summary:

Hello everyone, it's been a long time! I sincerely apologize for the three-month delay in my update, as I've been designing and developing an AI product during this time. Frankly, changing directions is indeed difficult. Any innovation must be built upon a clear understanding of the boundaries of its industry before making incremental improvements that push those boundaries. Therefore, I needed to catch up on a lot of prerequisite knowledge in AI. Now that the product is initially completed, I have more time to come back and share my observations on the macro environment and Web3. Today, I want to discuss an interesting topic: how should we view and respond to the current situation of USDT's negative premium and the continuous strengthening of the RMB? In general, I think there's no need to panic excessively. When building your investment portfolio, it's still advisable to retain a certain proportion of stablecoin assets, but you can appropriately mitigate exchange rate losses through on-chain currency hedging.

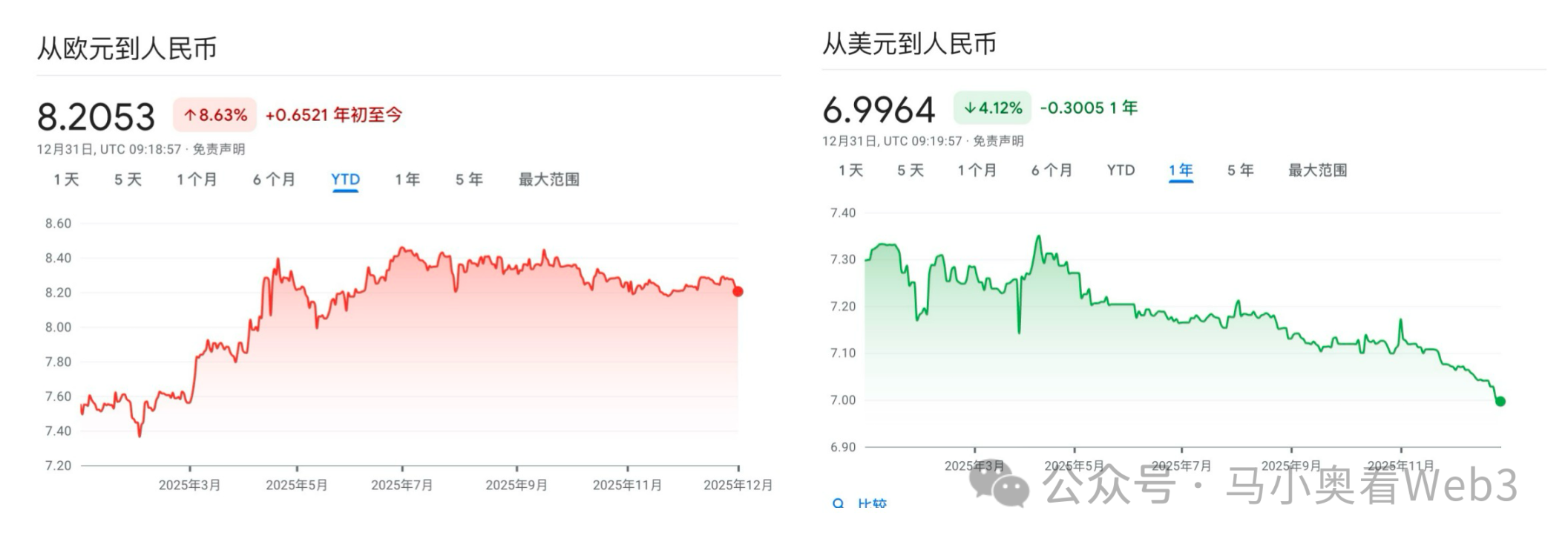

Why has the RMB entered an appreciation cycle, and why is USDT experiencing a negative premium?

