In terms of the density of Crypto topics and the breadth of participation, Hong Kong has replaced New York as the world's hottest blockchain city.

Article author and source: Brian, W Labs

In early August 2025, Hong Kong's RWA and stablecoin sectors were at their hottest peak in nearly five years. At that moment, the entire city was filled with a passion unseen in 2017-2018: executives from traditional financial institutions, AI entrepreneurs, and even heads of industrial capital flocked to Hong Kong to explore Web3 integration paths. Dinner parties and hotel lobbies were filled with heated discussions about tokenized government bonds, cash management tools, and stablecoin legislation. At the time, a Wall Street banker who had just moved from New York to Hong Kong bluntly stated: in terms of the density of Crypto topics and the breadth of participation, Hong Kong had surpassed New York to become the world's hottest blockchain city.

However, just over two months later, market enthusiasm plummeted. Mainland regulators signaled a clear tightening of policies regarding the tokenization of mainland financial institutions and assets in Hong Kong. Many previously imminent projects involving the tokenization of mainland physical assets were postponed or shelved, and trading volumes on some RWA platforms with Chinese capital backgrounds dropped by 70%-90%. The once-globally renowned Hong Kong RWA craze seemed to vanish in an instant, triggering temporary doubts about Hong Kong's status as an international Web3 center. On November 28, 2025, the People's Bank of China, along with 13 national departments including the Central Financial Stability and Development Office, the National Development and Reform Commission, and the Ministry of Justice, convened a "Coordination Mechanism Meeting on Combating Virtual Currency Trading and Speculation." The meeting, for the first time, included stablecoins within the scope of virtual currency regulation, clarifying that virtual currency-related businesses constitute illegal financial activities and emphasizing that they lack legal tender status and cannot be used as currency.

While stricter regulations in mainland China have impacted Chinese clients to some extent in the short term, restricting capital outflows and leading some mainland institutions to suspend RWA (Retail Advisory Services) operations in Hong Kong, Hong Kong's unique "one country, two systems" framework and independent regulatory structure mean it is theoretically unaffected by mainland policies. This is not a fundamental shift in Hong Kong's RWA policy, but rather another manifestation of the recurring "cooling down at a high level – structural repositioning" cycle in this sector over the past two years. Looking back at 2023-2025, a three-stage evolutionary path can be clearly outlined:

2023-2024 H1: Regulatory Activation and Sandbox Testing Period

HKMA launched Project Ensemble, SFC approved multiple tokenized money market ETFs and bond funds, and local licensed platforms such as HashKey and OSL obtained virtual asset VA licenses, officially establishing Hong Kong's position as a "regulated RWA testing ground".

2024 H2 - July 2025: A period of explosive growth driven by internal and external factors.

The passage of the US GENIUS Stablecoin Act, the start of the Federal Reserve's interest rate cut cycle, the Trump administration's clear pro-crypto stance, and the release of a consultation document on Hong Kong's local stablecoin legislation have triggered an accelerated influx of global funds and projects. Bosera-HashKey Tokenized Money Market ETF, XSGD, and several tokenized private credit funds saw their AUM surge from tens of millions of US dollars to billions of US dollars in just a few months, briefly making Hong Kong the fastest-growing market for RWA globally.

August 2025 to present: Limited participation and risk isolation period

Mainland regulators have adopted a more cautious approach to cross-border asset tokenization, explicitly restricting the deep involvement of mainland institutions and individuals in the Hong Kong RWA ecosystem. This has objectively cut off the most important source of incremental funds and assets previously. Hong Kong local and international capital continues to be allowed to participate fully, but the growth driver has shifted from "on-chaining mainland assets" to "local + global compliant funds allocating to US-led on-chain assets".

The underlying logic behind this cyclical cooling is the dynamic balance that policymakers are striking between "participating in the new global digital economy order" and "preventing systemic financial risks." Hong Kong's role has been redefined: to fully integrate with the US-led blockchain economic network, limited by local resources, while simultaneously building a firewall to prevent risks from spreading to the mainland.

This means that the Hong Kong RWA market has not declined, but has entered a clearer and more sustainable third phase: shifting from the previous "wild growth" to a new pattern of "compliance-driven, DeFi-integrated, and global funding connected to US-based on-chain assets." Pure on-chain, highly transparent, and low-risk cash management RWAs (money market funds, government bond tokens) will continue to grow rapidly, while the path of physical RWAs that heavily relies on mainland assets and funds has been significantly compressed.

For practitioners, the short-term pain caused by repeated policy changes is unavoidable, but there is still ample room for compliance. In particular, the brief window of leniency for DeFi by US regulators, combined with the on-chain services that licensed platforms in Hong Kong can legally provide, creates a rare synergistic advantage, providing a valuable strategic runway for further developing on-chain liquidity, structured products, and cross-chain asset allocation within a regulated framework.

The story of RWA in Hong Kong is far from over; it has simply moved from a period of fervent enthusiasm to a more calm and professional phase of development. This article will further elaborate on the Hong Kong RWA market and relevant representative projects.

Hong Kong RWA Market Landscape

As a leading hub for the integration of blockchain and traditional finance globally, Hong Kong's RWA market was established as Asia's most regulated and mature ecosystem hub by 2025. Driven by the Hong Kong Monetary Authority (HKMA) and the Securities and Futures Commission (SFC), the market focuses on tokenized money market instruments, government bonds, green bonds, and emerging physical assets (such as charging station revenue and international shipping charter rates) through the Project Ensemble sandbox and the "Digital Asset Policy 2.0" framework. The overall landscape is characterized by "institutional dominance, compliance first, and gradual DeFi integration": shifting from experimental issuance in 2024 to large-scale infrastructure construction in 2025, emphasizing cross-chain settlement, stablecoin integration, and global liquidity connectivity. The Hong Kong RWA ecosystem has transformed from a "financing window" into an "innovation platform," deeply integrated with the US-led on-chain network while simultaneously building robust risk barriers to prevent cross-border transmission.

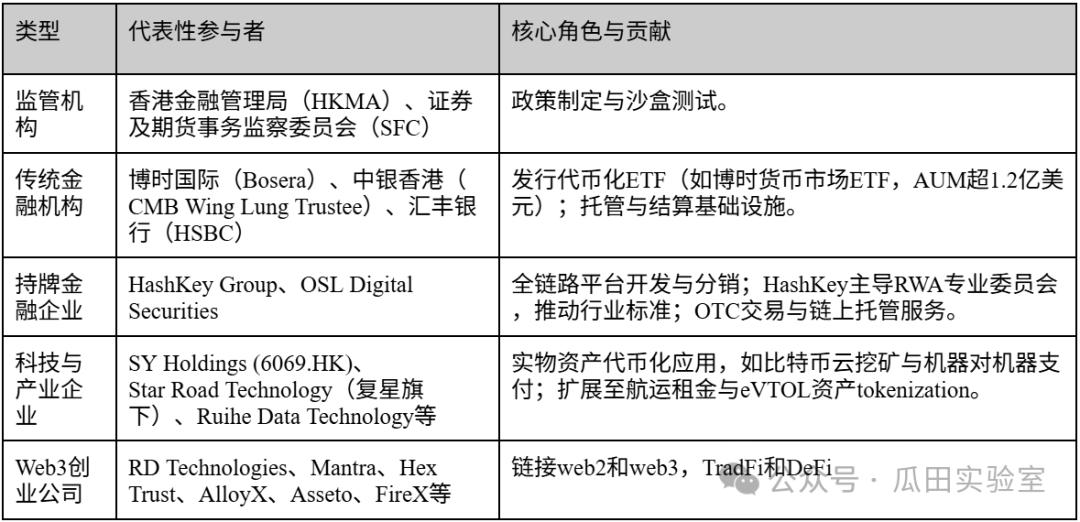

Participant types: dominated by institutional capital, with both technology companies and startups.

The Hong Kong RWA market is highly segmented, dominated by institutional capital, supplemented by local technology companies and emerging Web3 startups, forming a closed-loop ecosystem. The following table outlines the main types (based on active entities in 2025):

It can be seen that the Hong Kong market is still dominated by institutional investors, accounting for about 70%, who lead the issuance of high-barrier products; while enterprises and startups fill the gaps in technology and application, and benefit from the expansion of SFC's VA license.

