Author: Packy McCormick (Founder of Not Boring, former advisor to a16z Crypto)

Compiled by: Jia Huan, ChainCatcher

Today (January 9), a16z announced that it has raised $15 billion in new funding.

To commemorate this moment, I've written an in-depth analysis of the company. I spoke with the company's general partners, limited partners, and founders of portfolio companies with a total valuation of approximately $200 billion , reviewed documents and presentations, and analyzed the returns of a16z's funds since its inception.

There are many articles online about where a16z's methodology goes wrong. You may be familiar with these arguments. They've been a constant presence since the company's inception.

I think it's much more interesting to understand what all these once-right smart people think a16z is doing now.

Frankly, aside from a16z's official employees, I'm probably the most biased observer you can find.

For over two years, I have been an advisor to a16z crypto (but have not received any compensation from the company). Marc Andreessen (co-founder of a16z) and Chris Dixon (head of a16z Crypto) are limited partners at Not Boring Capital. I occasionally appear on the same equity structure sheet as a16z. I am friends with many people at the company and with most of the new media team. I work with these people and like and respect them.

However, readers aren't expecting me to analyze whether a16z's fundraising presentation at this moment is a worthwhile investment. Established institutional partners have already made their decision, investing $15 billion. It may take a decade to know if they made the right decision, and neither what I nor any critics say can change that outcome, just as it has in the past.

What I hope to offer is a way of thinking about "what a16z really is," based on my unique experience. I believe a16z is the best-marketed company in the venture capital world. It is able to, and truly is, tell a story about itself. In my experience, I can tell you that its story is consistent with its actions. What a16z says to the public is the same as what it says when training its internal team. Its current publicity is exactly the same as what it said in its first fundraising prospectus. And you can judge its return on investment for yourself.

There are many great venture capital funds and investors, some of the best of whom have recently become well-known. Their methods and successes are increasingly appreciated and understood.

But a16z is doing something different, bigger, and less… low-key. This doesn’t feel like what venture capital “should” be like, partly because I think a16z doesn’t care whether it’s doing “venture capital.” It just wants to build the future and devour the world.

Let's begin.

"I live in the future, so the present is my past, and my existence is a gift." — Kanye West (American rap superstar and entrepreneur)

a16z has heard your feedback.

It's said to be too noisy. Politically, it should "shut up and just play ball (investment)." It disagrees with one or two recent investments. It's considered inappropriate to retweet the Pope's tweets. It's said that such a massive fund could never generate reasonable returns for LPs.

a16z definitely heard it. At this very moment, it has been listening to you for nearly twenty years.

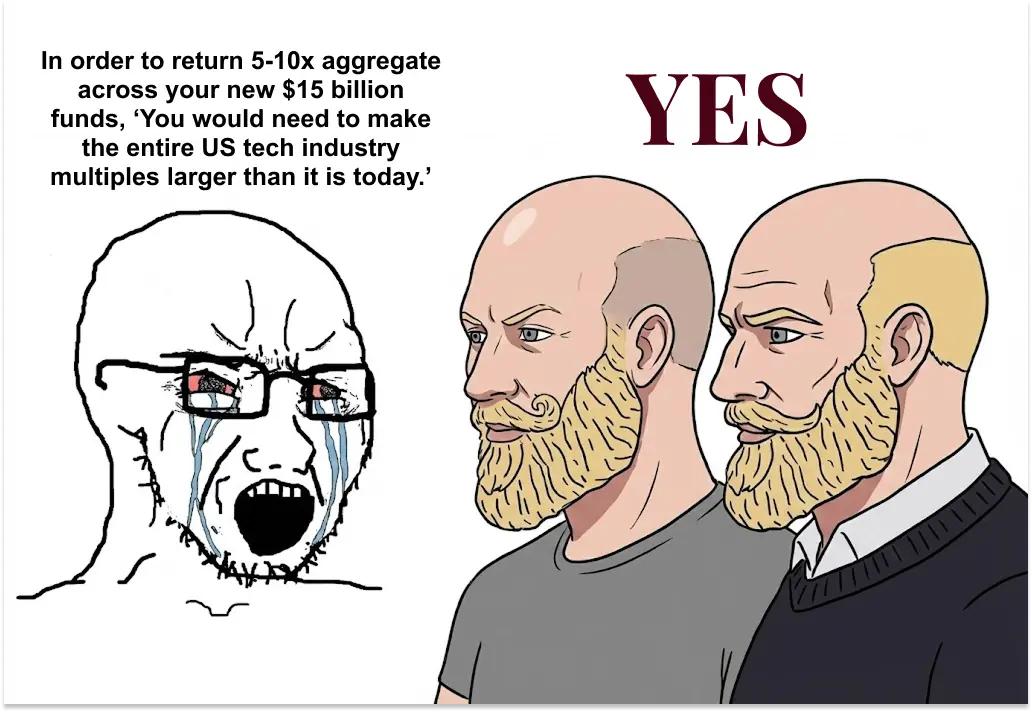

Just like back in 2015, when Tad Friend (a contributing writer for The New Yorker) was writing "The Pioneers of the Future" and had breakfast with Marc Andreessen, Friend had just heard from an eager competitor that a16z's funds were too large and their shareholdings too small, so that to achieve a 5-10x total return on their first four funds, their portfolio would need to be worth between $240 billion and $480 billion.

“When I started checking the math with Andreessen,” Friend wrote, “he made a jerking-off motion and said, ‘Blah blah blah. We have all the economic models, we’re hunting elephants, we’re chasing big prey!’”

I hope you will remember this scene.

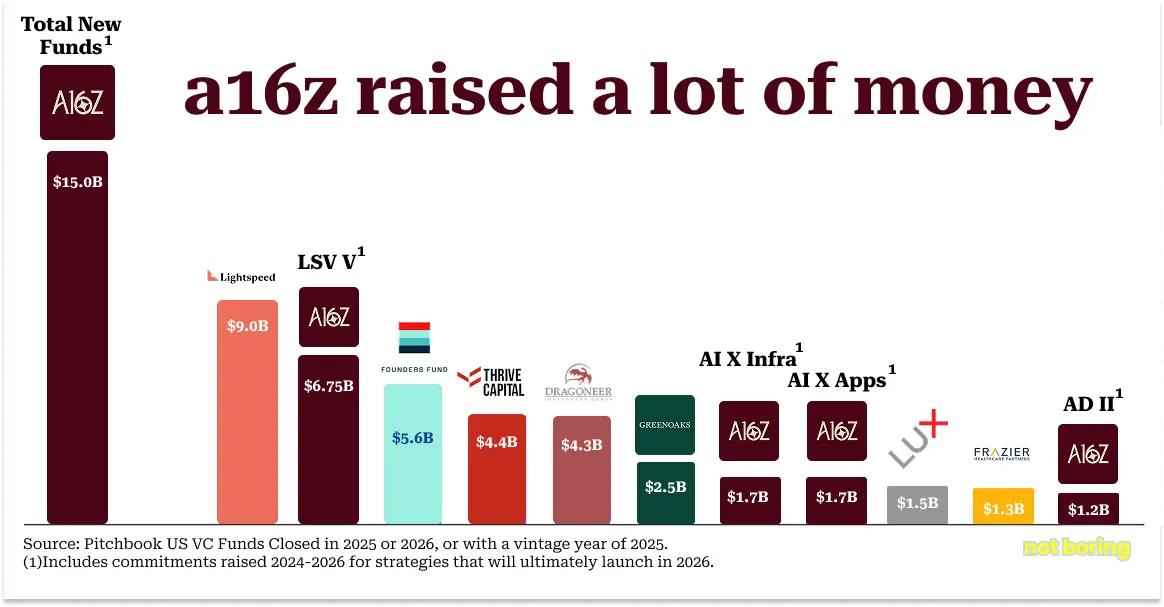

Today, a16z announced that it has raised a total of $15 billion across all its strategies, bringing its total assets under management to over $90 billion.

In that year, although VC fundraising was dominated by a few large companies, a16z raised more money than the next two funds, Lightspeed (which raised $9 billion) and Founders Fund (founded by Peter Thiel, which raised $5.6 billion), combined in 2025.

In that year, although VC fundraising was dominated by a few large companies, a16z raised more money than the next two funds, Lightspeed (which raised $9 billion) and Founders Fund (founded by Peter Thiel, which raised $5.6 billion), combined in 2025.

In what has been the worst VC fundraising market in five years, a16z accounted for over 18% of all US VC fund fundraising in 2025. In that year, the average VC fund takes 16 months to raise capital, while a16z completed fundraising in just over three months from start to finish.