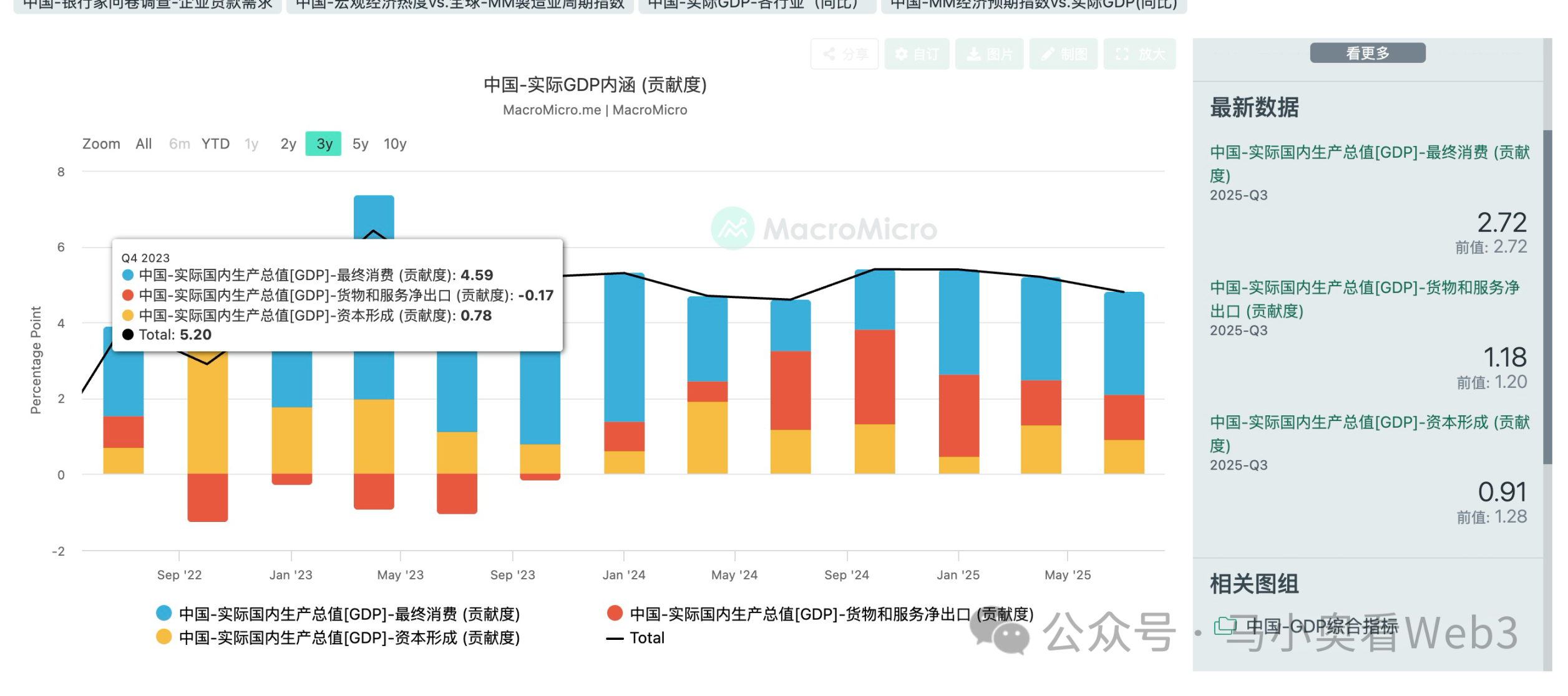

First, I'd like to discuss why the RMB is currently in an appreciation cycle. To address this, let's return to a fundamental economic concept: GDP. Generally speaking, while GDP has some shortcomings, it remains the simplest and most effective indicator for assessing the overall state of a country's economy. GDP is composed of:

GDP = C + I + G + (X – M)

in:

- C: Consumption expenditure: Total expenditure by households and individuals on final goods and services.

- I: Investment expenditures: Enterprise capital formation (new equipment, plant, etc.) and residential construction expenditures.

- G: Government spending: Government spending on goods and services (excluding transfer payments).

- X–M: Net Exports: Exports (X) minus Imports (M).

Having clarified this simple formula, the reasons for the appreciation of the RMB become clearer, mainly due to three points:

1. Attract foreign investment and increase investment spending.

The first benefit of RMB appreciation lies in rapidly attracting foreign investment inflows. We know that for some time now, both China and the US have faced the same problem—debt. In the US, this manifests in explicit federal government debt, i.e., the size of the national debt, while in China, it manifests in implicit local government debt. Because US Treasury bonds are tradable and held by foreign investors at a higher rate, the pressure to reduce debt is greater, as default risk is quickly reflected in bond prices through the secondary market, thus affecting the US's refinancing capacity. Therefore, only through dollar depreciation can the real value of dollar-denominated debt for foreign creditors decrease. This "inflation tax" reduces the real value of nominal debt. The means are naturally interest rate cuts and quantitative easing. In contrast, China's local government debt is more domestic debt, mainly held by domestic commercial banks or domestic investors. There are relatively more ways to reduce debt, such as using time to buy time, such as debt rollovers and transfer payments. Therefore, relatively speaking, the RMB exchange rate does not face as much pressure from the debt problem. However, this debt problem has had an impact on both China and the United States, limiting the government's ability to borrow. In other words, it is not easy to boost the country's GDP by increasing government spending. Therefore, in order to stimulate the economy at this stage, the appreciation of the RMB is conducive to attracting capital backflow.

