Author: KarenZ, Foresight News

Original title: Strategy's financial report flashes red after a massive loss of tens of billions! What did the top management say?

The cryptocurrency market is currently mired in a severe correction. As Bitcoin's price retreated to $60,000, market sentiment quickly turned to extreme panic.

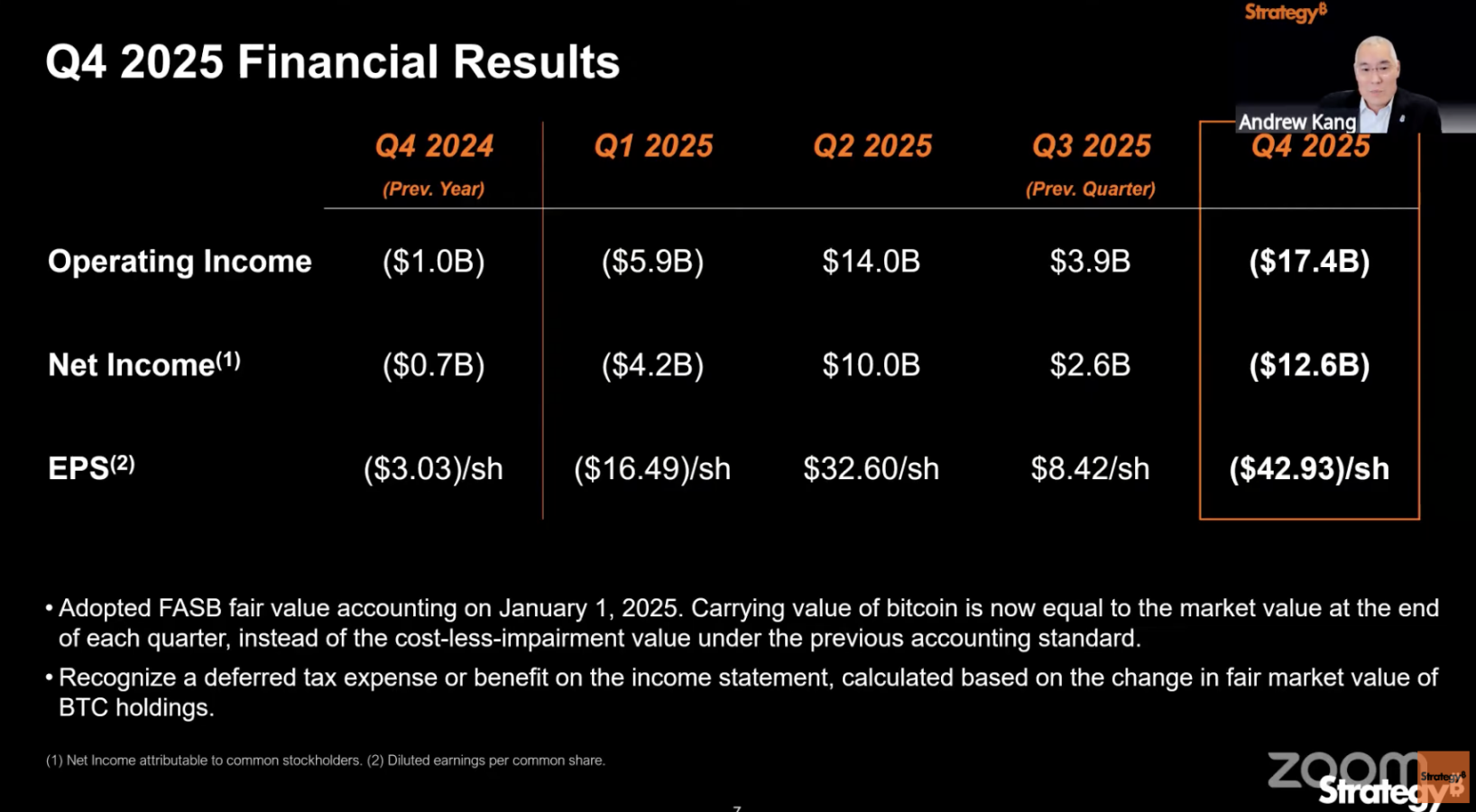

At this turbulent time, Strategy (formerly MicroStrategy), the world's largest corporate Bitcoin holder, released its Q4 2025 financial report, which undoubtedly added insult to injury and poured a bucket of cold water on the already sluggish market: a net loss of $12.4 billion in a single quarter.

