Author: Patrick , Artemis

Compiled by: Felix, PANews

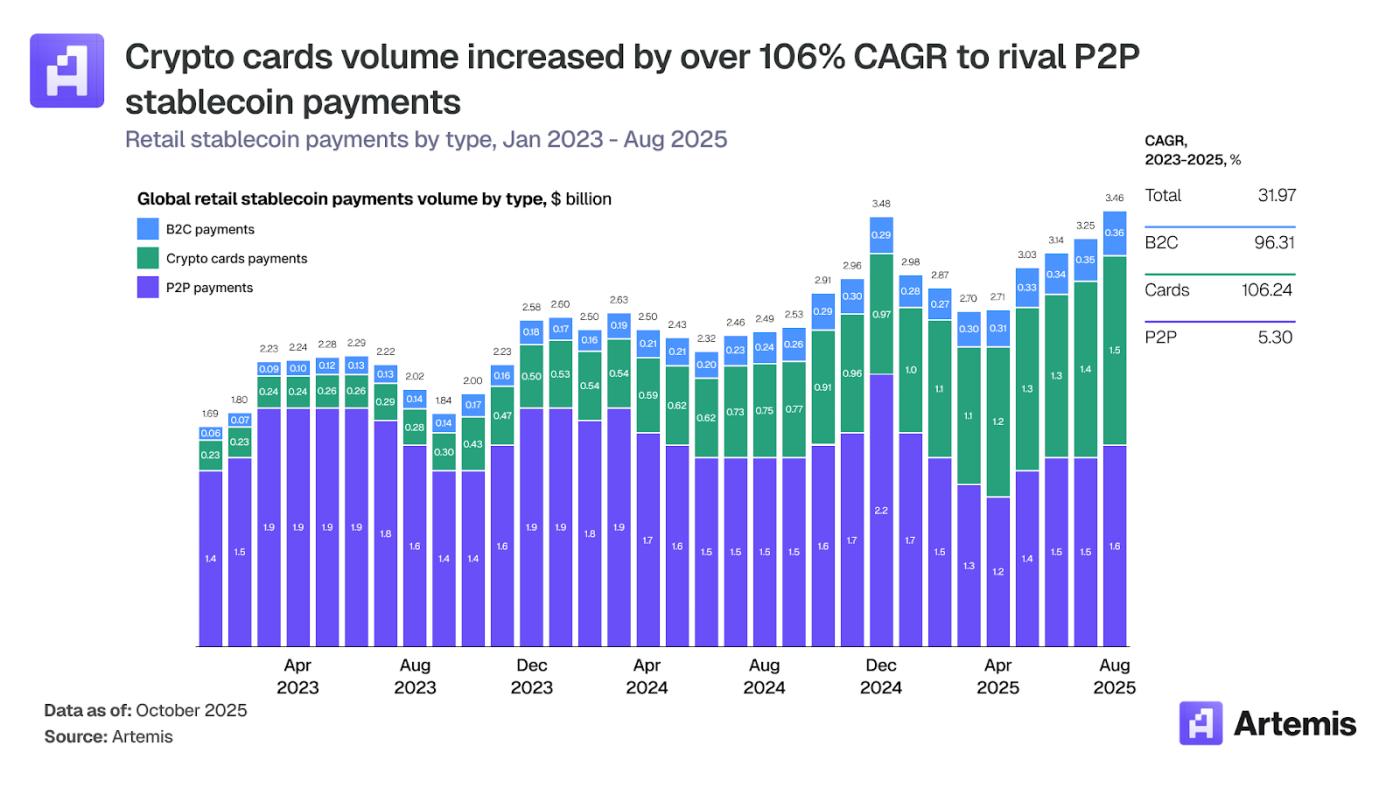

Crypto cards, which allow users to make purchases using stablecoins and cryptocurrencies at traditional merchants, are one of the fastest-growing segments in the digital payments market. Transaction volume grew from approximately $100 million per month in early 2023 to over $1.5 billion by the end of 2025, representing a compound annual growth rate of 106%. On an annualized basis, the market is now worth over $18 billion, comparable to the $19 billion in peer-to-peer (P2P) stablecoin transfers, which grew by only 5% during the same period.

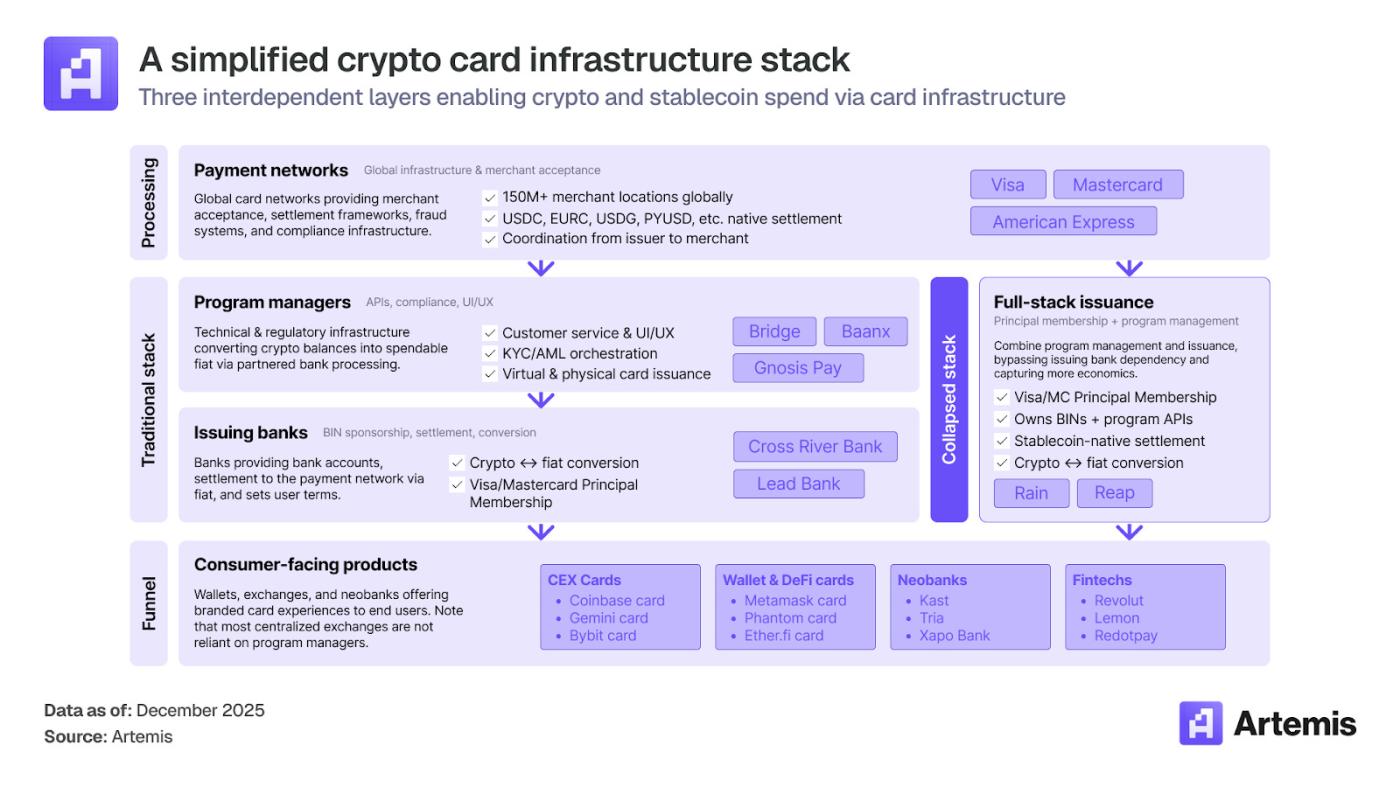

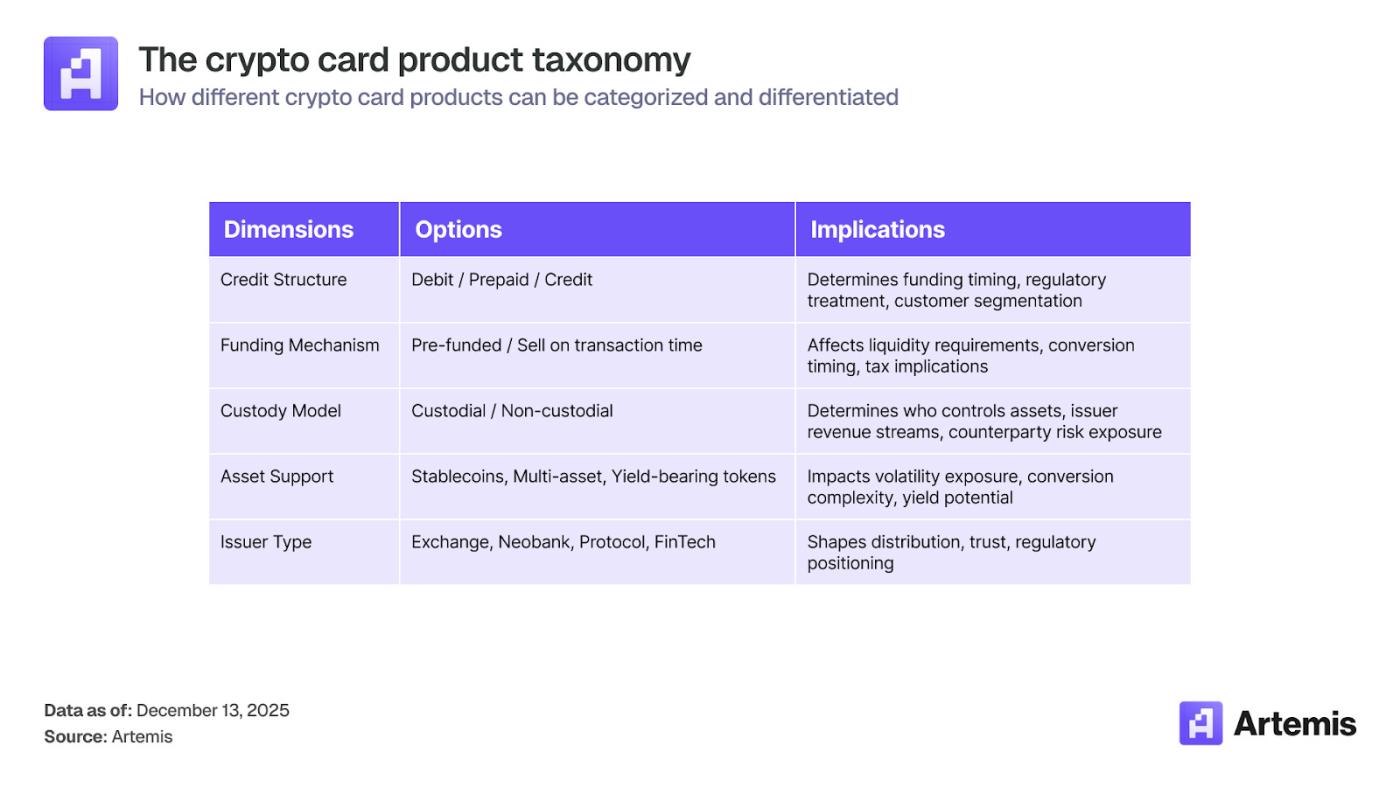

Infrastructure. The crypto card business consists of three layers: payment networks (Visa, Mastercard), card program managers and issuers, and consumer-facing terminal products. While Visa and Mastercard have nearly the same number of card programs (both over 130), Visa, through its early partnerships with infrastructure providers, accounts for over 90% of on-chain card transaction volume. The most significant structural development is the emergence of full-stack issuers—companies like Rain and Reap, which directly own memberships and combine program management with card issuance, bypassing dependence on traditional issuing banks and thus capturing more revenue per transaction.

Geographic factors. Opportunities for stablecoin cards are concentrated where stablecoins can solve real-world problems. India (with $338 billion in cryptocurrency inflows) and Argentina (USDC accounting for 46.6%) are global exceptions. India's opportunity lies in cryptocurrency-backed credit cards (the Unified Payments Interface (UPI) has commoditized debit cards); Argentina's opportunity lies in stablecoin debit cards for hedging against inflation (currently, there are no competing digital payment methods). For developed markets, the opportunity lies not in addressing unmet needs, but in attracting differentiated, high-value user groups whose services cannot be optimized by traditional products.

