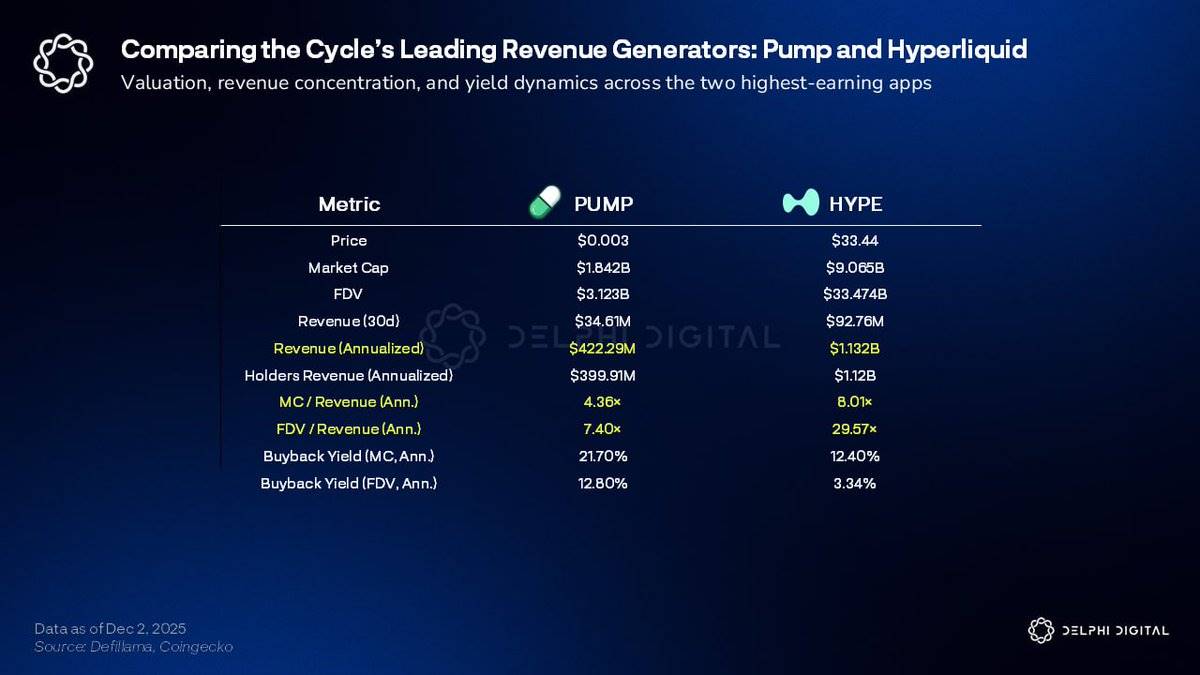

In terms of the buyback-to-market-cap ratio, no major token currently has a lower trading multiple.

Based on current data, Pump's annualized revenue is $422 million, and its market capitalization is $1.84 billion. This translates to a market capitalization/revenue ratio (MC/Rev) of 4.36 and an annualized buyback yield of approximately 12.8%. This level is significantly lower than other large-cap tokens, including Hyperliquid, which has an MC/Rev ratio of approximately 8.01 and a yield of approximately 3.34%.

Even so, the market remains skeptical about Pump's long-term commercial prospects.

Market concerns may include: whether the team can consistently launch meaningful products; the impact of future unlocking on the market with approximately 40% of the token supply still locked; and the uncertainty surrounding the final allocation of airdrops and creator incentives. Furthermore, the overall contraction of Meme coin activity in the crypto market, reduced terminal activity, and the sustainability of Pump's revenue base also raise questions.

