Written by: Huang Wenjing and Yan Xuesong

introduction

Looking back from the beginning of 2026, 2025 was a year that reshaped the crypto world—Bitcoin hit new highs, key projects were launched, and the market steadily rose rationally. Even more profound changes came from the maturation of global regulation: stablecoins, permissioned trading, and anti-money laundering rules were clearly implemented in many countries, injecting much-needed certainty into the industry.

The EU's MiCA regulation, which came into full effect at the end of 2024, entered a critical implementation phase in 2025. This unified framework, covering 27 countries, serves as a guiding light, defining compliance boundaries and illuminating new growth opportunities. With the transition period officially ending in many countries in the fourth quarter of last year, the European market has undergone a profound transformation – 68 new licensed institutions have entered the market, traditional VASPs have successfully transformed into CASPs, and new forces have made a strong debut.

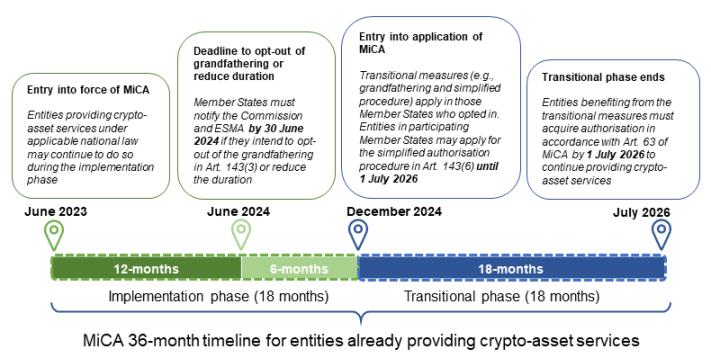

MiCA timeline for 36 months for licensed entities that have provided crypto asset services

(Source: Latest guidance from the ESMA official website)

This article will start with the latest regulatory trends, analyze the types and characteristics of newly licensed institutions, interpret the differentiated paths taken by different countries, and reveal the next evolutionary trend of the industry. It will help you see through the changes and gain insight into the true pulse of the European market.

A map of 68 newly licensed institutions and the new landscape of the European market

1. The logic of service licenses: a license ≠ omnipotence

The core of the MiCA regulation is to set a uniform entry threshold for crypto asset service providers across Europe. Licensed entities that pass the review and approval of their respective national authorities (NCAs) can legally operate throughout the EU through the "EU Passport" mechanism. According to MiCA, licensed institutions can provide 10 types of services, including custody, operating trading platforms, exchange, order execution, and investment advice.

However, the scope of authorization for a license varies highly, depending on the service mix selected at the time of application. Common business logic includes:

- Platform-based services: Operating a trading platform typically requires supporting services such as custody, exchange, and order execution to ensure a complete trading loop.

- Asset management services: Portfolio management often needs to be combined with order execution to achieve dynamic rebalancing of managed assets.

- Independent services: Custody, investment advice, transfer, etc. can also exist independently, which is suitable for institutions that focus on a niche area.

It's important to note that the above possible service combinations are not mandatory, but rather represent a general business logic: large, comprehensive platforms (such as Coinbase and Kraken) typically apply for multiple services because they can support each other to create a closed-loop user experience. However, smaller or specialized institutions can focus on a single service, such as providing custodial wallets, independent advice, or cross-chain bridges, which is perfectly acceptable.

In practice, various business combinations mainly emerge in scenarios where one wants to provide a "one-stop" service. If one only wants to operate a very simple business or has a limited budget, it is entirely possible to avoid relying on other services, saving both money and effort. This also means that when an organization claims to hold a MiCA license, it is best not to assume that it can "do everything."

Understanding this helps us to view the strategies and capabilities of newly licensed institutions more objectively and to clarify the following common misconceptions:

- Does holding a MiCA license mean complete compliance and no risk? — Not at all. A license only means that one can conduct business within the authorized scope, and does not exclude other operational and market risks.

- Does an organization claiming to have a MiCA license equate to possessing all service qualifications? — Not necessarily. Their actual business may be limited to a single aspect such as custody, exchange, or advice.

- Are institutions that provide portfolio management necessarily able to execute trading orders? — Not necessarily. Such institutions can achieve trade execution by partnering with licensed third-party service providers.