Overall Scale and Growth Trend

In 2025, the Hong Kong RWA market size, embedded within the global on-chain TVL framework of $26.59 billion to $35.8 billion, saw its AUM jump from tens of millions of US dollars at the beginning of the year to billions of US dollars. This growth was driven by a confluence of policies—the 2025 Policy Address called for investment in RWA infrastructure, and stablecoin regulations were set to take effect in 2026, expected to reduce cross-border payment costs by 90% and settlement time to 10 seconds. The annualized growth rate exceeded 200%, and TVL expanded 58 times in three years. However, high compliance costs (over $820,000 per product issuance) limited retail penetration, with institutional inflows accounting for over 80%.

Future development potential assessment

Hong Kong's RWA market has immense potential, projected to reach a trillion-dollar market size by 2025-2030, ranking among the top three globally (after the US and Singapore). Its advantages lie in the rapid iteration of its regulatory sandbox, aligning with international standards: the SFC is about to open global order book sharing, enhancing liquidity; the Ensemble project will build a tokenized deposit settlement system, extending to emerging trade chains in Brazil and Thailand. The DeFi tolerance window and the integration of AI + blockchain (such as shipping charter tokenization, unlocking a $200 billion market) will drive diversified scenarios, with the startup ecosystem expected to add 50+ new projects. Challenges include cost barriers and the isolation of mainland funds, but this actually strengthens Hong Kong's position as a "global neutral hub": attracting European and American institutions to allocate to US Treasury bonds/MMFs, while local companies deepen their presence in Asian physical assets. Overall, Hong Kong's RWA is shifting from "hype-driven" to "sustainable growth," with key factors being policy continuity and mature infrastructure.

Hong Kong RWA related platforms

1. HashKey Group – The “Full-Stack” Cornerstone of the Compliance Ecosystem

In Hong Kong's grand narrative of becoming a global Web3 hub, HashKey Group is undoubtedly the most representative "flagship" entity. As a leading end-to-end digital asset financial services group in Asia, HashKey is not only a pioneer in Hong Kong's compliant trading market but also a builder of key infrastructure for RWA asset issuance and trading. Its strategic layout, from underlying blockchain technology to upper-level asset management and trading, forms a complete compliance closed loop.

Founded in 2018 and headquartered in Hong Kong, HashKey Group has a deep connection with Wanxiang Blockchain Labs. From the very beginning of the Hong Kong Securities and Futures Commission's (SFC) implementation of the licensing system for virtual asset trading platforms, HashKey established a policy of embracing regulation.

In August 2023, HashKey Exchange became one of the first exchanges in Hong Kong to receive upgrades to its Type 1 (Securities Trading) and Type 7 (Automated Trading Services) licenses, authorizing it to provide services to retail investors. This milestone not only solidified its legitimate monopoly advantage in the Hong Kong market (as one of the duopoly players) but also provided an effective channel for the secondary market circulation of compliant RWA products (such as STOs, Security Token Offerings) in the future.

On December 1, 2025, HashKey Group passed the Hong Kong Stock Exchange's listing hearing and is about to be listed on the Hong Kong Main Board, potentially becoming the "first licensed virtual asset stock in Hong Kong." Many industry experts have analyzed HashKey's prospectus and listing prospects. This author believes that HashKey's listing is a landmark event that will help Hong Kong compete globally (especially relative to Singapore and the United States) for pricing power and influence in the Web3 field, establishing Hong Kong's position as a "compliant digital asset center."

HashKey's architecture is not a single exchange model, but rather an ecosystem that serves the entire lifecycle of RWA:

HashKey Exchange (trading layer): Hong Kong's largest licensed virtual asset exchange, providing fiat currency (HKD/USD) deposit and withdrawal channels. For RWA, this is the future destination for liquidity after asset tokenization.

HashKey Tokenisation (Issuance Service Layer): This is the core engine of its RWA business. This division focuses on assisting institutions in tokenizing physical assets (such as bonds, real estate, and artwork), providing a one-stop STO solution from consulting and technical implementation to legal compliance.

HashKey Capital (Asset Management): A top global blockchain investment firm with over $1 billion in assets under management (AUM). Its role in the RWA field is primarily focused on providing funding and developing products (such as ETFs).

HashKey Cloud (Infrastructure Layer): Provides node verification and underlying blockchain technology support to ensure the security and stability of asset on-chain.

In the Hong Kong RWA market, HashKey's core competitiveness lies in two dimensions: "compliance" and "ecosystem synergy."

Regulatory Competitive Advantage: RWA's core lies in mapping regulated offline assets onto the blockchain. HashKey possesses full compliance licenses, enabling it to legally handle tokens classified as "securities," a barrier that most unlicensed DeFi platforms cannot overcome.

"Consolidation" level ecosystem capabilities: It can connect the asset side, the funding side, and the trading side. For example, a real estate project can be tokenized by HashKey Tokenisation, with HashKey Capital participating in early subscriptions, and finally listed and traded on HashKey Exchange.

Institutional-grade connectors: HashKey has established fiat currency settlement partnerships with traditional financial institutions such as ZA Bank and Bank of Communications (Hong Kong), solving RWA's most critical problems of "deposit and withdrawal" and fiat currency settlement.

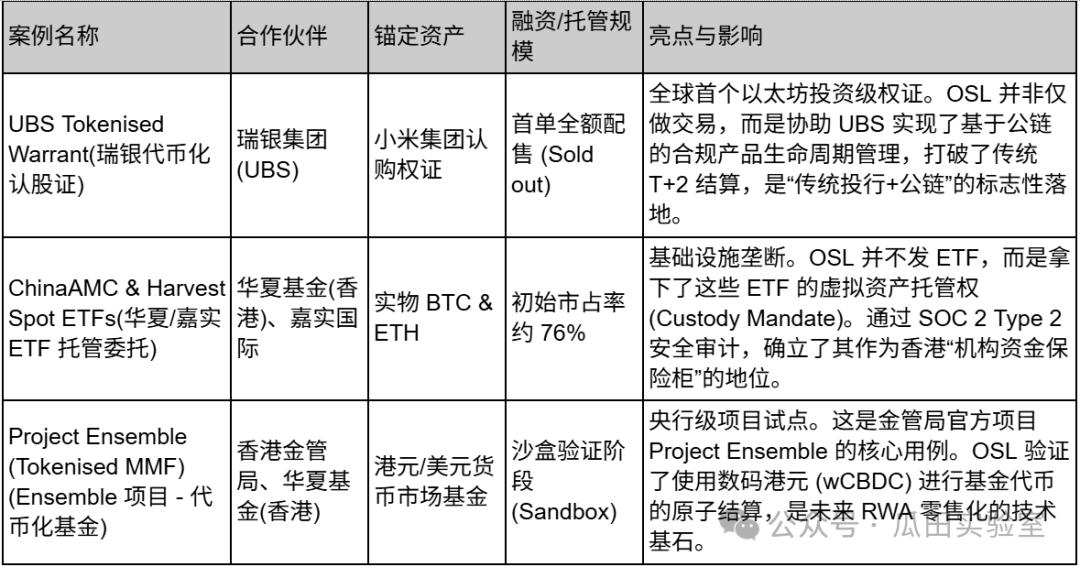

HashKey's practices in the RWA field are mainly reflected in two directions: "on-chaining of traditional financial assets" and "compliant issuance." The following is a summary of its typical cases:

HashKey Group is more than just an exchange; it's the operating system of the Hong Kong RWA market. By holding scarce compliance licenses and building a full-stack technological infrastructure, HashKey is transforming "asset tokenization" from a concept into an executable financial business. For any institution looking to issue or invest in RWA in Hong Kong, HashKey is currently an indispensable partner.

2. OSL Exchange – The “Digital Arms Dealer” and Infrastructure Expert of Traditional Finance

In the RWA game in Hong Kong, if HashKey is the "flagship" that charges ahead and builds a complete ecosystem, then OSL Group (formerly BC Technology Group, 863.HK) is the "arms dealer" that works behind the scenes and provides technology to traditional financial institutions.