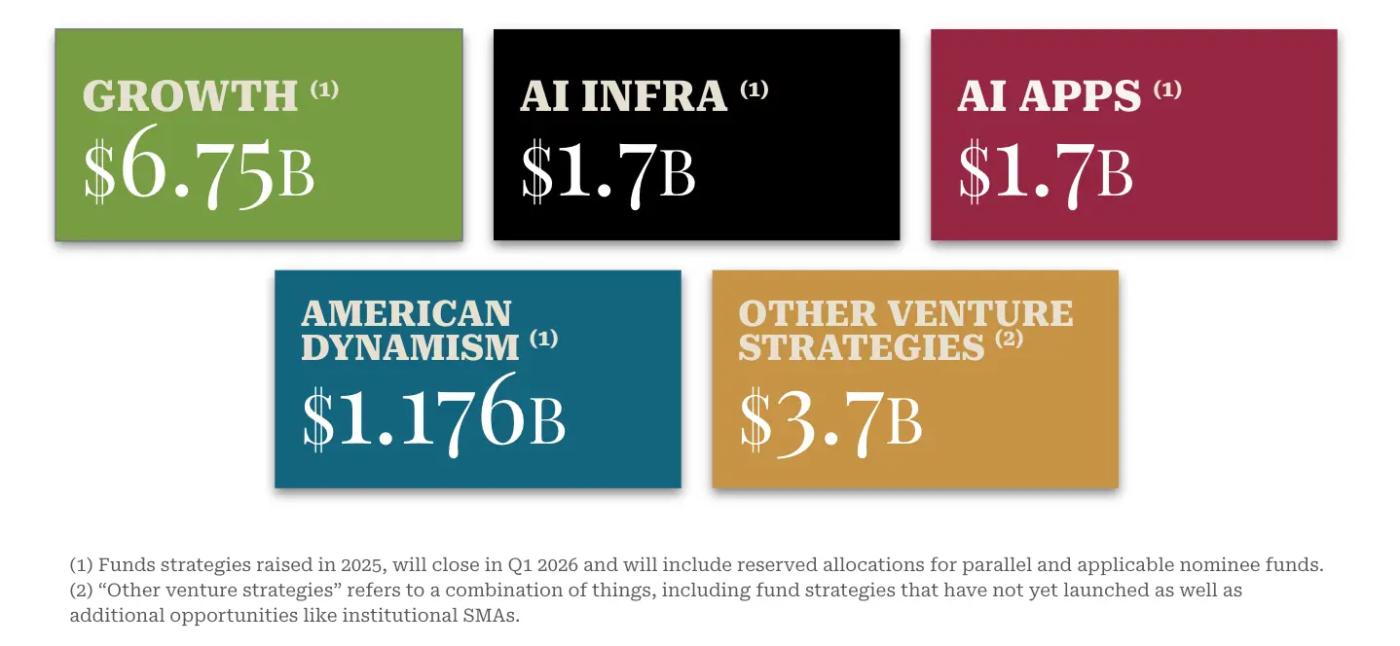

Breaking it down, a16z has four individual funds. If we compare them individually with the total fundraising amount of other companies, they would all be in the top 10 in 2025: Late Stage Venture (LSV) V will rank 2nd, Fund X AI Infra and Fund X AI Apps will tie for 7th, and American Dynamism II will rank 10th.

Some might say that this is far too much money for a venture capital fund, and no extraordinary returns can be expected. To that, I imagine the a16z all making a shooting gesture and saying, "Blah blah blah." This is elephant hunting, chasing large prey!

Today, across all its funds, a16z is an investor in 10 of the top 15 privately held companies by valuation: OpenAI , SpaceX , xAI , Databricks (a big data AI platform giant), Stripe (a global payments giant), Revolut (a UK fintech unicorn), Waymo (Google's self-driving car company), Wiz (a cloud security unicorn), SSI (a security intelligence company), and Anduril (a defense technology company).

Over the past decade, it has invested in 56 unicorn companies through its funds, more than any other company.

Its AI portfolio encompasses 44% of the value of all AI unicorn companies, more than any other company.

From 2009 to 2025, a16z led 31 early-stage funding rounds that eventually grew into $5 billion companies, 50% more than its two closest competitors.

It possesses a comprehensive economic model. And now, it boasts a distinguished track record.

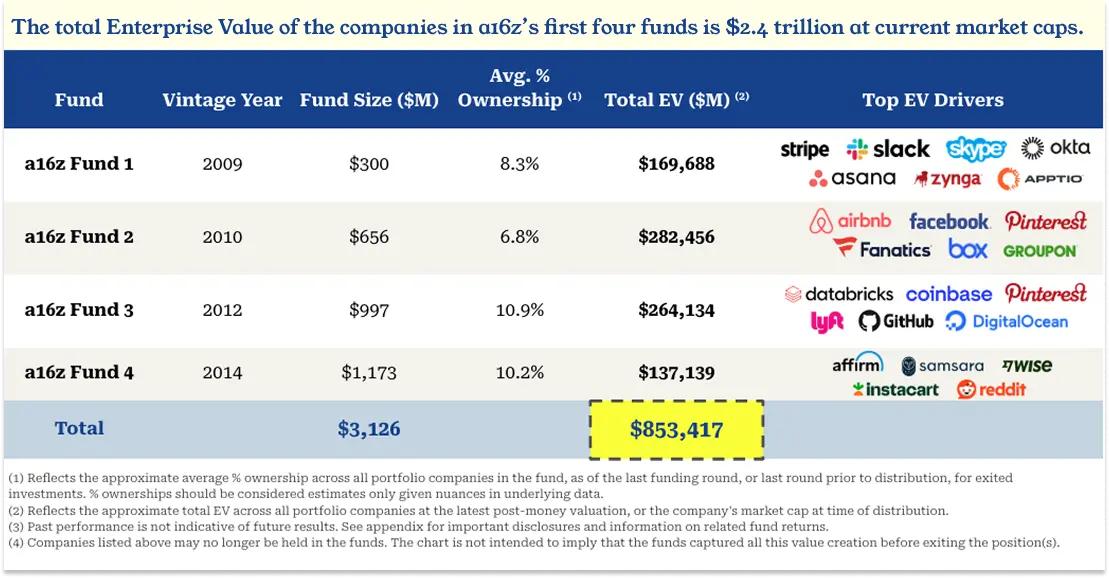

The chart below shows the total portfolio value of the first four funds, which is the threshold that the competing venture capitalist mentioned—$240-480 billion—needs to cross. Combined, the total enterprise value of a16z funds 1-4 at the time of allocation or at the latest post-investment valuation is... $853 billion .

And this is only the value at the time of distribution. Facebook alone has since added more than $1.5 trillion to its market capitalization!

This pattern repeats itself: a16z made a crazy bet on the future. Some "experts" said it was foolish. Wait a few years. It turned out it wasn't foolish at all!

Following the 2009 global financial crisis, a16z raised $300 million in its first Fund I, touting its platform to support founders' operations. "We visited a lot of VC friends, and many of them said it was a really stupid idea, that we should absolutely not do it, that people had tried it before but failed," recalls Ben Horowitz (co-founder of a16z). Today, almost every major VC firm has some form of platform team.

In 2009, when it used $65 million of its fund to acquire Skype from eBay for $2.7 billion alongside Silver Lake and other investors, "everyone said it was an impossible deal because of the intellectual property risks." Ben recounted the skepticism at the time in a blog post less than two years after Microsoft 's $8.5 billion acquisition of Skype.

In September 2010, Marc and Ben raised $650 million in Fund II and began making large-scale late-stage investments in companies such as Facebook (investing $50 million at a $34 billion valuation), Groupon (the pioneer of group buying, investing $40 million at a $5 billion valuation), and Twitter (investing $48 million at a $4 billion valuation), betting on the opening of the IPO window. The Wall Street Journal, in a classic article titled "Venture Capital Novice Shocks Silicon Valley," reported that competitors were furious, arguing that private equity deals were simply not what venture capitalists were supposed to do. Matt Cohler (a partner at Benchmark and former Facebook executive) famously said, "You can make money on pork and oil futures, but that's not what we do."

In November 2011, Groupon went public with an opening market capitalization of $17.8 billion. In May 2012, Facebook went public with a market capitalization of $104 billion. In November 2013, Twitter went public with a closing market capitalization of $31 billion on its first day of trading.

When Marc and Ben raised $1 billion in Fund III and a $540 million parallel opportunity fund in January 2012, criticism turned to a familiar topic: size. a16z's funds accounted for 7.5% of all VC funding raised in the U.S. in 2012, a time when the VC industry was performing poorly. Legendary venture capitalist Bill Draper said, "The growing consensus in Silicon Valley about venture capital is that too much money is chasing too few top-tier companies." That certainly sounds relevant today.

