Author: Owen Chen, Peking University Chain Association (X @xizhe_chan)

Original Title: "Trillion-Yuan" Liquidity Release: Can Pre-IPO Equity Tokenization Restructure PE/VC Exit Models? — The Evolution from PERPS to TaaS

summary

Pre-IPO stocks represent a trillion-dollar value in global asset allocation, but have long been constrained by two structural dilemmas: high barriers to entry for participation and a scarcity of liquidity exit channels. With the tokenization of real-world assets (RWAs) becoming a focal point of financial innovation, "equity tokenization" is seen as a key mechanism to break the liquidity predicament of the private equity market. This report focuses on the underlying equity tokenization of pre-IPO companies (especially unicorn companies), aiming to clarify the evolutionary logic of this sector from early-stage speculation to compliant infrastructure by analyzing the current market situation, implementation paths, and key challenges. The report's core conclusions are as follows:

1. Current Market Situation: Despite global unicorn valuations reaching trillions of dollars, the actual scale of the tokenization market is only in the range of $100-200 million (if some non-freely circulated projects are excluded, the actual tradable scale is only in the tens of millions). The market exhibits a strong head effect, with assets highly concentrated in a few AI technology unicorns such as OpenAI and SpaceX. This indicates that the industry is still in the very early stage of transitioning from a "narrative space" to an "effective market," and has not yet formed a large-scale asset supply and absorption capacity.

2. Path Differentiation: The industry has formed three differentiated paths, the core difference of which lies in the "degree of confirmation of rights" and the "participation of the target company":

Synthetic assets (Republics, Ventures): including Perps and debt securities, do not hold underlying equity, only provide valuation exposure, use high leverage to meet speculative demand, and mainly serve to introduce liquidity.

SPV indirect holding (Jarsy, PreStocks, Paimon): Holding shares and tokenizing equity through offshore SPVs is currently the most mainstream implementation model. However, it faces dual compliance challenges from the target company and regulatory agencies. Recent public warnings from companies such as OpenAI have exposed the legal vulnerability of this model in violating "transfer restriction clauses".

Native Collaborative Models (Securitize, Centrifuge): Essentially, these provide TaaS (Tokenization as a Service) for target companies. Leveraging transfer agent qualifications, they achieve a legal mapping between on-chain tokens and shareholder registers, enabling true on-chain equity ownership. While the implementation cycle is long, it resolves the legal finality dilemma and provides a compliant path for IPO transitions.

3. Trend Analysis: Tokenization does not automatically create liquidity; the current market faces liquidity issues (thin market, pricing failure). The future breakthrough for the industry lies not in unilateral issuance, but in collaboration with the target company.

On the compliance side: Under pressure from both regulatory agencies and the company's legal department, the business model will gradually shift towards compliance collaboration, that is, the service provider will provide TaaS infrastructure for the issuer.

On the asset side: the target assets will shift from crowded leading unicorns to long-tail private enterprises with a more urgent need for exit.

On the infrastructure side: It is necessary to build native RWA trading facilities (such as compliant AMMs and on-chain order books) that are adapted to the securities attributes to solve the problem of insufficient depth.

On the ecosystem side: the future market will move towards a multi-layered symbiotic pattern, rather than a single model of survival of the fittest. Synthetic asset models serve as traffic entry points and play a role in user cultivation; SPV indirect holding models have strong flexibility and can perform early verification of specific assets; native collaborative models provide TaaS services and are a standardized path for undertaking institutional funds and realizing large-scale asset on-chaining in the future.

Keywords: Pre-IPO equity tokenization, RWA, SPV architecture, TaaS (Tokenization as a Service), Transfer Agent

1. Scope and Key Definitions of the Study

Equity in non-listed companies, especially equity in high-growth unicorns, constitutes an important asset sector in the global economy that cannot be ignored. [1] However, for a long time, its investment access and main value-added returns have been dominated by professional institutions such as PE/VC and a small number of high-net-worth individuals, making it difficult for ordinary investors to access. As blockchain technology matures, the path of "equity tokenization" has become feasible—that is, mapping equity shares with on-chain digital tokens to improve the efficiency of private equity asset circulation within the scope of compliance. Boston Consulting Group (BCG) predicts that the on-chain RWA market size is expected to reach $16 trillion by 2030. [2] This reflects the market's high attention to the direction of tokenization: on the one hand, it stems from the huge value of leading non-listed companies themselves, and on the other hand, it comes from the expectation that tokenization technology will reduce the threshold and transaction friction of traditional financial markets.

Against this backdrop, this article will systematically review the market background and current development status of tokenization of unlisted equity, analyze the pain points of the traditional market and the advantages of the tokenization mechanism, and combine major platform cases, technical and regulatory points and key challenges to make a judgment on the future evolution direction.

1.1 Research Subjects

This report will focus on the tokenization of underlying equity at the enterprise level—specifically, non-listed companies (especially unicorn companies), that is, the direct tokenization of "target company equity," rather than the tokenization of LP shares in private equity funds (PE funds) in the traditional context.

This is primarily because discussions on "private equity tokenization" typically focus on the investment side, using traditional financial frameworks for calculation and analysis. This often overlooks the larger components of a unicorn's equity structure—such as founding team ownership and employee stock ownership plans (ESOPs). This omission can lead to biases in assessing the scope of assets that "equity tokenization" can cover and the actual liquidity needs, thereby underestimating the market's actual potential and room for expansion.

1.2 Research Prerequisites

Timeline: The research period of this paper ends on December 27, 2025.

Data caliber: Valuation of unlisted equity naturally lacks a unified official caliber, so market size and tokenized market capitalization are estimated using publicly available statistics and platform data.

Equity liquidity: Unlisted equity is inherently subject to lock-up, transfer restrictions, and shareholder register management requirements, and there are difficulties in tokenization in actual implementation. Therefore, we distinguish between the two sets of concepts: "theoretical tokenization (full amount)" and "tradable tokenization (after restrictions)".

Currency and exchange rate caliber: Since the pricing involves multiple currencies, this article uses the US dollar as the standard. The exchange rate conversion is approximated by the assumption that the US dollar is a stablecoin, and no separate scenarios are discussed for extreme de-pegging situations.

Special products: Synthetic contract products on platforms such as Bybit and Hyperliquid are listed and measured separately by open interest and are not included in the "equity token market value" calculation.