As the only publicly listed company in Hong Kong focusing on digital assets, OSL possesses the financial transparency and auditing standards of a listed company. This makes OSL the preferred "safe passage" for traditional banks and sovereign wealth funds that are extremely risk-averse to enter the RWA market.

Unlike HashKey, which actively expands its retail user base and builds a public blockchain ecosystem, OSL's strategic focus is heavily concentrated on institutional business. Its architecture is not designed to "create an exchange," but rather to "help banks build their products."

The unique competitive advantage of a listed company:

RWA's core strength lies in passing compliance reviews by traditional financial institutions (TradFi). For large banks, the compliance costs of partnering with a public company are far lower than those of a private enterprise. OSL's financial statements are audited by the Big Four accounting firms, and this "institutionalized trust" is its biggest asset in the B2B market.

Technology Provider (SaaS Model):

OSL is not committed to having all assets traded on its platform. Instead, it is willing to provide its technology (OSL Tokenworks) to help banks build their own tokenized platforms. This is a "selling shovels" strategy—OSL profits from whoever issues an RWA as long as it uses OSL's underlying technology or liquidity pools.

Monopolistic position in the custody industry:

In the first batch of Bitcoin/Ethereum spot ETFs issued in Hong Kong, both Harvest and ChinaAMC chose OSL as the virtual asset custodian. This means that OSL controls the security of more than half of the underlying assets in the Hong Kong ETF market. For RWA, "whoever controls the custody controls the lifeline of the assets."

In the RWA industry chain, OSL defines itself as a sophisticated conduit connecting traditional assets with the Web3 world:

RWA Structurer & Distributor:

Leveraging its status as a licensed brokerage firm, OSL excels at structuring complex financial products. It goes beyond simply "putting assets on-chain," focusing instead on the tokenization of investment-grade products such as bank notes and structured products.

Cross-border compliant liquidity network:

OSL has deep partnerships with Zodia Markets, a subsidiary of Standard Chartered Bank, and Japanese financial giants. Regarding RWA liquidity, OSL utilizes an "institutional-to-institutional" dark pool and over-the-counter (OTC) trading approach, rather than a retail order book model.

OSL's case studies are typically not limited to Hong Kong, but have a strong international demonstration effect, and its partners are all top TradFi giants. Due to its B2B nature, the scale of its funding is generally not disclosed.

To make the differences between the two more intuitive, a comparison table of HashKey vs. OSL has been compiled:

If HashKey is building a bustling "Web3 business metropolis" in Hong Kong, then OSL is like the chief engineer responsible for the city's underground pipe network, vault security, and power transmission. In the RWA market, OSL does not pursue the most high-profile "issuance," but rather strives to become the safest "warehouse" and the most compliant "channel" for all RWA assets.

3. Ant Digital – A “Trusted Bridge” for On-Chain Physical Assets

In the Hong Kong RWA landscape, Ant Financial (and its Web3 brand ZAN) represents a disruptive force from internet giants. Unlike financial institutions that focus on "licenses" and "transactions," Ant Financial's core competitiveness lies in solving RWA's most fundamental pain point: how to prove that on-chain tokens truly correspond to off-chain physical assets?

Ant Financial's strategic path is very clear: leveraging AntChain's high-performance technology, which has been deeply rooted in China for many years, and combining it with Trusted IoT, it provides technical standards and verification services for global RWA projects in Hong Kong, an international gateway.

Ant Financial does not operate as a "trading venue" in the Hong Kong RWA market, but rather positions itself as a Web3 technology service provider. Its business logic can be summarized as "two ends and one cloud":

On the asset side: Trusted modules are embedded in physical equipment such as photovoltaic panels, charging piles, and construction machinery to collect data in real time and upload it directly to the blockchain. This transforms RWA from being "based on issuer credit" (trusting the issuer) to being "based on asset credit" (trusting the real-time cash flow generated by the equipment).

Capital Side: Through the ZAN brand, we provide institutional investors with KYC/KYT (customer identity verification), smart contract auditing, and node services to ensure the compliance of fund inflows and outflows.

Privacy protection: It is one of the very few vendors in the Hong Kong Monetary Authority's Project Ensemble (sandbox) that can provide zero-knowledge proof (ZKP) technology, solving the deadlock that banks have to "verify transactions without disclosing trade secrets" when settling assets on public blockchains.

While HashKey and OSL process "securitized assets" (such as bonds and funds), Ant Financial is extremely adept at handling "non-standard physical assets":

Trustworthy source: Traditional RWA relies on auditors to conduct inventory checks in warehouses, while Ant Financial, by implanting chips, allows the operational data (power generation, mileage) of new energy vehicles, batteries, and even biological assets (such as cattle) to be recorded on the blockchain in real time.

Large-scale concurrent processing: Inheriting the technological genes of Alipay's "Double Eleven" level, Ant Financial's blockchain can support the concurrent on-chain processing of hundreds of millions of asset data, which is difficult for most public chains to achieve.

ZAN's internationalization: In 2024-2025, ZAN rapidly rose to prominence in Hong Kong, becoming a key middleware platform connecting Web2 developers and the Web3 world, especially gaining a foothold in the field of compliance technology.

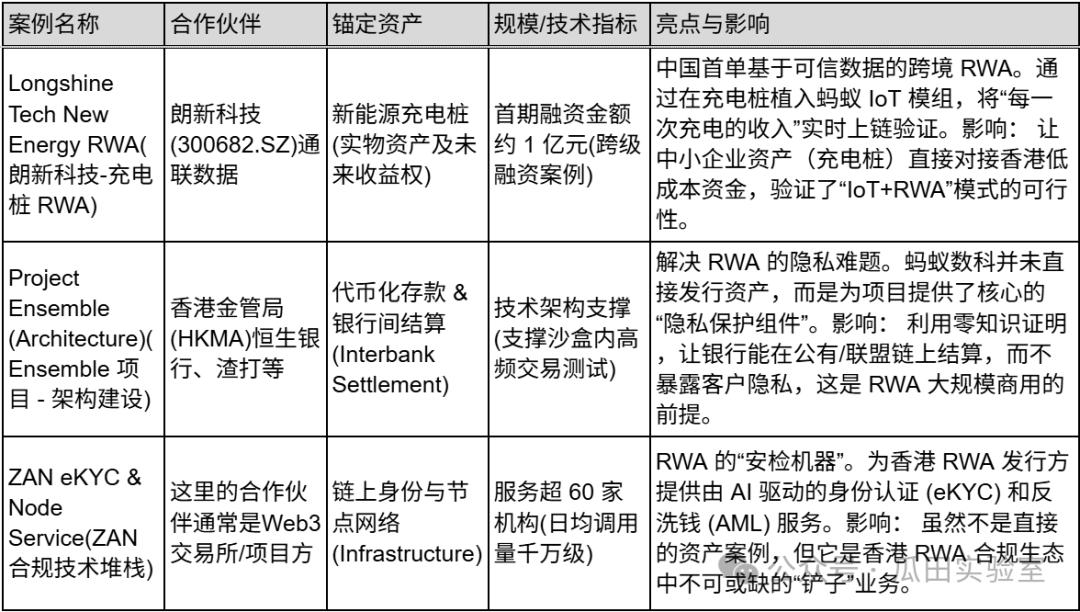

Ant Financial's case studies mainly embody "on-chain integration of the real economy" and "interbank settlement architecture".

If HashKey is like Taobao, building a platform for buying and selling RWA products, and OSL is like a vault, providing the most secure warehouse to safeguard RWA assets for institutions, then Ant Financial is like a "smart factory + quality inspector." They delve into the production process (charging piles, batteries), assigning each asset a "qualification label" (IoT verification) and providing technology to ensure the smooth circulation of these assets. In the Hong Kong RWA market, Ant Financial focuses on data, aiming to become the "customs officer" and "translator" for physical world assets connecting to the Web3 world.

4. Conflux Network – A “compliant public blockchain” foundation connecting Mainland China and Hong Kong

In the Hong Kong RWA market, most platforms (such as HashKey and OSL) mainly address the issue of "how to trade assets locally in Hong Kong," while Conflux addresses the issues of "how to legally export mainland assets" and "what currency to use for settlement."

