Ahoy! Long time no post. 2025 has been a blur welcoming a new daughter and building at Powerhouse, but I couldn’t resist chiming in with a take on the top DeFi memes for 2025. I’ve done this for every year of the 2020s (2020, 2021, 2022, 2023, 2024). I know the timeline is onto 2026 predictions but I’m more of a reflection kind of guy.

There’s a lot of negativity in the broader crypto space best caputred by Dougie Deluca’s “Crypto is dead” post that argues that crypto culture will not be adopted even if blockchains are. That feels right because the decade’s excesses — memecoins, VC L1s, Web3 games, NFTs — have poisoned the well.

But DeFi still feels like the cleanest part of crypto: transparent markets, composable primitives, and a culture that takes the plumbing seriously. If crypto culture fades, maybe DeFi’s memes get louder because they’re tethered to utility instead of vibes.

We’ll see. The world keeps barreling to a financial system run on smart contracts on truly digital rails, but what will it look like? One can only meme.

Solana bros are shilling Internet Capital Markets hard; TradFi has embraced RWAs; Stripe is wielding stablecoins as a trojan horse; or perhaps Coinbase and Robinhood hope tokens just eat everything.

DeFi is still where I’m planting my flag. It’s just cooler.

Anyway, here are the top memes and charts for DeFi in 2025

1. STABLE GENIUS

The biggest victory for DeFi in 2025 was regulatory momentum for stablecoins. The GENIUS Act, signed into law in July, created the first federal framework for payment stablecoins by requiring 1:1 reserves and regulated issuance. It might end up as the most significant bipartisan legislation passed in the 2020s (or the CHIPs Act). That says more about the rancor and stasis in Washington these days but it says even more about the undeniable utility of onchain money. Stablecoins are simple, easy to understand, and carry no speculative baggage.

With the rules set, the adoption phase has finally arrived. We are seeing three distinct categories emerge:

Savings & Investment (The Bedrock)

Payments (The Growth)

Agentic AI (The Frontier)

Issuers love to talk about transaction volume, but the reality is that the vast majority of the $300b now onchain is there to store wealth. Total stablecoin supply remains the ultimate scoreboard for comparing chains. But going forward, the growth story shifts.

The payments layer is poised to explode in 2026, led by stablecoin cards and the “fintech-ification” of crypto. Meanwhile, AI agents using stablecoins makes intuitive sense but still seems a ways off.

What stablecoins have proven is a sustainable business model. Stablecoins turn distribution into deposits: win the wallet and you capture the spread on reserves plus fees on flows. Tether is widely known as one of the most profitable companies in the world, while Circle soothed the haters this year with a public markets valuation 5x as big as the industry valued it a year ago.

Now stablecoins look less like a crypto feature and more like the revenue strategy for a new generation of consumer financial products.

Read more: The Stablecoin Pact: Crypto’s New Order after the GENIUS Act

2. Ethereum L1

For years, Ethereum supporters and haters alike preached of a multichain future, but the story of 2025 was one of consolidation: DeFi apps relearned that being everywhere has a cost, and liquidity increasingly concentrated on a smaller set of chains. Ethereum’s L1 is still standing strong after several years of well-financed (and incentivized) competitors trying to entice liquidity away.

In 2024, “parasitic L2s” was on our list of top memes, but a reboot at the Ethereum Foundation has recommitted the ecosystem to scaling the L1. It shows: gas costs are at multi-year lows even though transactions are at all-time highs. The refocus on the L1 has not greatly affected Ethereum’s L2 ecosystem, either. Base and Arbitrum are major ecosystems in and of themselves, while launching an L2 on Ethereum seems to be the clear winner of the “appchain” thesis.

It seems that Ethereum might be able to have its cake and eat it too. The next few years will see an onslaught of TradFi and Big Tech companies launching a “stablecoin + chain“ combo. There will be more Robinhoods and Celos that see the benefits of being an Ethereum L2 than Tempos and Arcs that go through the trouble of launching an L1.

This consolidation is quantifiable. Ethereum L1 retains a dominant 57% share of stablecoin supply, but the real story is credit: it has $25bn of active loans, roughly 10x its nearest competitors (Plasma and Solana).

That’s not to say Ethereum L1 will be the only game in town (especially as it relates to this year’s meme #4). The pie will be big enough for alternatives but this was a year where Ethereum’s L1 reasserted itself.

3. Risk curators

Risk curators — or, as I prefer, DeFi vault managers — were one of the clearest signs in 2025 that DeFi is maturing. Their lineage runs back to 2020 and Yearn, but the category leveled up once ERC-4626 standardized vault design and modular lending platforms like Morpho and Euler made it easy to package strategies into one-click products. In practice, vault managers have become the user-facing layer of DeFi: they choose collateral, set risk parameters, and route capital across markets so users don’t have to.