2. Market Background: The "Trillion-Dollar Siege" of Unlisted Equity

2.1. Asset lineage and shareholder structure

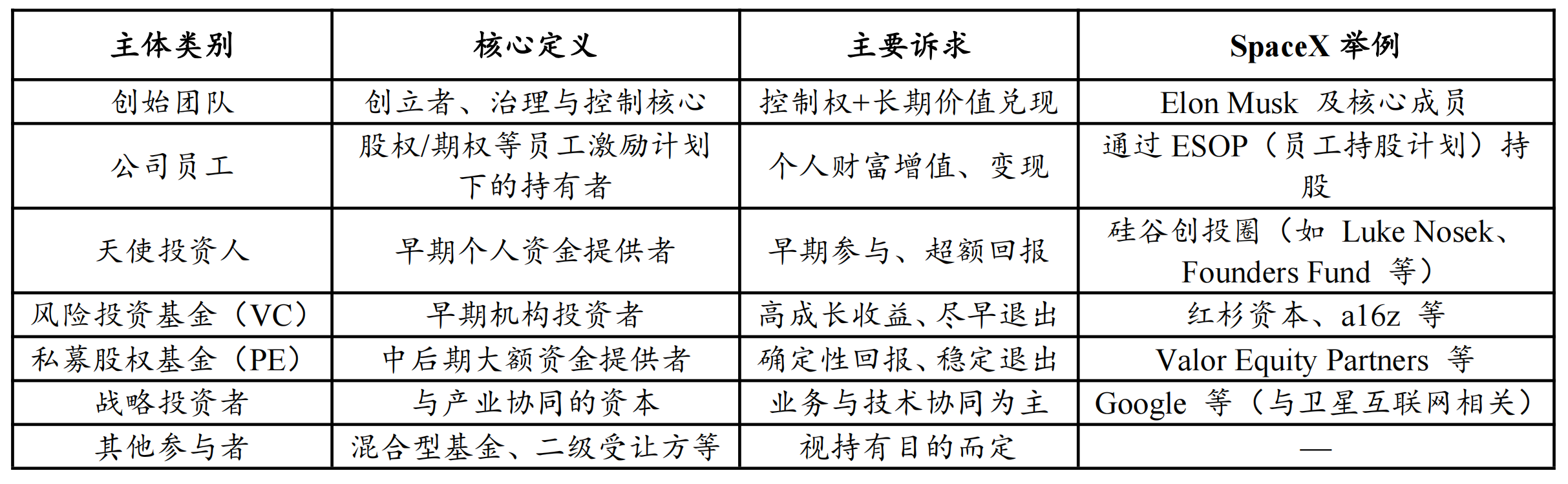

In a broad sense, equity in unlisted companies covers the shares of all companies not listed on public exchanges, and is highly diverse in type, ranging from early-stage startups to mature large private groups. Holders are not limited to institutional funds, but commonly include: founding teams, employee shareholders (equity and stock options), angel investors, VC/PE firms, strategic investors, and various secondary acquirers.

Table 1: Common Holder Structure of Unlisted Equity

Source: Compiled by PKUBA Research

Aside from strategic investors and some founding teams, other equity holders generally have varying degrees of need to realize their assets: institutions emphasize exit efficiency; employees often need readily available liquidity when leaving or at financial planning junctures. However, under traditional mechanisms, apart from a few methods such as share buybacks, the efficiency of equity circulation in the secondary market is low, thus "difficulty in exiting" is a long-standing structural dilemma.

2.2. Scale Characterization: Dual Evidence from Capital Allocation and Asset Valuation

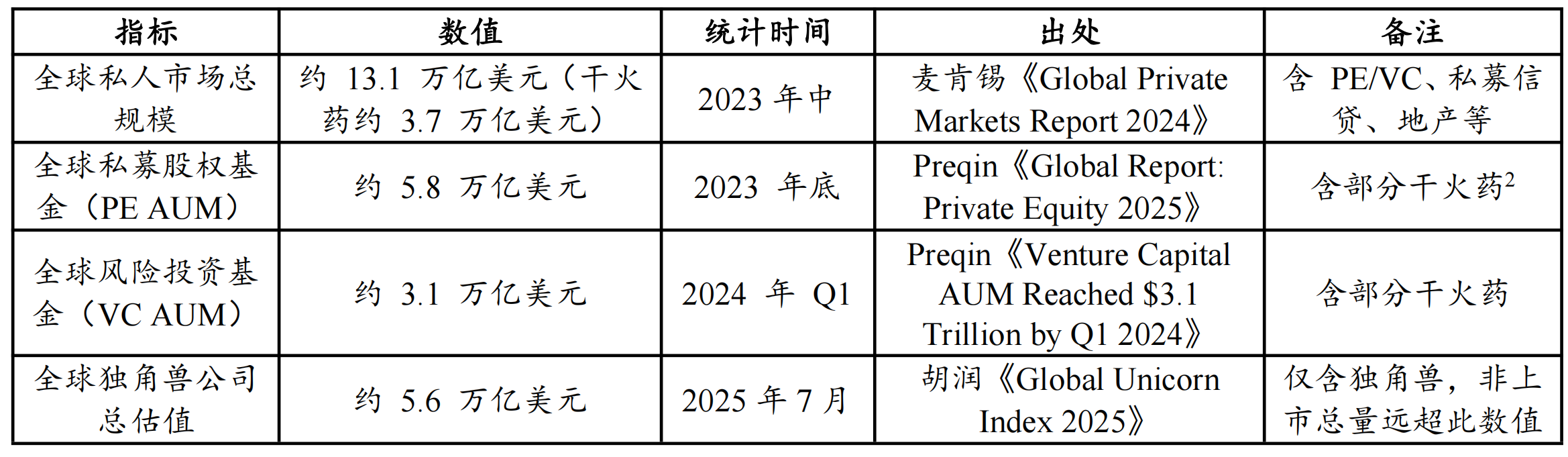

It is important to emphasize first that, since there is no unified official definition of the size of unlisted equity, this section mainly relies on statistical data from mainstream institutions to make inferences about the magnitude from two dimensions: "capital allocation capability" and "asset valuation size".

Table 2: Key Indicators for Global Private Market and Unicorn Valuation

Data sources: Hurun, McKinsey, Preqin

According to the data, in terms of "capital allocation capability", the total assets under management of PE and VC are approximately US$8.9 trillion (5.8T + 3.1T), which constitutes an important capital base for unlisted equity assets;

In terms of "asset valuation," the valuation of unicorns alone has reached trillions of dollars. According to statistics from Hurun Research Institute [3], this figure was US$5.6 trillion by mid-2025. According to CB Insights, as of July 2025, the cumulative valuation of 1,289 unicorns worldwide exceeded US$4.8 trillion. [4]

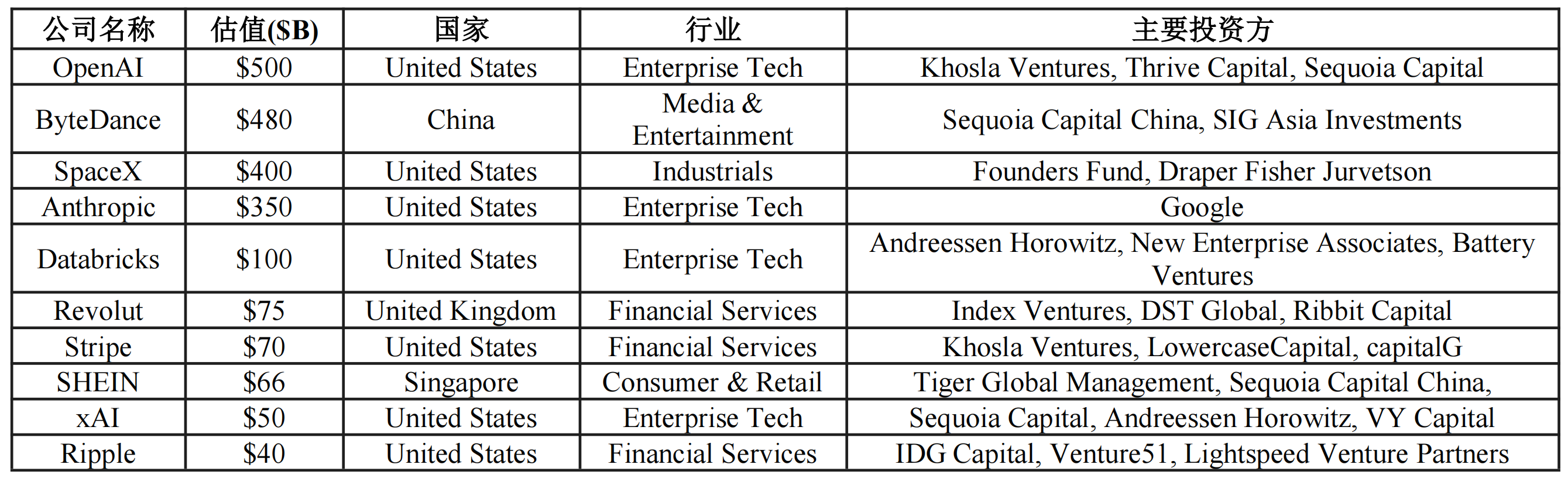

Table 3: Top 10 Global Unicorn Companies by Valuation

Source: CB Insights (as of December 2025)

It is important to emphasize that whether it is 4.8 trillion or 5.6 trillion, these are only the top few thousand companies at the very top of the pyramid; the enormous value of tens of thousands of mature private enterprises and growth companies worldwide that have not yet reached the unicorn level has not been included in the statistics.