Looking ahead, merchants directly accepting stablecoins face significant launch challenges: no established user base, no exclusive inventory, and no better solution for the average Western consumer or merchant than credit cards. All successful payment networks in recent years started with exclusivity or mandatory features—stablecoin payments offer neither. The real opportunity lies not at the point of sale, but in the behind-the-scenes settlement process. Stablecoin-backed bank cards represent a fusion of the two: bank cards offer universal acceptance; stablecoins provide cross-border value storage. Developers recognizing this will focus on the integration level, rather than using technology to combat behavioral economics.

Crypto cards are the infrastructure for the next phase of stablecoin adoption: stablecoins can store value anytime, anywhere, while bank cards can be used for spending anywhere.

I. What is an encrypted card?

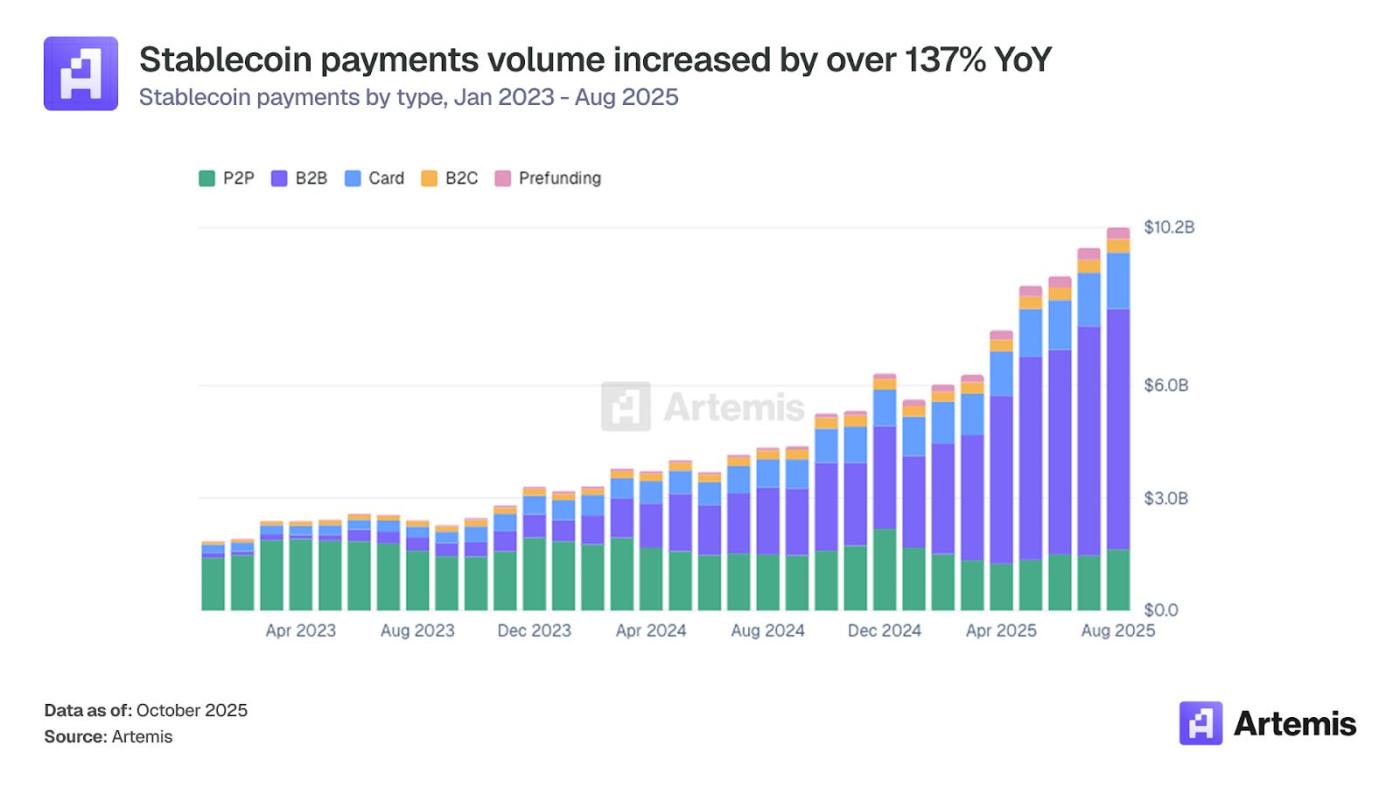

Stablecoin payments have entered a new growth phase. Monthly transaction volume increased from $1.9 billion in January 2023 to $10.2 billion in August 2025, driven by continued demand for stablecoin payments in emerging markets, improved user interfaces/user experiences, and increasing institutional acceptance of stablecoin payment channels.

Since January 2023, crypto card transaction volume has grown at a compound annual growth rate of 106%, reaching an annualized transaction volume of $18 billion, while P2P stablecoin transfers have only grown by 5% during the same period, with an annualized transaction volume of $19 billion. Crypto card transaction volume has grown from a fraction of retail transaction volume to a level comparable to P2P transaction volume.

1.1 What is an encrypted card?

A crypto card is a type of payment card—prepaid, debit, or credit—that allows users to make purchases using cryptocurrencies or stablecoins at traditional merchants through existing card network infrastructure. When users hold stablecoins in their wallets or Bitcoin on exchanges and want to buy coffee, pay rent, or shop online, a crypto card connects these digital assets to a global network of merchants that accept Visa and Mastercard.

1.2 Transaction Process Mechanism

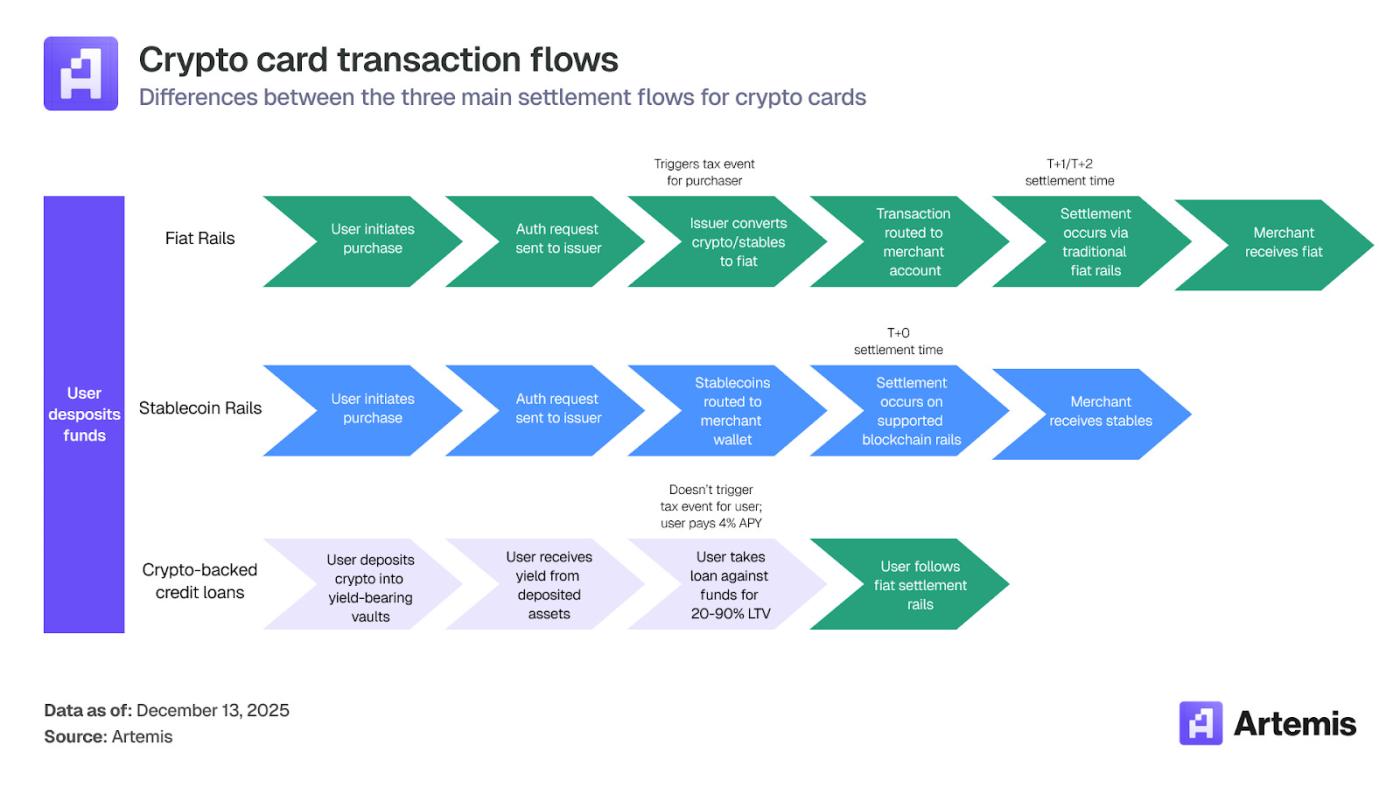

When a user swipes an encrypted card at a merchant terminal, what happens to the funds? The answer depends on the card's underlying infrastructure. Currently, there are three settlement processes in the market, each with a different technical architecture, counterparty relationships, and different impacts on the broader payment ecosystem.

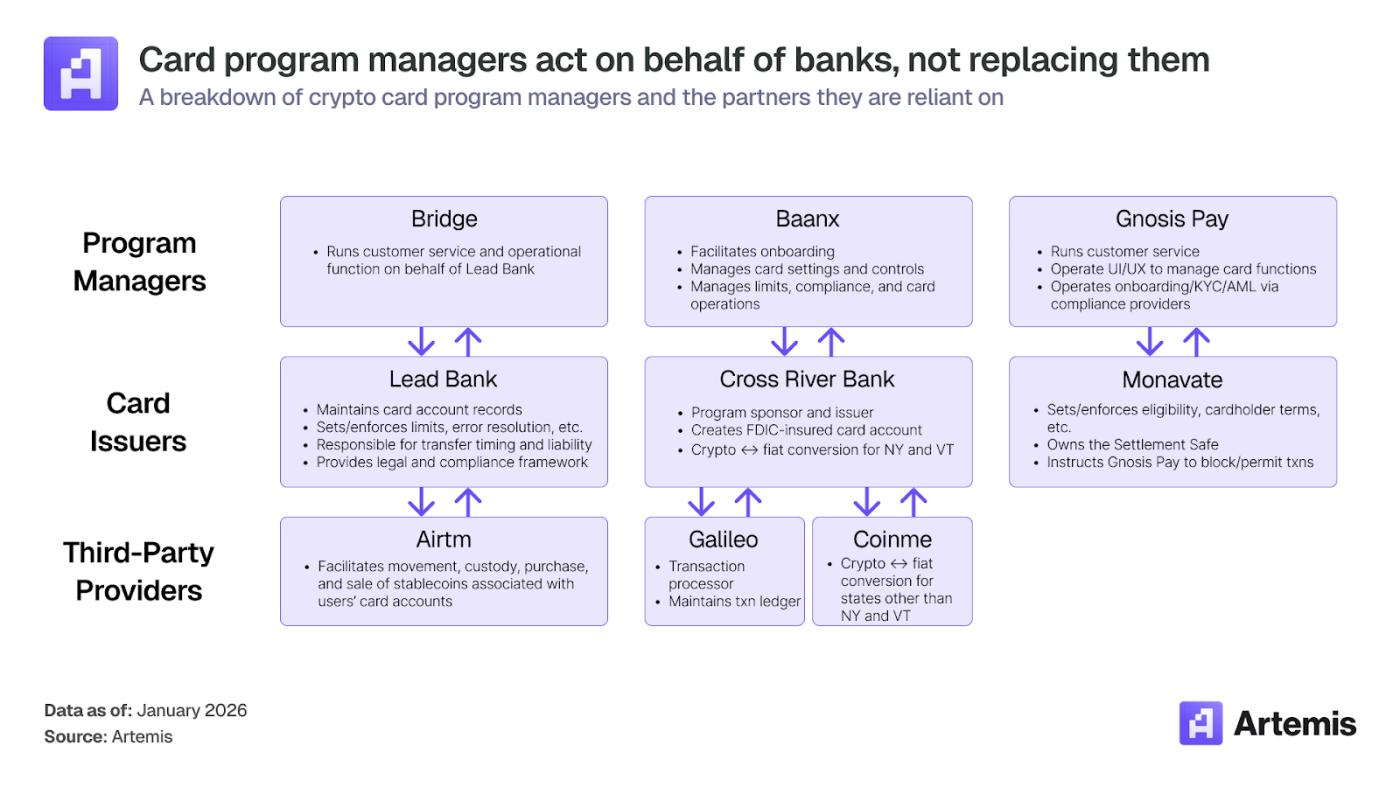

Currently, the vast majority of crypto card transactions are settled in fiat currency. This remains the default option because it requires no merchant integration. The cryptocurrency-to-fiat conversion occurs before settlement to the payment network, so when the transaction arrives at the network, it is no different from any other card payment. It's worth noting that typical project managers like Baanx's Crypto Life and Bridge do not handle settlement to their designated payment networks; instead, they partner with issuing banks such as Lead Bank and Cross River Bank, respectively, who handle the settlement. Full-stack issuing platforms like Rain settle by clearing stablecoins or crypto assets to the Visa network, which then routes the funds to the acquiring bank in the required fiat currency. From the merchant's perspective, there is no change for the vast majority of crypto card usage.