2. Boost consumption and increase consumer spending.

Another benefit of RMB appreciation is that it makes it cheaper for domestic investors to consume foreign goods. This is mainly reflected in two aspects. First, it gives ordinary consumers more money for consumption and investment. This is particularly evident in essential consumer goods categories, such as food and energy, which account for the largest proportion of total consumer spending. It is believed that in the near future, most people will see more and more imported goods on supermarket shelves, and their prices will become increasingly cheaper. Second, it lowers the cost for businesses to import foreign raw materials or key components, increasing profit margins and allowing them to have more capital for business expansion and profit distribution.

3. Easing political friction caused by international trade and reducing government spending.

Since the announcement in November that China's trade surplus had surpassed $1 trillion, there has been increased international discussion about the undervaluation of the RMB, and China is facing growing friction in trade negotiations with major exporting countries, particularly the major consuming nations of the European Union. Why is this?

We know that, theoretically, in accounting principles, the sum of global international trade current accounts must always be zero, because a country's exports are always another country's imports, and income/transfer payments are also mutually corresponding economic flows. Therefore, when a trade surplus reaches a new high, it inevitably means that the trade deficits of some net importing countries are also increasing. In the current macroeconomic environment, all countries prioritize boosting their economies; therefore, a widening trade deficit will drag down their GDP growth, especially for some developed countries that have already entered a low-growth phase. For them, even small fluctuations in data can have a greater impact on GDP growth. There are generally two ways to alleviate trade deficits: first, increasing tariffs based on trade protectionism; and second, adjusting exchange rate relations. The former has come to an end with the temporary truce in the tariff war between China and the US, while the orderly appreciation of the RMB is conducive to quickly alleviating political conflicts arising from trade frictions with other countries, thereby reducing the resulting government spending.

While RMB appreciation has the aforementioned advantages, a core principle is that it must be stable and orderly, not too rapid. The recent month's RMB appreciation has been noticeably too rapid. This is partly because the economic growth target for the first three quarters of the year has already been achieved at 5.2%, essentially reaching the annual target of "around 5%." Therefore, appropriately loosening the appreciation range is beneficial for making early arrangements for economic transformation in the coming year, observing market developments, and proactively identifying development opportunities and risks. Otherwise, with its massive foreign exchange reserves, the central bank could relatively easily stabilize the exchange rate.

I believe the rate of RMB appreciation will slow significantly next year. The reason is simple: while the contribution of net exports to China's GDP growth is converging, it remains crucial. If the RMB appreciates too rapidly, it will obviously lead to a rapid decrease in net exports, thus putting pressure on achieving next year's economic growth target.

Having clarified the reasons for the short-term appreciation of the RMB, let's discuss why USDT exhibits a negative premium. I believe there are three main reasons:

1. The crypto market remains sluggish, lacking sufficiently attractive investment opportunities, prompting investors to reallocate their portfolios.

2. At the end of the year, many companies engaged in international trade tend to concentrate their foreign exchange settlements, leading to a surge in demand for converting US dollars into RMB. We know that there are significant restrictions on onshore RMB exchange quotas. Therefore, many small and medium-sized enterprises (SMEs) engaged in international trade or overseas operations choose to settle their foreign exchange through USDT, which avoids quota restrictions and is more convenient and cost-effective.

3. The Chinese government has recently tightened its policies on stablecoins, which has increased the risk premium for cryptocurrency investments, thus triggering a flight to safety.

In conclusion, the author believes that the negative premium of USDT will not last long. This situation is more affected by short-term changes in supply and demand. However, the strong appreciation of the RMB in the short to medium term will inevitably lead to RMB-denominated investors suffering certain exchange rate losses.

Should I exchange my USD stablecoin back into RMB?

Now that the RMB has entered an appreciation phase, should we exchange our USD stablecoins back into RMB to avoid exchange rate losses? I believe that unless your portfolio has an excessively high proportion of USD stablecoins, in which case you can adjust accordingly, it's advisable to maintain a certain percentage in your asset allocation. There are three reasons for this:

1. Exchange losses due to short-term USDT negative premium: As mentioned in the previous analysis, I believe the current USDT negative premium is due to short-term factors rather than a structural risk. Rushing to exchange currency at this time could result in significant exchange losses. Therefore, I suggest that even if portfolio adjustments are necessary, it's advisable to wait until the negative premium reverts to its mean before taking any action.