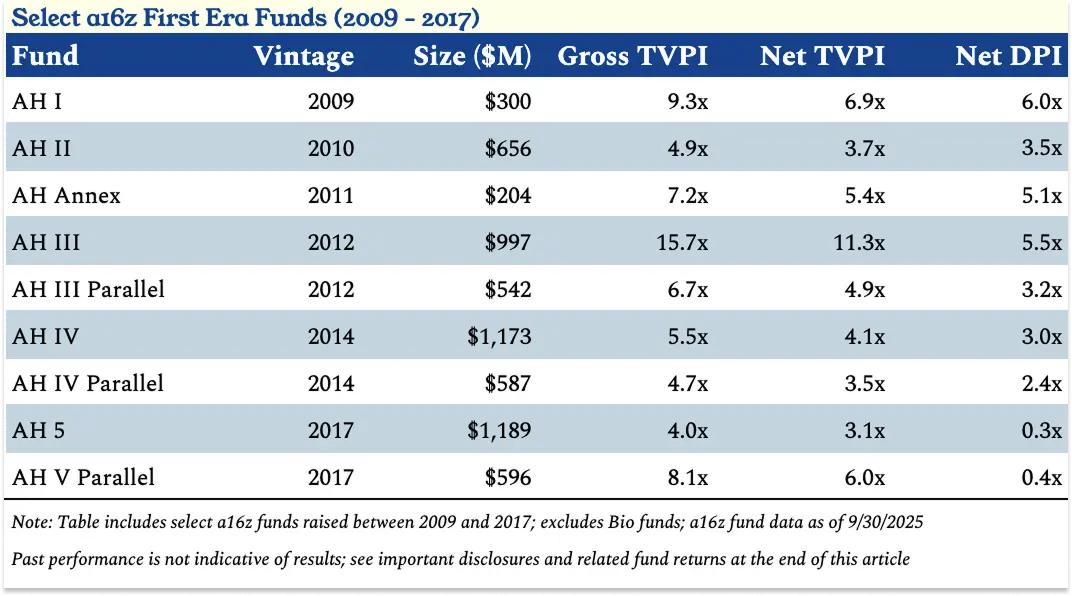

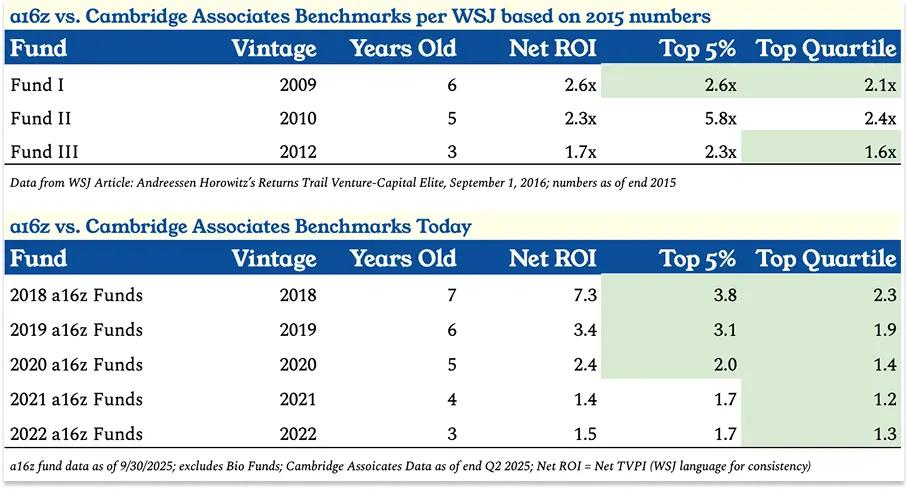

In 2016, The Wall Street Journal published an article that David Rosenthal (host of the Acquired podcast) called "clearly a smear campaign by competitors," titled "a16z's Returns Lag Behind the Venture Capital Elite." At the time, a16z's funds were seven, six, and four years old, respectively. The article showed that while AH Fund I was in the top 5% of VC funds, AH II was only in the top 25%, and AH III was actually slightly outside the top 25%.

In hindsight, this is quite interesting, because that fund, AH III, was a monster fund : as of September 30, 2025, its net TVPI (total return multiple) was 11.3 times, and if parallel funds are included, it was 9.1 times net TVPI.

AH III's portfolio includes Coinbase (which has generated $7 billion in total dividends for a16z LPs across its various participating funds), Databricks , Pinterest , GitHub , and Lyft (though not Uber , which powerfully demonstrates that missing out is better than making a mistake), making it one of the best-performing large venture funds ever. Since Q3 2025, Databricks (currently a16z's largest holding) has raised capital at a valuation of $134 billion, meaning Fund III's performance is now even stronger. a16z has already net paid out $7 billion in dividends to LPs from AH III and its parallel funds, and still has almost the same amount of unrealized value on its books.

Most of the unrealized value is in one company, Databricks: a massive big data company that was very small when the Wall Street Journal was pessimistic about a16z in 2016, months away from reaching a valuation of $500 million. Today, Databricks accounts for 23% of a16z's total net asset value (NAV).

If you spend any time at a16z, you'll hear the name Databricks frequently. Besides being its largest holding (which is certainly one of the top three largest holdings in the entire venture capital world), its story is also the clearest example of how a16z operates at its best.

The formula for success of Databricks and a16z

Before we begin talking about Databricks, it will be helpful to understand some of the company's characteristics that we haven't discussed yet.

First, a16z was founded and run by engineers. Not just founders, but engineers as founders. This influenced how they designed the company (to win through scale and network effects) and how they selected markets and companies within them.

Secondly, at a16z, perhaps there's no greater investment sin than investing in the "second-place" winner. If you miss out on a winner early on, you can always invest in later rounds. But if you invest in the second-place winner, you shut yourself out of the winner's door. This is true even before the ultimate winner emerges.

Third, once a16z is convinced it has found the winner in the category, classic a16z practice is to give it more money than it thinks it needs. Everyone laughs at them for this.

These three things have been true since the company was founded.

Back in the early 2010s, just a few years after a16z was founded, big data was a hot topic (you should remember this), and the dominant big data framework of that era was Hadoop. Hadoop used a programming model called MapReduce (originally developed by Google) to distribute computation across clusters of inexpensive commercial servers instead of expensive dedicated hardware. It "popularized big data," and a plethora of companies sprang up to promote and capitalize on this popularity. Cloudera, founded in 2008, raised $900 million in 2014, and that year investment in Hadoop companies quintupled to $1.28 billion. Hortonworks, spun off from Yahoo, went public that same year.

Big data, big dollars. But a16z didn't make any money from it.

Ben Horowitz, the "z" in a16z, dislikes Hadoop. A computer science student before becoming CEO of LoudCloud/OpsWare, Ben doesn't believe Hadoop will be the winning architecture. Its programming and management are extremely difficult, and Ben believes it's unsuitable for the future: each step of the MapReduce computation writes intermediate results to disk, making it incredibly slow for iterative workloads like machine learning.

So Ben avoided the Hadoop craze . Jen Kha told me that Marc at the time:

"He was absolutely furious, because at that moment, Hadoop was making all the headlines, and he said, 'We're going to miss this. We've completely messed up. We've dropped the ball.'"

Ben said, 'I don't think this is the next architectural shift.'

Then finally, when Databricks came along, Ben said, 'This might be it.' And of course, he bet everything he had on it.

Databricks came at just the right time, and it's located right on the road near UC Berkeley.

Ali Ghodsi and his family fled Iran during the 1984 Iranian Revolution and moved to Sweden. His parents bought him a Commodore 64 computer, which he used to teach himself programming. He actually became very good at it, so much so that he was invited to be a visiting scholar at the University of California, Berkeley.

At Berkeley, Ali joined AMPLab, where he was one of eight researchers (including dissertation advisors Scott Shenker and Ion Stoica) working to realize ideas from doctoral student Matei Zaharia's dissertation and to build Spark, an open-source software engine for big data processing.

The idea was to "replicate what large tech companies do with neural networks, but without the need for complex interfaces." Spark set a world record for data sorting speed, and the paper won the Best Computer Science Paper of the Year award. Following academic tradition, they released the code for free, but almost no one uses it.

So, starting in 2012, these eight people got together for a series of dinners, during which they decided to form a team to start a company on top of Spark. They called it Databricks. Seven of the eight joined as co-founders, and Shenker signed on as an advisor.

Databricks co-founder Ali Ghodsi sat in the middle of the front row.

Databricks co-founder Ali Ghodsi sat in the middle of the front row.

The team believed that Databricks needed a little money. Not much, just a little. As Ben explained to Lenny Rachitsky:

“When I met them, they said, ‘We need to raise $200,000.’ I knew at the time they had this thing called Spark, and the competitor was something called Hadoop. Hadoop already had very well-funded companies running towards it, while Spark was open source, so time was of the essence.”

He also realized that, as academics, the team tended to do things on a smaller scale. “Typically, professors… if you start a company and make $50 million, that’s a pretty big win. Like, you’re a hero on campus,” he told Lenny.

Ben brought bad news to the team: "I'm not going to write you a check for $200,000."

But he also brought very good news to the team: "I'm going to write you a check for $10 million."

His reasoning was, “You need to build a company. If you’re going to do that, you need to go all in. Otherwise, you should stay in school.”

They decided to drop out of school. Ben increased the amount of the check, and a16z led Databricks' Series A funding round, valuing the company at $44 million post-money. It owns 24.9% of the company.

This initial encounter—Databricks asking for $200,000, and a16z offering much more—set a pattern. When a16z invests in you, they believe in you.