Stablecoin settlements are growing rapidly, but are still in their early stages. It is estimated that Visa's stablecoin-related card spending reached an annualized rate of $3.5 billion in the fourth quarter of fiscal year 2025, representing a year-over-year increase of approximately 460%, but still only accounting for about 19% of total crypto card settlements.

1.3 Infrastructure Stack: Three-Tier Architecture

The infrastructure stack of an encryption card can be divided into three core layers, each of which is interdependent.

First layer: Payment network

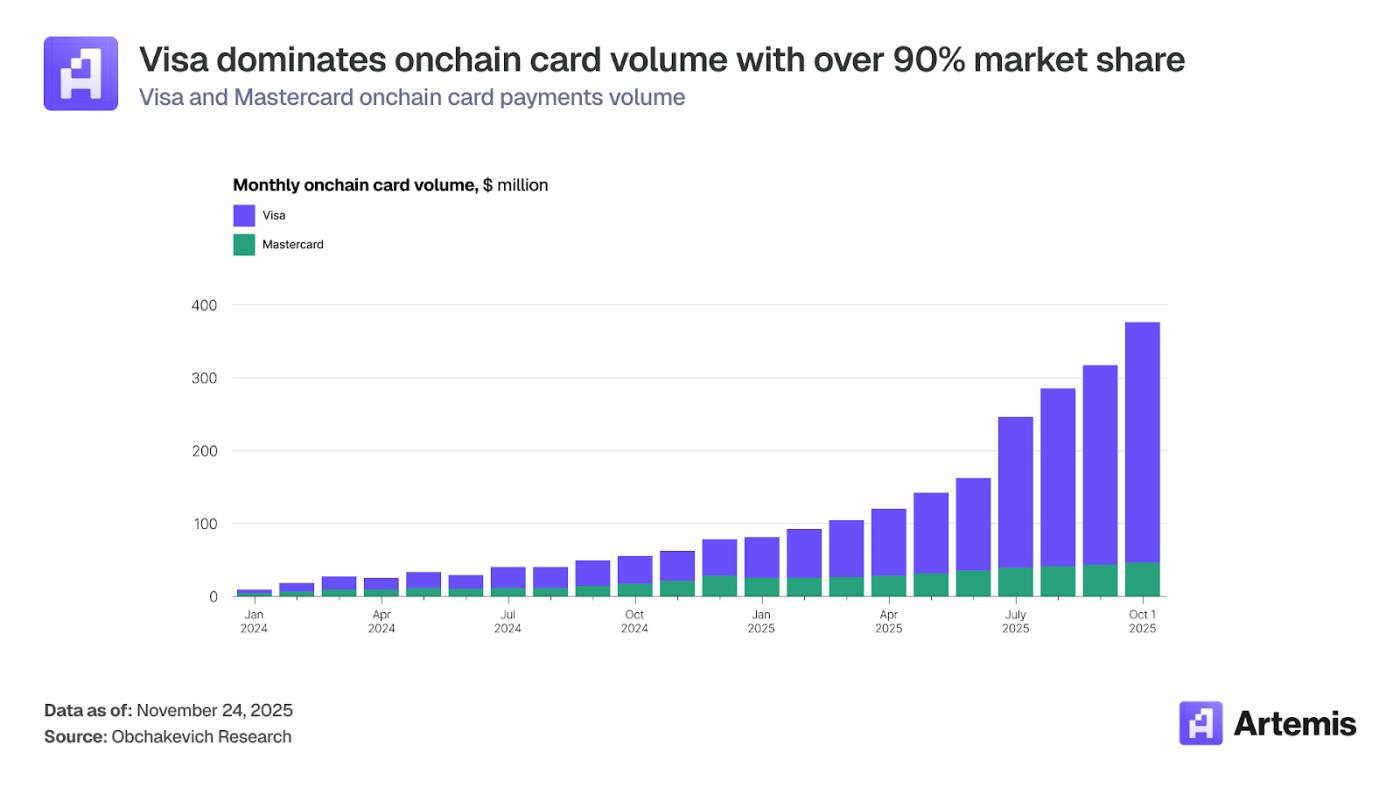

According to a Nilson report, as of 2024, Visa and Mastercard controlled over 70% of the card network payment infrastructure market share. In the crypto card industry, their current market share may be close to 100%, with a few exceptions such as the Coinbase One card issued by American Express.

Although the number of payment items is similar for both companies, Visa's share of on-chain transaction volume far exceeds that of its competitor. This difference reflects their different market strategies.

Visa's strategy has consistently revolved around establishing partnerships early with emerging project managers such as Rain, Reap, and other infrastructure providers to quickly capitalize on the entry of new crypto-native card issuers into the market. These partnerships allow Visa to access dozens of downstream card products through a single integration, enabling it to rapidly scale its business as new projects emerge.

In contrast, Mastercard has consistently focused on establishing direct partnerships with centralized exchanges (CEXs). Revolut, Bybit, and Gemini all operate Mastercard-branded card programs. This strategy allows Mastercard's crypto card trading volume to be more closely tied to the exchange's user base and trading activity cycles.

Importantly, their strategies are not mutually exclusive, and these networks often compete with each other within the same card issuer's customer base.

- Bybit's global debit and prepaid cards use Mastercard, but in the Asia-Pacific region, its credit card products are offered in partnership with Visa.

- Mastercard is also a major network provider for Crypto Life, a subsidiary of Baanx. Crypto Life is a white-label project management company that supports products such as MetaMask and Ledger cards.

Visa's dominance suggests that controlling the infrastructure layer may be more efficient than partnering with individual exchanges one by one.

Second layer: Card issuance infrastructure

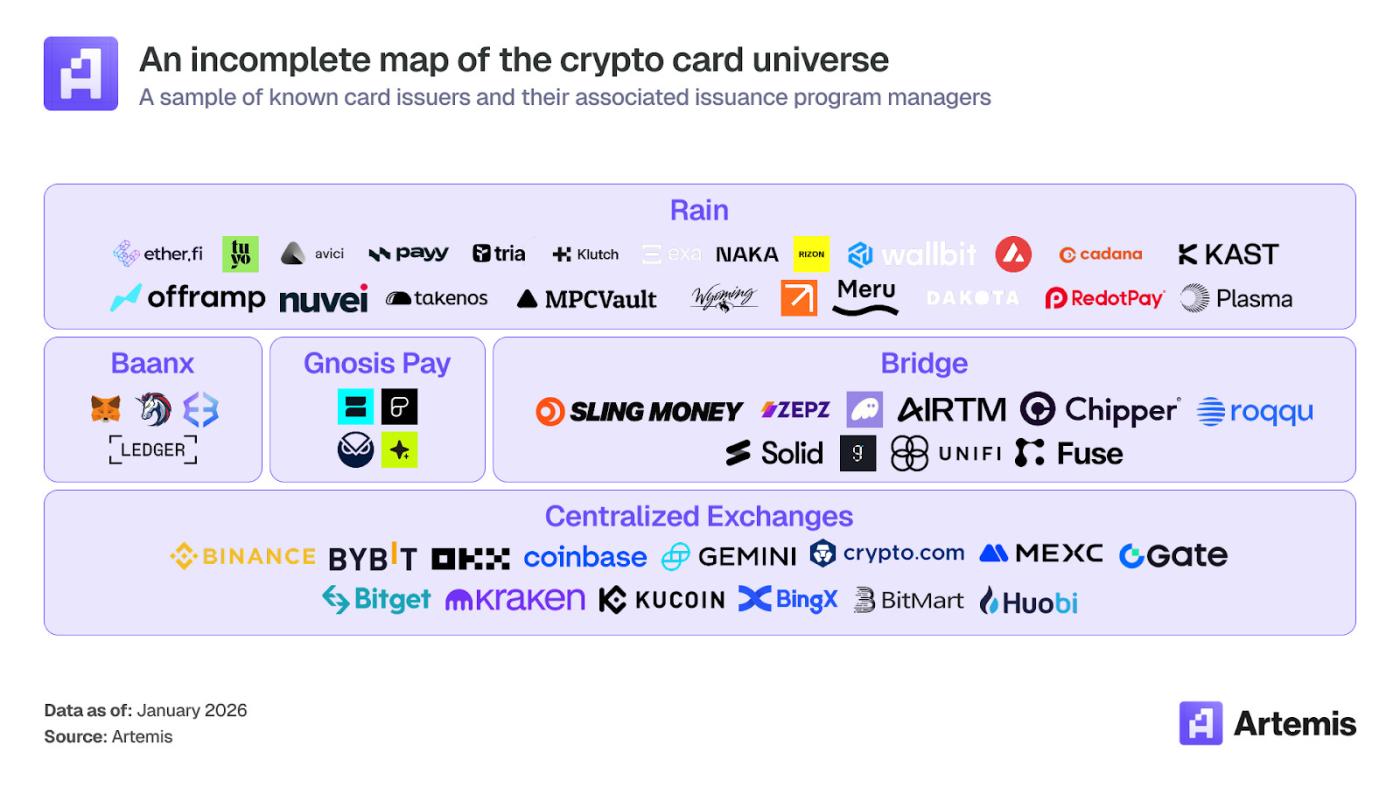

Specialized platforms provide technical and regulatory infrastructure for card projects. These platforms can be divided into two main categories: project management platforms and full-stack card issuance platforms.

Project management platforms typically partner with issuing banks holding primary Visa or Mastercard memberships to manage BIN sponsorship relationships, handle compliance requirements, and operate the settlement system from the user-created bank account to the required payment network. Each project management platform is responsible for converting crypto assets or stablecoins held in the user's linked digital wallet into fiat currency, making it compatible with the issuing bank's settlement infrastructure. Project management platforms offer white-label functionality, enabling other companies to launch their own branded card products. Examples of these white-label card project management companies include Baanx, Bridge, and Gnosis Pay.

In contrast, full-stack card issuance platforms like Rain and Reap integrate these various services into a single, unified service. These "Cards-as-a-Service" platforms demonstrate how infrastructure providers are preparing for the future of stablecoin-native applications.

As a key member of Visa, Rain and Reap enable direct card issuance on the Visa network without intermediaries. Rain uniquely leverages the significant value that typically flows to banks and other intermediaries by integrating existing card issuance processes—primarily involving BIN guarantees, acting as a record lender, and direct settlement to the Visa network—into a single product.