2. Opportunity Cost: While the overall fundamentals of the Chinese economy have shown resilience, it still faces significant challenges, namely the loss of wealth effect across society due to declining real estate prices. Therefore, in this context, economic policy should prioritize stability, focusing on debt reduction, industrial restructuring, and optimized redistribution. Thus, although we have seen a general rise in the Chinese stock market, I believe this should only be viewed as valuation repair or speculation, and does not necessarily indicate a significantly favorable environment for long-term development. Furthermore, the continued decline in RMB government bond yields amplifies the opportunity cost of this strategy. Holding stablecoin assets, on the other hand, offers greater flexibility and facilitates global asset allocation, especially given the ample liquidity in the US during its interest rate cut cycle.

3. Uncertainty Regarding RMB Appreciation: The tariff dispute between China and the US is not permanently resolved, but merely paused for a year. The US is unable to respond to the rare earth issue in the short term, and with the midterm elections approaching, it can only call a halt and focus on internal development. However, this does not mean the tariff war will not reignite. We have systematically analyzed the Trump administration's policies in previous articles. Therefore, before achieving the goal of bringing key manufacturing back to China, the possibility of a renewed tariff war remains high. The RMB exchange rate will inevitably be affected.

How to hedge exchange rate losses using on-chain strategies, particularly with gold and Euro stablecoins.

So, based on this strategy, how can we appropriately hedge against exchange rate losses caused by the appreciation of the RMB? Our first thought is naturally to use currency derivatives to hedge the impact of RMB appreciation. However, this is extremely difficult to achieve in an on-chain environment. At the beginning of last year, I considered creating a decentralized currency derivatives platform to address this demand in advance. However, research showed that the development of some competing products was not satisfactory. Taking DYDX's Foreign Derivatives section as an example, we can see that the market depth is very shallow and liquidity is clearly insufficient, indicating that market makers have little interest in this business. The reason for this is the regulatory pressure. We know that exchange rate controls have always been a highly valued tool for various manufacturing countries, such as China and South Korea. Therefore, compared to cryptocurrency investment, currency derivatives certainly face a higher level of regulation, and most investors with currency hedging needs are also investors from these countries, so the resistance they face is considerable.

However, this does not mean there are no ways to alleviate the situation. I believe the following three asset classes deserve the most attention:

Stablecoins in Hong Kong Dollar, Japanese Yen, and South Korean Won: Around the middle of the year, with the US passing stablecoin legislation, countries around the world launched a wave of stablecoin issuance. The unique characteristics of the Hong Kong dollar and the overlapping industrial structures of East Asian countries inevitably lead to a convergence in exchange rate trends. Therefore, investing in such stablecoins can, to some extent, mitigate exchange rate losses caused by the appreciation of the RMB. However, recently we have clearly seen that countries are tightening their exploration of stablecoin issuance due to concerns about exchange rate controls. Therefore, we can only say that we should keep an eye on it and allocate funds after a mature product is launched.

On-chain gold RWA: Gold's price increase over the past few years has been astonishing. Geopolitical uncertainty and expectations of a depreciating dollar have fueled the demand for gold assets. For on-chain investors, purchasing RWA tokens is relatively easy and offers ample liquidity. Examples include Tether Gold and Pax Gold. However, discussions about whether gold is in a bubble have persisted. The recent sharp fluctuations in precious metals suggest that the market has entered a delicate game of strategy. For investors with lower risk tolerance, remaining on the sidelines is safer than taking pre-emptive measures.

Euro stablecoins: In my opinion, euro stablecoins are the most noteworthy asset class among these three. Firstly, Circle's compliant euro stablecoin, EURC, has a sufficiently large issuance volume and good liquidity. Secondly, I personally believe that the euro-yuan exchange rate fluctuation will be more moderate compared to the dollar. The reasons are as follows:

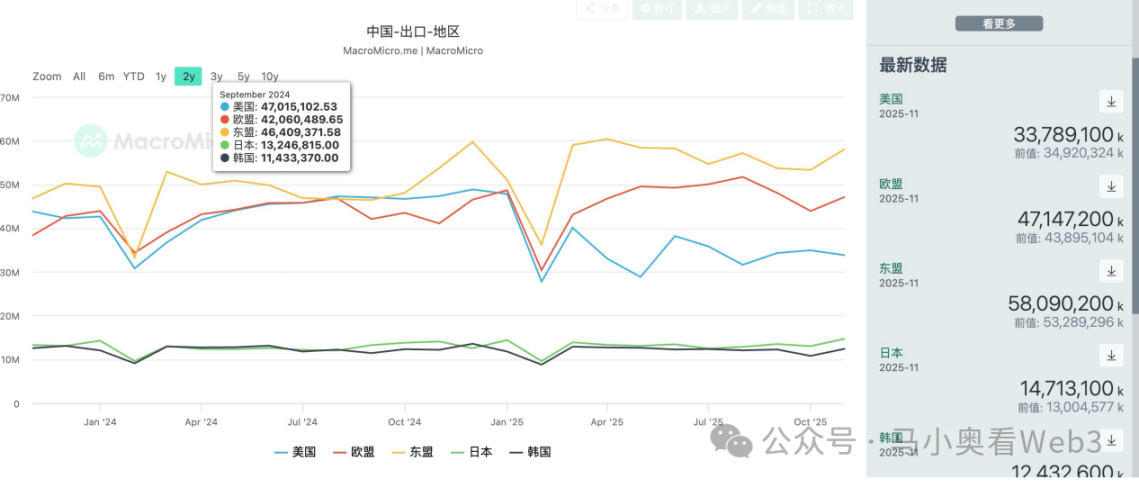

Let's look at China's export data. We can see that the top three contributors to China's exports are currently ASEAN, the EU, and the US. Affected by the trade war, China's exports to the US have shown a clear downward trend; of course, we're not discussing re-exports. The most significant contributors to the incremental growth are still the EU and ASEAN.

We know that ASEAN is primarily composed of developing countries with relatively high economic growth rates. This means that the impact of net exports is mitigated by other indicators. Furthermore, ASEAN has absorbed a significant amount of low- and mid-range product transfers and investments from China, and a large portion of its imports come from machinery, equipment, and industrial goods necessary for industrial upgrading. Therefore, the overall impact on the economy is generally positive. Of course, on the political front, the rise of China's military power has also created certain constraints. Therefore, we can see that China and ASEAN are showing a trend of restraint in political friction.

However, the story unfolds differently with the EU. Manufactured goods constitute a larger proportion of China's exports to the EU, resulting in higher profit margins compared to other markets like ASEAN. Therefore, Europe is naturally a crucial market for China's stablecoin trade surplus. Since trade settlement between China and the EU is primarily in euros, there is reason for the RMB to maintain a lower exchange rate against the euro in order to enhance the influence of Chinese goods in this market.

Of course, exchange rate risk also lies in how to resolve political friction with the EU. Since most EU countries are developed nations, and manufacturing accounts for a much higher percentage of GDP than in the US (European manufacturing accounts for 15% of GDP, while in the US it's less than 10%), this means that wages constitute a larger proportion of the income of ordinary Europeans compared to capital gains from investment. In the past, the EU has lost access to cheap energy from Russia, leading to rising costs and significantly impacting its manufacturing sector. In particular, China's industrial upgrading has severely impacted one of Europe's pillar industries, the automotive sector. This means a decline in overall European industrial profits. The decline in corporate profits leads to two effects: a decrease in government tax revenue and a slowdown in wage growth. The former will also affect the maintenance of Europe's previously high welfare system through fiscal constraints. Both of these will reduce the wealth effect on residents, thus affecting consumption. On the investment front, due to a lack of high-quality AI targets, Europe has lost its competitiveness in the AI field, with most European capital flowing into the US AI market to seek higher expected returns. Therefore, the investment outlook is also not optimistic. Therefore, the impact of net exports on the economy is amplified, leading to a more aggressive stance from European governments towards trade deficits.

However, this author believes that the EU currently lacks the bargaining power that the US demonstrated in its tariff war with China, and EU member states also have differing attitudes towards China, such as those of Hungary and Spain. Therefore, it is difficult to secure more benefits during negotiations. Thus, this author believes that the EU-China trade rebalancing will not ultimately be based on a significant exchange rate adjustment, but rather on an agreement for local investment of euro profits as the final cooperation framework. On the one hand, compared to other emerging markets such as India, Vietnam, and Brazil, Europe has a more robust capital market system and relatively better capital protection. China currently has ample foreign exchange reserves, allowing it to increase profit margins through reinvestment. On the other hand, a stable exchange rate also helps Chinese goods maintain sufficient competitiveness in Europe.