As "China's only compliant public blockchain," Conflux leverages its background with the Shanghai TreeGraph Blockchain Research Institute and deeply integrates with "national team" resources such as China Telecom and the Belt and Road Initiative. In the Hong Kong market in 2025, Conflux will no longer be just a technology public blockchain, but will evolve into the core issuance layer of offshore RMB/HKD stablecoins.

Conflux's RWA strategy differs significantly from others; it avoids the crowded asset management track and focuses on the very bottom layer of infrastructure:

The lifeblood of RWA (stablecoins): Conflux incubated and supported AnchorX (primarily funded by Hony Capital), which is dedicated to issuing a compliant Hong Kong dollar stablecoin (AxHKD). In RWA transactions, asset tokenization is the first step, but "what to use to buy" is the second. Conflux aims to make AxHKD the settlement currency for the Hong Kong RWA market, pegged to USDT/USDC.

Physical Entry Point (BSIM Card): The BSIM card, launched in partnership with China Telecom, directly embeds the blockchain private key into the phone's SIM card. For RWA, this means that future asset ownership verification (such as purchasing a tokenized property on your phone) can be linked to the telecom operator's real-name identity, solving RWA's most challenging "DID (Distributed Identity Authentication)" problem.

Mainland-Hong Kong Connector: Utilizing its R&D center in Shanghai (tree diagram), Conflux can meet the overseas expansion needs of mainland enterprises and use technology to legally map mainland physical assets (such as photovoltaics and supply chains) onto the Conflux public chain in Hong Kong for financing.

At the RWA circuit, Conflux's moat lies in its geopolitical advantage:

Interoperability after "de-sensitization": Conflux has implemented a unique technical architecture that complies with mainland regulations (for tokenless blockchain technology applications) while enabling tokenized transactions in Hong Kong via cross-chain bridges. This makes it the most "politically correct" choice for mainland state-owned enterprises and central enterprises attempting to expand RWA overseas.

Payment and settlement closed loop: Through the AnchorX project, Conflux is actually participating in the Hong Kong Monetary Authority's "sandbox supervision". Once the Hong Kong dollar stablecoin is launched, Conflux will transform from a mere "road" into a financial network with the power to set "tolls".

High-performance throughput: RWAs (especially high-frequency notes or retail assets) require extremely high TPS (transactions per second). Conflux's tree-graph structure claims to achieve 3,000-6,000 TPS, which is more advantageous than the Ethereum mainnet when handling high-concurrency transactions in traditional finance.

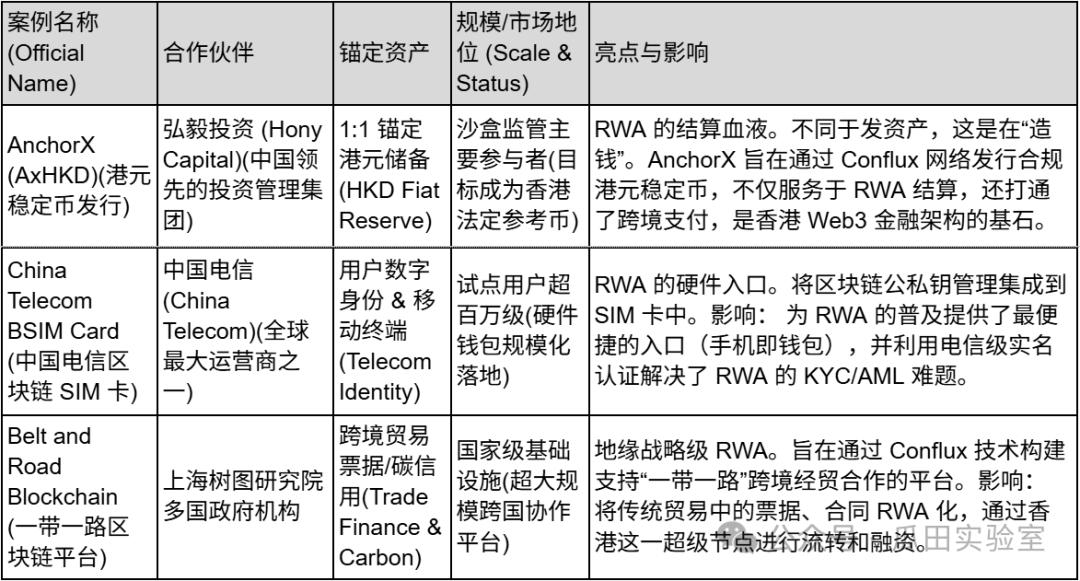

Conflux’s case studies focus on “monetary infrastructure” and “national-level cooperation”.

Conflux Network is the only "public blockchain-level" player in the Hong Kong RWA market. It does not make money directly from transaction fees, but instead attempts to become a "digital Silk Road" connecting Chinese manufacturing with global capital by setting underlying standards (stablecoin standards, SIM card standards).

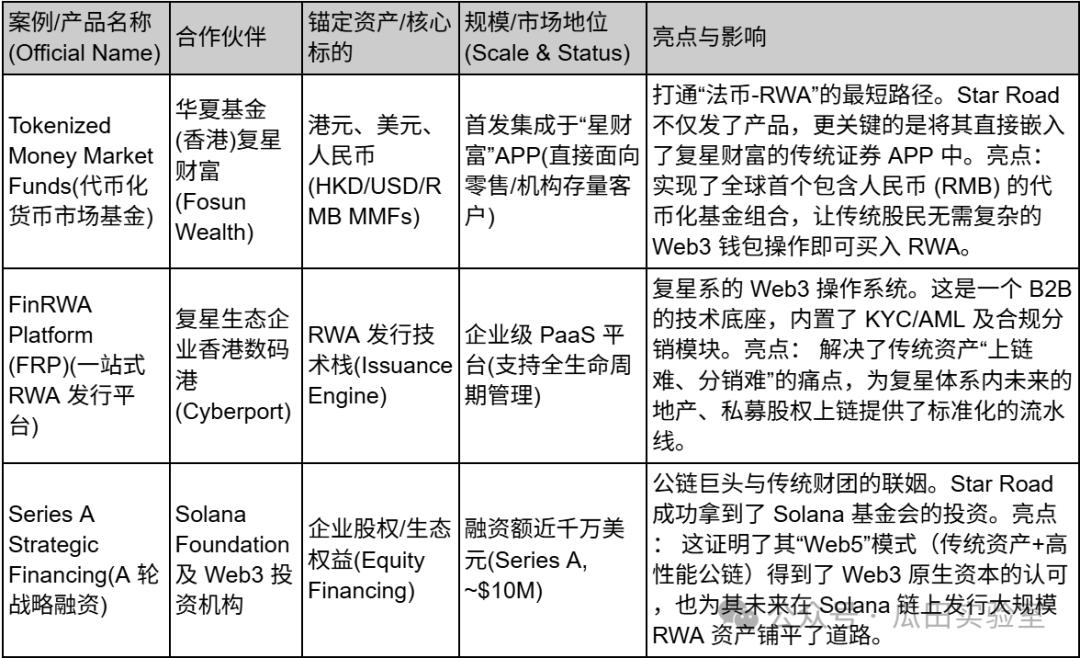

5. Star Road Technology – A Customized First-Class Gateway for "Old Money" to Web3

Amidst the clamor in Hong Kong's RWA market, Star Road Technology (sometimes marketed as Finloop overseas) is not the loudest "disruptor," but it is very likely the most well-established "successor."

Rather than viewing Star Road as an independent Web3 startup, it's more accurate to see it as an "official landing craft" dispatched by Fosun International, a large conglomerate, to the digital asset world. Independently incubated by Fosun Wealth, Star Road's very existence carries a distinct corporate vision: it doesn't aim to build a new financial order from scratch, but rather to smoothly and compliantly "ferry" the vast existing assets and high-net-worth clients of traditional finance to the world of blockchain.

Star Road has proposed a unique "Web5" concept at the strategic level. Unlike the purely decentralized idealism of Web3, Star Road's Web5 strategy is more like a pragmatic compromise—it attempts to integrate the mature user experience and traffic entry points of the Web2 era (Fosun Wealth's customer base) with the value interconnection technology of the Web3 era.