For white-label project managers, the broader significance lies in the fact that as stablecoin settlement volumes expand and regulatory frameworks mature, infrastructure providers with major memberships and native settlement capabilities will become key channels for next-generation card issuance. Project managers can adopt a capital-light model, scaling with the ecosystem's growth and acquiring transaction volume across dozens of downstream products without incurring high customer acquisition costs. However, full-stack card issuance platforms are likely to retain their largest clients and continue to erode the market share of existing players.

Third layer: Consumer-oriented products

The consumer tier encompasses card products that users actually interact with, including downloaded apps, cards in wallets, and brands associated with cryptocurrency spending. This tier can be further subdivided into four distinct categories, each with different strategic motivations, user groups, and business models.

Category 1: CEX Card

- Coinbase Card, Crypto.com Card, Bybit Card, Binance Card, Gemini Card, Krak Card

- Integrated with exchange wallets; typically prepaid cards or debit cards; if they are credit cards, they function similarly to regular credit cards, allowing payments from bank accounts or associated exchange holdings and cashing out in cryptocurrency.

Category 2: Self-hosted/Protocol Native Card

- Ether.fi Cash, MetaMask Card, Phantom Card

- Users hold assets before making a purchase.

- Typically integrates DeFi yields or collateralized lending.

Category 3: Crypto-native New Banks

- KAST (based on Solana), Offramp (based on Tron), Xapo Bank (based on BTC)

- A complete banking experience built around cryptocurrency

- Targeting crypto-native users seeking key banking relationships

Category 4: Traditional Fintech New Banks

- Revolut (EU, India, etc.), Chime (USA), N26 (EU)

- Adding cryptocurrency functionality to existing fintech platforms

II. Fund Operation

2.1 Who drives the fund operation?

Incentives for driving the adoption of crypto payment cards vary across ecosystems, but can generally be categorized into three strategies.

① Exchanges and DeFi protocols: Cards as user acquisition channels and profit layers

For centralized exchanges (CEXs) and DeFi protocols, issuing credit cards is essentially a distribution strategy. The cards act as an incentive mechanism, guiding users to a wider platform and enabling companies to convert everyday spending into platform engagement, and ultimately, profitable balances.

In this model, rewards programs effectively become a customer acquisition cost (CAC) tool. The platform subsidizes cardholders through cashback programs, offsetting this expense through subsequent user deposits and floating balance sheet earnings. The level of subsidy varies depending on the business model.

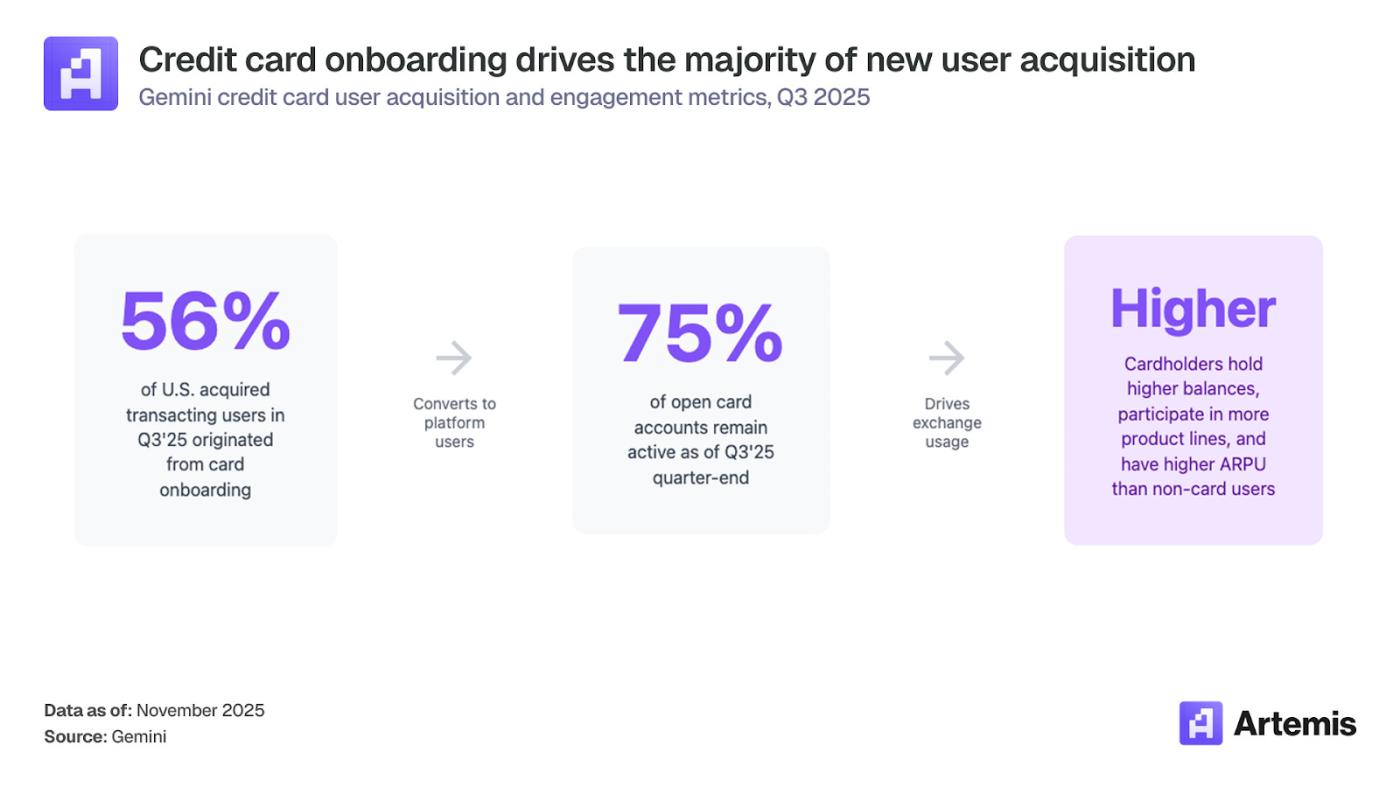

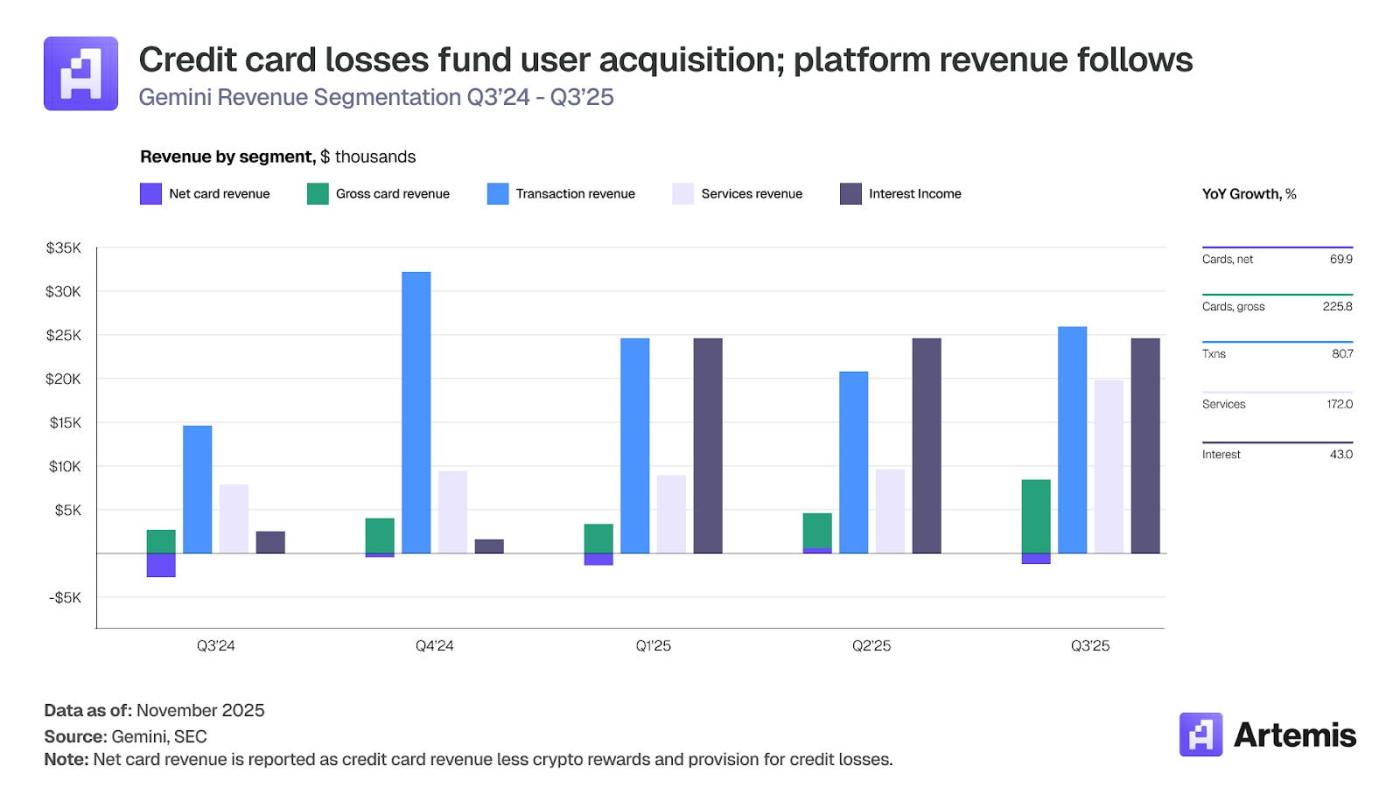

CEXs that pay rewards in fiat currency or highly liquid cryptocurrencies (such as Gemini, Coinbase, and Kraken) incur actual USD costs and must rely on transaction fees, interest income, and asset returns to offset customer acquisition costs. Following its acquisition of Blockrize in January 2021, Gemini launched a credit card program with cryptocurrency cashback rewards in 2022. Despite continued losses in its credit card business (see the purple section in the chart below showing net credit card revenue), Gemini continues to invest in and operate its credit card product due to its strong performance in user acquisition and retention.