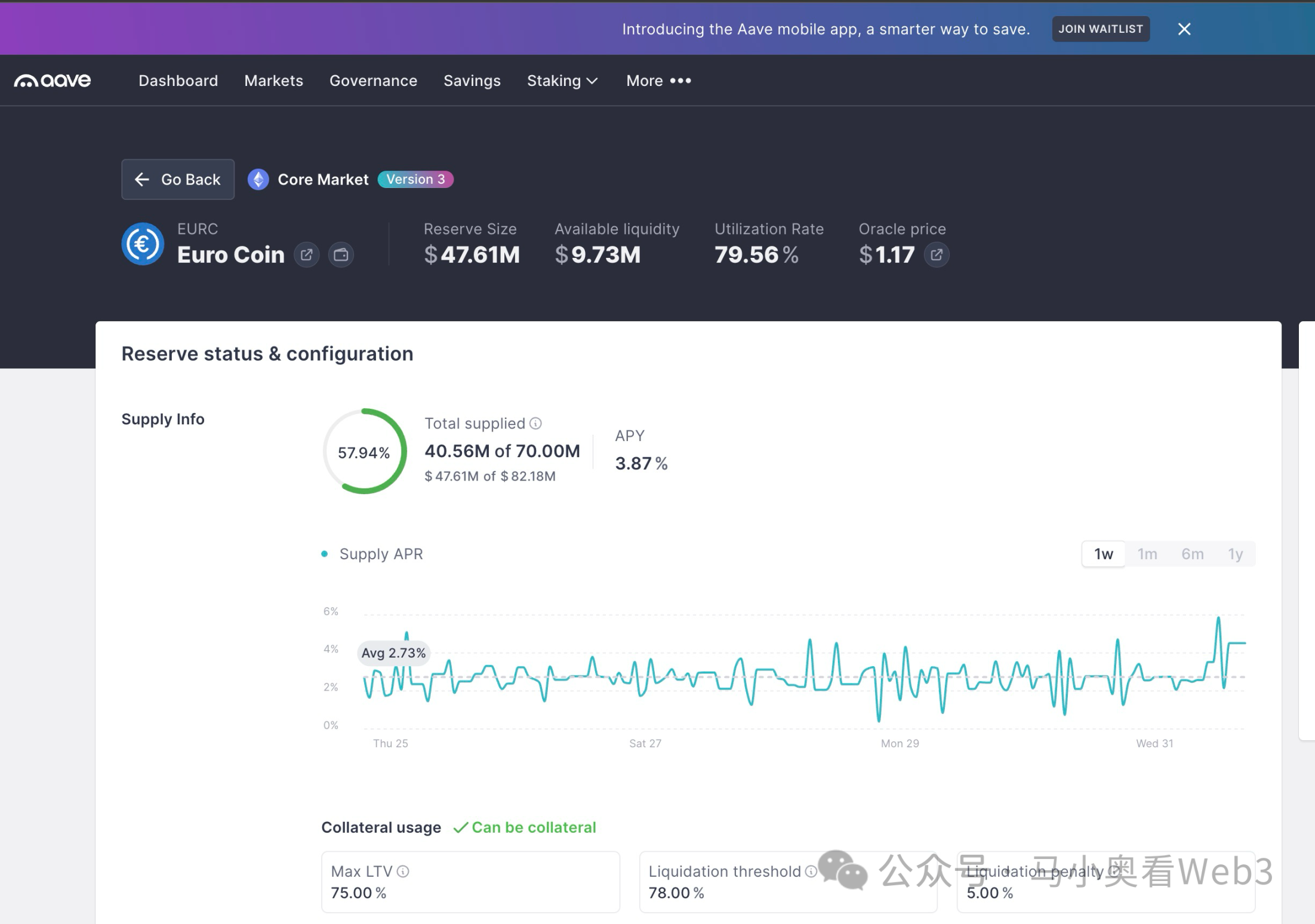

Returning to the topic of exchange rate hedging strategies, I believe a practical approach is to convert USD stablecoins into EURC, and then deposit them on leading platforms like AAVE to earn interest. Currently, the lending rate can reach 3.87%, which is quite attractive. If you want to maintain positions in risky assets like BTC while hedging exchange rate risk, you can use EURC as collateral to borrow USD stablecoins and then allocate your assets, such as purchasing BTC.