When I asked about the impact of a16z, Ali was unequivocal: “I don’t think Databricks would exist today without a16z. Especially Ben. I don’t think we would exist. They genuinely believed in us.”

In its third year, the company's revenue was only $1.5 million. "At that time, it was far from certain whether we would succeed," Ali recalled. "The only person who truly believed it would be very valuable was Ben Horowitz. Much more than we were. Note that he believed it much more than I did. This is all thanks to him."

Faith is a cool thing. It becomes even more valuable when you have the power to make it self-fulfilling.

Just like in 2016, when Ali was trying to reach an agreement with Microsoft. From his perspective, this was obvious given the huge demand for using Databricks on Azure. He asked some of his VCs to introduce him to Microsoft CEO Satya Nadella, and they did, but those introductions "got buried in the loop of executive assistants."

Then Ben formally introduced Ali to Satya. “I received an email from Satya saying, ‘We’re absolutely interested in building a very deep partnership,’” Ali recalled, “and copied his deputy, and his deputy’s deputy. Within hours, I had 20 emails in my inbox from Microsoft employees I’d tried to talk to before, all saying, ‘Hey, when can we meet?’ It was like, ‘Okay, this is different. This is going to happen.’”

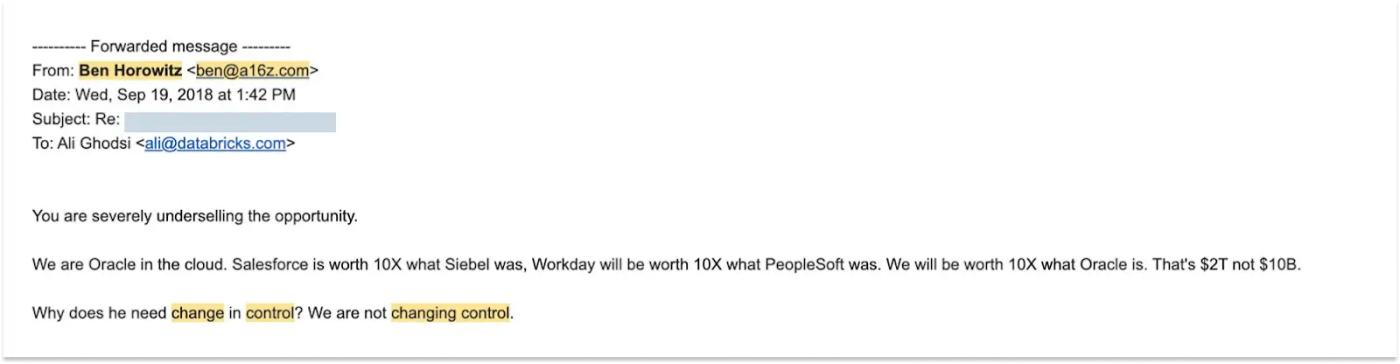

Or, in 2017, when Ali was trying to hire a senior sales executive to keep the company's growth momentum going, this executive wanted to include change of control provisions in his contract—basically, options that would vest faster if the company were acquired.

This was a stalemate, so Ali asked Ben to help persuade the man that Databricks was worth "at least $10 billion." After speaking with him, Ben sent Ali this email:

An email from Ben Horowitz to Ali Ghodsi, September 19, 2018

An email from Ben Horowitz to Ali Ghodsi, September 19, 2018

"You have seriously underestimated this opportunity."

We are the Oracle of the cloud. Salesforce is worth 10 times Siebel. Workday is worth 10 times PeopleSoft. We are worth 10 times Oracle. That's $2 trillion, not $10 billion.

Why does he need a change of control clause? We either don't change control at all.

This is one of the most hardcore corporate emails ever, especially considering that Databricks was valued at only $1 billion and had annual revenue of only $100 million at the time, while it is now valued at $134 billion and has annual revenue of over $4.8 billion.

“They envision the full potential of things,” Ali told me. “When you’re like us, mired in the mire of operations every day, seeing all the challenges—deals not going through, competitors beating you, money running out, nobody knowing who you are, people leaving you—it’s hard to think about the world that way. But then they come to the board meeting and tell you, ‘You’re going to take over the world.’”

They were right, and their faith paid off. In summary, a16z invested in all twelve of Databricks' funding rounds. It led four of them. This company is one of the reasons why AH3 Fund (the fund that made the initial investments) performed so well, and also a driver of returns for its larger later-stage venture capital funds 1, 2, and 4.

“First and foremost, they genuinely care about the company’s mission. I don’t think Ben and Marc see it primarily as a return on investment. That’s secondary,” Ali observed. “They are tech believers who want to change the world with technology.”

If you don't understand Ali's comments about Marc and Ben, you won't understand a16z.

What is a16z?

a16z is not a traditional venture capital fund. On the surface, that's obvious! It just completed its largest VC fundraising of all its strategies since SoftBank's $98 billion Vision Fund in 2017 and Vision Fund II in 2019.[8] This is anything but traditional. But even the SoftBank Vision Fund is a fund. a16z is not that.

Of course, a16z raised capital and needs to generate returns. It had to excel in that regard, and so far, it has been outstanding. Not Boring has a16z's fund return data to date, which we will share below.

But first—what is a16z?

a16z is a tech enthusiast. Everything it does is aimed at bringing better technology and making the future better. It believes that "technology is the glory of human ambition and achievement, the vanguard of progress, and the realization of our potential." Everything stems from this belief. It believes in the future and stakes the entire company on it.

a16z is a company. It's a business, an enterprise. It was built to scale and improve as it scales. I think there are many characteristics of a company that don't apply to traditional funds, and we'll cover those. I think this distinction addresses one of the strangest things about the venture capital self-image: that venture capital is an industry that sells the world's most scalable product (money) to the most scalable companies (tech startups), but it itself cannot scale.

This distinction—company > fund—comes from a16z GP David Haber, the most East Coast-financial-minded person in the group, who describes himself as a student of investment firms as businesses. “The objective function of a fund is to generate the most carried equity with the fewest people in the shortest possible time,” he explains. “A company is about delivering superior returns and building a source of competitive advantage through compounding. How do we get stronger as we grow, rather than weaker?”

a16z is run by engineers and entrepreneurs. While stereotypical fund managers try to grab a larger share of a fixed pie, engineers and entrepreneurs try to make the pie bigger by building and scaling better systems.

a16z is a sovereign in time. It's an institution built for the future. In its more ambitious moments, the company positioned itself as a peer of the world's leading financial institutions and governments. It once stated its goal was to become the (original) JPMorgan Chase of the information age, but I think that underestimates its true ambitions. If governments represent blocks in space, then a16z represents that vast block of time known as the future. Venture capital is simply the way it has discovered that can have the greatest impact on the future and the business model that best aligns with its profit objectives.

a16z creates and sells power. It builds its power through scale, culture, networks, organizational infrastructure, and success, and then empowers the tech startups in its portfolio primarily through sales, marketing, hiring, and government relations, though this seems to encompass much, according to its founders.

If you were to design an organization that believes technology is “devouring a market far larger than anything the tech industry has ever pursued,” an organization that believes everything is technology, you would build a company that sells the power to win to hundreds or thousands of companies that may one day become economic entities. I think you would build an organization that looks a lot like a16z.

Because companies that may one day become economic players start small and vulnerable. They start fragmented, each with its own goals and competitors; often, they compete with each other. And they face entities that dominate the market and are unwilling to concede to new entrants. A small company, however promising, may not be able to hire the best recruiters to bring in the best engineers and executives. It may not be able to advocate for policies that give it a fair chance. It may not have an audience to deliver its message to the world in a way that people are willing to listen to. It may not have the legitimacy to sell its products to governments and large corporations inundated with promises of the next big thing.

For any small company, investing billions of dollars to build those capabilities and then amortizing it all over itself makes no sense. But if you can amortize those capabilities across all those companies, across trillions of dollars in future market value, then suddenly, small companies can have the resources of large companies. They can decide the outcome based on the quality of their products. They can deliver the future they deserve.

What if you could combine the agility and innovation of a startup with the power and weight of a time sovereign?

This is what a16z is trying to do, and what it has been trying to do since it was a startup.

Why did Marc and Ben found a16z?

In June 2007, Marc wrote a blog post titled "The Only Thing That Matters," as part of Pmarca's guide to startups. Ostensibly advice for tech startups, it reads more like a manual for founding a16z. It answered the question: Which of the three core elements of a startup—team, product, or market—is most important?

Entrepreneurs and venture capitalists talk about their teams. Engineers talk about their products.

“Personally, I hold a third position,” Marc wrote. “I assert that the market is the most important factor in the success or failure of a startup.”

Why? He wrote:

In a great market—a market with a large number of real potential customers—the market will pull products out of startups…

Conversely, in a bad market, you can have the best product in the world and an absolutely killer team, but it doesn't matter—you will fail…

In tribute to Andy Rachleff, a former Benchmark Capital employee who crystallized this formula for me, I developed Rachleff's Law of Startup Success:

The number one killer of companies is a lack of market presence.

This is what Andy said:

When a great team encounters a bad market, the market wins.