On the day the financial report was released, Strategy's stock price plummeted by about 17%. As of now, its stock price has fallen by nearly 80% from its all-time high in November 2024.

From a once-star company that soared with its "Bitcoin Treasury Strategy" to now being plagued by huge losses and its stock price has been halved again and again, Strategy's situation is a true microcosm of the current turmoil in the cryptocurrency market. On one hand, there are huge losses on paper, and on the other hand, there is an almost obsessive hoarding of coins. This company is staging a high-stakes gamble on the future of the enterprise with a series of contradictory data.

Key data: Frenzied accumulation of shares amidst huge losses

The core contradiction in Strategy's Q4 2025 financial report lies in the stark contrast between the record high book losses and the all-time high in Bitcoin holdings.

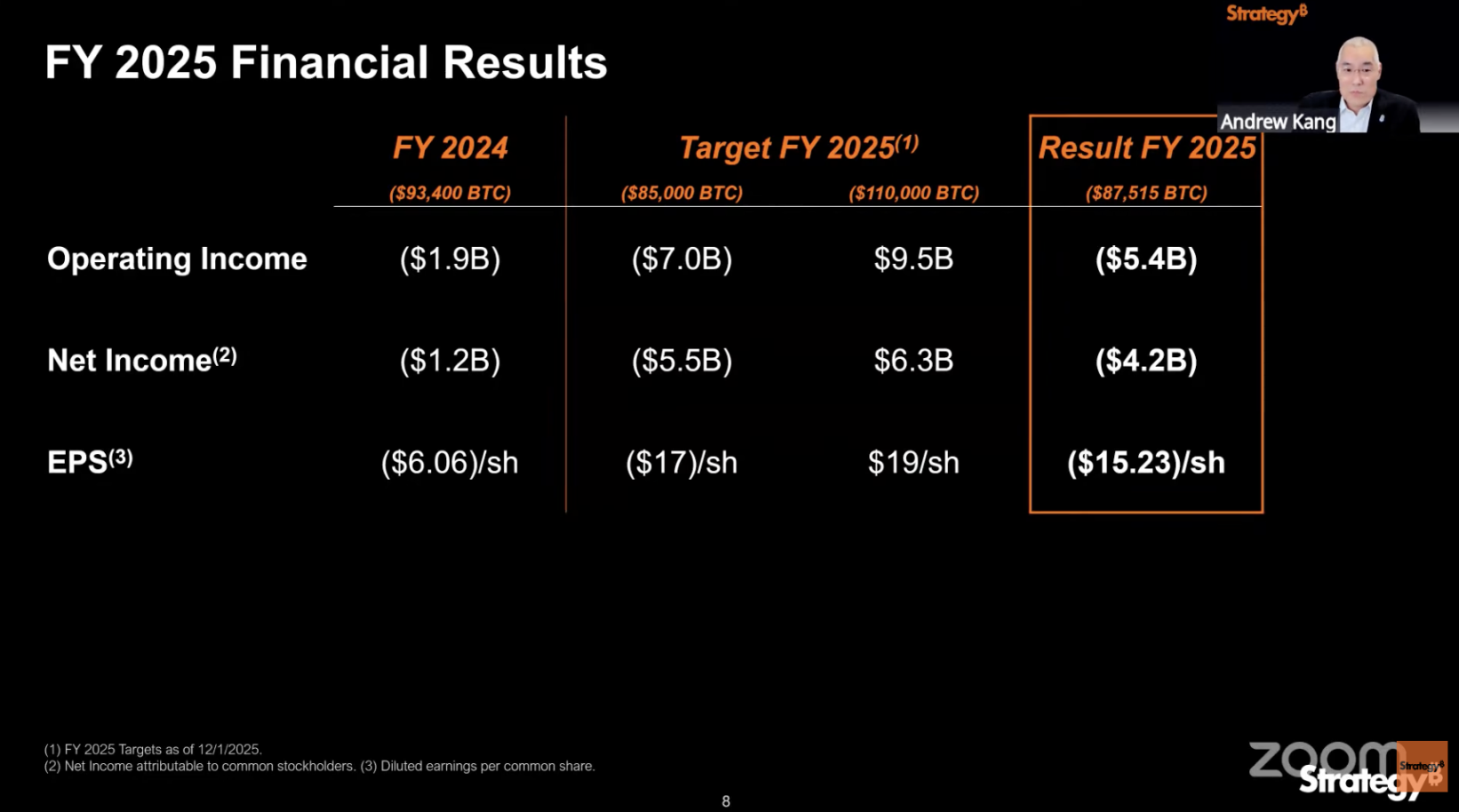

1. Huge book losses under fair value accounting standards: In the fourth quarter of 2025, Strategy's operating loss reached a staggering $17.4 billion, with a net loss of $12.4 billion. This was mainly due to the fair value accounting standards adopted by the company starting January 1, 2025. According to this standard, the company is required to reassess all its Bitcoin holdings at market prices at the end of each quarter. Price fluctuations are directly reflected in the profit and loss statement. The continued correction in Bitcoin's value directly translated into book losses, becoming the most direct "negative factor" in the financial report.

2. A Unwavering Commitment to Buying Bitcoin Against the Trend: Despite market volatility, Strategy continued its aggressive buying spree, purchasing a substantial 41,002 Bitcoins in January 2026. As of February 1, 2026, Strategy held 713,502 Bitcoins, representing approximately 3.4% of the total Bitcoin supply, firmly establishing itself as the world's leading corporate Bitcoin holder.

3. Super Fundraising Machine: In fiscal year 2025, Strategy raised more than $25.3 billion in total capital, accounting for about 8% of the total equity financing in the United States that year.