Within this narrative, Star Road built its core infrastructure—the FinRWA Platform (FRP). This is an enterprise-grade RWA issuance engine, but its initial design wasn't to serve anonymous on-chain geeks; rather, it was intended to serve institutions and high-net-worth individuals within the Fosun ecosystem. It acts as a sophisticated converter, connecting Fosun's long-established real estate, consumer goods, and cultural tourism assets on one end, and a compliant digital asset distribution network on the other. For Star Road, RWA is not the goal, but rather a means to activate the liquidity of the group's existing assets.

Unlike other platforms that are keen to explore high-risk, high-return DeFi gameplay, Star Road has chosen the most stable entry path: tokenization of money market funds.

Through a deep alliance with China Asset Management (Hong Kong) and its parent company Fosun Wealth, Star Road's first flagship product focuses on tokenized money market funds in Hong Kong dollars, US dollars, and RMB. This choice demonstrates remarkable strategic foresight—money market funds are the most familiar and accessible investment option for traditional investors. By using its technology to tokenize these funds, Star Road is effectively providing a safe entry point for those with "old money" who are hesitant about cryptocurrencies.

More importantly, Star Road has established an RWA (Remotely Used Asset) channel for the RMB. Given Hong Kong's position as an offshore RMB center, this capability allows Star Road to accurately target mainland-based capital holding substantial amounts of offshore RMB that seek compliant overseas capital appreciation.

Star Road's business model resembles that of a traditional exchange, more akin to a "boutique digital investment bank." Its case studies demonstrate a complete closed loop, from "underlying technology" to "asset issuance" and then to "ecosystem capital."

Star Road Technology represents the traditional financial elite's understanding and transformation of Web3: not pursuing radical decentralization, but rather the ultimate in compliance, security, and user experience. For institutions and high-net-worth individuals who want to retain the traditional financial services experience while allocating digital assets, Star Road is the most seamless and convenient entry point.

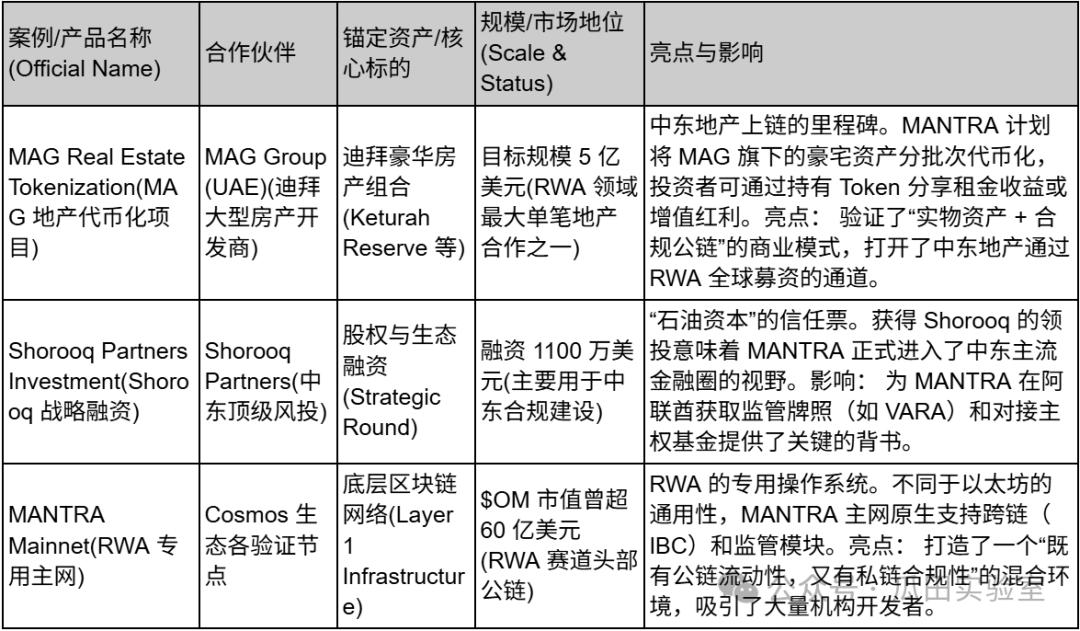

6. MANTRA – RWA's "compliant highway" connecting the Middle East and Asia.

In the era of RWA's fierce competition, MANTRA represented the rise of the "infrastructure faction." It was not content with simply issuing a single asset, but rather attempted to define the underlying standards for RWA assets to run on the blockchain.

Formerly known as MANTRA DAO, MANTRA has evolved over several years into an RWA public blockchain focused on regulatory compliance. Its strategic focus is unique – avoiding the fiercely competitive US market and not even entirely relying on Hong Kong, it instead heavily invests in the UAE, leveraging Dubai's highly favorable Virtual Asset Regulatory Framework (VARA) to build a corridor connecting Middle Eastern capital with Asian liquidity.

MANTRA addresses a core pain point at the strategic level: the contradiction between the "permissionless" nature of public blockchains and the "strong regulation" of finance.

Native Compliance: MANTRA Chain has built-in identity authentication (DID), KYC/AML modules, and a compliance whitelist mechanism in its underlying protocol. This means that developers do not need to write complex compliance code themselves; they can directly call MANTRA's modules to issue regulatory-compliant real estate tokens or bonds.

Connecting the Middle East's "Oil Capital": MANTRA secured a lead investment from Shorooq Partners, a top Middle Eastern venture capital firm, and established a deep partnership with Dubai real estate giant MAG. This not only brings funding but, more importantly, access to the vast real estate and sovereign wealth resources of the Middle East—a unique advantage that other platforms primarily reliant on US dollar or Hong Kong dollar assets lack.

Mainnet Incentives and Token Economics: MANTRA has built a tight economic loop through the buyback and staking mechanism of its native token, $OM. It uses token incentives to attract institutional validators and asset issuers, attempting to leverage Web3 incentive models to drive the on-chaining of assets on TradeFi.

On the asset side, MANTRA has chosen the most demanding yet also the most attractive track: real estate. Unlike government bond RWA (which is also a strength of platforms like Star Road), real estate RWA requires handling complex offline title confirmation and legal structures. MANTRA is partnering directly with Dubai developer MAG, planning to tokenize a $500 million luxury real estate portfolio. This approach is extremely ambitious—if MANTRA can turn Dubai's luxury homes into on-chain circulating tokens, it will prove its ability to handle "non-standard, large-value, physical assets," which provides a much deeper competitive advantage than simply tokenizing government bonds.

In addition, MANTRA launched a large-scale token buyback program in 2025 (committing at least $25 million), a behavior similar to a listed company's "stock buyback," which greatly enhanced institutional investors' confidence in its token economic model.

MANTRA's business portfolio exhibits a clear characteristic of "Middle Eastern assets + Asian technology + global compliance":

Although MANTRA originated in Hong Kong, it has shifted its focus to the Middle East to align with its RWA compliance strategy. MANTRA represents another possibility in the RWA market: not just putting assets on the blockchain, but building a dedicated blockchain for those assets. For investors optimistic about the rise of Middle Eastern capital and the prospects of blockchain-based real estate, MANTRA is currently the most representative infrastructure target.