2. Key characteristics of newly licensed entities in Q4

The 68 newly licensed institutions in the fourth quarter of 2025 were directly due to the concentrated end of the MiCA unified regulatory transition period in most member countries. Institutions that previously relied on the existing VASP regimes in each country faced the final deadline of "licensing or exiting the market," thus forming a concentrated wave of compliance applications and conversions.

This phenomenon is both a natural result of the regulatory transition period and a reflection of the strategic choices made by institutions in adapting to the new regulations. Whether international giants or local upstarts, all have completed their identity transformation before the deadline, reflecting the clear trend of the crypto industry evolving in layers and integrating its ecosystem in the process of standardization.

- Total number surged: The total number of licensed entities reached 133, with 68 new licensed entities added in the fourth quarter—a significant increase, far exceeding the growth rate of the first three quarters.

- Service concentration: The main service types are hosting, transfer and exchange, with a low proportion of licensed entities holding full-service/multi-service licenses and a high proportion of narrow-domain authorizations.

- Regional concentration: Approximately 60% are concentrated in Western Europe (Germany, France, Netherlands, Austria, and Ireland, totaling 42 companies), while Eastern Europe and EEA countries (Liechtenstein) are becoming more active.

- The Rise of the Nordic Countries: The Nordic region has seen a "dark horse" emerge: Finland increased from 1 to 5 companies in Q4, and Sweden went from having none to having one.

- Cross-border activity: Passport utilization is high, and most institutions cover more than 10 EU countries.

The new tiers of licensed entities: the tension between emerging and traditional ones

Overall, these new institutions can be broadly categorized into three types: giants, midstream players, and newcomers. This classification is based on their size, market influence, and service breadth.

1. Giants: Leading Market Unification

Among the licensed institutions in the fourth quarter, the entry of industry giants is particularly noteworthy. These institutions typically tend to apply for more than five types of service licenses to build a "one-stop" platform covering multiple functions such as custody, trading, and exchange, in order to quickly respond to the needs of the EU single market.

UK-based digital bank Revolut has obtained a license in Cyprus to offer six services, including custody, trading platform operation, and fiat currency exchange, potentially bringing its more than 50 million users to the crypto world. Global exchange KuCoin has secured five service licenses in Austria, covering core functions such as custody, exchange, and underwriting; meanwhile, Blockchain.com (Malta) and crypto bank AMINA EU (Austria) have also entered the market as integrated service providers.

Features:

- Economies of scale: These licensed entities typically enjoy international or continental reputations, a large user base, substantial capital, and mature technology. They are expected to expand rapidly and capture a significant share of the EU's unified market.

- Internal integration: Market entry is often achieved by establishing subsidiaries, thus strategically avoiding external risks.

2. Midstream: The power of steady progress

Alongside the giants are some midstream licensed entities, which typically have a stable and medium-sized user base and mature technology in a certain area, and previously relied on national-level VASP registration.

For example, Bitonic BV, founded in 2012, is the oldest and largest local Bitcoin broker in the Netherlands. It has long focused on the domestic market, offering stable and reliable services with virtually no major security incidents, earning the trust of individual clients. On November 21st, the company obtained a MiCA license, authorizing it to provide custody, exchange, order execution, and transfer services, representing the standard development path for mainstream platforms in the Netherlands—most other newly licensed institutions in the Netherlands also possess these types of permissions.

Another typical example is Renta 4 in Spain, an established bank that is undergoing transformation and has a moderate size and good reputation in the traditional investment field. It has been approved to provide custody and transmission services.

The advantage of these mainstream institutions lies in their in-depth understanding of the local market. They typically choose a medium-range service package while keeping compliance costs under control, thus avoiding direct competition with large international platforms. This makes them a trustworthy choice for ordinary users.

Features:

- After deepening its local presence, it is expanding: from single-country services, or gradually moving towards multiple passports.

- Medium-sized service mix: 3-5 service categories.

- Low risk: There is already a compliance foundation and high user loyalty.

3. New Players: Rising Stars

Emerging or localized licensed entities are often small in scale, and the emergence of such institutions gives the impression of a "catch-up" behavior in fear of missing the last train of MiCA.