In summary, the global private equity market is a vast, encircled territory with a total value far exceeding trillions of dollars. This astonishingly large but illiquid blue ocean of assets undoubtedly offers highly imaginative application prospects for tokenization.

3. The core contradiction and the value path of tokenization

Unlisted equity has long exhibited a balance between high value and low liquidity, fundamentally due to the dual constraints imposed on both participation and exit by institutional and market structures. Based on this, the potential value of equity tokenization is primarily reflected in three aspects: circulation channels, price discovery, and financing channels.

3.1. Dual Bottlenecks: Limited Participation and Obstacles to Exit

Unlisted equity has long exhibited a structural characteristic of "high value volume - low liquidity supply," which stems from the fact that both the participation and exit ends are subject to the dual constraints of institutional arrangements and market structure: on the one hand, entry rules and capital thresholds compress the investor coverage; on the other hand, exit channels rely on end events and inefficient secondary circulation, making assets difficult to circulate.

On the participation side: High barriers to entry and small-circle compliance constraints. In most jurisdictions, transactions of unlisted equity are usually strictly limited to qualified investors or institutional investors; at the same time, the minimum investment amount is often hundreds of thousands to millions of US dollars, coupled with qualification requirements such as net assets and income, forming significant institutional and financial barriers, resulting in a high concentration of asset dividends and limited breadth of market capital supply.

Exit Strategy: Scarcity of Exits and Lengthened Cycles. Traditional exits heavily rely on final events such as IPOs or mergers and acquisitions (M&A), but the trend of "unicorns delaying their IPOs" has significantly lengthened the holding period, making it difficult to realize paper wealth in a timely manner. Even when transferring through the private secondary market, transactions often rely on offline matching, which generally suffers from problems such as lack of transparency, significant friction in due diligence and settlement, high costs, and slow settlement, resulting in inefficient and unstable liquidity supply.

3.2. Three Types of Gains: Circulation Channel, Price Discovery, and Financing Supplement

Compared to the "tokenization of listed stocks," which mainly improves trading time and accessibility, the tokenization of unlisted equity is more like a redesign of the private equity market structure, which is mainly reflected in three core benefits:

First, in terms of circulation channels: tokenization reduces the "siege" dilemma with continuous secondary liquidity, and builds a two-way channel for the participation and exit sides.

To address the challenges on the participation side, the potential benefits of tokenization are mainly reflected in expanding access through divisibility: by splitting equity interests or economic benefit rights into finer granularities, the threshold for participation in a single transaction can be lowered within the compliance framework, allowing more compliant investors to access exposure to growth targets that were previously difficult to allocate, thereby alleviating the structural constraints of "difficulty in participation" in the private equity market.

Addressing the challenges on the exit side, the core benefit of tokenization lies in supplementing liquidity outlets: for employees, early investors, and institutional funds, it can provide a more continuous transfer channel beyond IPOs/M&A/buybacks, expand liquidity options, and reach a wider range of potential buyers, thereby improving exit options and timing flexibility without changing the endgame path.

Figure 1: Summary of Exit Paths in the Primary Market

Source: Compiled by PKUBA Research

Secondly, regarding price discovery: Tokenization introduces more continuous price discovery signals, enhancing financing pricing and market capitalization management capabilities. Traditional valuation of unlisted equity is primarily anchored to financing rounds, with low frequency and insufficient transparency. Valuation signals often lag behind changes in corporate operations and market expectations. Equity tokenization enables relatively continuous secondary trading, providing more continuous price discovery signals, helping to narrow the valuation gap between primary and secondary markets, and offering a "quasi-public market" reference for subsequent financing pricing and market capitalization management.

Third, in terms of supplementary financing: Tokenization opens up new financing channels and is expected to explore new models of STOs and "digital listings." Tokenization not only serves the transfer of existing equity but may also become a tool for incremental financing. Some companies can access compliant global digital capital pools through security token offerings (STOs), which can reduce the cycle and cost of traditional IPOs to some extent and provide new options for financing and capital structure management. Platforms such as Opening Bell are also exploring similar "digital listing" paths, but cooperation and large-scale implementation at the non-listed company level still require more case studies for verification.

4. Current Market Situation: From Narrative Space to Measurable Scale

4.1. Current Scale: A "tens of millions" scale in the early verification phase

Since some platforms do not disclose market capitalization, and synthetic contracts are measured by open interest, this article mainly uses the disclosures from CoinGecko and the project's official website for estimation.

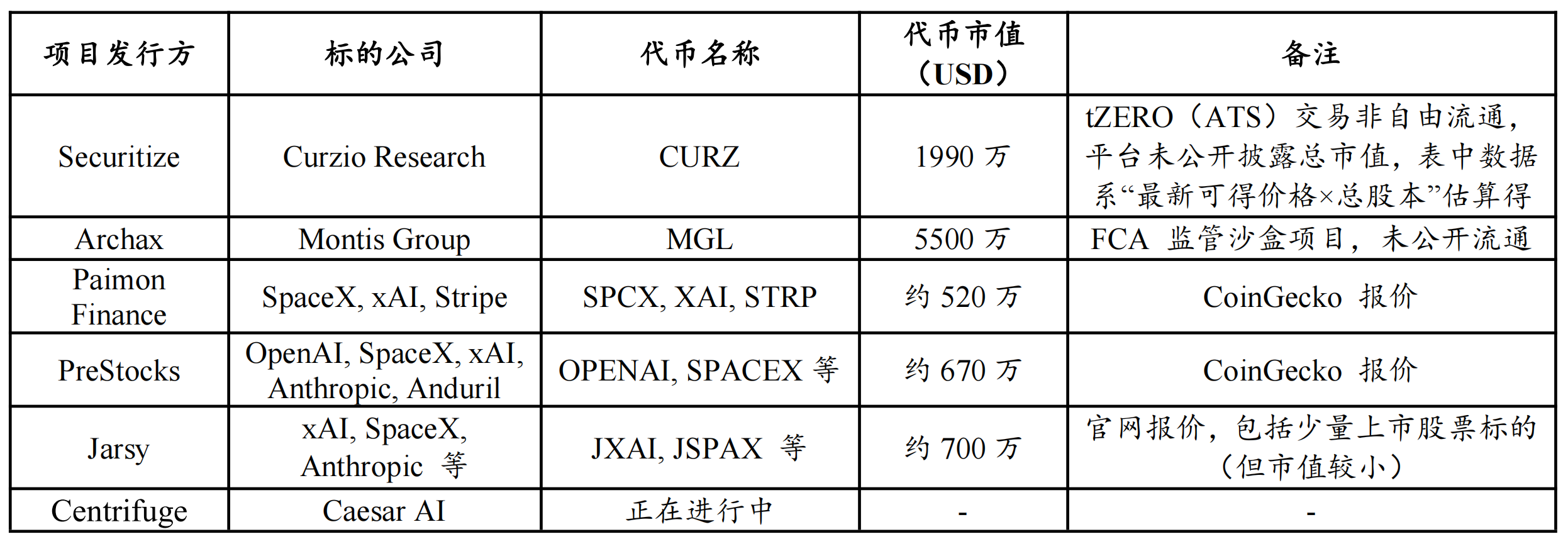

Table 4: Statistics on Major Equity Tokenization Projects of Non-Listed Companies (Incomplete Statistics)

Data source: CoinGecko, project website, etc., as of December 27, 2025.