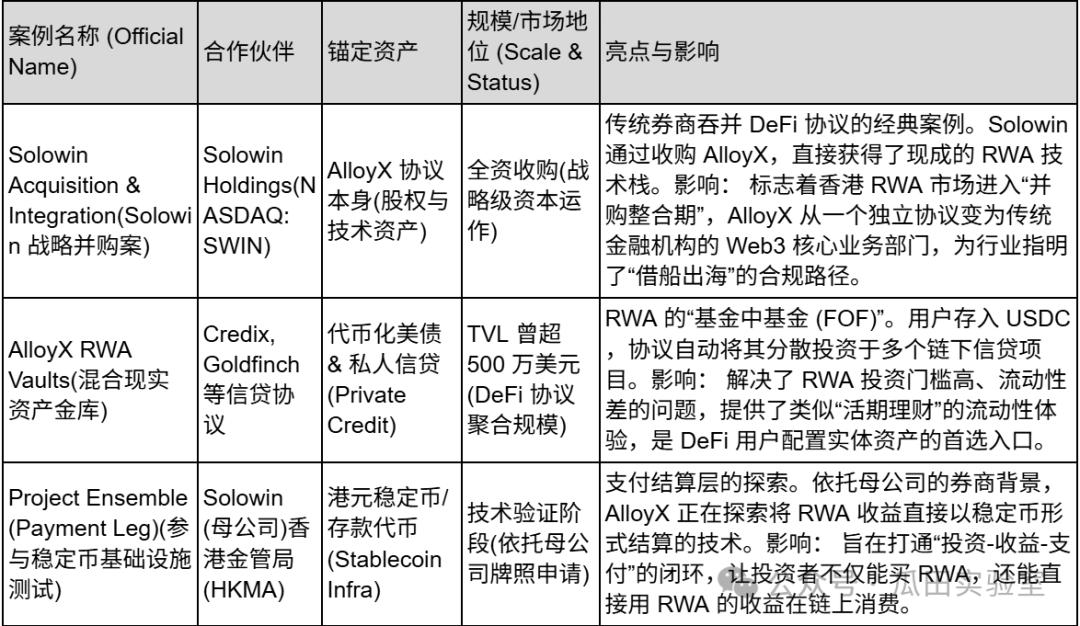

7. AlloyX – A “Hybrid Aggregator” Connecting DeFi Liquidity and Real-World Assets

In the grand narrative of RWA in Hong Kong, if HashKey and OSL are building “asset-heavy” infrastructure similar to Nasdaq or bank vaults, then AlloyX represents another agile force in the RWA market – a “DeFi native aggregator”.

As a Web3 fintech company originating from San Francisco, USA, and later wholly acquired by Hong Kong-listed brokerage Solowin Holdings (NASDAQ: SWIN), AlloyX plays a unique "CeDeFi (centralized and decentralized hybrid finance) connector" role in the Hong Kong RWA landscape. It does not directly hold heavy physical assets, but instead uses smart contract technology to "package" credit assets scattered across different chains and protocols into highly liquid financial products, directly delivering them to investors in the crypto world.

AlloyX's business logic is completely different from traditional exchanges. It is essentially an aggregation protocol for RWA assets.

In the early RWA market, assets were fragmented: investors wanting to buy US Treasury bonds might have to go to one platform, while those wanting to invest in private lending might have to go to another, with extremely high barriers to entry. AlloyX addresses this pain point. It has built a modular "Vault" system that can access assets from multiple upstream lending protocols such as Centrifuge, Goldfinch, and Credix. By standardizing these assets into a unified tokenized product, AlloyX allows users to easily allocate stablecoins like USDC to real-world lending assets, much like depositing money into a money market fund.

With its formal acquisition by Solowin Holdings in 2025, AlloyX completed a remarkable transformation from a "pure DeFi protocol" to a "compliant fintech flagship." Now, AlloyX is more like a tentacle of Solowin, a traditional brokerage firm, extending into the Web3 world. Leveraging Hong Kong's compliance license advantages, it distributes traditional securities, funds, and other assets to global investors in the form of tokens through AlloyX's technological channels, achieving true "asset ownership confirmation in the traditional world and liquidity release in the blockchain world."

In the highly competitive Hong Kong market, AlloyX's competitive advantage lies primarily in the combination of its unique shareholder background and technological architecture.

First, the endorsement and resource injection from a listed company is its biggest differentiating advantage. As a wholly-owned subsidiary of Nasdaq-listed Solowin, AlloyX transcends the compliance dilemmas faced by ordinary DeFi projects. It can directly utilize the Type 1, 4, and 9 licenses held by its parent company from the Hong Kong Securities and Futures Commission (SFC) to legally design and distribute tokenized products involving securities. This "front-end DeFi experience + back-end licensed brokerage risk control" model perfectly aligns with Hong Kong's CeDeFi regulatory direction.

Secondly, AlloyX possesses exceptional composability capabilities. Unlike single-asset issuers, AlloyX excels at using algorithms to mix and package RWA assets of varying risk levels (such as low-risk US Treasury bonds and high-risk trade finance) to create on-chain products similar to structured notes. This capability allows institutional investors to customize their RWA portfolios on-chain according to their risk appetite, significantly enriching profit strategies in the RWA market.

AlloyX's business practices mainly focus on two dimensions: "asset aggregation" and "compliant issuance." The following are its most representative business cases:

Looking back at AlloyX's development path, we can clearly see that it doesn't pursue a large and comprehensive platform traffic, but rather focuses on the refined operation of the asset side. Through its acquisition by Solowin, AlloyX has effectively become a "technology engine" for traditional financial institutions' digital transformation of RWA. For the market, AlloyX has proven that RWA is not just a game for giants; technology-based protocols, through deep integration with licensed institutions, can also find a core ecosystem within the high walls of compliance.

8. Asseto – An RWA "asset packaging factory" designed specifically for institutions.

In Hong Kong's RWA industry chain, Asseto plays a crucial role as the "source of assets." It is located at the very top of the industry chain, directly connecting with the real economy.

As the flagship RWA infrastructure project strategically invested in by HashKey Group, Asseto boasts a strong "pedigree." Instead of directly engaging with retail investors, it focuses on solving the most challenging "first mile" problem in RWA: how to transform a building or a fund into a compliant token through legal structure, technical standards, and compliance processes?

Asseto's business model is highly vertical and has high barriers to entry, primarily serving TradFi giants with billions of dollars in assets.

RWA Asset Issuance Gateway: Asseto provides a standardized technology stack that allows institutions to "one-click on-chain" assets such as cash management products, real estate, and private lending. It not only provides smart contracts but, more importantly, offers "legal packaging" services to ensure that on-chain tokens have a genuine claim to the underlying assets under Hong Kong law.

The "asset conveyor belt" of the HashKey ecosystem: As a portfolio company of HashKey, Asseto is an important source of potential RWA assets for the HashKey Exchange. Asseto is responsible for organizing the assets off-chain (cleaning, ownership verification, tokenization), and then distributing them to secondary market investors through HashKey's compliant channels.

Asseto, a "situational partner" in the stablecoin sandbox, is working closely with several institutions applying for stablecoin licenses in Hong Kong. They are committed to using RWA assets as reserve assets for stablecoins and exploring advanced approaches such as "issuing stablecoins using tokenized government bonds/cash".

Asseto's core advantage in the Hong Kong market lies in the top-tier resources afforded by its shareholder structure.

HashKey's technical and channel support: HashKey not only provides funding but also opens up the HashKey Chain (L2 public chain) to Asseto as its preferred issuance platform. This means that assets issued on Asseto inherently have access to Hong Kong's largest compliant liquidity outlet.

Asset injection from DL Holdings: DL Holdings (1709.HK), a Hong Kong Main Board listed company, not only invested in Asseto but also signed a strategic agreement to tokenize its managed family office assets (such as commercial real estate and fund shares) through Asseto. This solves the most troublesome "asset shortage" problem for the RWA project—Asseto started with high-quality assets from a listed company.

Asseto's case studies are highly "customized" for institutions, primarily focusing on real estate and cash management:

Asseto is the "asset alchemist" of the Hong Kong RWA market. Instead of directly targeting retail investors, it operates behind the scenes, using sophisticated legal and technical tools to transform the massive and cumbersome assets of traditional financial institutions into coins suitable for circulation in the Web3 world.