When a bad team encounters a great market, the market wins.

When a great team meets a great market, something special happens.

I think what Marc and Ben saw in venture capital was a great market (nobody realized how great it was) full of terrible teams (nobody realized how terrible they were).

Between 2007 and 2009, Ben and Marc were figuring out what to do next. They were very successful tech entrepreneurs, but despite their success, they were dissatisfied, and because of their success, they had the kind of "fuck you money" attitude they could have.

But how?

As entrepreneurs and then as angel investors, Marc and Ben have dealt with many terrible venture capitalists, and they think it might be interesting to compete with these people.

“For Marc, it’s not about money, at least not from my perspective,” David Haber told me. “He’s been rich since he was 20. In the beginning, it was probably more about punching Benchmark or Sequoia in the face.”

Venture capital has another advantage, something very few people realized during the deep recession triggered by the global financial crisis: it may be the greatest market on earth. This is extremely important to Marc.

Of course, not all venture capital is bad. The two companies Marc wanted to criticize—Sequoia and Benchmark—were excellent (Marc quotes Andy Rachleff!), except they tended to oust founders. For founders who wanted to stay in control, Peter Thiel launched Founders Fund in 2005 and was deploying FF II in 2007, which, as Mario writes, later returned $18.60 in real money (DPI) for every $1 invested.

But compared to today, it was, overall, a lazy, small-circle, workshop-style industry.

Marc likes to tell a story about a meeting he had in 2009 with the GP of a top firm when he and Ben were considering launching a16z. The GP likened investing in startups to grabbing sushi from a conveyor belt. According to Marc, this GP told him:

Venture capital is like going to a conveyor belt sushi restaurant. You just sit on the dune road and startups come in; if you miss one, no problem, because another sushi boat is right behind you. You just sit and watch the sushi go by, occasionally reaching out to grab a piece.

If the goal is to maintain the current good situation, "as long as the industry's ambitions are limited," Marc explained to Jack Altman on Uncapped.

But Marc and Ben's ambitions knew no bounds. In their company, there was no greater sin than "missing out" on a great company. This was crucial because they saw that as the market grew, large tech companies would only get bigger.

“Ten years ago, there were only about 50 million consumers on the internet, and relatively few people had broadband connections,” Ben and Marc wrote in their fundraising prospectus for Andreessen Horowitz Fund I in April 2009. “Today, there are approximately 1.5 billion people online, many of whom have broadband connections. Therefore, the biggest winners on both the consumer and infrastructure sides of the industry are likely to be much larger than the most successful tech companies of the previous generation.”

At the same time, the cost and difficulty of starting a company have been greatly reduced, which means there will be more companies.

“Over the past decade, the cost of creating a new technology product and getting it to market, at least in the testing phase, has dropped dramatically,” they wrote in a letter to potential LPs. “It now typically costs between $500,000 and $1.5 million, compared to $5 million to $15 million a decade ago.”

Finally, the companies' ambitions have grown as they have shifted from tool companies to competing directly with existing businesses, meaning that every industry will become a technology industry, and every industry will become bigger as a result.

That's why the market was so great back then. He went on to say:

From the 1960s to, say, 2010, there was a venture capital script… the companies were basically tool companies, right? Pickaxes and shovels. Mainframes, desktop computers, smartphones, laptops, internet access software, SaaS, databases, routers, switches, disk drives, word processors—tools.

Around 2010, the industry underwent a permanent change... The big winners in the tech world are increasingly companies that directly enter existing industries.

Did a16z pay too high a price for the company in its early stages? Or did it pay a good price relative to its perceived future value?

In hindsight, it would have been easy to claim the latter. What's impressive about a16z is that they said the same thing beforehand.

As they wrote, if about 15 tech companies that eventually reach $100 million in annual revenue each year generate about 97% of the publicly traded market capitalization of all companies founded that year—which is now known as the power law—then they should invest in as many of those 15 promising companies as possible at all costs, and then be in a position to double or triple their bets on the winners.

To do this, relying solely on two investment partners, a16z had to think about how to build a company in a way that was different from anyone else's.

Therefore, after sharing the basic terms of the AHI investment—a target fund size of $250 million, of which the general partner will commit $15 million—Ben and Marc summarized their company strategy in one sentence.

AH Fund I Prospectus

This is the strategy they are still implementing today, even though the company has grown to a size far exceeding the ambitions of two partners and the top five.

The Three Eras of a16z

Since its first fund, throughout the company's history, a16z's overly strong belief in the future, its asymmetric belief, has, in my view, been its core competitive advantage. This is the differentiator from which all other advantages derive.

As a company's ambitions, resources, fund size, and power grow, how it leverages this advantage and chooses how to differentiate itself also evolves over time.

First Era (2009-2017)

In the first era of a16z (2009-2017), the core insight was: if software is eating the world, then the best software companies will become far more valuable than anyone else is currently pricing them.

This belief enabled a16z to do three things that transformed it from a new entrant into a top 5 company:

Paying high prices for deals. As mentioned earlier, a16z's early-stage fund deals were considered by many to be too expensive or unorthodox at the time. "The usual criticism is that they paid a premium to buy fame for themselves, to buy winners," Ben Gilbert said on the Acquired podcast, but he argued that it was rational at the time, noting, "Would anyone argue today that anything they did between 2009 and 2015 was actually overvalued? Absolutely not." As Ben Horowitz explained in the 2014 HBS case study, "Even with valuations in the billions, investors may underestimate a company's potential." That underestimation was a16z's advantage.

Building what others would call wasteful operational infrastructure: hiring a full-service team, recruiting partners, an executive briefing center… all of this seemed like a fund manager’s expense at the time. But if you believe a portfolio company can become a category-defining firm and requires corporate strength to get there, then this expenditure is justified. They were building for a future where a startup needs to look like a real company to win Fortune 500 deals.

They viewed tech founders as a scarce resource. It was also a gamble, as companies became increasingly cheap and easy to build, and tech geniuses without traditional management skills could and would build even more significant companies. Therefore, they went to great lengths to win them over and support them, introducing the CAA (Creative Artist Agency) model to venture capital. "Founder-friendly" is a meme now, but it was truly novel at the time.

The key point is that in this first era, the most important thing is simply to invest in the right companies and profit as they become as successful as a16z believes. Of course, they focus on helping founders, but primarily, they are taking advantage of available arbitrage opportunities.

AH III, which has Coinbase and Databricks, is a prominent example, but its consistency is also noteworthy.

“As LPs, we’re pleased with a fund that consistently delivers net 3x TVPI, and occasionally a fund that delivers net 5x+ TVPI, and that’s what they deliver,” VenCap CIO David Clark told me, an LP who has been investing in a16z since AH3. “a16z is one of the few companies that can deliver this kind of performance on a large scale over a sustained period.” You can see that in the performance figures above.

If this is an era where a16z is willing to pay a high price and "invest in pig's belly" in order to gain fame and reap rewards in the future, then such a deal does not seem to cost much in the short term.

Second Generation (2018-2024)

In the second era of a16z (2018-2024), the key belief is that the winners have indeed become much larger than anyone expected, they have remained private for longer, and technology is devouring more industries than anyone else realizes.

I believe this belief enabled a16z to do three things, thus transforming it from a top 5 company into a leader:

To raise a larger fund.

In its first phase, a16z raised $6.2 billion through nine funds. In its second phase, over five years, a16z raised $32.9 billion through 19 funds. Standard VC wisdom dictates that returns decrease as fund size increases. a16z counters this: if the biggest winners become increasingly large, you need more capital to maintain meaningful ownership through multiple rounds of funding. The worst thing you can do is miss out on the winners and not own enough of the winners you already own. Marc likes to say that you can only lose a maximum of 1x, but your ceiling is practically unlimited.

Establish a structure that goes beyond a single fund.