Based on the above samples, a relatively clear conclusion can be drawn: the market for tokenized unlisted equity is still in its early verification stage. Based on disclosable data and estimable estimates, the overall industry size is roughly in the range of $100-200 million. However, excluding projects like Securitize (CURZ) and Archax (MGL) that are not freely tradable on-chain, the freely tradable market size is approximately tens of millions of dollars.

This result implies that even with a vast market narrative space, secondary market liquidity, trading depth, and participation breadth remain limited at this stage, and in the short term, it is more like a small sample completing market education and model validation.

4.2. Target Preference: Concentration on Leading Tech Unicorns and AI Assets

From the perspective of the underlying asset distribution, apart from a few special projects, the current tokenized assets show obvious characteristics of high homogeneity and concentration at the top, mainly focusing on top US technology unicorns, and with AI-related assets as the core (such as OpenAI, SpaceX, xAI, etc.).

The reason for this concentrated preference is that in the early stages of the market, project teams often prioritize assets with high brand awareness, strong narratives, and concentrated attention to generate transaction buzz and traffic conversion at a lower educational cost, thereby promoting product launch and market validation. In contrast, although some project teams claim to have contacted or communicated with the owners of unicorns with Chinese capital backgrounds, there is still a lack of publicly verifiable successful cases, indicating that this approach has not yet formed a replicable path in terms of asset acquisition, compliance boundaries, and transaction structures.

5. Implementation Path: Structural Differences and Rights Boundaries of the Three Models

In practice, three main solutions have emerged regarding "how to transform unlisted equity into tradable assets on the blockchain." The differences between these solutions lie in: whether there is actual shareholding, whether the target company is involved, whether the token corresponds to shareholder rights, and compliance licenses and qualifications.

Table 5: Comparison of Equity Tokenization Models for Non-Listed Companies

Source: Pharos Research

5.1. Synthetic Asset Type: Value Mapping Detached from Underlying Ownership Confirmation

Synthetic assets typically do not require the permission of the underlying company and do not hold underlying equity. Instead, they issue contracts that track valuations, giving investors economic exposure to the underlying asset. Their key characteristics are: investors are not included in the shareholder register, do not enjoy shareholder rights such as governance or dividends, and returns are entirely determined by the contract terms and settlement mechanism. Therefore, their product attributes are closer to synthetic derivatives.

The advantages of this model are its fast deployment speed, flexible structure, and low dependence on asset acquisition; however, the risks are also relatively concentrated, mainly including counterparty credit risk, tracking error and pricing deviation risk, clearing and settlement mechanism risk, and regulatory uncertainty across jurisdictions.

This approach better aligns with the trading and speculation needs of native Web3 users regarding risk exposure, but it is difficult to equate it with an assetization solution in the sense of putting equity on the blockchain. Currently, representative practices of this model can be broadly categorized into two types: one is debt instruments (such as Republic), and the other is valuation perpetual contracts (such as Ventures, based on Hyperliquid).

Figure 2: Introduction to Equity Tokenization in the Ventures Official White Paper

Source: Ventures official documentation

5.2. SPV Indirect Holding Type: First verify the mainstream form of demand.

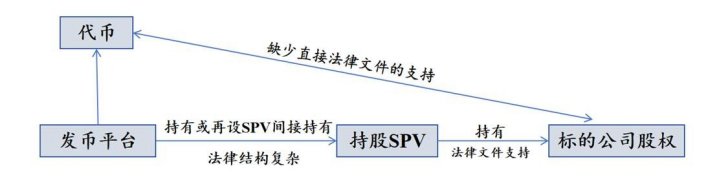

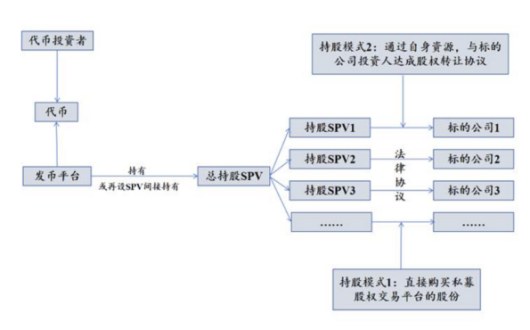

The SPV model structure is as follows: the platform establishes an SPV to acquire and hold actual equity in the traditional private secondary market; the tokens sold to external parties are not the equity of the target company itself, but rather equity certificates of the SPV. Therefore, investors are usually not on the target company's shareholder register, nor do they directly possess governance voting rights.

Figure 3: SPV Indirect Holding Issuer Structure Diagram

Source: Pharos Research

The advantage of this structure lies in its flexibility, but the risks are also relatively concentrated, mainly in two aspects:

Transparency challenges: Offshore SPVs have complex structures, and investors can often only verify the asset-side proof of whether the SPV holds shares, but it is difficult to fully penetrate the operational and financial information on the liability side.

The target company warns of the following risks: If the target company determines that the company has violated the shareholder agreement or transfer restrictions, it may trigger legal and compliance conflicts, which will be detailed later.

5.3. Native Collaborative Model: Real Stock On-Chain Transaction Centered on the Transfer Agent

The premise of native collaboration is the deep involvement of the target company, which can be understood as providing TaaS (Tokenization-as-a-Service) services to the target company. However, unlike asset on-chaining in the general sense, this model requires the project party to have the qualification of Transfer Agent (TA) to achieve a one-to-one correspondence between equity and tokens. The Transfer Agent is the core to connect the mapping relationship between on-chain tokens and offline shareholder registers, thereby realizing the on-chaining of rights in terms of legal structure.

A transfer agent typically refers to a registered transfer agent with the SEC, used to maintain and update the shareholder register. Only when token issuance and transfer trigger compliant updates to the shareholder register do on-chain tokens have a substantive correspondence with equity; correspondingly, token holders can obtain more complete shareholder rights within the company's bylaws and applicable legal framework, including voting rights, dividends, and information rights. This is the fundamental reason why native collaborative tokens have less controversy and a clearer basis for rights compared to SPVs and synthetic assets.

However, the implementation cost of this model is also significantly higher. On the one hand, its transaction and transfer processes are more susceptible to strict regulatory scrutiny; on the other hand, it often requires additional licenses and trading facilities such as Broker-Dealer (BD) and ATS to form a compliant closed loop from issuance and registration to secondary circulation. Therefore, its main constraints are not theoretical feasibility, but rather the completeness of compliance, the implementation cycle, and the willingness of the target company to cooperate. Regarding current market developments:

Opening Bell is currently being implemented more in scenarios involving listed companies, while collaborations with non-listed companies are still mainly limited to official publicity and promotion.

The Securitize approach has strong reference value for compliance practices, which will be discussed further below.

Centrifuge, a leading project in the RWA field, announced its entry into equity tokenization in November this year, extending its business focus from private lending to unlisted equity. Its subsequent progress is worth paying close attention to.

Figure 4: Centrifuge's official website promotional image for entering the unlisted equity tokenization market.