2025 was a breakout year for the sector, with total AUM surging from $1.6b in January to a peak of over $10b by late October. However, the market proved fragile. In November, the collapse of Stream Finance triggered a contagion event that wiped out hundreds of millions in value, punishing managers who flew too close to the sun with opaque, yield-chasing looping strategies.

MEV Capital and Re7 took the hardest hits with AUM decreasing 80%+ for both over the last three months. Steakhouse and Gauntlet have emerged from the wreckage as the clear winners with their marketshare sitting at 26% and 21% respectively.

With the hierarchy of trust now established, the focus for 2026 shifts to distribution and the race to capture mainstream capital. Vault managers need to win both institutions (clear mandates, reporting, liquidity discipline) and retail (simple UX without hiding where yield comes from). The most scalable path may look like a “DeFi mullet”: centralized rails in the front and onchain vaults on the back end — plus new channels like L2 treasuries putting bridged assets to work and, maybe even from Digital Asset Treasuries (DATs).

Read more: DeFi Curators in 2025: Navigating Chaos, Building Resilience [Chorus One]

4. Perps

Perps have long been crypto’s most successful product, but they’ve been dominated by CEXs. While protocols like dYdX, Synthetix and GMX innovated with novel liquidity models, they historically struggled to match the high-frequency experience of centralized venues. That gap finally closed in 2025 as specialized execution environments made onchain perps fast enough to compete on feel, not just ideology.

At the beginning of the year, Binance’s daily perp volume was roughly 5-6x that of all onchain DEXs combined. Today, onchain venues regularly flip them.

Hyperliquid kicked the door down by building a high-performant perps protocol, but they’ve been joined by Lighter, Aster and others that have been able to replicate their success.

An astute reader may notice I’m calling these protocols “onchain” rather than “DeFi.” In my book, DeFi requires verifiability, and much of the leading perps stack still falls short: Hyperliquid is not open-source, and neither is Aster. Lighter just made their code source-available, which is a meaningful step toward making performance and transparency coexist.

The category still has sharp edges, and the auto-deleveraging incident of October 10 made that plain. Gauntlet’s Tarun Chitra published research claiming Hyperliquid’s queue-based engine inefficiently destroyed over $650 million in trader profits, arguing for a pro-rata model instead. Paradigm’s Dan Robinson and the Hyperliquid team pushed back, saying Tarun’s model incorrectly assumed total equity seizure rather than standard position closure.

This controversy illustrated the precise danger of closed-source execution: without visible code, the market was forced to debate theoretical models rather than simply verifying the facts.

Ultimately, while perps may be used by gamblers now, the success of these protocols brings the vision of onchain price discovery closer to reality. The question in 2026 is whether equity perps will emerge and whether they find a market outside of crypto gamblers.

Read more: Autodeleveraging, Hyperliquid, and the $653m Debate [Nagu/Dare to Know]