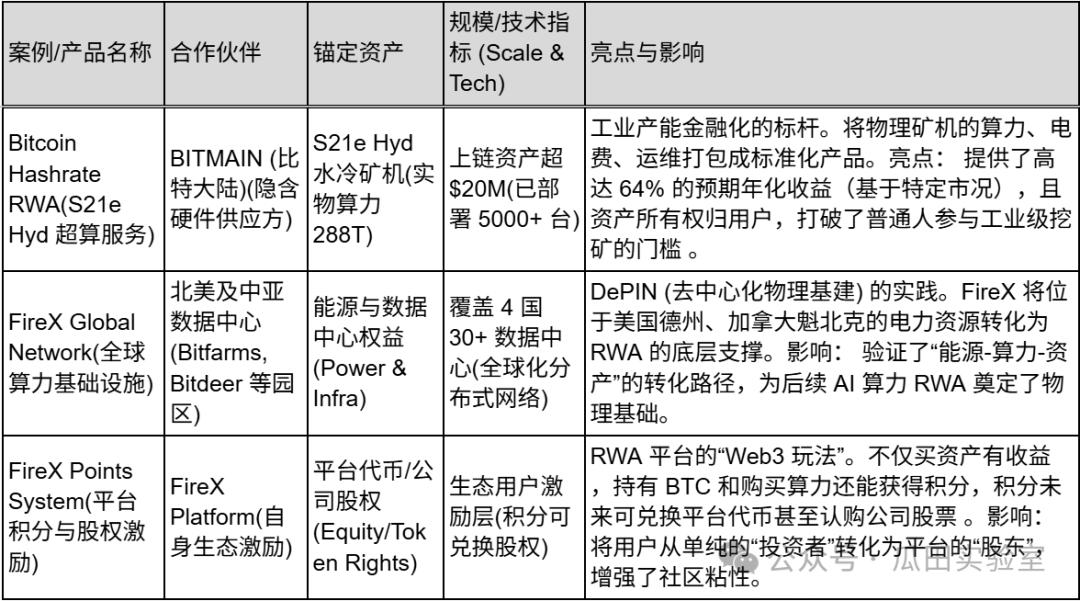

9. FireX – An “industrial-grade” RWA platform for unlocking computing power liquidity.

In the Hong Kong RWA market, most platforms deal with "paper assets" (such as bonds and equities), while FireX focuses on "productive assets".

FireX is an institutional-grade RWA trading platform whose core narrative is "financializing Bitcoin's source of power (computing power)." Through partnerships with top infrastructure providers like Bitmain, it encapsulates data centers and mining machines located globally (in the US, Canada, Kazakhstan, etc.) into on-chain tradable RWA tokens. For investors, purchasing FireX's RWA products is essentially buying the "right to future cash flow" from a running supercomputer.

FireX's business logic is very vertical, solving the mismatch problem between the traditional mining industry's "poor liquidity" and Web3 funds' "lack of stable real returns":

Assetization of computing power: FireX transforms the "S21e Hyd mining machine" and its generated computing power (288 TH/s), which originally belonged only to the physical world, into on-chain assets. This means that users do not need to build their own mining farms or maintain the machines to hold computing power and earn Bitcoin mining rewards.

FireX, a global energy arbitrage network, is more than just a trading platform; it's backed by a vast network of physical infrastructure. It owns or partners with over 30 data centers in locations such as Texas, Quebec, and Ethiopia. Essentially, it's engaged in global energy arbitrage—finding the cheapest electricity, converting it into Bitcoin, and then distributing the profits through RWA.

Diversified Asset Allocation Gateway: Beyond its core Bitcoin hash power, FireX's vision includes global high-quality stocks (such as NVDA and MSFT), pre-IPO equities, and the RWA-ification of AI computing power assets. It aims to create a comprehensive asset allocation basket "covering both the digital and physical worlds."

Unlike pure software protocols, FireX's competitive advantage is built on a heavy foundation of "hardware" and "ecosystem relationships":

Verifiable Entity Scale: FireX currently has over 5,000 supercomputing servers deployed, managing over 1,000 PH/s of computing power, with on-chain assets valued at over $20 million. This tangible entity scale provides RWA with the most fundamental credit backing—ownership belongs to the customer, and the assets are genuinely in operation.

Top-tier ecosystem: According to disclosures, FireX's partner network includes mining machine giant BITMAIN, mining pool Antpool, and leading institutions such as Binance, Coinbase, and Tether. This resource integration capability, spanning the entire industry chain from "mining machine production to mining, exchanges, and stablecoins," ensures the stability of its asset supply and low-cost advantages (such as zero machine space fees and zero service fees).

High-yield product design: During a Bitcoin bull market, FireX's RWA (Return on Investment) demonstrates extremely high return elasticity. According to calculations for its S21e Hyd product, under the optimistic assumption that Bitcoin's price reaches $150,000, the ROI (Return on Investment) could even approach 100%. This is significantly more attractive than traditional government bond RWAs.

FireX's business is highly focused on "financialization of computing power" and "global asset allocation":

FireX is a "hardcore industrial" player in the RWA (Real-Time Web Application) field. It goes beyond the simple "old wine in new bottles" model of traditional financial assets (such as government bonds), and instead provides the Web3 world with a basic revenue layer supported by real machine noise and electricity consumption by "securitizing and packaging" Bitcoin computing power, a native digital asset.

Bipolar Narrative: A Deep Comparison of the Hong Kong and US RWA Markets

If 2024 was the year of proof-of-concept for RWA, then 2025 will be the year that the "bipolarization" of the global RWA market landscape takes shape. In the global RWA landscape, the United States and Hong Kong represent two completely different, yet mirror-like, evolutionary paths.

The United States, relying on its native DeFi innovation and dollar hegemony, has become a "super factory" for RWA assets; while Hong Kong, relying on its unique institutional advantages and geographical location, has become a "super boutique" and "distribution hub" for RWA assets.

1. Regulatory Philosophy: "Enforcement-Style Tolerance" vs. "Sandbox-Style Access"

The United States: The Law of the Jungle from the Bottom Up

The RWA market in the United States has grown wildly in the cracks of regulation. Although the regulatory environment softened after the Trump administration took office in 2025, its core logic remains the game between "regulation by enforcement" and "DeFi first".

Characteristics: US projects (such as Ondo and Centrifuge) often start as DAOs or decentralized protocols, pursuing scale and technological innovation first, and then using complex legal structures (such as SPVs for offshore segregation) to circumvent the SEC's securities determination.

Advantages: Extremely rapid innovation; asset portfolios can be created through smart contracts without the need for license approvals, making it easy to create phenomenal products with strong economies of scale, such as BlackRock BUIDL.

Disadvantages: The legal gray area is large, and once cross-border distribution or non-qualified investors (retail) are involved, there are extremely high compliance risks.

Hong Kong: Top-down Design

Hong Kong has taken a completely opposite approach – “Licensing Regime”. From HashKey obtaining its exchange license to Star Road relying on licenses 1, 4, and 9 held by Fosun Wealth, every step of Hong Kong RWA’s development has been within the sights of the SFC and HKMA.

Features: "No license, no RWA". All projects (such as OSL, HashKey) must operate within the Project Ensemble sandbox or existing securities framework. Regulators are not only judges, but also "product managers" (such as guiding the design of tokenized deposits).

Advantages: Extremely high certainty. Once the product is approved (such as China Asset Management's tokenized product), it can legally connect to the banking system and retail funds, possessing the trust endorsement of traditional financial institutions.

Disadvantages: The entry barriers and compliance costs are extremely high (over $800,000 per project), which stifles grassroots innovation and results in market participants being mostly "elite" companies or "conglomerates".

2. Market Structure: "Fundamentalist DeFi" vs. "Traditional Consortiums"

The United States: Home Ground for DeFi Native Capital

The US RWA market structure is "DeFi backward compatible with TradFi". Major funding sources include on-chain USDC/USDT whale, DAO treasuries, and crypto hedge funds. Project teams are typically led by tech geeks who disdain cumbersome offline processes and focus on converting everything (including government bonds) into ERC-20 tokens, then placing them on Uniswap or Aave for collateralized lending.

Typical profile: Protocols like MakerDAO or Compound use the RWA module to purchase US Treasury bonds to provide yield support for stablecoins.

Hong Kong: Digital Transformation of Traditional Conglomerates

Hong Kong's RWA market structure is "TradFi adapted to Web3". The main sources of funding are family offices, high-net-worth individuals (HNWIs), and corporate treasuries seeking diversified wealth management. Project teams often have strong industry backgrounds (such as the mining computing power resources behind FireX, Fosun Industrial Capital behind Star Road, and real estate funds behind Asseto).

A typical example is Star Road Technology's "Web5" strategy—utilizing Web3 technology to serve existing Web2 customers. Hong Kong's RWA, on the other hand, isn't aiming to create new assets, but rather to make "old money" feel both trendy and secure.