Source: Centrifuge official website

6. Case Studies: Typical Case Breakdowns of the Three Models

Based on the path classification described above, the compliance strategies and trading facilities corresponding to the three models differ significantly. This section will further break down specific implementation cases of the three models and compare and analyze their business processes and operational effectiveness.

6.1. Synthetic Asset Type: Introduction of Speculative Flows

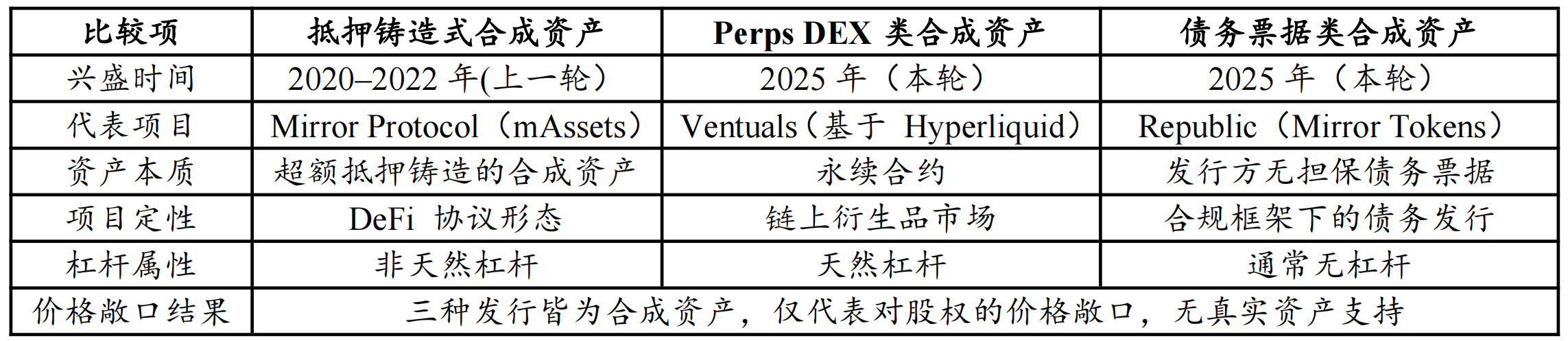

Synthetic assets do not acquire underlying equity; instead, they break down the valuation of the underlying asset into basic contract units and provide price exposure to the market through on-chain matching. Current practices mainly diverge into two paths: one is synthetic assets based on perpetual contract platforms (Perps DEX), and the other is debt instruments that realize exposure in the form of notes.

Both share the characteristic of not corresponding to actual equity or generating shareholder rights; the differences lie mainly in compliance boundaries, transaction mechanisms, and capital attributes, and differ from the previous round of synthetic asset narratives primarily based on collateralized creation (such as Mirror Protocol). Specifically:

Perps DEX-type synthetic assets: These are essentially perpetual contracts that improve trading efficiency and capital turnover through leverage and funding rate mechanisms. A representative project is Ventures (based on Hyperliquid).

Synthetic assets such as debt instruments: These are essentially tokenized notes issued by the platform, belonging to debt instruments. They are linked to the performance of the underlying asset according to the contract terms. A representative project is Republic's Mirror Tokens.

Table 6: Comparison of the Three Forms of Equity Synthetic Assets

Source: Compiled by PKUBA Research

From the perspective of product positioning and capital structure, the market shows a clear differentiation: Republic's approach is more compliant and traditional financial framework, holding a Broker-Dealer license and disclosing and issuing under the framework of US securities law, with a relatively clear scope of investor access; Perps DEX's approach is closer to the logic of the native trading market, and its core competitiveness is not in legal rights, but in the trading attributes themselves, including leverage tools, continuous liquidity supply and low trading friction.