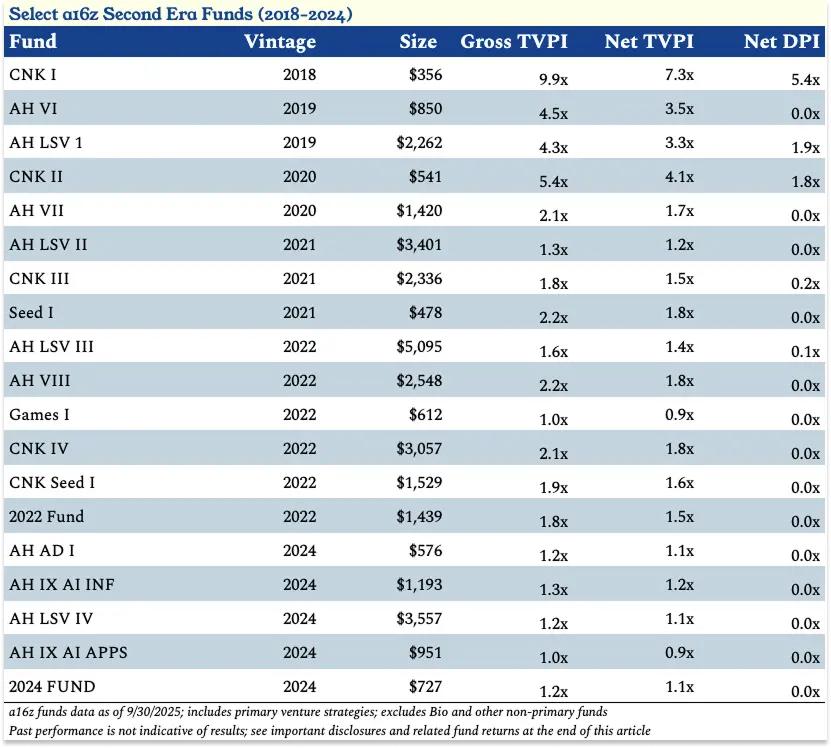

In its first phase, a16z raised its core fund and subsequent late-stage funds. All a16z GPs invested from the same funds, even though they each had their own areas of focus. It also raised a bio fund, as bio is a completely different beast. For the purposes of this article, I'll focus on a16z venture funds that don't focus on bio and health. In its second phase, a16z began to decentralize. In 2018, it launched CNK I, a16z's first dedicated crypto fund led by Chris Dixon. In 2019, it recruited David George to lead a dedicated late-stage venture capital (LSV) fund and raised its largest fund to date: LSV I, approximately $2.26 billion, roughly twice the size of any previous a16z fund. During this period, it raised new funds across core, crypto, bio, and LSV, as well as a dedicated seed fund ($478 million AH Seed I in 2021), a dedicated games fund ($612 million Games I), and its first cross-strategy fund ($1.4 billion 2022 Fund), which allowed LPs to invest proportionally in all funds for that year. Importantly, while individual funds can leverage the company’s centralized resources, such as investor relations, each fund has designed its own dedicated platform team—marketing, operations, finance, events, policy, and more—to meet the specific needs of founders in its vertical.

Hold positions for a longer period of time.

In a16z's second era, leading companies began to remain private for longer periods and raise more capital in the private market, both in the primary market (to fund the company) and the secondary market (to provide liquidity for employees and early investors). Matt Cohler's analogy of a16z's purchase of late-stage secondary stock in Facebook as buying a pig's belly became standard practice, as companies like Stripe, SpaceX, WeWork, and Uber gained access to liquidity in the private market that was previously only available in the public market. This presented a challenge for the industry—LPs couldn't easily access liquidity, hindering capital allocation cycles—but for companies that believed tech companies would grow larger, it was a godsend. It provided an opportunity to invest more capital in high-quality companies that happened to be private and to pull returns that would have belonged to public market investors into the private market. I believe this shift is one of the key reasons why VC firms like a16z have been able to grow larger without crushing returns.

In response, a16z did several things. It became a Registered Investment Advisor (RIA), allowing it to freely invest in cryptocurrencies, public stocks, and secondary markets, and launched LSV 1, the aforementioned fund led by David George. In its second phase, LSV raised $14.3 billion out of a16z's total $32.9 billion across all its funds. The crypto fund in its fourth phase (Fund IV) was also split into a seed phase ($1.5 billion) and a later phase ($3 billion).

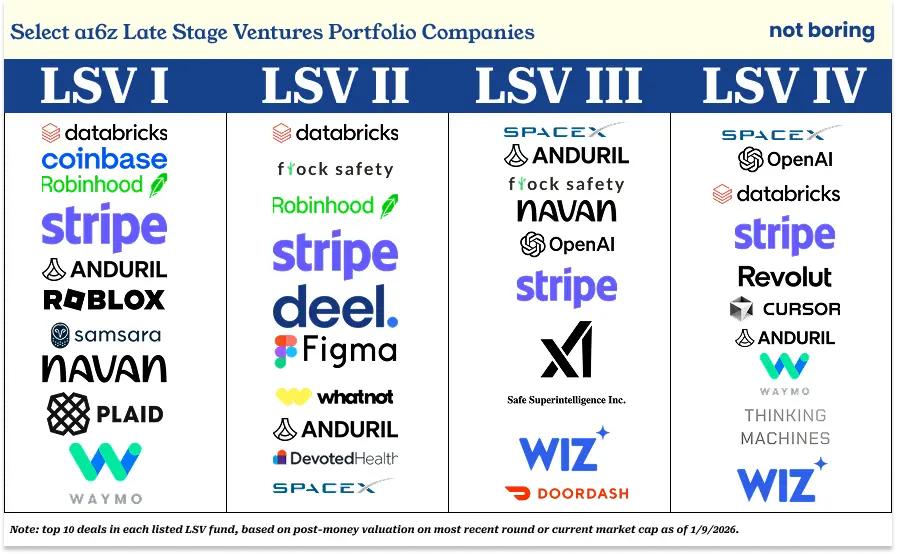

These are the top 10 deals for each listed LSV fund, based on the most recent post-money valuation or current market capitalization:

LSV I: Coinbase, Roblox, Robinhood, Anduril, Databricks, Navan, Plaid, Stripe, Waymo, and Samsara

LSV II: Databricks, Flock Safety, Robinhood (they exited the public market and are now investing in more Databricks), Stripe, Deel, Figma, WhatNot, Anduril, Devoted Health, and SpaceX.

LSV III: SpaceX, Anduril, Flock Safety, Navan, OpenAI, Stripe, xAI, Safe Superintelligence, Wiz, and DoorDash

LSV IV: SpaceX, Databricks, OpenAI, Stripe, Revolut, Cursor, Anduril, Waymo, Thinking Machine Labs, and Wiz

As a16z has been criticized in the past, if you're going to buy Logo, you'll almost certainly get something worse. That said, according to Cambridge Associates data as of Q2 2025, LSV I is in the top 5% of its year, while LSV II and LSV III are both in their respective top quartiles (top 25%).

As of September 30, 2025, LSV I has a net TVPI of 3.3x, LSV II has a net TVPI of 1.2x (although it could be higher after the recent funding rounds for Databricks and SpaceX), and LSV III has a net TVPI of 1.4x (which could also be higher, up >2x, after SpaceX completes its major secondary sale at a reported $800 billion valuation).

By believing that the results of these star companies will be much greater than most people (not all, of course; see: Founders Fund and SpaceX, Thrive and Stripe) believe, a16z is able to invest more in the best privately held tech companies.

Crucially, they have begun to demonstrate that, under the right conditions, it is possible to achieve venture-like returns in growth funds. Specifically, based on analysis I saw from an a16z LP, companies with strong early-stage businesses can offer venture-like multiples (and higher internal rates of return, IRR) by continuing to invest in growth-stage funds. Of course, deeper relationships with these companies can also increase their power.

In the second phase, a16z believes the most important thing is to own as many winners as possible. This is easier if you understand these companies better from the early stages of investment and have dedicated later-stage funds to continue doubling down or correcting early mistakes. (Although it's still not as much of a majority equity investment as you'd see in other asset classes.)

This is also a form of arbitrage, although I believe a16z has done more to help its individual companies succeed in this era.

The returns of the second generation are still in their early stages, but they are ahead of the performance of the first generation funds at similar stages of their life cycle, when the Wall Street Journal reported on their poor performance.

The net TVPI of funds was 7.3 times in 2018, 3.4 times in 2019, 2.4 times in 2020, 1.4 times in 2021, and 1.5 times in 2022.

Of particular note in this era is the outstanding performance of the crypto funds (CNK 1-4 and CNK Seed 1). CNK 1 has returned 5.4x net DPI to its LPs.

Perhaps more surprising to those who think a16z crypto raised too much money at the wrong time in 2022 is that the $3 billion it raised for CNK IV reflects (or “book value”) a net TVPI of 1.8 times to date.

The two biggest stories of this second era, LSV and crypto, illustrate two aspects of a16z's belief in the future. LSV is a response to the fact that companies are staying private for longer and have a greater need for private market capital. Crypto represents the idea that innovation (and returns) can come from entirely new areas that are completely different from the areas you are used to investing in.

These also illustrate that a16z needs to expand what it does on behalf of its portfolio companies and industries. To help its later-stage companies thrive, it must rebuild some of the advantages of being publicly listed in the private market.

To ensure the survival of encryption in the United States and to ensure that all types of new technology companies have a fair chance in the fight against vested interests, it needs to go to Washington.

This brings us to a16z’s third era (2024-Future), in which the key belief is that new technology companies, if allowed, will not only reshape but also win every industry, and a16z must lead industries and countries in the right direction.

This belief has once again altered the nature of a16z. At a certain scale, $15 billion in new funding is a good dividing line; simply picking winners is not enough.

You must create winners by shaping the environment in which they compete.

As Ben put it, "It's time to take the lead."

a16z's era of leadership

You might imagine that at this stage of the game, an analyst from a rival VC firm would text journalist Tad Friend something like, "To achieve a 5-10x total return on your new $15 billion fund, 'you need to make the entire U.S. tech industry several times larger than it is today.'"

To this, you can imagine Marc and Ben saying: Yes.

This is the company's clearly stated plan. The logic is as follows.