4. Risk buffer of special reserves: As of February 1, 2026, Strategy has $2.25 billion in US dollar reserves specifically for covering preferred stock dividends and debt interest payments over the next 2.5 years, attempting to alleviate market concerns about its cash flow pressure.

In terms of holding costs, Strategy's original total cost of holding Bitcoin reached $54.26 billion, with an average cost of $76,052 per coin. With the current price of Bitcoin at approximately $65,000, the company's unrealized loss on its Bitcoin holdings exceeds $7.8 billion.

The marginalized "core business" and the amplified "leverage"

Ironically, Strategy's traditional core business—enterprise analytics software—has become a nearly forgotten footnote in its financial statements, its scale and contribution being vastly different from the size of its Bitcoin strategy.

In the fourth quarter of 2025, although the company's software business maintained positive growth, the data performance was relatively flat: total revenue was US$123 million, an increase of only 1.9% year-on-year; subscription service revenue was US$51.8 million, an increase of 62.1% year-on-year; and the overall gross profit in the fourth quarter was US$81.3 million, with the gross margin remaining at a relatively high level of 66.1%.

The data clearly shows that although the software business has stable profitability and a high gross profit margin, its revenue is only in the hundreds of millions. Compared with the company's tens of billions of yuan in fundraising, tens of billions of yuan in Bitcoin holding costs, and tens of billions of yuan in quarterly losses, the marginal contribution of this main business is almost negligible.

For Strategy today, the company's core resources and strategic focus have long been completely tilted towards Bitcoin. Through complex financial instruments such as stocks, bonds, and preferred shares, Strategy provides investors with leveraged Bitcoin exposure. It has also become completely "Bitcoin's shadow," with its development deeply tied to Bitcoin's price; its rise and fall are intertwined.

What happens when convertible bonds mature?