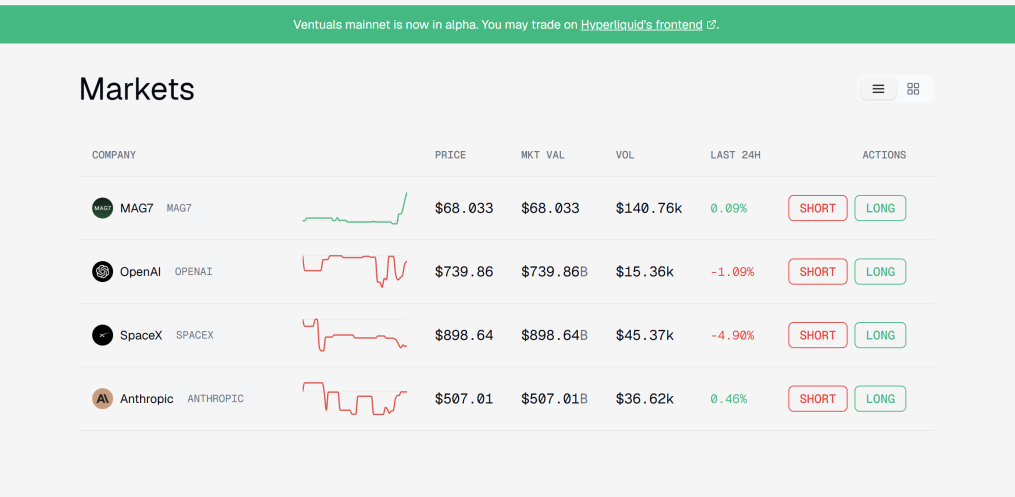

Figure 5: Vendors Platform Pre-IPO Contract Product Showcase

Source: Ventures official website

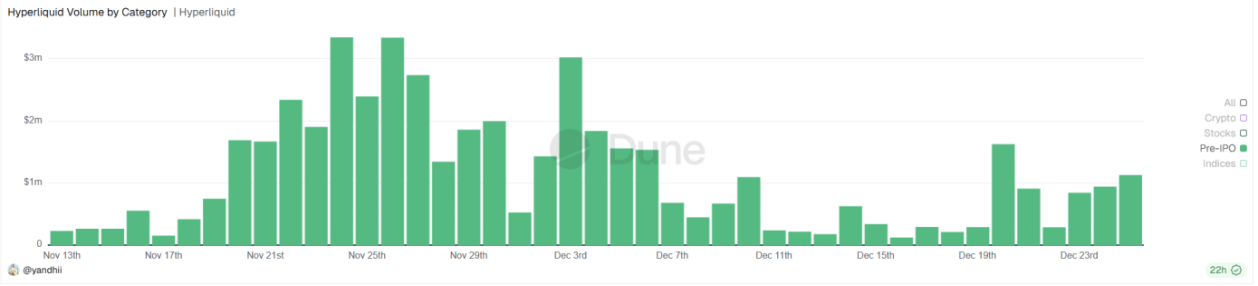

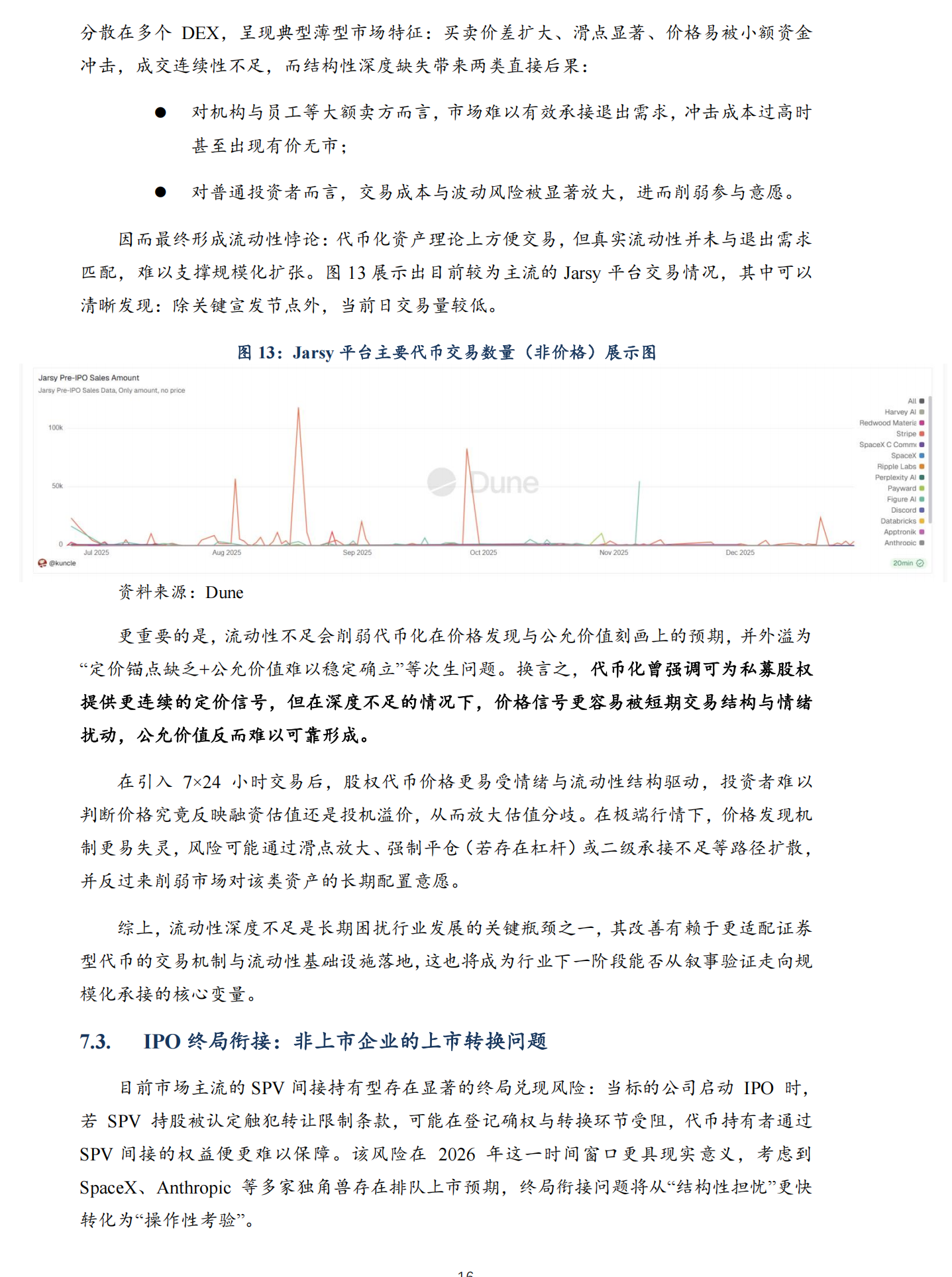

From a liquidity perspective, the Perps route based on Hyperliquid has a greater advantage in the short term. According to Dune data, the daily trading volume of pre-IPO related assets on Hyperliquid has reached millions of dollars (see Figure 6), which contrasts with the performance of SPV indirect holdings in terms of secondary market trading volume and depth (see Figure 13 below for comparison). The reason for this is that synthetic assets, especially Perps, are more in line with the funding preferences of the crypto market: high-frequency trading combined with high leverage mechanisms makes it easier to attract speculative funds and trading users, thereby generating considerable trading volume and educating users about the category of non-listed equity exposure on the demand side.

Figure 6: Daily trading volume of Pre-IPO related assets on the Hyperliquid platform (USD)

Source: Dune

Further analysis suggests that synthetic assets may not necessarily replace real shares on the blockchain. They are more likely to play a role in cultivating demand and warming up liquidity in the early stages: by first gathering users and funds on the trading side, they can then provide a potential market foundation and demand for a more compliant and secure equity tokenization path in the future.

6.2. SPV Indirect Holding: The Coexistence of Low Barriers to Implementation and High Compliance Controversies

The core logic of SPV indirect holding is to have a special purpose vehicle (SPV) typically located in an offshore jurisdiction hold the equity of the target company, and then tokenize the beneficial certificates of the SPV, thereby providing the market with economic exposure to unlisted equity without directly accessing the shareholder register of the target company.

Figure 7: SPV Indirect Holding Type Token Issuance Structure Diagram

Data source: Pharos Research

This model, due to its flexible structure and relatively low barriers to entry, has become the most common practice in the field of unlisted equity tokenization. However, it has also exposed controversies regarding compliance and governance. In terms of asset acquisition, SPVs typically acquire the target equity through two paths:

Path 1: Purchase through a private equity secondary market platform. Typical platforms include EquityZen, Forge Global, and Hiive. This path is relatively standardized and more replicable, but it often comes with higher structuring costs and compliance review requirements.

Path Two: Acquisition through the issuer's PE/VC resources. The issuer leverages its resources within the traditional private equity circle to acquire shares from private equity funds or venture capital funds holding the target equity. In this structure, the SPV often indirectly holds shares as a new LP (Limited Partner), essentially turning the transaction into a transfer of fund shares.

The key to the rapid expansion of this model lies in its attempt to structurally circumvent transfer restrictions in shareholder agreements. Because the acquired shares are often small and may be formally considered as transfers of LP shares within the fund, some transactions do not need to be reported to the target company on a transaction-by-transaction basis, thus providing the platform with limited structural space and time window.

However, along with "easy implementation" comes "high controversy." The transparency of the SPV model is usually one-sided: investors can often only verify the asset-side proof of "whether the SPV holds shares," while the platform's own funding arrangements, fee structure, risk isolation, and operational stability still retain a certain degree of opacity. This is particularly evident in the issuance pace, with two common operating methods in the market:

Buy first, issue later: The project team first purchases equity with its own funds, and then issues tokens to recoup funds. The assets are locked up first, and the uncertainty of performance is relatively lower.

Issue tokens first, then buy: Tokens are issued to raise funds, and then a commitment is made to purchase equity; if the funds raised are insufficient or price fluctuations prevent the transaction from being completed, investors will face higher execution and delivery risks.