However, they also fill some local gaps. Typical examples include six local German banks (Volksbank Mittlerer Schwarzwald eG, Hannoversche Volksbank eG, VR TeilhaberBank Metropolregion Nürnberg eG, etc.), all approved in December, but only capable of providing order execution services. The advantages of these emerging institutions lie in their flexibility and cost advantages.

Features:

Narrow domain services: Focusing on specific pain points and needs in the local encryption market.

Potential risks: Small user base, limited business volume or not yet started, making it easy to become a future acquisition target or difficult to fulfill compliance obligations in the long term.

Distribution of newly licensed entities: the underlying market drivers

The styles of institutions vary greatly across different regions, reflecting differences in local economies, user habits, and regulatory environments. Western European countries such as Germany, France, and the Netherlands dominate new additions, while Eastern European countries such as Slovakia, Slovenia, and Latvia offer more retail-oriented services.

1. Regional differences:

Eastern Europe: Clearly retail-oriented, with a concentrated push for compliance.

In Q4, Eastern European countries added 10 new licensed institutions, primarily from Slovakia, Slovenia, and Latvia. These institutions generally focus on retail service packages, commonly offering "custody + exchange + transfer" services, and are less involved in trading platform operations. For example, Slovakia's FUMBI holds more than five service licenses, while Latvia's BlockBen focuses on the "gold tokenization" niche market.

This phenomenon mainly stems from:

- Centralized compliance transformation before the end of the transition period;

- The local market is dominated by retail investors, with low participation from institutional funds.

- The lower compliance costs compared to Western Europe attract many local startups and SMEs.

- With limited regulatory and approval resources, Q4 will be dedicated to processing the backlog of applications.

New licensed entities in Western European countries: taking France and Germany as examples

Germany and France are the main representatives of newly added institutions in Western Europe. Germany added 16 institutions, the vast majority of which are traditional banks that only provide single order execution or transmission services; France added 5 institutions, among which the encryption division of Société Générale, one of the "Big Three" French banks, only applied for custody and transfer services, showing the characteristic of "narrow-domain compliance".

Despite Western Europe's well-developed financial infrastructure and institutional capital, high compliance costs have led many institutions to streamline their services to control initial investment. This also illustrates that the activity in the crypto market is not entirely in sync with the size of the regional economy.

EEA Country - Liechtenstein

The emergence of this new name is eye-catching. There are only two registered licensed entities in the country, both offering services centered around custody, giving it a "small but sophisticated" high-end positioning. This is because its neutral and low-tax environment attracts private banks and asset management firms. Furthermore, even though Liechtenstein is not an EU member state, the MiCA still applies, making the passport valuable; the market is niche and high-end, with investors primarily being professional players such as family offices.

2. Industry consolidation trend: Hidden restructuring rather than explicit mergers and acquisitions

Although no significant M&A deals were seen in the fourth quarter, the industry was quietly consolidating. Many giants chose to establish their own EU subsidiaries instead of acquiring others, thus maintaining full control over their businesses while avoiding the complex due diligence and approval risks.

The report shows that some small organizations were acquired by mainstream platforms throughout 2025, and in the fourth quarter, more organizations were "running on their own"—applying independently before the end of the transition period.

Conclusion

According to incomplete statistics and actual data feedback, the success rate of MiCA applications is not as high as expected. The regulatory authorities' review approach still emphasizes substance: licenses are not created by piling up application materials, but are the natural result of a genuine and reliable business model.

- For investors, the MiCA license is not a one-time "protective shield." The license is just the starting point, not the end. Obtaining the license does not necessarily mean that the business is mature. Investors need to carefully examine whether a specific service is actually provided and which countries the passport covers before they can use the service with greater confidence.

- For operators, the large number of new entities in certain countries or regions does not necessarily mean that the regulatory difficulty is lower. Rather, it may be a business strategy or expedient measure tailored to the existing service providers.

The actual expenses involved in obtaining a MiCA license should not be underestimated. Applicants should ask themselves: do I really need this license? While a proactive approach to compliance is commendable, clarifying one's own positioning and long-term goals may be a wiser move. Hopefully, this article will help you understand the European crypto market and find your own opportunities amidst change.