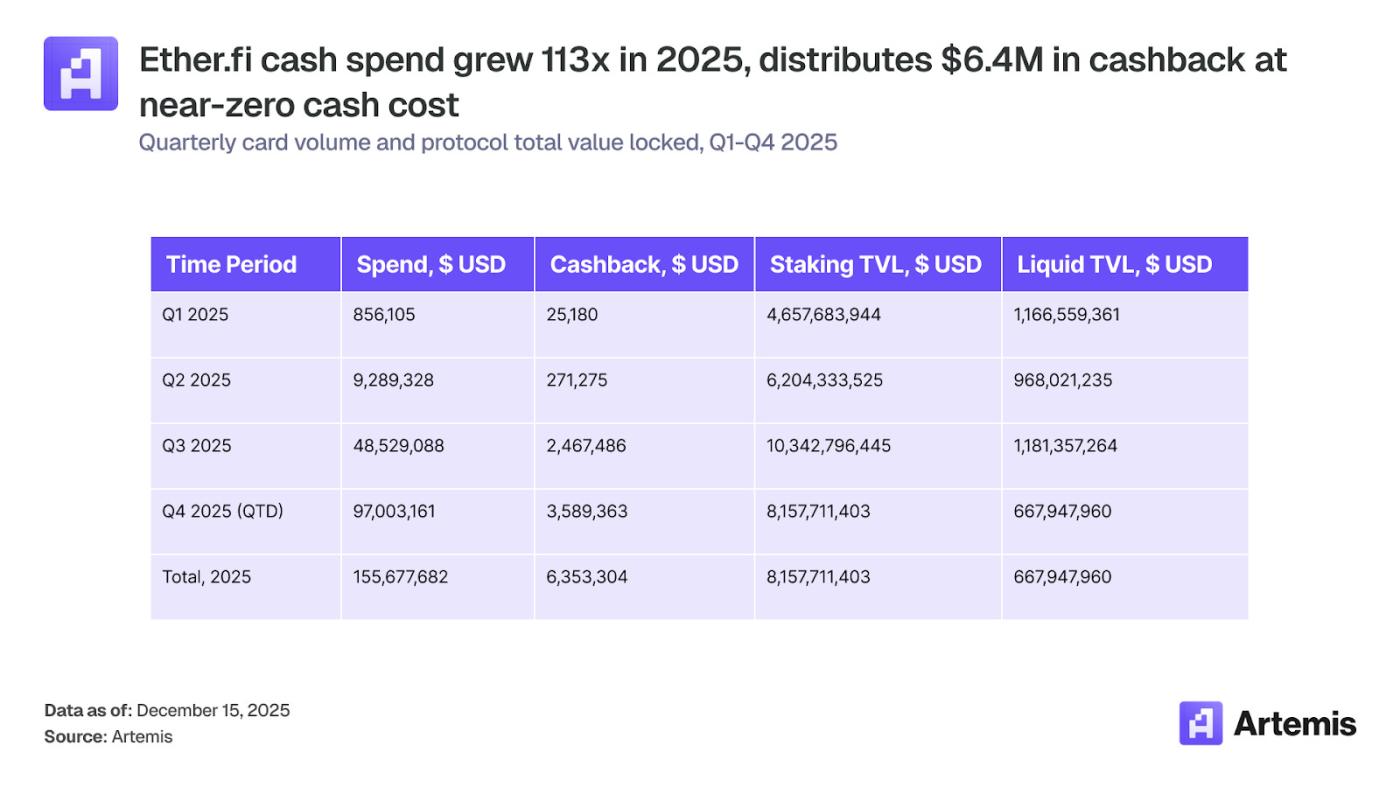

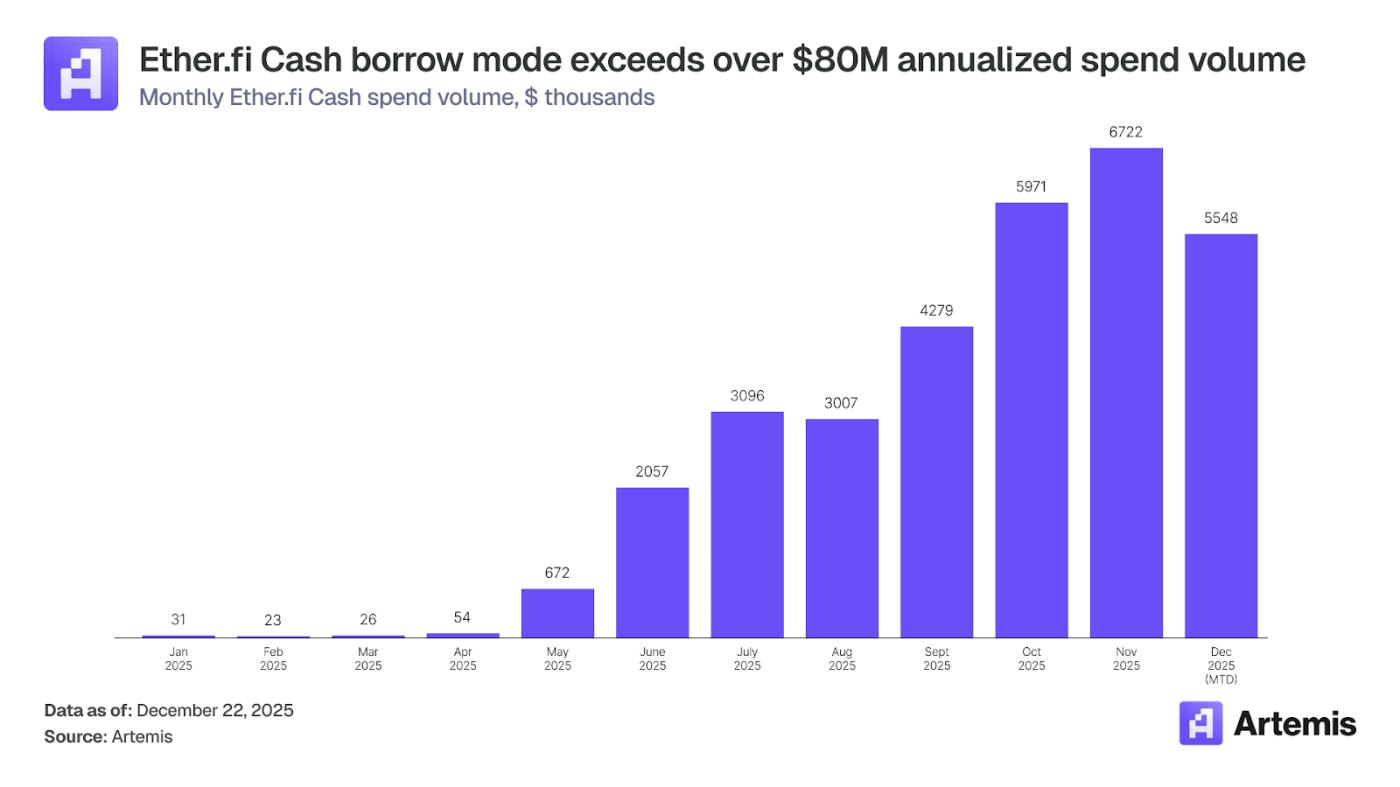

It's worth noting that outside of centralized exchanges (CEXs), there are many different reward program designs to choose from to attract users. Token-incentivized platforms (such as Ether.fi paying rewards with $SCR, and NewBank rewarding users with native tokens) have near-zero marginal costs for rewards, thus enabling them to offer higher cashback rates without consuming large amounts of capital. Ether.fi Cash's average cashback rate is approximately 4.08%, higher than the "up to 4% cashback" offered by many CEXs.

Users of Ether.fi Cash who enable the "lending mode" deposit ETH as collateral into Ether.fi's staking or liquidity vault products to increase the protocol's TVL and management fee revenue. Although Ether.fi's TVL has fluctuated with the overall market this year, its structural flywheel effect remains: bank cards drive deposits, deposits drive TVL, and TVL drives fee revenue.

② Crypto-native wallets: Increasing average user income by issuing payment cards

Unlike exchanges and DeFi protocols, which primarily use payment cards as a customer acquisition tool, native crypto wallets and fintech platforms issue payment cards for entirely different reasons. Due to fundamental differences in their business models, their motivations are also vastly different.

Self-custodial wallets like MetaMask and Phantom boast a large global user base but lack the ability to generate custody rewards. They cannot earn interest on deposits, re-collateralize customer assets, or participate in staking rewards without the user's explicit consent. Consequently, their revenue streams are concentrated on highly cyclical activities—primarily transaction fees, cross-chain bridge inflows, and partner integration revenue.

For wallets, payment cards offer a highly attractive monetization model. Transaction fees and subscription fees provide diversified revenue streams, while the use of payment cards deepens user engagement and reduces churn. Cards enable wallets to convert sporadic crypto activity into habitual spending, thereby increasing average revenue per user (ARPU) and improving user retention. By partnering with project management organizations to issue cards, wallets can deploy cards with minimal regulatory burden while still profiting from users' on-chain and off-chain activities.