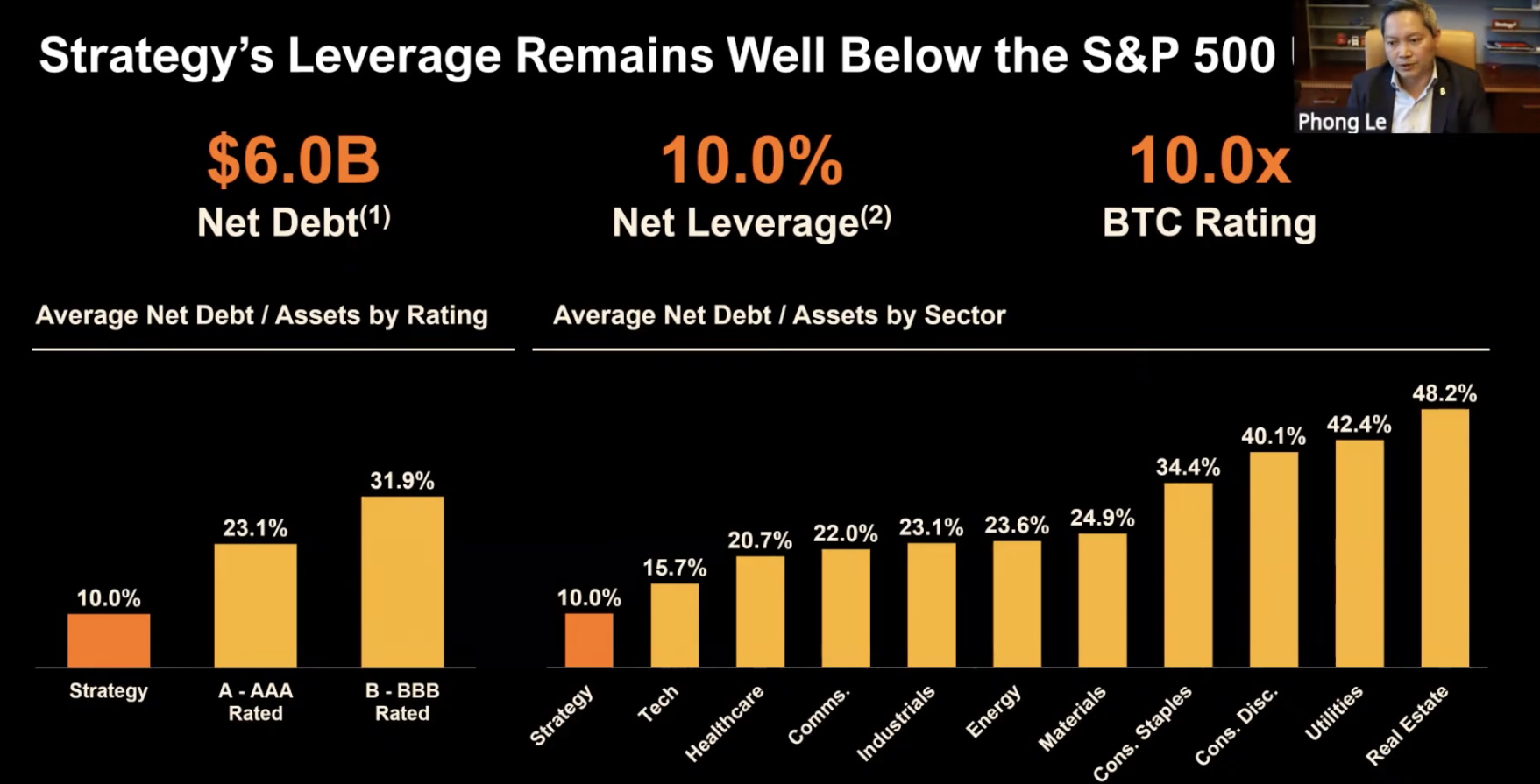

In the latest earnings call, Phong Le stated, "Strategy currently has $6 billion in net debt, with a leverage ratio of around 13%, which is only half that of investment-grade firms and one-third that of high-yield firms. In an extreme scenario, if the price of Bitcoin drops by 90% to $8,000, our Bitcoin reserves will equal our net debt. At that point, we will be unable to repay convertible bonds with our Bitcoin reserves and will consider restructuring, issuing new shares, or issuing additional debt."

In addition, Phong Le hopes that the company will gradually become equity-based. If equity-based equity cannot be achieved at that time, other ways will be sought to restructure the debt, with the aim of sustainably reducing leverage, avoiding selling coins, and continuing the Bitcoin accumulation strategy.

When the flywheel becomes loose

Strategy's "Bitcoin flywheel" model is built on an extremely fragile assumption: that the price of Bitcoin will rise in a long-term spiral and that the capital market will always be willing to provide premium financing for its companies, thus creating a positive cycle that drives the company's stock price and holding size to grow in tandem.

However, when the price of Bitcoin fell below its average holding cost ($76,000), the risks and paradoxes faced by Strategy were exposed.