3. Asset and Project Spectrum: Standardized Government Bonds vs. Non-Standard Structured Assets

The United States: Unilateral Hegemony over Treasury Bonds

In the US RWA market, approximately 80% of TVL (total value of liquidated assets) is concentrated in "tokenized US Treasury bonds." This is the most standard, liquid, and readily accepted collateral by DeFi protocols. Most US RWA projects focus on low transaction fees and T+0 settlement.

Hong Kong: A Testing Ground for Diversified Assets

Limited by its market size, Hong Kong cannot compete with the United States in the pure US Treasury bond market, and has therefore turned to "differentiation" and "physicalization".

Physical and Industrial RWA: FireX packages Bitcoin computing power and energy into RWA, a unique “hardcore industrial” innovation in Hong Kong that leverages Asia’s advantages in the global mining supply chain.

Real Estate & Alternative Assets: Mantra (headquartered in Dubai but with a strong presence in Asia) and Asseto focus on structuring non-standard assets such as real estate and private credit. Hong Kong is better at handling complex offline title confirmations (such as the Fosun Group assets handled by Star Road).

Infrastructureization: OSL and HashKey are not just about assets, but also about building a complete infrastructure of "exchange + custody + SaaS", which reflects Hong Kong's service-oriented nature as a financial center.

RWA's recommendations regarding mainland assets and enterprises investing in Hong Kong

Given the recent tightening of regulations, the window of opportunity for companies with mainland China backgrounds (shareholders, teams, operating entities) to issue RWAs through the "mainland assets/team + Hong Kong shell" model has essentially closed. This is not merely a matter of increased compliance difficulty, but rather a shift in nature from a "gray area" to a "high-risk criminal offense."

On November 28, 2025, a meeting of 13 departments, including the People's Bank of China, explicitly stated that stablecoins are virtual currencies and lack legal tender status, and related businesses constitute illegal financial activities. This essentially severed RWA's core "payment and settlement" function. RWA's revenue is usually settled in stablecoins (USDT/USDC), which is defined as illegal. On December 5, 2025, seven major industry associations issued risk warnings, explicitly listing RWA investment and financing as illegal activities, constituting illegal public financing, for the first time.

Under this policy environment, mainland companies face three obstacles in issuing RWAs in Hong Kong:

A. The "long arm" extension of legal jurisdiction (penetrating supervision)

The previous operating model involved setting up an SPV (Special Purpose Vehicle) in Hong Kong, while the mainland parent company only provided technical support or consulting services. This "barrier" is now ineffective.

Personal jurisdiction: Even if the issuer is in Hong Kong, if the actual controller, senior executives or technical team are in mainland China, they will be considered to be "cooperating with illegal financial activities" under the new regulations.

Aiding and abetting crimes: The December policy specifically emphasized cracking down on the entire industry chain. Mainland entities (and individuals) that provide technical development, marketing, payment settlement, or even market-making services for overseas RWA projects may be guilty of illegal business operations or aiding and abetting cybercrime under the Criminal Law.

B. "Supply interruption" on the asset side

The Hong Kong RWA market is most eager for high-quality physical assets from mainland China (such as photovoltaic power plant revenue rights and commercial real estate rentals).

Assets Leaving the Country Locked Up: Since RWA is defined as an illegal financial activity, packaging domestic assets and using RWA to finance overseas is suspected of illegal foreign exchange trading and tax evasion.

The dilemma of ownership confirmation: Domestic laws do not recognize on-chain tokens as ownership of domestic assets. If a project defaults, and overseas investors use the tokens to sue in mainland courts to demand the execution of assets, the courts will not support such claims (due to violations of public order and good morals and mandatory provisions).

C. "Blockade" on the funding side

Funds cannot be returned to the mainland for use in the real economy, even if you raise USDT/USDC in Hong Kong. This money cannot be returned to the mainland through formal banking channels for the purpose of real economic development (because banks will refuse to accept funds for "virtual currency related business").

Marketing red lines targeting mainland Chinese investors: Marketing to Chinese citizens is strictly prohibited. If your RWA Product Presentation (PPM) has a Chinese version, or if your roadshow activities involve mainland Chinese IP addresses, it will directly trigger the regulatory red line.

According to market feedback, the Hong Kong RWA market has experienced a sharp reaction since November 28. Approximately 90% of RWA consulting projects with mainland China backgrounds have been suspended or canceled, and the share prices of Hong Kong-listed companies involved in RWA (especially those with mainland China parent companies, such as Meitu, NewFire Technology, and Boyaa Interactive) have fallen sharply.

Therefore, companies with purely mainland Chinese backgrounds (Team in China, Assets in China) that still wish to participate in RWA token issuance face extremely high risks. They may not only fail to comply with regulations but also face criminal liability. It is recommended that they abandon the RWA tokenization narrative and return to traditional ABS (asset-backed securities) or issue traditional bonds in Hong Kong.

For companies that are entirely overseas (Global Team, Global Assets), it is theoretically still feasible, but it requires separation, including physical and legal separation, for example:

Personnel separation: The core team and private key controllers cannot be located within mainland China.

Asset separation: The underlying assets must be overseas assets (such as US Treasury bonds or overseas real estate), and cannot be domestic assets.

Market segmentation: Strict KYC procedures, blocking mainland China IP addresses through technical means, and no advertising or promotion on Simplified Chinese websites.

Conclusion and Outlook: Hong Kong's Path from "Frenzy" Back to "Origins"

Looking back at 2025, the Hong Kong RWA market underwent a near-brutal stress test. From the widespread attention surrounding the launch of Project Ensemble at the beginning of the year, to the frenzy of capital inflows in the middle of the year, and then to the freeze and restructuring caused by tightened regulations in mainland China at the end of the year, this process, though painful, completed a profound reshuffling of the market.

After the dust settles, the speculators who were swimming naked are eliminated, leaving behind the seven pillars we have analyzed in depth in this article:

- HashKey and OSL have upheld the bottom line of compliant transactions and custody, becoming the "water, electricity, and gas" of Hong Kong Web3;

- Star Road and Asseto have demonstrated the feasibility of traditional conglomerates using RWA to revitalize existing assets;

- FireX showcased Hong Kong's unique ability to connect physical industries (computing power/energy) with digital finance;

- Mantra and AlloyX provide the market with the necessary underlying public blockchain infrastructure and DeFi aggregated liquidity.

Looking ahead to 2026, the Hong Kong RWA market will exhibit the following three major trends:

- The shift from "domestic circulation" to "external circulation": With the tightening of capital flows from the mainland, Hong Kong will completely abandon the shady notion of "helping mainland funds go overseas." Future growth will primarily come from "global assets, distributed in Hong Kong." This means utilizing Hong Kong's compliant channels to package US Treasury bonds, Dubai real estate (as in the Mantra case), or global computing power (as in the FireX case) and sell them to institutional investors in Southeast Asia, the Middle East, and Japan and South Korea. Hong Kong will become a true "offshore financial router."

- The blurring of the lines between RWA and DeFi (CeDeFi): Simply "putting assets on-chain" is no longer profitable. The core of the next phase of competition is "composability." We will see more aggregators like AlloyX using Star Road's tokenized funds as collateral to generate stablecoins or leverage operations on-chain. Compliant CeFi assets will become the highest quality underlying "Lego bricks" for DeFi protocols.

- Stablecoins are the ultimate battleground for RWA: all RWA transactions and settlements ultimately point to currency. With the implementation of Hong Kong's stablecoin regulations, "interest-bearing stablecoins" (stablecoins backed by RWA assets) will become the largest single RWA product. Whoever controls the issuance scenarios of RWA (such as mining revenue settlement for FireX and real estate rental distribution for Asseto) will control the minting power of Hong Kong dollar/US dollar stablecoins.

The story of RWA in Hong Kong is far from over; it has only just turned the page on its "grassroots startup" phase and entered the main chapter of "institutional competition." In this new phase, compliance is no longer a burden but the greatest asset; technology is no longer a gimmick but a vehicle for trust. Hong Kong, a city that is forever evolving through crises, is redefining itself as a financial center for the digital age.