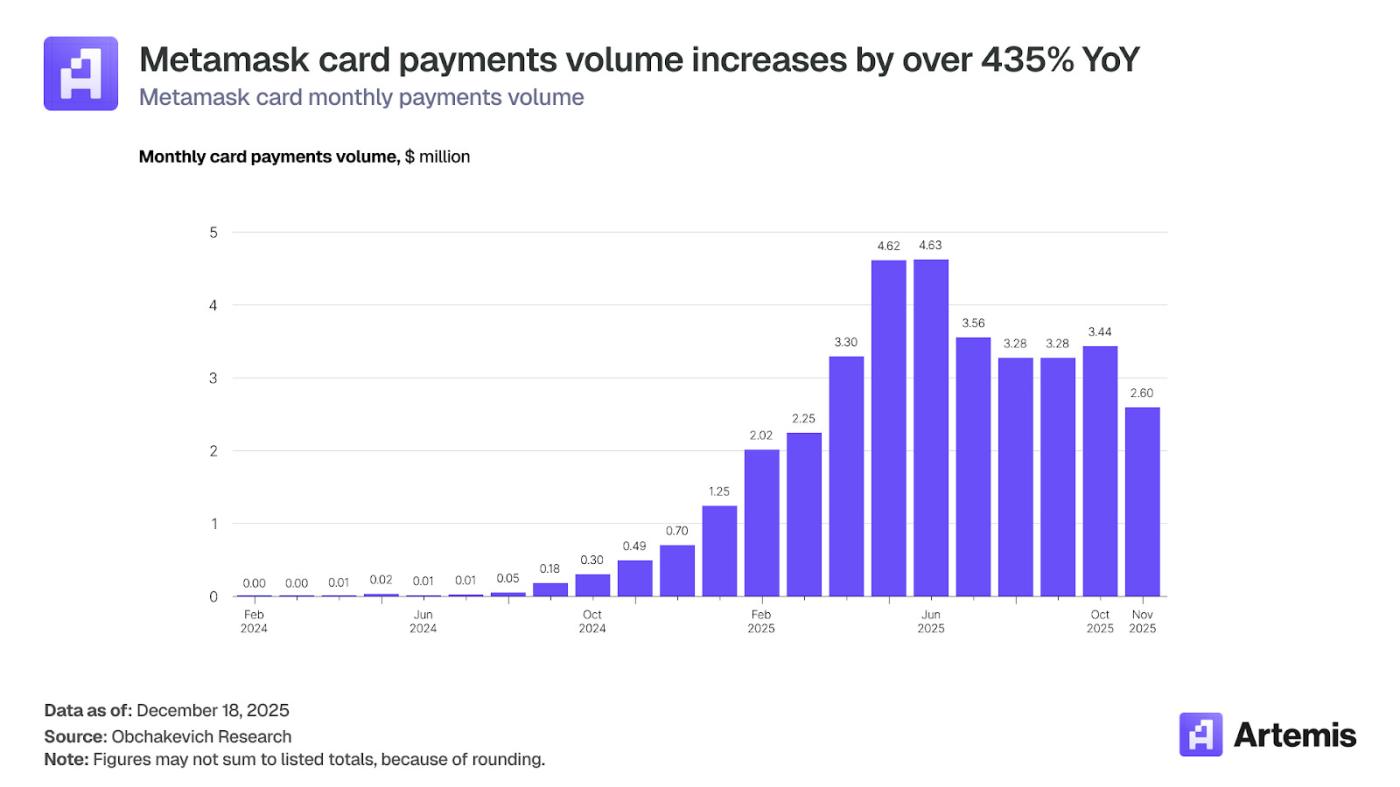

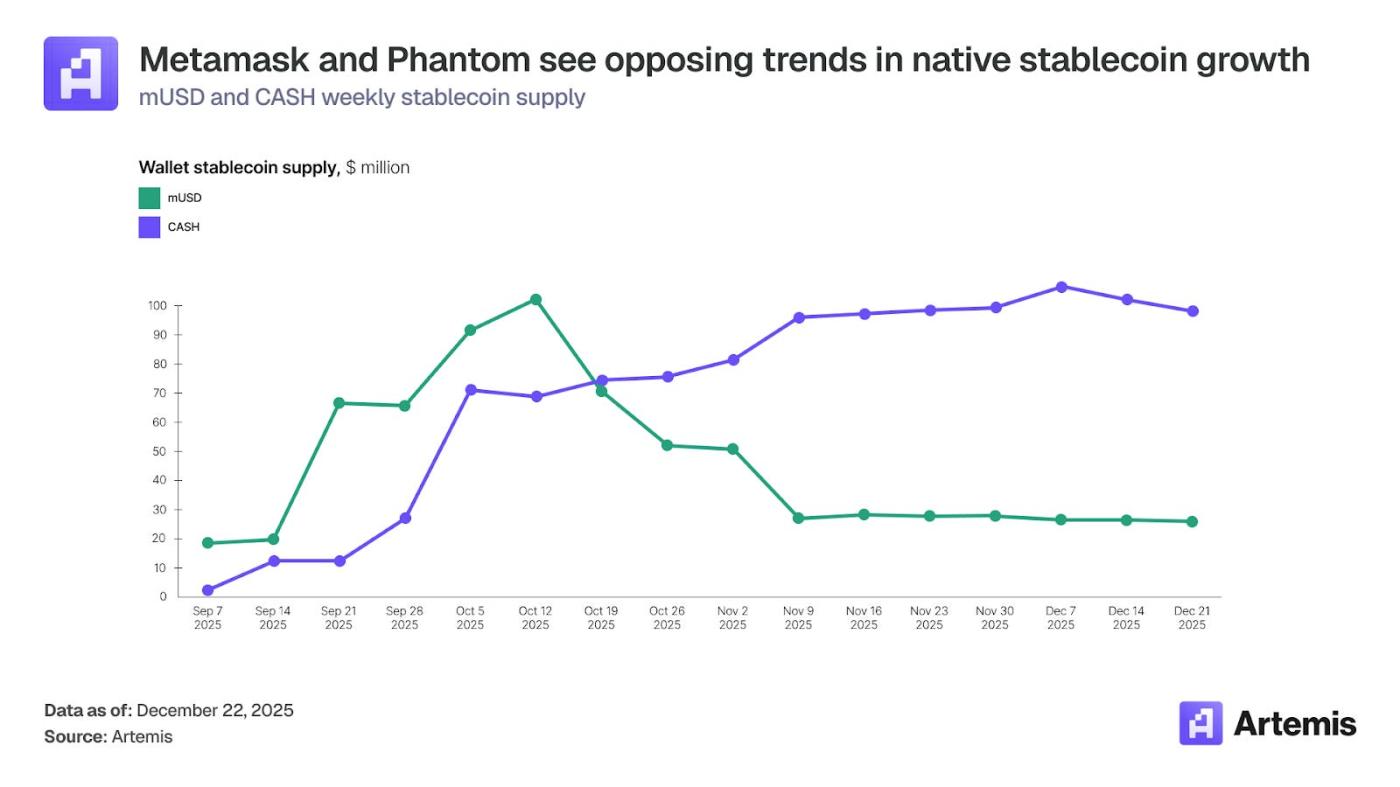

Beyond revenue directly related to card usage, some of the world's largest wallet providers have also begun issuing their own stablecoins. At the end of Q3 2025, MetaMask and Phantom launched their native stablecoins, $CASH and $CASH, respectively, specifically to fund their respective debit card products. These wallets no longer rely on users holding USDC or USDT; instead, they have built closed ecosystems where users can convert their assets into the wallet's native stablecoin for spending.

Early data showed that the two companies followed drastically different trajectories. Phantom's mUSD supply steadily increased from approximately $25 million in September to approximately $100 million by the end of December, indicating consistently stable user acceptance and retention. In contrast, MetaMask's mUSD briefly approached $100 million in early October before falling back to approximately $25 million, a drop of 75%.

The introduction of native stablecoins brings numerous benefits to wallet providers:

- Vertical integration: Controlling the stablecoin layer can capture additional profits that would otherwise flow to Circle (USDC) or Tether (USDT).

- Ecosystem lock-in: Users holding mUSD or CASH are less inclined to switch wallets. Stablecoins become a retention mechanism, further increasing ARPU.

The divergent development trajectories of mUSD and CASH highlight a strategic question related to card issuance: when should wallets launch native stablecoins to support their card products, and when should they allow users to top up their cards using existing stablecoins?

For card products, integration should be the default option. Cards topped up with USDC function well: users are likely to hold USDC, liquidity is ample, and the settlement infrastructure already supports USDC.

Adding a proprietary stablecoin layer introduces friction, artificially satisfying non-existent demand. For wallet providers, stablecoins might solve bank card issues, but they shouldn't exist as a separate profit-generating layer.

③ Emerging markets and “last mile” access service providers

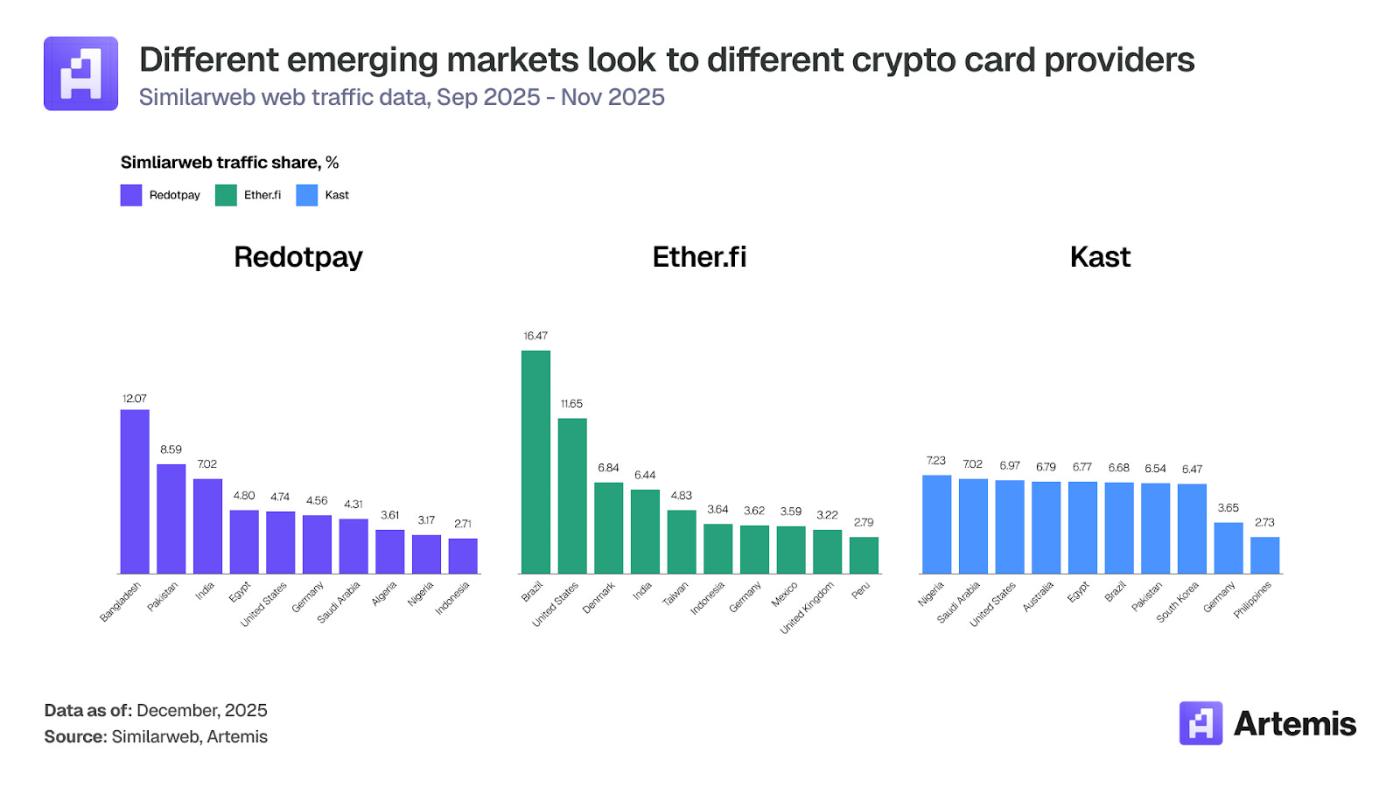

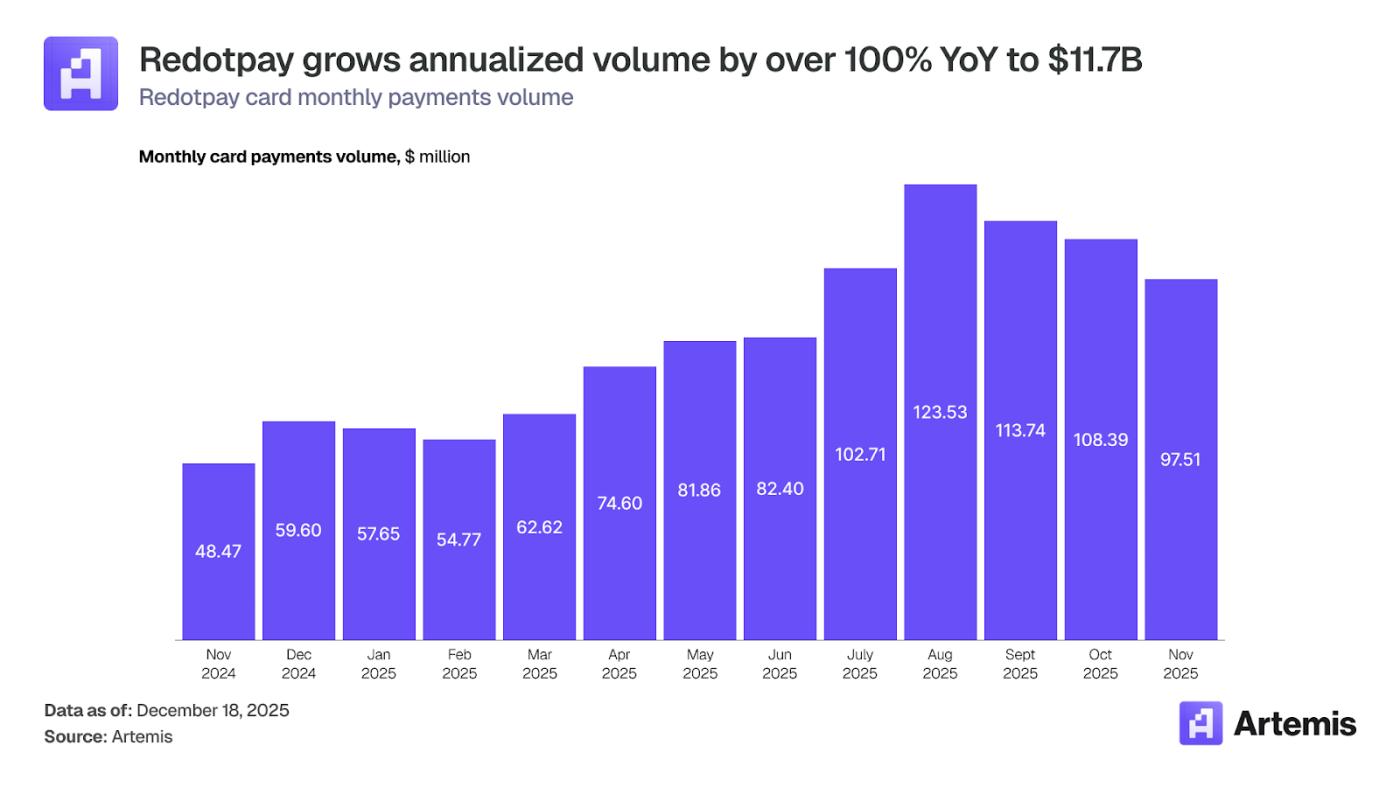

In Latin America, Europe, the Middle East, Africa, and Southeast Asia, a unique category of fintech companies views cryptocurrency-linked cards as the infrastructure for accessing digital dollars. These companies target individuals facing severe financial frictions: inflated local currencies, capital controls, unreliable banking infrastructure, and high costs of cross-border payments. Companies like Redotpay, Kast, and Holyheld are working to provide crypto cards for these users.

In these contexts, stablecoin-linked cards address a structural market need. They allow users to hold savings in the form of assets pegged to the US dollar, circumvent local foreign exchange restrictions, and access global merchants without having to interact with volatile domestic banking systems. For many consumers, cryptocurrency-linked cards represent a viable pathway to financial stability.

These card issuers also have different economic models. They do not rely on transaction revenue or custody fees, but rather generate profits through the following methods:

- Foreign exchange spread

- Cryptocurrency to fiat currency conversion fee

- Merchant and cross-border transaction fees

- Exchange income

Their strategy is to provide “last-mile” financial services. In this way, they are able to capture most of the value created in the informal dollarization process in these regions through specific credit card fees.