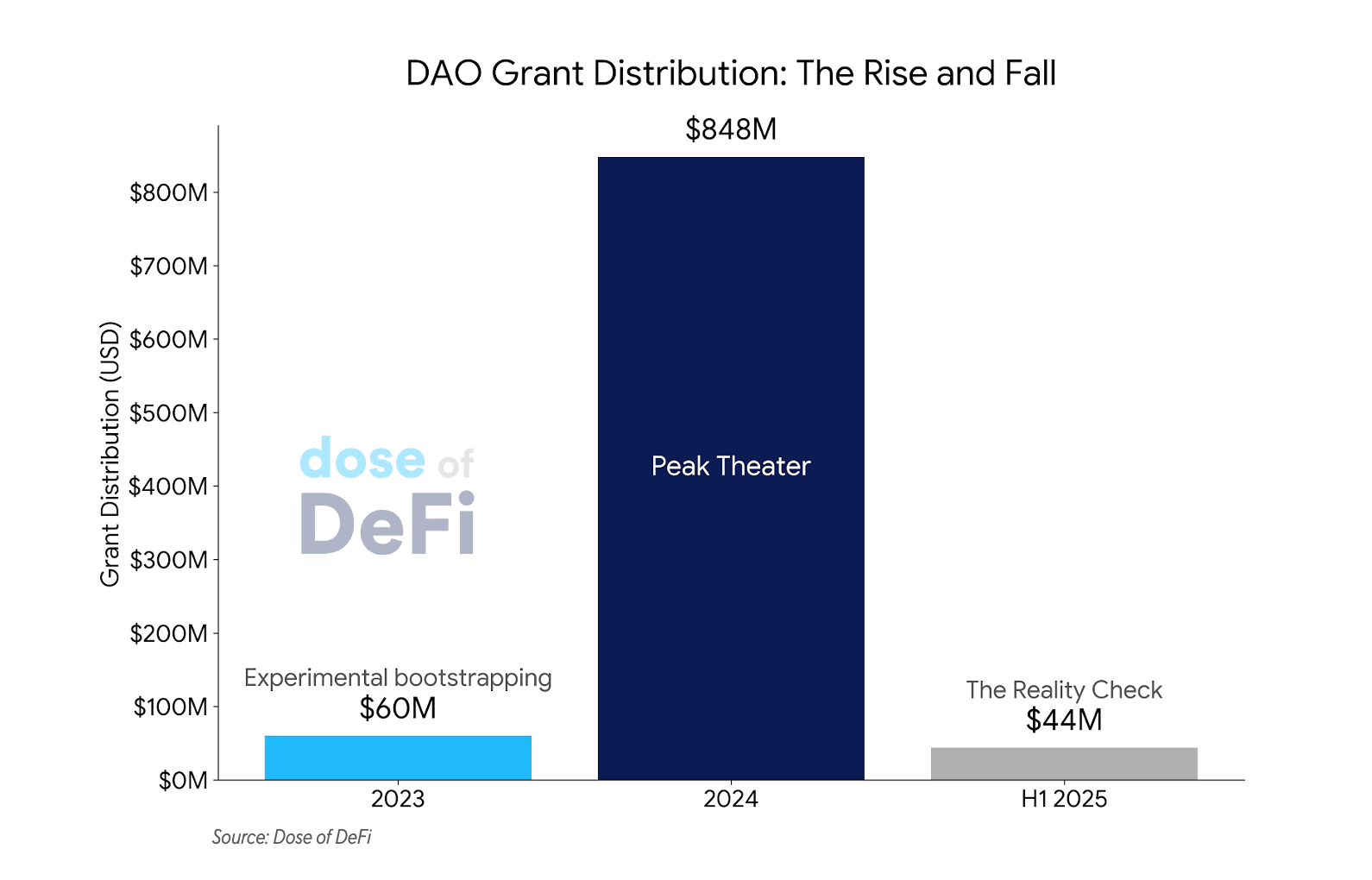

5. DAOs are dead

As a longtime DAO contributor, this has been a tough meme to digest. But the shift is real. DeFi governance is moving away from “DAO-first” ideals and toward control fights and corporate-style consolidation. The latest example is the civil war inside Aave over who controls Aave’s IP and the fees on Aave.com. It is also showing up in the numbers: DAO grant distribution fell to $44m in the first half of 2025, down from $848m in all of 2024.

The same pattern is playing out elsewhere. a16z called for the end of the foundation era this year and Uniswap is moving in that direction with the UNIfication proposal, which just passed a Snapshot vote last week. The proposal folds the foundation into Labs while rerouting economic value from the entire Uniswap Ecosystem into the UNI token.

Here’s the uncomfortable truth: the DAO meme was often used as a token launch strategy. It gave projects a credible claim to decentralization, especially when regulatory pressure was high. As the regulatory winds shift, there is less appetite for decentralization theater.

That is not a bad thing. For years, too much of crypto treated “decentralization” as a loophole for issuing speculative assets. The real point of decentralization is simpler: it changes the market structure. When anyone can build, fork, or route around the network, it creates credible alternatives and forces competition, which is what drives innovation over time.

Before blockchains, we could only introduce this kind of competition at the economy level, using markets and governments to check monopolies. But in the digital realm, those checks hit a ceiling because the infrastructure itself stayed proprietary. Governments can regulate firms, but they can’t make a privately hosted execution environment neutral or verifiable. When a single company controls the servers, the front end, and the rails, they control the rules. Blockchains changed that by enabling execution on a shared, permissionless base layer, extending free-market dynamics into digital infrastructure itself. They are a necessary step toward credible decentralization, but they are not sufficient.

We need coordination structures that align incentives in a network. This was the dream of DAOs but they have failed.

What’s missing is an economic model that lets open-source software capture value, and a network structure that can interface with the real world.

At Powerhouse, we call the framework open-source capitalism: making open-source investable by tying it to revenue-generating hubs and turning profits into durable funding for builders. We call the structure a Scalable Network Organization (SNO): a DAO as the decision layer, connected to operational, commercial, investment, and IP entities so the network can act like a company without becoming one.

DAOs are dead. Long live DAOs.

That’s it! Feedback appreciated. Just hit reply. Just finished before the year is done! Written primarily in Austin, Texas. I hope everyone has a happy New Year.

Dose of DeFi is written by Chris Powers, with help from Denis Suslov and Financial Content Lab. I spend most of my time contributing to Powerhouse, an ecosystem actor for MakerDAO/Sky. Some of my compensation comes from SKY, so I’m financially incentivized for its success. All content is for informational purposes and is not intended as investment advice.