STRC's high dividend payouts: High returns correspond to high risks

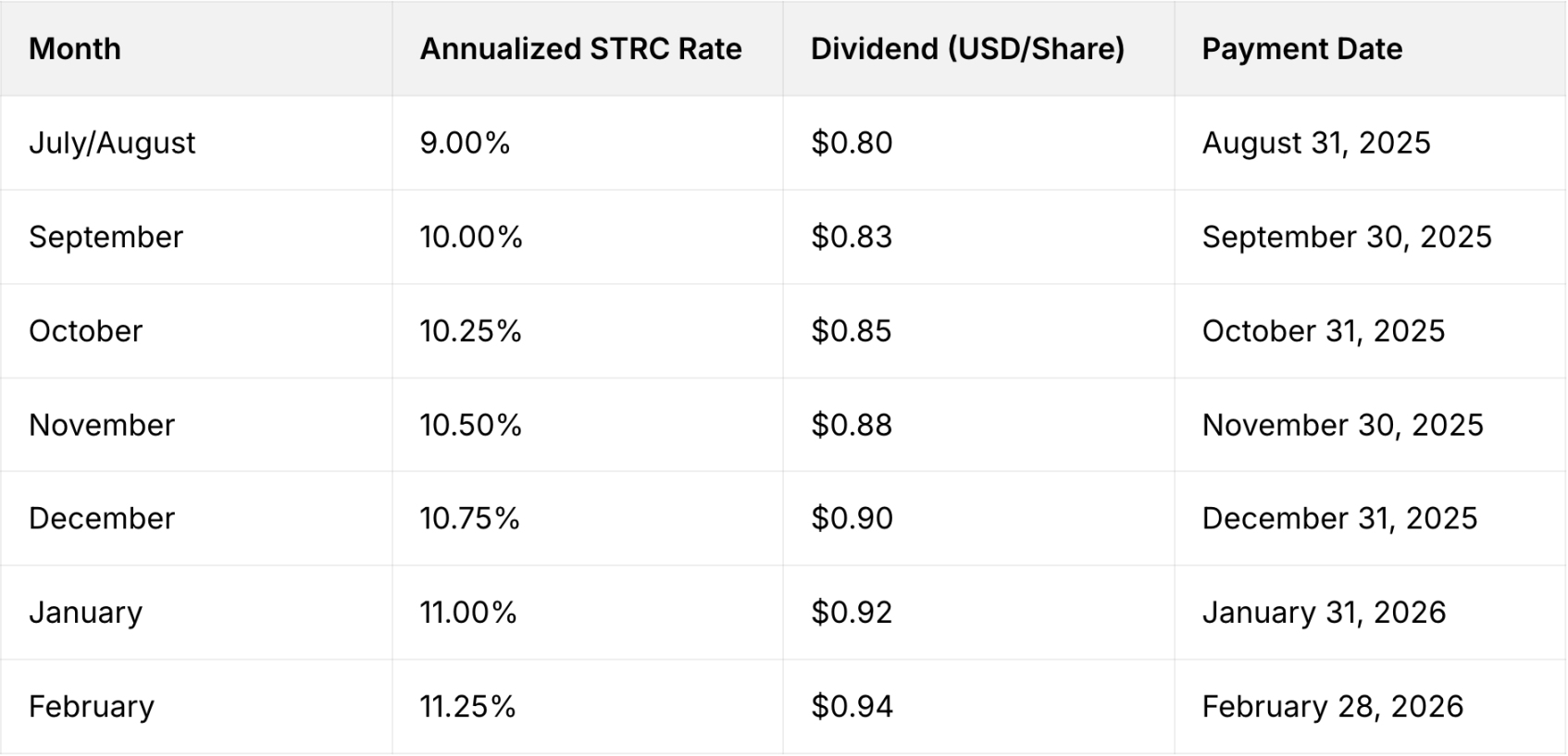

Strategy's perpetual preferred stock, STRC, currently has a dividend yield of 11.25%, and this yield has been increasing since July 2025.

Strategy designed this variable mechanism to keep the price of STRC as stable as possible around its $100 face value, reduce volatility, and position it as an alternative to "short-term high-yield credit" or "high-yield savings account".

In the current low-interest-rate environment, a nominal yield of 11.25% is indeed very attractive, especially for investors seeking high fixed income. However, the fundamental logic of the capital market has never changed: high returns inevitably come with high risks. Behind STRC's high dividends lies enormous uncertainty deeply tied to Strategy's Bitcoin strategy.

Strategy's core strategy is "Bitcoin leverage + financing expansion," and its solvency is highly dependent on: long-term Bitcoin price increases and continuous financing to buy more BTC through the issuance of MSTR common stock, other preferred stock, or debt.

If the Bitcoin bear market extends, mNAV remains depressed or even trades at a discount, or equity financing becomes more difficult, the reserves could be depleted rapidly. Although the company has established $2.25 billion in dollar reserves as a buffer, this is merely a 2.5-year insurance policy for this high-stakes gamble.