2.2 Where did the funds go?

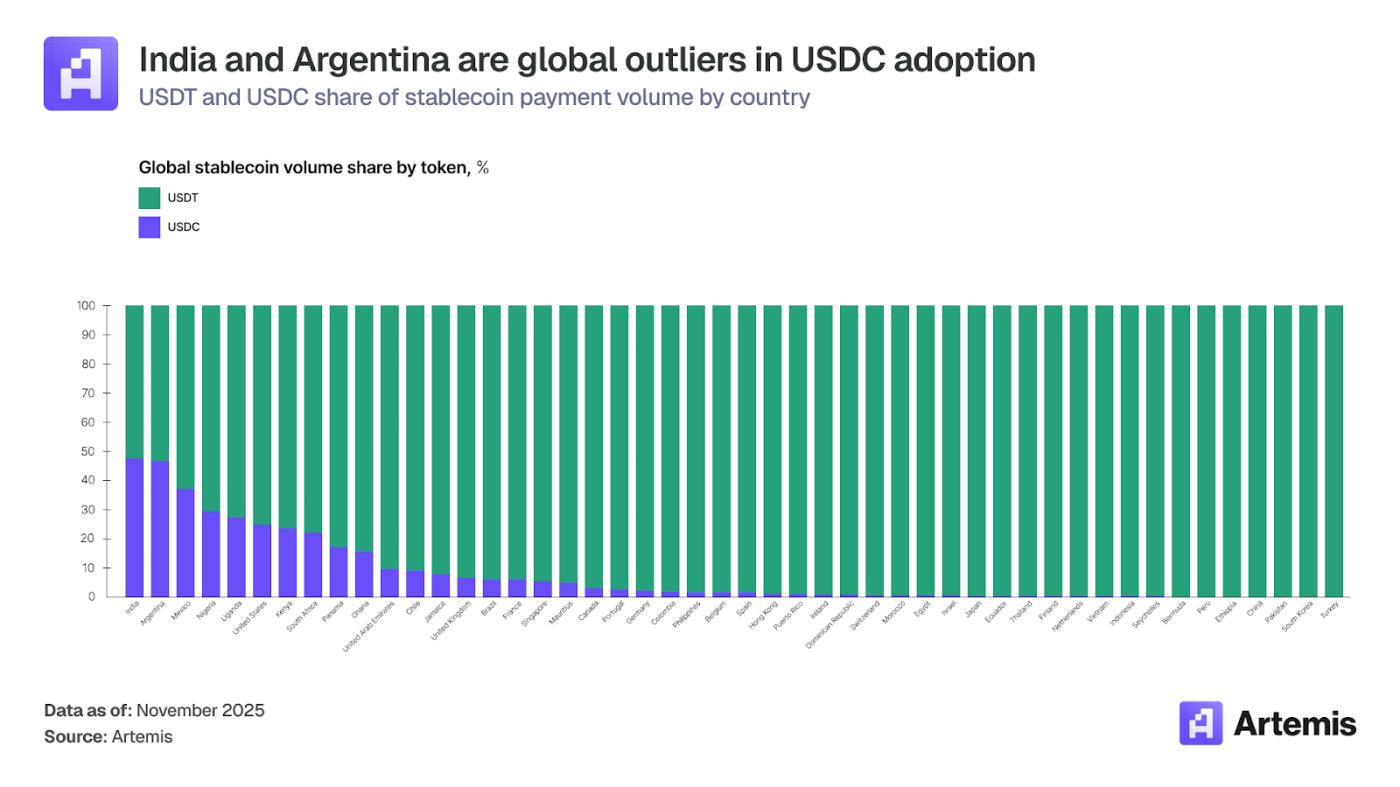

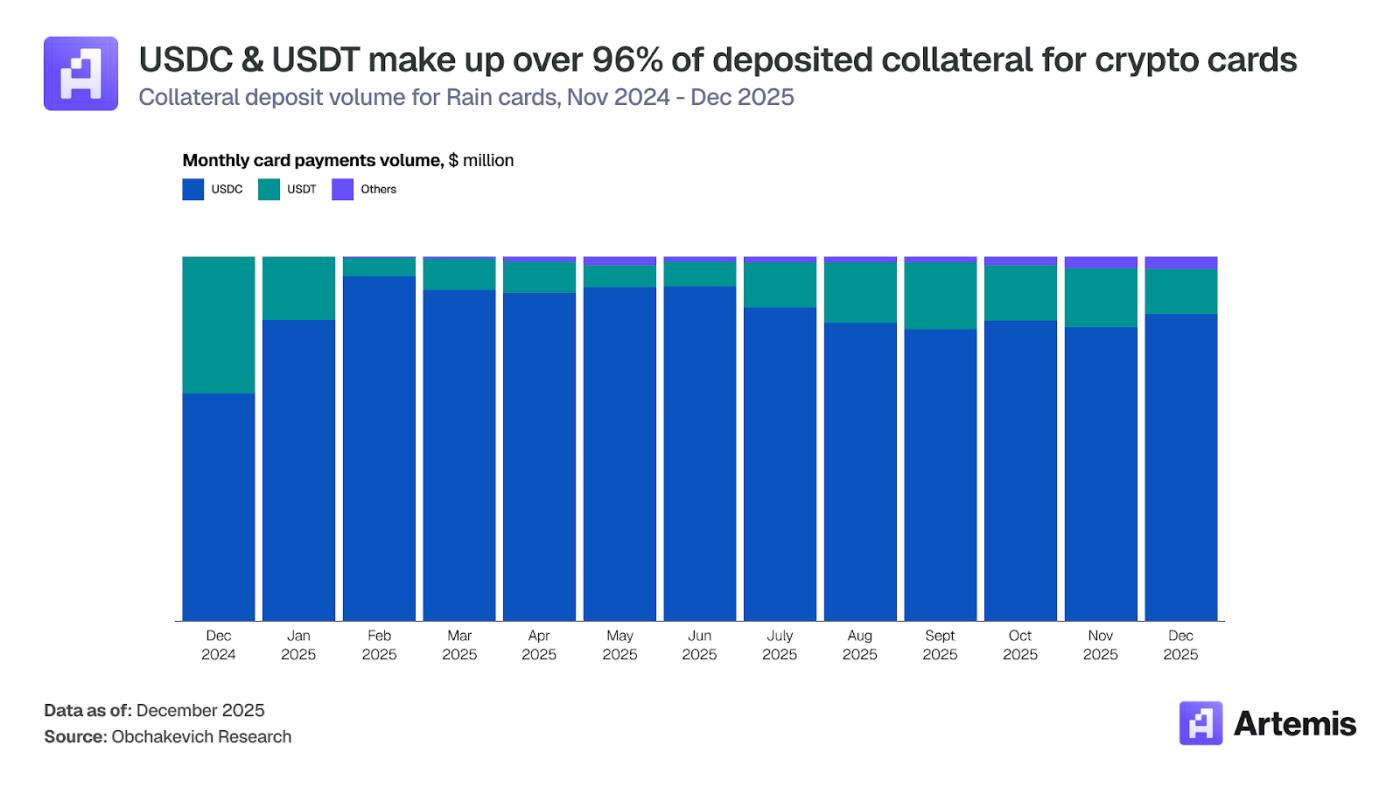

As more merchants accept native stablecoins for payments, understanding where stablecoin-denominated business activities actually occur and which tokens dominate these payment flows becomes crucial. Native stablecoin settlement—where card networks settle directly in stablecoins rather than fiat currencies—offers advantages in speed, availability, and counterparty risk. Visa and Mastercard's native stablecoin settlement networks support only a few regulated stablecoins: USDC, USDG, PYUSD, and EURC, while Mastercard also supports FIUSD. Notably, USDT, the world's largest stablecoin by market capitalization and trading volume, is absent, its regulatory uncertainty preventing its access to mainstream native stablecoin settlement networks.

However, the combination of stablecoins is far less important than it seems. Today, the vast majority of crypto card transactions are ultimately settled in fiat currency, regardless of the cryptocurrency or stablecoin held by the user. The user's stablecoins are converted to local fiat currency at the time of the transaction; merchants only see the local currency. The fact that USDT is not included in the native settlement system does not mean that markets with a high proportion of USDT cannot use crypto cards.

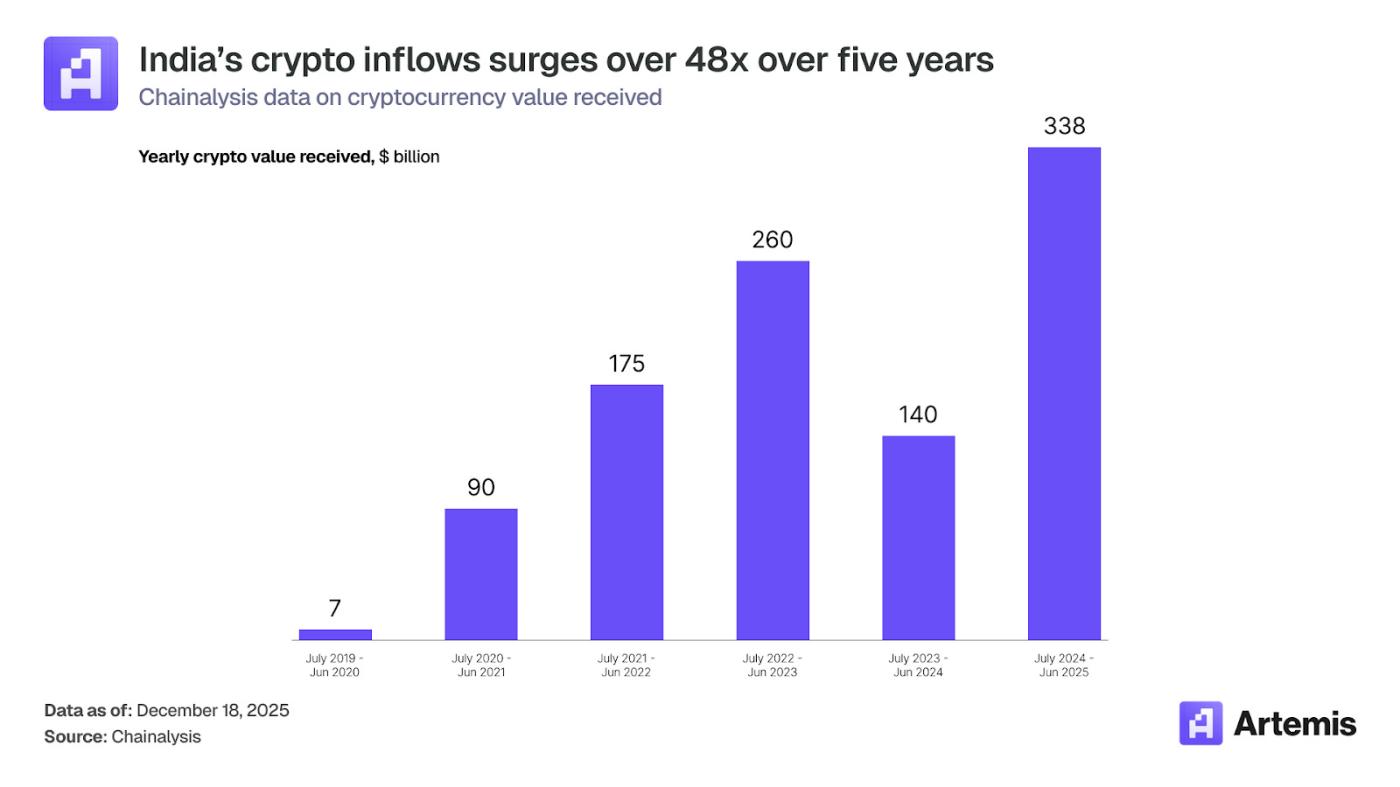

In almost all markets, USDT dominates stablecoin trading volume. However, two countries stand out as notable exceptions: India (47.4% USDC) and Argentina (46.6% USDC), where USDC usage is nearly equal to USDT. Both countries possess significant potential in the crypto card market, but their natures are fundamentally different.

In the 12 months ending June 2025, India became the largest crypto market in the Asia-Pacific region with $338 billion in inflows, a 48-fold increase in five years. However, such a massive volume of transactions is almost entirely outside the formal financial system, creating the world's largest "debanking" gap—a huge divide between actual cryptocurrency activity and regulated, compliant channels.