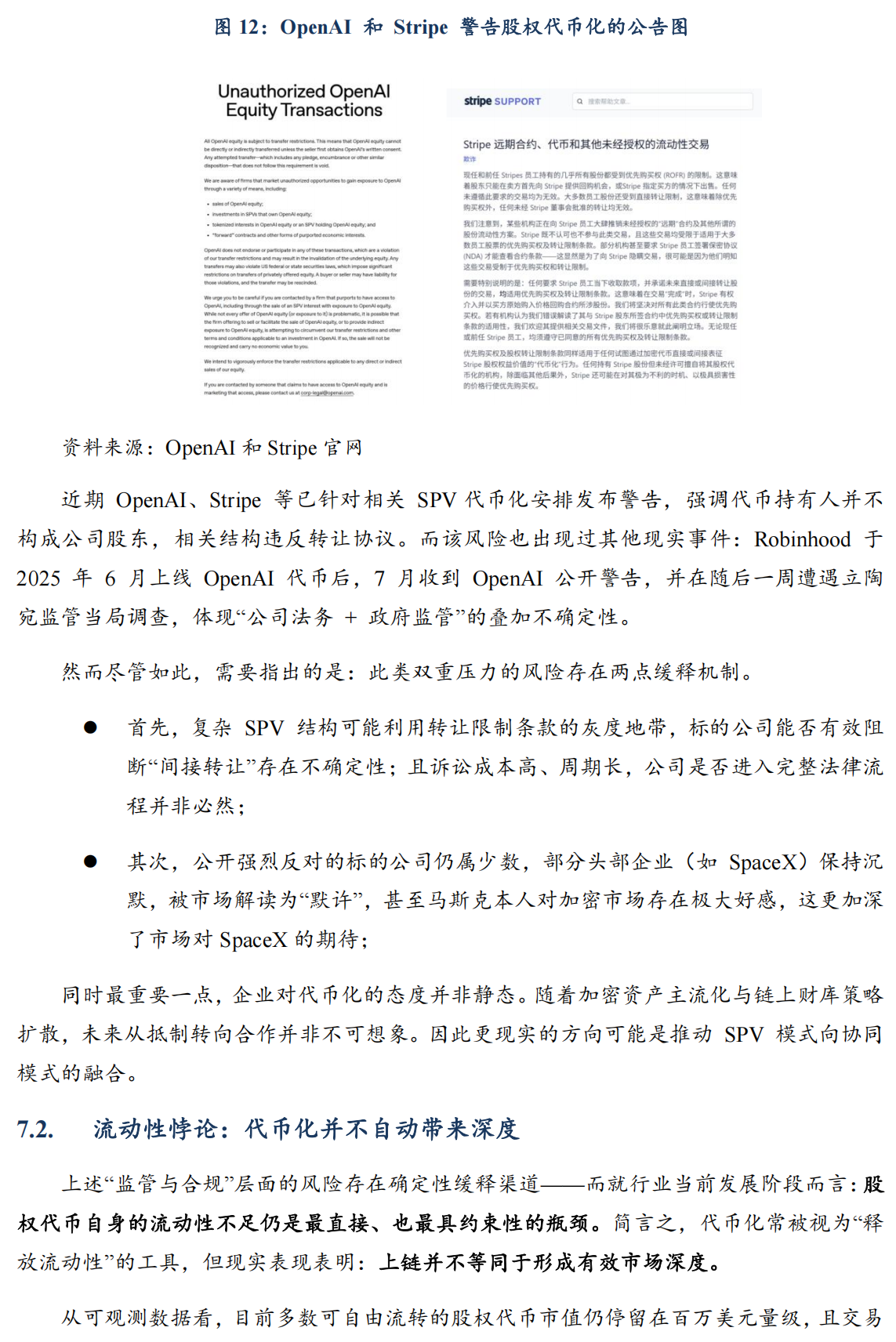

Compared to synthetic asset-backed securities without any asset backing, the SPV model at least has equity backing, thus offering greater certainty regarding the "existence of the assets." However, its core risks are not limited to internal operations but lie in external legal and compliance challenges: when tokenization is deemed by the target company to violate shareholder agreements or transfer restrictions, it may simultaneously trigger compliance pressure from government regulators and legal claims from the target company. Recent public statements from some target companies (such as OpenAI) opposing related arrangements have further highlighted the external uncertainties of this model. The mechanisms of risk transmission and impact will be discussed in more detail below.

6.3. Native Collaborative Model: Implementing TaaS Service Model through Licensing Compliance

The key to successful implementation of native collaborative solutions lies in the uniformity of the compliance framework: it requires the target company to directly access the government regulatory system, achieving compliant digitization of assets by mapping company equity to digital securities on-chain. In industry practice, this model is gradually evolving from a single on-chain tool into a full-stack TaaS (Tokenization-as-a-Service) solution for the target company. Service providers are no longer limited to technology delivery, but offer a closed-loop process covering issuance, registration, holder management, and even secondary market circulation.

Among the currently observable market samples, the most representative native collaborative paths are concentrated in two infrastructure institutions: one is Securitize, which has formed a relatively complete compliance path and has verifiable cases; the other is Centrifuge, which recently proposed a reference architecture for compliant on-chain equity, but actual issuance cases are still in the development stage.

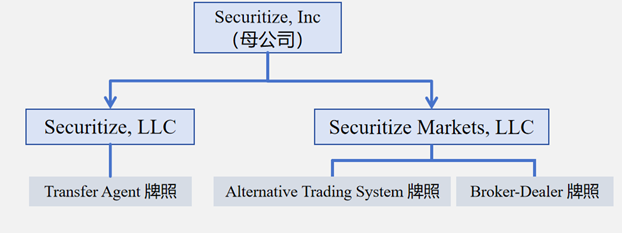

Figure 8: Securitize Compliance Licenses and Structure Diagram

Source: Securitize official website

Therefore, this section mainly focuses on the architectural direction of Centrifuge and the implementation cases of Securitization, with the Securitization part mainly following two paths:

Securitize Path A: The Lifecycle of a Tokenized IPO (Exodus)

Securitize Path B: The Normative Form of Long-Term Private Placement (Curzio Research)

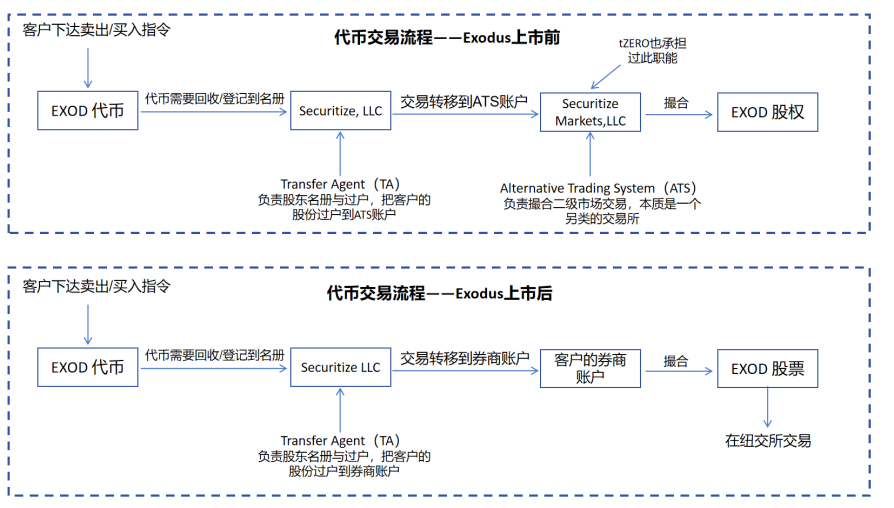

6.3.1. Securitize Path A: Exodus – A Lifecycle Sample from ATS to the NYSE

As of the end of December 2025, the project's token market capitalization was approximately $200 million, making it an important component of the tokenized stock market. Its evolution path reflects the different ways liquidity was absorbed at different stages:

2021: Exodus, as a privately held company, partnered with Securitize to mint Class A common stock into equity tokens on the Algorand blockchain via the DS protocol; Securitize acted as the transfer agent, responsible for token creation, maintenance, and destruction; subsequently, the peer-to-peer transfer from whitelisted wallets gradually expanded to compliant trading on Securitize Markets and tZERO (ATS, Alternative Trading System);

December 2024: Exodus was listed on the NYSE American (ticker symbol: EXOD), completing its transition from unlisted tokenized equity to publicly traded securities;

2025: Exodus announced a partnership with Superstate’s Opening Bell to expand its stock tokens to networks such as Solana and Ethereum, but Securitize’s core role as the Transfer Agent remains unchanged.