The market has already factored in some of these concerns: the price of STRC is below its $100 face value, currently at $93.67.

With mNAV compressed to 1.07, will financing channels be smooth?

The core driving force behind Strategy's ability to issue unlimited shares to buy Bitcoin lies in its mNAV metric, a key indicator used to measure its stock valuation relative to its Bitcoin reserves. When mNAV > 1, it means that the market values Strategy higher than the value of its Bitcoin holdings (i.e., premium trading), and investors are willing to pay an additional premium for its "Bitcoin leveraged strategy."

Strategy's current mNAV has compressed to 1.07. If it falls below 1, its funding channels may be forced to close. At that point, Strategy may lose its ability to support the price and cover margin calls, becoming a complete prisoner of Bitcoin's price fluctuations.

Contrary to his remarks at the latest meeting, Strategy CEO Phong Le stated in a November 2025 interview with What Bitcoin Done that selling Bitcoin would be "mathematically" reasonable if the company's mNAV fell below 1 and funding options dried up. However, he clarified that this would be a last resort, not a policy adjustment.

Negative feedback loop?

For Strategy, the most terrifying thing is not the current huge losses, but the potential negative feedback loop that could be triggered, which is the scenario that no player in the crypto market wants to face:

Bitcoin price decline → Company net assets shrink → mNAV falls below 1, premium disappears → Unable to obtain new funds through financing → Unable to pay high interest and dividends → Forced to sell Bitcoin to raise funds → Increased Bitcoin selling pressure, further price decline → Net assets shrink further…

Can favorable policies and technological promises rebuild confidence?

During the earnings call, Michael Saylor did not focus on the short-term negative impact of the company's quarterly loss. Instead, he outlined a long-term positive blueprint for Bitcoin's development, centering on the comprehensive shift in US policy and the accelerated adoption by the financial industry. At the same time, he addressed the market's biggest concerns about quantum technology risks and implementation plans, rebuilding market confidence in the company's Bitcoin strategy.

Michael Saylor emphasized that Bitcoin's current development is experiencing an unprecedented period of dual policy and financial benefits. On the policy front, the US government's attitude towards digital assets has undergone a fundamental shift from skepticism to acceptance. The president and 12 cabinet members have all explicitly expressed their support for Bitcoin, and bipartisan consensus has been reached on the regulation and adoption of digital assets, placing the US among the leading countries in global digital asset development.

On the financial front, Bitcoin's industry adoption has seen explosive growth: major banks have launched full-chain services for Bitcoin trading, lending, and custody; fintech companies continue to increase their Bitcoin investments; and the dual entry of public markets and traditional financial institutions has continuously strengthened Bitcoin's financial attributes, leading to increased liquidity and acceptance.

Michael Saylor also gave a direct response to the various FUD sentiments that are prevalent in the market, especially focusing on concerns about the core technology of quantum computing: the commercial threat of quantum computing to Bitcoin will not be apparent for at least another 10 years, and the Bitcoin community has the ability to upgrade global consensus, which is sufficient to cope with future technological challenges.

Michael Saylor further stated that Strategy will proactively shoulder industry responsibility by launching a global Bitcoin security initiative, uniting global resources in the fields of cybersecurity and cryptocurrency security, researching and launching consensus solutions for quantum computing and emerging security threats, and promoting the healthy and stable development of the entire cryptocurrency industry.

summary

If the market continues to decline, the $17.4 billion quarterly operating loss and $12.4 billion net loss may only be the beginning of Strategy's predicament.

The real test lies in whether faith can overcome gravity when market panic spreads, the "premium" disappears, and new funds dry up. For investors, Strategy now may be an extremely high-risk, high-reward option contract: if you bet right, the price of Bitcoin will rebound, the flywheel will start spinning again, and investors will reap rewards; if you bet wrong, a negative feedback loop will start, the company will fall into crisis, and investors will face heavy losses.

The outcome of this high-stakes gamble on the company's future remains to be seen, but Strategy has already sounded the alarm for the entire cryptocurrency industry—in the midst of frenzied market sentiment, excessively fanatical faith and unrestrained leverage may face a backlash from reality.

Twitter: https://twitter.com/BitpushNewsCN

BitPush Telegram Community Group: https://t.me/BitPushCommunity

Subscribe to Bitpush Telegram: https://t.me/bitpush