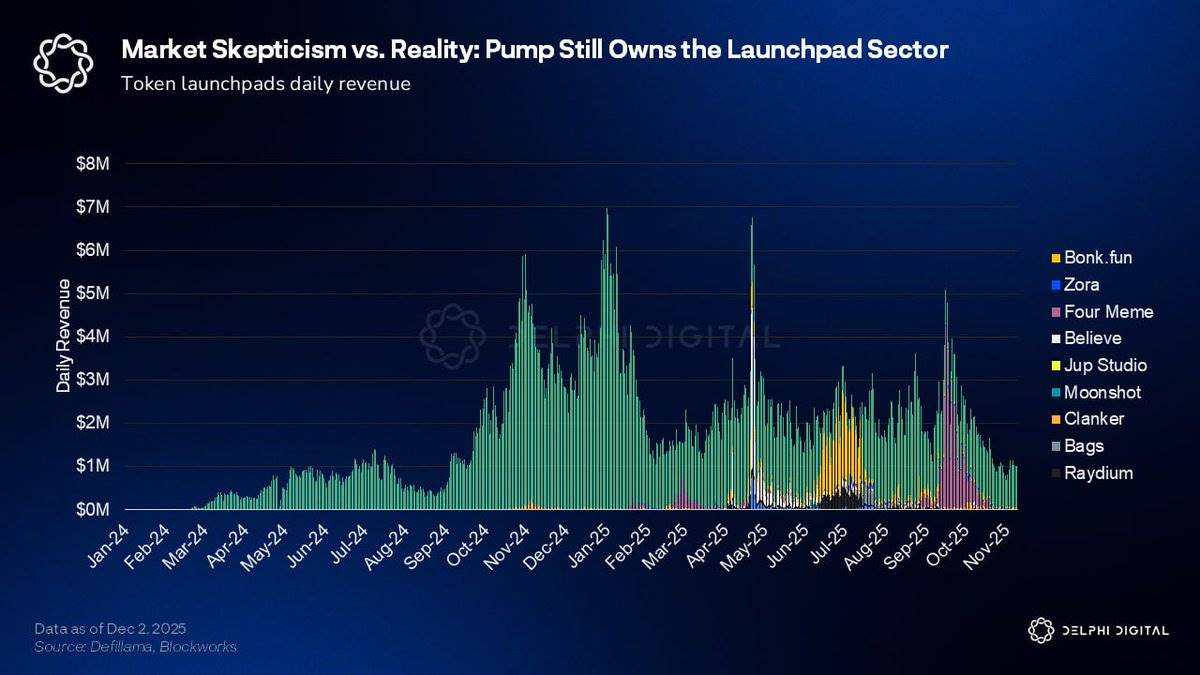

Despite these concerns, Pump remains dominant in the Meme coin issuance platform space, earning (and repurchasing) approximately $1 million per day even in the current extremely challenging market environment.

Pump's daily Launchpad revenue has plummeted by nearly 85% from its peak of almost $14 million at the beginning of the year, currently hovering around $2 million. However, competitors posed a threat to Pump's position only briefly, failing to deliver a substantial challenge. This aligns with our initial report's prediction of a brief challenge phase from Bonk and Raydium: even amidst cyclical contractions in trading volume, Pump maintained its structural advantage, holding a dominant share of industry activity.

The acquisition of Padre supports the view that Pump intends to expand into a multi-chain ecosystem beyond Solana, and has enabled support for BNB ecosystem assets through the Padre frontend. This also aligns with our earlier prediction that Pump would eventually acquire a terminal or terminal-related asset to strengthen user acquisition channels and integrate more user journeys.

In addition to these actions, the team has maintained a low profile recently. An investor conference call is planned, but has not yet taken place as of this writing; therefore, more details may be disclosed later.

The leadership team has also expressed interest in the broader ICM (Initial Community Fundraising) category, although we believe this is not a core area of Pump's current brand positioning or product strengths. Pump initially experimented with the Believe model but failed to gain real market attention. MetaDAO, on the other hand, has become a leader in the "high-quality founder + community" fundraising space.

Furthermore, the culture and structure of ICM seem somewhat misaligned with Pump's brand positioning. Pump's core brand revolves around a meme culture of speculation, speed, and creators, rather than long-term governance or a futarchy-based system. If Pump wants to succeed in the ICM space, they need to lean towards a more governance-focused structure and attract non-crypto teams looking to operate on-chain. However, this doesn't entirely align with the needs and positioning of Pump's current users and creators. While theoretically, ICM could potentially offer some benefits if implemented, we believe it's more of a secondary or optional direction than a natural extension of Pump's existing flywheel effect in 2026.

Looking ahead to 2026, Pump faces several key challenges: whether it can ultimately establish an incentive-compatible creator token model, whether it can achieve substantial expansion of the multi-chain market through Padre, how to manage the risks of token unlocking and decreased revenue visibility, and which product vertical to focus on. Currently, Pump's strategy appears to be diversified across multiple areas, including streaming, ICM, and mobile.

At some point in the future, the team may need to focus on a single core breakthrough. For most of 2025, that breakthrough seemed to be streaming, but now that's becoming less clear.

The bigger question is whether Pump can attract a larger number of creators outside of crypto. This may require a redesign of the creator token flywheel mechanism to provide stronger, longer-term incentives to support viral spread beyond the crypto-native user base. Pump has the basics to achieve this. The Bagwork craze of 2025 briefly demonstrated the potential for this model to succeed, at which point Pump seemed close to crossing the chasm.

Furthermore, Pump still has ample room to expand its product suite. One strategic direction the team should seriously consider is entering the iGaming (online gambling) or casino-related verticals. Adopting a Kick or Stake-like model would naturally align with Pump's speculative-driven user base. This direction would deeply synergize with its Meme coin and streaming strategic goals, and the profit potential in this area has already been proven.

Shuffle's net gaming revenue and weekly lottery distribution demonstrate the enormous potential of this sector under successful execution.

Pump's mobile app is another underutilized strength. Expanding further into mobile could broaden user acquisition channels, making the product more accessible to mainstream users, while providing creators with more monetization opportunities. Combined with iGaming, this would not only significantly expand Pump's potential audience but also strengthen the platform's existing success factors.

Despite the uncertainties, Pump remains one of the most resilient consumer apps in this cycle, maintaining its dominance even as the overall market landscape shifts. Substantial progress in any key direction could trigger a significant shift in market sentiment and help Pump break through, attracting a broader, non-crypto-native user base.

Twitter: https://twitter.com/BitpushNewsCN

BitPush Telegram Community Group: https://t.me/BitPushCommunity

Subscribe to Bitpush Telegram: https://t.me/bitpush