Figure 9: Schematic diagram of the token trading process before and after Exodus' listing

Source: Paramita Venture

The diagram above illustrates the liquidity mechanisms at different stages before and after the IPO. It can be seen that the core of Exodus's token liquidity before and after the IPO is completed through the Transfer Agent (TA), but after the IPO, tokens and stocks can be converted into each other.

Prior to listing (2021–2024): ATS was the primary platform. Investors first deposited tokens into the Transfer Agent to update their register. The Transfer Agent then transferred the holdings to the ATS (Alternative Trading System) brokerage firm, where ATS matched trades and settled the transactions.

Post-listing (December 2024 – present): Transferred to public market stock trading. Investors use Transfer Agents to convert tokens into traditional registered shares (street-name held) in brokerage accounts and trade them regularly using EXOD tokens.

In addition, there is another underlying, persistent liquidity path: compliant OTC transfers. Both parties' wallet addresses must be whitelisted, the price is negotiated offline, the consideration is arranged separately, and the token transfer is completed on-chain. It's worth noting that this path was a primary liquidity method during Exodus's transition from delisting from ATS to preparing for its NYSE listing.

6.3.2. Securitize Path B: Curzio Research – A Sample of Private Placement of Unlisted ATS

Exodus demonstrates an ideal life cycle, but for most private companies, the circulation within ATS may not be a transitional phase, but rather a long-term "endgame phase."

Figure 10: Curzio Research Token Market Cap Trend Chart

Source: MarketCapWatch, as of December 27, 2025

The Curzio Research (CURZ) case illustrates this: Equity tokenization and trading on the ATS (Audience Trusts System) for accredited investors provides a compliant but limited secondary market for companies not planning to go public or unable to do so, alleviating shareholder exit pressures. Its trading performance also reflects the thin market characteristics of the ATS: a prolonged decline after issuance, bottoming out in early 2024, followed by high volatility, characterized by large spreads, sparse trading, and low price discovery efficiency (significantly different from the depth of the public market).

6.3.3. Centrifuge's Entry: A Directional Signal for the Native TaaS Route

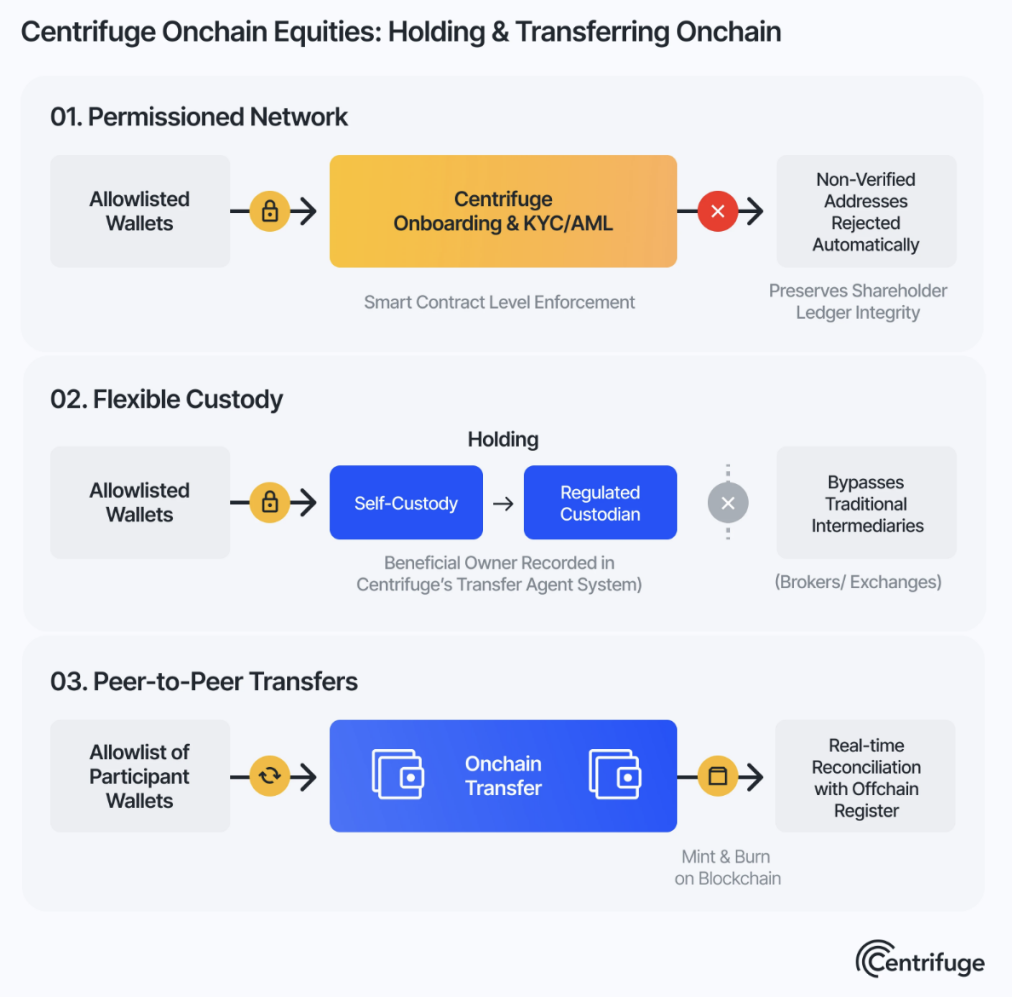

From the perspective of industry evolution, Centrifuge's entry into the market is more like a directional signal: native collaboration is moving from case-by-case driven to standardized architecture.

On December 5, 2025, Centrifuge released "Centrifuge Tokenized Equities: A Reference Architecture for Regulated Onchain Equity", which systematically provides a reference framework for compliant on-chain equity. Its core idea is consistent with the logic that has been verified in the market: the shareholder register is uniformly managed by a regulated transfer agent to achieve transparency in the restricted transfer process and ensure that the legal effect of on-chain tokens is consistent with that of physical equity.

Figure 11: Centrifuge Equity Tokenization Architecture Diagram

Source: Centrifuge official website

Of particular note is Centrifuge's first disclosed case study: a collaboration with Caesar AI. This partnership positions Centrifuge's strategy towards a broad range of issuers (especially cryptocurrency-native startups) rather than large unicorn companies. If this model becomes a replicable implementation template, it will significantly accelerate the maturation of TaaS offerings for Web2 enterprises, providing rich infrastructure for the large-scale expansion of native collaborative models.

7. Key Challenges: Three Types of Bottlenecks Determine the Industry's Upper Limit

Although the tokenization of unlisted equity has a clear narrative space and potential incremental value, from the perspective of feasibility and scalability, there are still several hard constraints in this field. The key bottlenecks that currently determine the upper limit of industry expansion can be summarized into three categories: compliance squeeze, insufficient liquidity depth, and uncertainty about the final outcome of IPOs.

7.1. Compliance Pressure: Dual Pressure from Regulators and the Target Company's Legal Department

Compared to the tokenization of listed stocks, the compliance complexity of tokenization of unlisted equity is significantly higher because it faces the combined effects of government compliance supervision (SEC) and legal constraints on the target company.

On the one hand, product issuance and trading may involve securities laws and licensing systems (such as the SEC regulatory framework); on the other hand, more decisive constraints often come from the equity management constraints of the target company, especially the transfer restrictions clauses in the shareholder agreement. Under structures such as SPV indirect holding, the issuing platform attempts to achieve "indirect equity transfer" at the LP level through structural design, but this practice may violate the transfer agreement and trigger company-side measures.

Twitter: https://twitter.com/BitpushNewsCN

BitPush Telegram Community Group: https://t.me/BitPushCommunity

Subscribe to Bitpush Telegram: https://t.me/bitpush