India's 2022 amendments to the Income Tax Act imposed a flat 30% tax rate on income earned by individuals and businesses from cryptocurrency transactions, along with a 1% withholding tax (TDS) on all transfers. As a result, much of India's crypto activity shifted overseas. The Indian Ministry of Finance reported that in the 2024-2025 fiscal year, crypto exchage withheld only $5.67 million in taxes, and crypto transfers through registered virtual digital asset providers totaled only about $567 million. This indicates a significant potential demand for compliant crypto products, with regulation being the limiting factor rather than user interest.

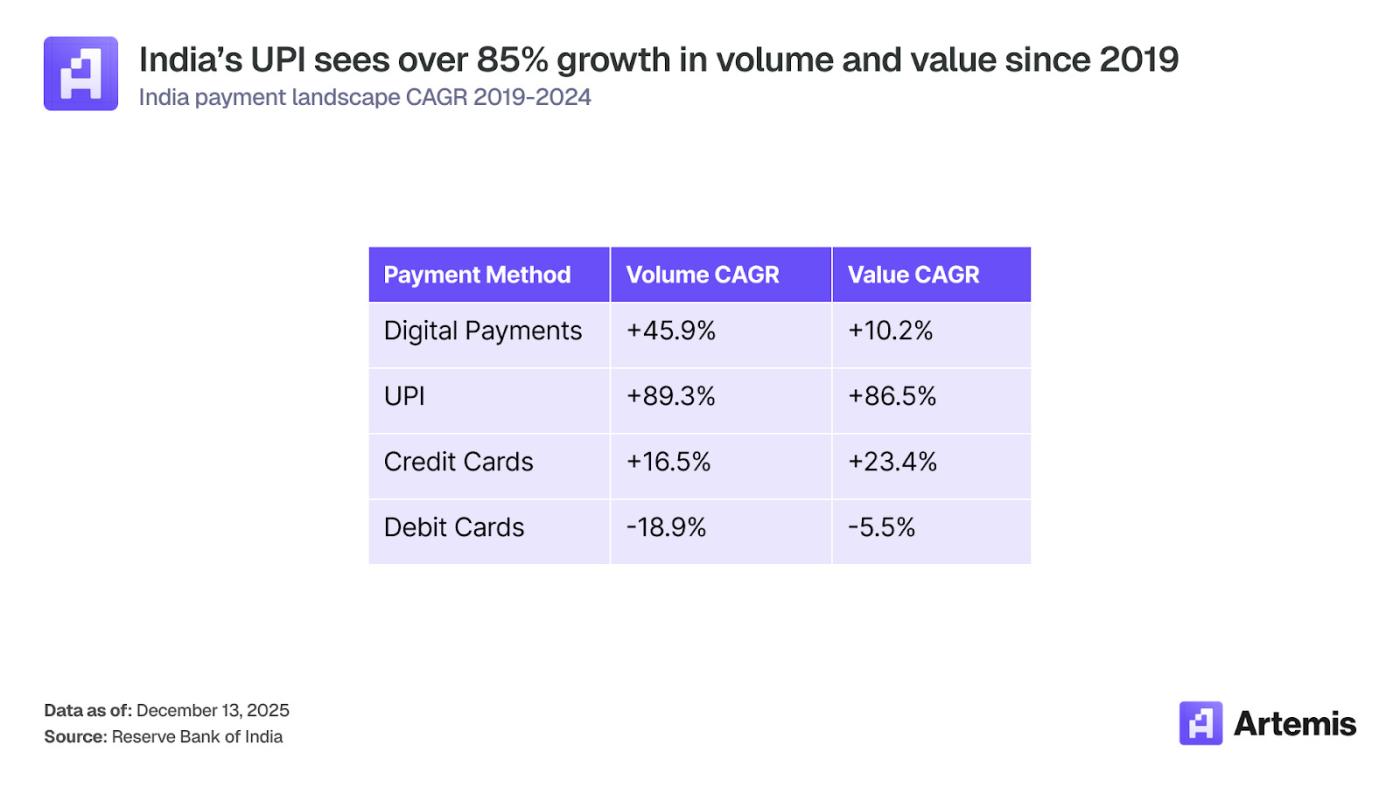

However, to understand the opportunities presented by crypto cards in India, it must be placed within the context of the country's Unified Payments Interface (UPI). Since its launch in 2016, UPI has revolutionized India's digital payments landscape.

According to the Reserve Bank of India's "Payments Systems Report 2025," the share of digital transactions using the UPI system grew from 19% to 83% between 2018 and 2024. The features offered by this system align perfectly with the value proposition of crypto cards, such as instant fund transfers, 24/7 availability, and virtual payment addresses. Consequently, many crypto card issuers have begun integrating with UPI to reach potential customers.

Due to stringent regulatory scrutiny, the vast majority of crypto transactions in India have moved overseas. As the country with the fastest-growing crypto adoption rate in Asia, India is poised to gain significant value from native stablecoin card issuance platforms.

Is the United States ready to embrace change?

In mature economies, both the number of credit card users and credit card companies continue to grow. Users expect unsecured credit in exchange for cash back, reward points, and numerous value-added services. For card issuers, credit card fees are significantly higher than debit card or other payment methods, especially in developed regions like the US and the EU, where transaction fees for debit and prepaid cards are subject to strict regulatory caps.

Credit card revenue has grown significantly in developed countries over the past decade, with companies like Robinhood, Revolut, and Coinbase recently entering the credit card market, and traditional financial institutions such as American Express, JPMorgan Chase, and Capital One continuing to expand their customer base.

The adoption of stablecoins is no longer limited to early crypto enthusiasts. The total supply of stablecoins exceeds $308 billion; the number of monthly active stablecoin addresses continues to grow, reaching an all-time high in December 2025; demographic data shows that the demographic that embraces cryptocurrencies is in its prime for income and consumption.

Compared to the total number of credit card users, the number of stablecoin holders is still small, but it is growing faster than the traditional user group and has high expectations for integrated, yield-generating, and native digital financial products.

A new user group is emerging in this market: consumers who hold substantial amounts of stablecoins and digital assets and increasingly expect seamless access to these assets. If card issuers continue to wait and see, they may be handing this group over to crypto-native competitors who have already established distribution channels and user relationships.

While unsecured credit has yet to emerge in the cryptocurrency and stablecoin credit card space, existing credit products such as the Coinbase One Card and Gemini Credit Card offer alternatives for users with cryptocurrency or stablecoin-denominated credit cards through familiar credit card product lines, providing options for payments and rewards.

On-chain solutions such as Ether.fi Cash Borrow Mode, Nexo Credit Line, and Redotpay Credit provide credit to financially savvy users who may:

- Those who are active on the blockchain but lack traditional credit history may find it difficult to obtain credit products, regardless of their actual financial capabilities.

- Seeking on-chain alternatives to replace traditional credit card products, thereby maximizing the use of their on-chain funds.

The signals displayed by stablecoin credit cards suggest that the traditional credit card economic model will not be immediately disrupted. The US credit card market is large, continues to grow, and possesses structural advantages due to its transaction dynamics and consumer credit needs.

However, various indications suggest that the user group holding stablecoins constitutes a differentiated market segment, whose characteristics deserve the attention of traditional card issuers:

- Higher financial participation and financial literacy

- More willing to accept new financial products

- The number of digital assets that can be used for credit card spending is constantly increasing.

- Behavioral data (on-chain activity) can support new underwriting and segmentation methods.

Pioneers in this field are crypto-native platforms: Coinbase, Gemini, MetaMask, Phantom, and Ether.fi. Traditional card issuers have advantages in scale, brand trust, regulatory relationships, and credit underwriting infrastructure. Opportunities remain for existing institutions that combine these advantages with the native functionality of stablecoins.

3. Future

As stablecoins gain wider adoption, payment innovation is shifting from bank card-mediated digital commerce to stablecoin-led payment channels. Global payment networks, including Visa, Mastercard, PayPal, and Stripe, are building infrastructure to enable merchants to directly accept digital dollars, while reducing transaction fees and accelerating settlement. These developments raise a strategically important question:

If merchants can natively accept stablecoins, will crypto cards still exist?

This issue reflects a broader structural contradiction: the shift from card-centric payment networks based on the economic relationship between issuers and acquirers and transaction fee revenue to asset-centric systems that enable settlement finality, programmability, and low-cost value transfer at the blockchain level.

While the direction of innovation is clear, the timing and feasibility of a full transition to native acceptance of stablecoins remain uncertain. Three structural realities suggest that crypto cards will remain strategically important for the foreseeable future, and their growth rate may outpace that of the crypto economy itself.

Network effects are extremely difficult to replicate

Card organizations and issuers operate at over 150 million merchant locations worldwide, spanning e-commerce, brick-and-mortar retail, hospitality, transportation, and SMEs. Building this infrastructure requires decades of coordinated investment: POS hardware deployment, merchant agreements, banking relationships, regulatory approvals, and establishing consumer trust.

Merchant coverage for native stablecoin payment methods is virtually zero. Significant penetration requires:

- Integrating the new POS system into hardware and software systems

- Establish merchant training, onboarding, and support infrastructure.

- Improve accounting, reconciliation and cash management

- Compliance measures taken to maintain the integrity of AML/KYC across jurisdictions

This is a transition period that could last for many years, or even a decade. Before that, crypto cards are the most convenient bridge connecting digital asset holders with merchant acceptance.

Furthermore, card organizations and issuers offer services far beyond transaction routing. They also provide a variety of services that consumers and merchants take for granted:

- Fraud Protection: Advanced Detection Models and Liability Framework

- Dispute resolution: Consumers have the right to refuse payment to protect themselves from breach of contract or fraud by merchants.

- Unsecured consumer credit: Allows consumers to use future income as collateral for purchases and repay in installments.

- Rewards program: Cash back, points, and mileage rewards based on redemption fees.

- Shopping Guarantee: Extended Warranty, Price Protection, Travel Insurance

The very nature of stablecoin payments limits the range of services they offer. Stablecoin issuers can blacklist addresses used by hackers, and customers can negotiate refunds with card issuers, but options remain limited. To achieve the same functionality as bank cards, a direct acceptance system would have to rebuild these services from scratch, incurring significant costs and increasing complexity.

Credit, in particular, represents a formidable competitive advantage. Global consumers still favor credit instruments for cash flow management and loyalty program accumulation. Payment methods that cannot offer credit face structural resistance to consumer adoption. Even if new technologies offer cost advantages, merchant adoption is often delayed due to operational constraints.

- POS systems and e-commerce platforms optimized for bank card payments

- Relying on established acquirer relationships and support infrastructure

- Tax filing and accounting system specifically designed for bank card settlement

However, the situation is different in some respects. For businesses with high transaction volumes and low profit margins (such as remittances, B2B invoices, and cross-border e-commerce), the economic benefits of stablecoins may be enough to attract them to invest in integration. But for most merchants, bank cards remain the most convenient payment method.

Stablecoin-native P2P and B2B payments will continue to expand in cross-border e-commerce, digital services, and markets where traditional banking services are underdeveloped. However, it is unlikely that stablecoins will completely replace bank card networks in the short term. Bank cards still offer unique advantages to consumers and merchants, such as:

- Everyday expenses (retail, food and beverage, subscriptions, travel)

- Applications requiring credit limits, rewards, or fraud protection

- Merchants unwilling to integrate new payment infrastructure

- Regions where stablecoin regulation is unclear or restrictions are strict

At the same time, stablecoin-based P2P payments also have their unique advantages, with almost no overlap with bank cards in these aspects, including but not limited to:

- B2B payment and invoicing for high-value transactions

- In cross-border trade, transaction fees and foreign exchange costs account for a large proportion of the total cost.

- Native crypto merchants and digitally savvy consumers

- Markets where bank card infrastructure has never been widespread

- High-frequency, low-profit trading, where 2-3% in transaction fees erode profits.

Related reading:Trump exerts high-profile pressure on multiple countries, Visa encrypted cards surge, increasing by 525%.