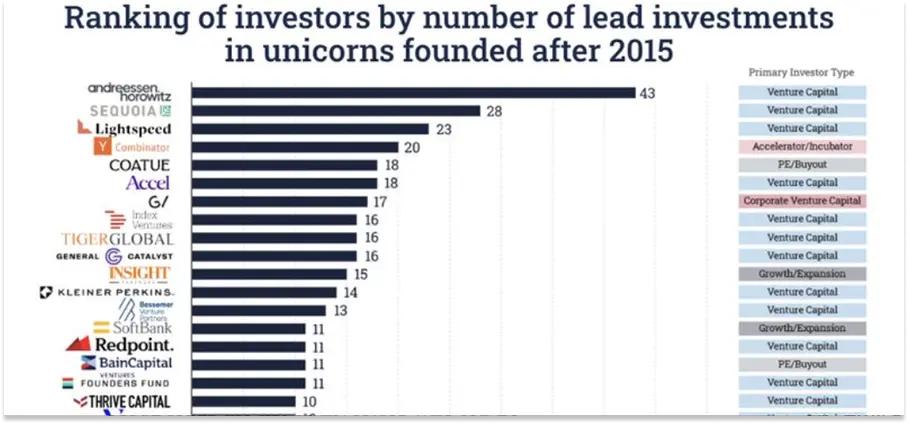

Since 2015, it has funded more unicorns in their early stages than any other investor, and the gap between a16z and the second-place (Sequoia) is as large as the gap between the second and twelfth place.

Source: Ilya Strebulaev, Stanford Professor

"The number of companies that became unicorns after receiving early-stage funding" is certainly a very specific and convenient way to judge "best." More commonly, returns are cited, in multiples or IRR, or simply the total amount of cash allocated to LPs. Others might point to hit rate or consistency. There are many ways to segment the rankings.

But this approach seems to align with a16z's view of the world. As I heard repeatedly during my time at a16z crypto, it's perfectly fine for many smart entrepreneurs to bet on a category and make a mistake because so many are building there. But it's unacceptable to pick the wrong company within a category and miss out on the ultimate winner for any reason. As Ben said:

We know that starting a company is a high-risk endeavor, so if we run the right processes and properly assess the risks when making this investment, we are not worried about investments that don't succeed. On the other hand, we are very concerned about whether we have misjudged whether the entrepreneur is the best in her category.

If we choose the wrong emerging category, that's fine. If we choose the wrong entrepreneur, that's a big problem. If we miss the right entrepreneur, that's also a big problem. Missing out on a groundbreaking company due to conflict or abandonment is far worse than investing in the best entrepreneur in a category we misjudged.

Based on its own assessment of what matters most, a16z has become a leader in the venture capital industry.

“And now?” Ben asked. “What does it mean to lead an industry?”

In the X article announcing the $15 billion funding round, he replied, "As a leader in American venture capital, the fate of America's new technologies rests partly on our shoulders. Our mission is to ensure that America wins the technology race for the next 100 years."

This is an extraordinary thing for a venture capital firm.

This is also why, if you accept the premise that technology is the engine of progress, that America’s continued leadership depends on technological superiority, and that A16Z is America’s largest and most influential backer of new technology companies, possessing the power and resources to empower them to compete fairly with existing businesses, it’s not entirely unreasonable.

To win the technology of the next 100 years (which, in a16z, is the same thing as winning the next 100 years), he went on to say, it must win the key new architectures—AI and cryptography—and then apply those technologies to the most important areas, such as biotechnology, defense, health, public safety, and education, and inject them into government itself.

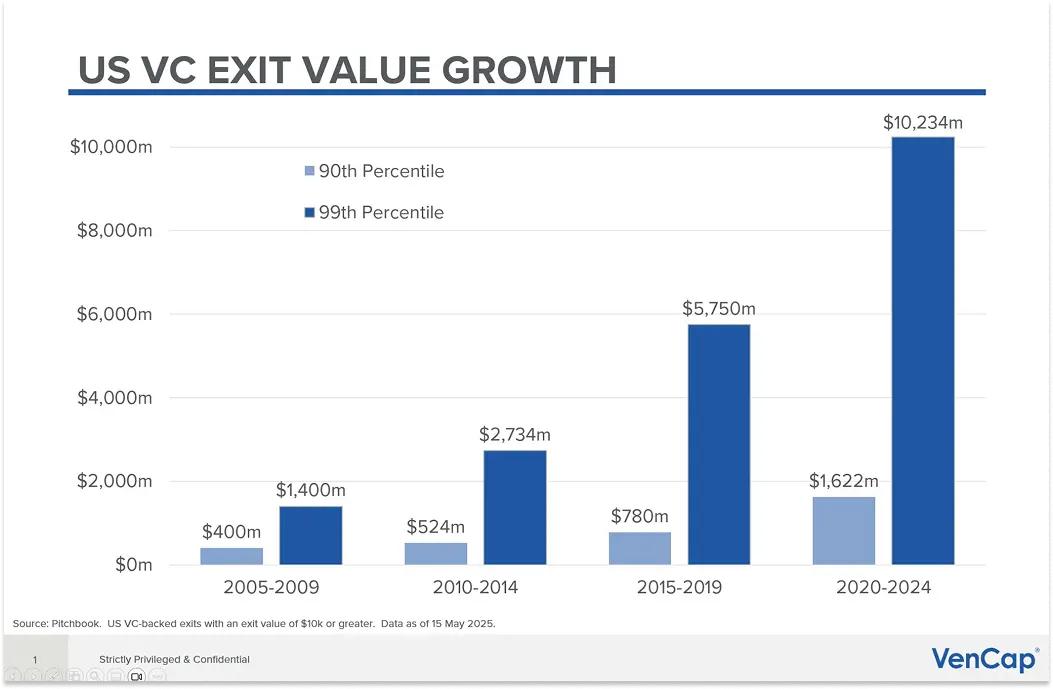

These technologies will make the market even bigger. As I argued in Tech is Going to Get Much Bigger and Everything is Technology, this means that industries and unfinished work that were not previously in the technology addressable market are now in it, which means that venture capital addressable value (VCAV) will also increase dramatically.

US VC exits are getting bigger, chart from David Clark of VenCap.

US VC exits are getting bigger, chart from David Clark of VenCap.

This is a continuation of the gamble a16z has been making, but with a significant shift in belief: if a16z does its job as a leader, this value will be unlocked, and the future of America (and the world) will be secured.

Specifically, this means five things:

Make America Great Again

Stepping into the gap between private and listed company construction

Bringing Marketing to the Future

Embrace new ways of building a company

While expanding our capabilities, we maintain a culture of building.

Almost everything about a16z that makes you scratch your head serves these five things.

Most notably, a16z has become more politically active over the past two years, with Marc and Ben publicly endorsing President Trump in the last election. This has angered many, with some arguing that venture capital funds should not influence national politics.

a16z would strongly oppose this argument. It wants to make American technology policy great again.

Marc and Ben articulated their arguments in The Little Tech Agenda, which can be summarized as follows:

New technology companies are crucial to our nation's success.

To win the future, we need laws, policies, and regulations that support innovation, and we must prevent regulatory capture by large, well-resourced existing companies.

The opposite has been happening all along: "We believe that bad government policies are now the number one threat to Little Tech companies."

No one fights for new technology companies in government halls or against existing businesses: large, established companies won't, and startups shouldn't waste their limited resources doing so.

Venture capital firms profit from the success of new technology companies, so VCs should be the ones fighting this battle, and as a leader in the VC industry, a16z has a responsibility to do so.

a16z is a single-issue voter. Small tech companies are its only concern. It is bipartisan.

These are the key points of the conversation—"We don't get involved in political battles outside of issues directly related to small tech companies," and "We support or oppose politicians regardless of political parties or their positions on other issues"—these are absolute truths based on everything I've seen on a16z.

The company isn't getting into politics for fun (although at least Marc seems to genuinely enjoy it; he seems to really enjoy a lot of things, finding humor in absurdity, which is an underrated competitive advantage, but we don't have time to discuss that today). a16z is willing to look foolish in the short term and take the hits to help the new technology thrive in the long term.

For a long time, as former Benchmark partner Bill Gurley argued in *2,581 Miles*, technology could essentially ignore Washington, and Washington could essentially ignore technology. A few years ago, this changed, partly because technology shifted from manufacturing tools to battling existing businesses, as I discussed earlier. Cryptography was the first sector to become critical in this regard.

When a16z first went to Washington, small tech companies weren't yet a voter base in the D.C. Large tech companies had their own lobbyists and connections. Existing businesses—banks, defense companies, whatever—had their own lobbyists and connections. But small tech companies, including crypto, didn't. No company, with the possible exception of Coinbase at the time, could afford the costs or infrastructure required to represent themselves in the nation's capital, let alone in state capitals across the country.

So in October 2022, a16z crypto hired Collin McCune as its head of government affairs, and Collin began educating American politicians about crypto. Collin, Chris Dixon, a16z crypto general counsel Miles Jennings, other team members, and the crypto founders, from the portfolio and the wider industry, traveled to Washington, D.C. multiple times to explain how crypto works, what it can become, and more generally, the dangers of stifling new technologies through regulation.

This worked. Thanks largely to their efforts, and the efforts of the industry's bipartisan Fairshake Super PAC, crypto is no longer facing an existential legislative risk. Last year, President Trump signed the GENIUS Act into law, the first regulation of crypto stablecoins, with comprehensive market structure legislation passing the House in an overwhelming bipartisan fashion. It is now under consideration in the Senate, with the hope of passing and being signed into law later this year.

This experience proved valuable as AI became a hot topic in Washington, D.C. McCune now leads the firm’s government affairs practice, with a permanent presence in the D.C., and work on AI, crypto, American Vitality, and more. It is currently advocating for comprehensive federal AI standards to avoid the chaos of competing state regulations, as well as other policies that support innovation.

While lobbying may be a dirty word, the reality is that competitors of small tech companies have sophisticated government affairs and policy teams dedicated to winning over regulators and preventing new entrants from competing on a level playing field.

To ensure technology wins the future and a16z reaps its funding rewards, staying out of politics is no longer an option. The good news is that, as a company that needs new companies to form, grow, and win to survive, a16z is incentivized as much as possible to keep the competitive environment open to innovation.

Because, as things stand at this moment, even a16z admits that it doesn't know which companies will be established in the future, or how they will be established.

Embracing new ways of building companies means being open to the idea that with AI, entrepreneurs may be able to build companies with one-tenth or one-hundredth of the staff they used to have, and the conditions required to build a great company may be drastically different from the past. This means that a16z also needs to adapt.

For example, it launched Speedrun, its own accelerator, through which it invests up to $1 million and runs 12-week programs for nascent companies. This allows a16z to gain early insights into how these new companies are built and the specifics of each company, enabling it to more intelligently invest more in the winners.

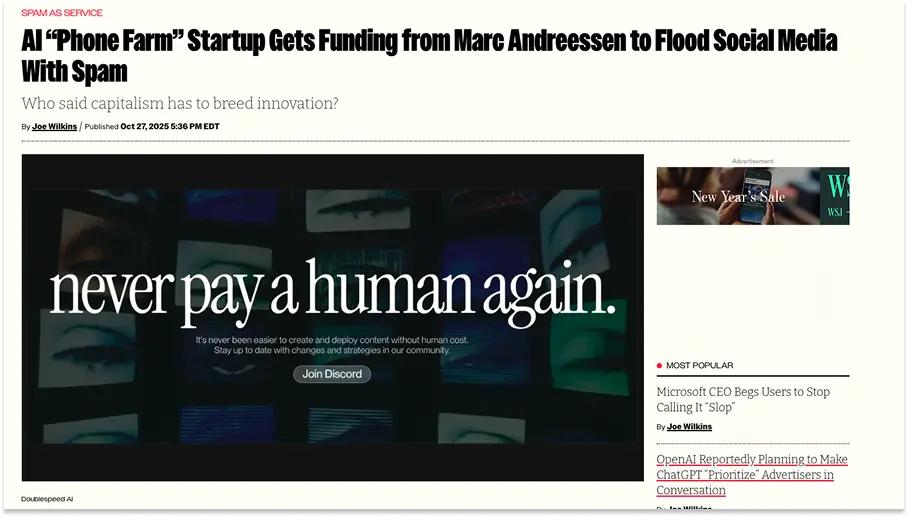

But this also carries risks: increasing the number of companies that can claim to be backed by a16z and lowering the barrier to entry risks diluting legitimacy. For example, a16z has been criticized on Twitter for backing Doublespeed with Speedrun, a company that calls itself “synthetic creator infrastructure” but which others have labeled as a “phone farm” and “spam-as-a-service.”

Futurism

This framework—"funded by Marc Andreessen"—is interesting because Marc doesn't make decisions on Speedrun applications under $1 million—each Speedrun check represents only about 0.001% of a16z's assets under management. But that precisely illustrates the challenge. Before speculating they were a Speedrun company and verifying, I saw numerous mentions on Twitter of this a16z-backed firm. Most people wouldn't do that.

A more notorious example in a similar vein is Cluely, a startup that promised to help its customers cheat on everything, which a16z led in a $15 million funding round from its AI applications fund.

There's reason to question why a16z, a company actively working to shape America's future, would invest in a startup that prioritizes virality over ethics. Does having a company like Cluely in a portfolio slightly diminish the legitimacy of all other companies, at least in the eyes of those very online?

Very likely. Personally, I don't like it. It feels wrong. It's improper.

However! This is consistent internally.

Beyond actual products, Cluely is promoting a completely new way of building a company in the AI era: assuming that underlying model capabilities are converging and becoming commoditized, distribution will be the only thing that matters, and if a little controversy is needed to get distribution, so be it.

If you're embracing new ways of building a company, $15 million and a bit of Twitter controversy are the cheap price to pay for a front-row seat in one of the most cutting-edge methods.

More generally, in the industry a16z operates in, occasionally appearing foolish is the price you pay to avoid following Kodak's path. You need to be willing to take risks, and taking risks doesn't just mean capital. At a16z's scale, a small amount of capital is the least risky thing.

However, one view holds that, from a macro perspective, the incident at X (which is itself a portfolio company of a16z) is completely insignificant. Katherine Boyle, a general partner at a16z who co-founded the firm's US practice, actually raised this point when I asked her about it:

You could say, yes, maybe we've gotten some backlash on Twitter because of a company that people don't like, whether they're in some corner of San Francisco or in New York or somewhere else. Like, "We don't like them doing American Vitality! We don't like them doing crypto!"

But the sheer size of the machine meant that the minor incident at that moment was utterly insignificant.

Top-tier institutions are large-scale systems. Like the United States of America. When the United States does something embarrassing on the global stage, do we care? No, it doesn't affect the United States, just as it doesn't affect the Roman Catholic Church.

We are thinking in centuries, not tweets.

You may disagree with everything a16z does, but you must respect the company's audacity.

In any case, when I ask some a16z LPs what they think of certain controversial companies on Twitter, I always get a blank "Who?" in response.

The only thing that seems truly important to a16z's returns is being a winner: discover them early, win their trades, and own as many shares as possible over time. Ask any a16z LP about Databricks; they know Databricks.

Now, in the third era, the era of "it's time to lead," it is equally important to help them grow, even as they become larger.

This is what I think Ben meant when he said stepping into the gap between private and public company building, and I think that's the most crucial restructuring to rethink a16z today and how it could potentially yield 5-10x returns on $15 billion.

“In the early stages,” Ben said, “venture capitalists helped companies generate $100 million in revenue, and then handed them over to investment banks to embark on the next journey as publicly traded companies.” That world is gone. Companies are staying private for longer and growing larger, meaning the venture capital industry, led by a16z, needs to expand its capabilities to meet the needs of larger companies.

To this end, the company recently brought in former VMware CEO Raghu Raghuram in a triple threat role—GP for the AI Infrastructure team alongside Martin Casado, GP for the Growth team alongside David George, and Managing Partner and Ben's "strategist, helping him run the company." Together with Jen Kha, Raghu is leading a series of new initiatives to "address the needs of large companies as they grow."

This means partnering with national governments around the world to help portfolio companies scale and sell into their regions, building strategic relationships with companies like Eli Lilly (with whom they jointly launched a $500 million biotechnology ecosystem fund), and increasing the quantity and depth of global LP relationships. It also means expanding the a16z Executive Briefing Center, where large companies can meet directly with a customized set of relevant a16z portfolio companies.

Even for larger companies, building each one from scratch wouldn't be cost-effective, but for a16z, building and distributing them across the portfolio might make sense. Coincidentally, these things happen at the level of governments, trillion-dollar companies, and trillions of dollars in capital.

All of this could mean that a company can remain private for longer without sacrificing the legitimacy, relationships, or access to capital that come with being a publicly traded company.

This means that companies can grow larger in the private market, where they are fully in the addressable market of a16z.

This means that a16z has the opportunity to invest more capital with a reasonable chance of generating strong returns, which means there is the potential to invest more resources to build more capabilities and greater power that it can lend to portfolio companies and increasingly to the entire new technology industry to help bring more and better new technologies to more parts of the economy so that we can all have a better future.

Of course, many things can go wrong. The more money, the more problems. Leaders take the brunt of attacks. And so on.

In my opinion, I think a16z is playing this game on a scale and scope that no one has played before, with all the opportunities and risks involved.

For example, a larger surface area means more potential vulnerabilities. And theoretically, the longer a company remains private, the more difficult it becomes to generate liquidity for LPs, and the more difficult it becomes for LPs to invest in new funds that allow a16z to invest in new companies that may one day become very large companies.

Ultimately, however, only two voter groups matter: founders and LPs, and the company's customers and investors.

The only truly important group: LPs and founders

How the founders and LPs view the company, as reflected in who they get money from and who they give money to, is a condensed version of ever