Compiled by: Block unicorn

In short: While current money market protocols (such as Aave, Morpho, Kamino, and Euler) serve lenders well, they fail to serve a broader borrower base, particularly institutions, due to the lack of fixed borrowing costs . Growth has stagnated because only lenders benefit.

From the perspective of money market agreements, P2P fixed interest rates are a natural solution, while interest rate markets offer an alternative that is 240-500 times more capital efficient.

P2P fixed rates and the interest rate market complement each other and are both crucial to each other's success.

Insights from leading agreements: All agreements aim to provide borrowers with fixed interest rates.

The team's roadmap at the beginning of the year usually sets the tone for the next stage of development.

Morpho , Kamino, and Euler Labs are currently the leading on-chain money market players, with a total value locked ( TVL ) of $10 billion. Looking at their 2026 roadmaps, one obvious theme stands out: Fixed Rate .

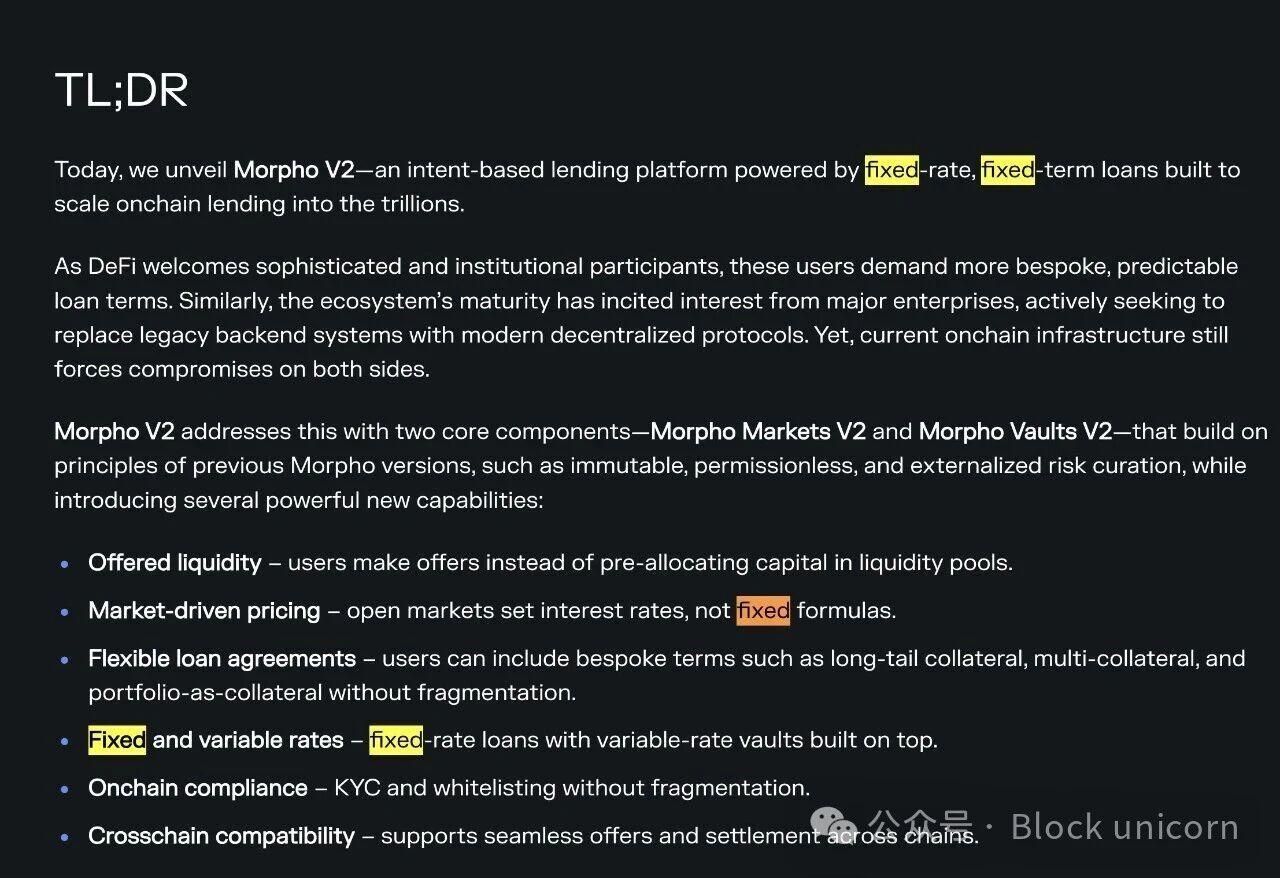

From Morpho

Morpho V2 Briefing

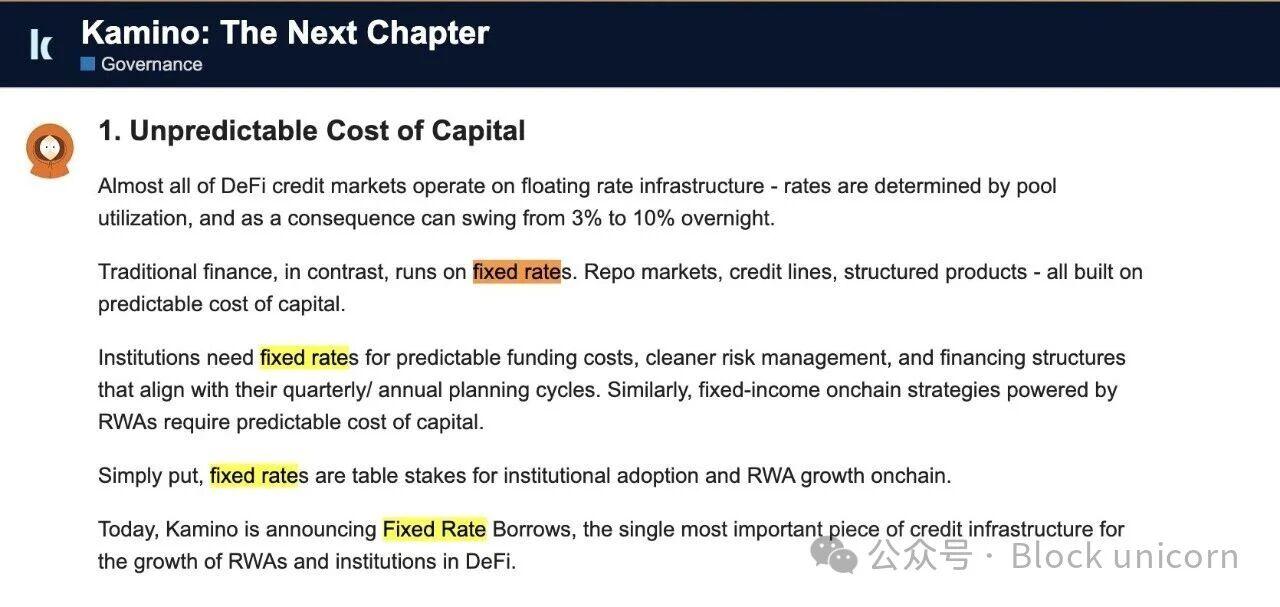

From Kamino

Kamino 2026 Plan

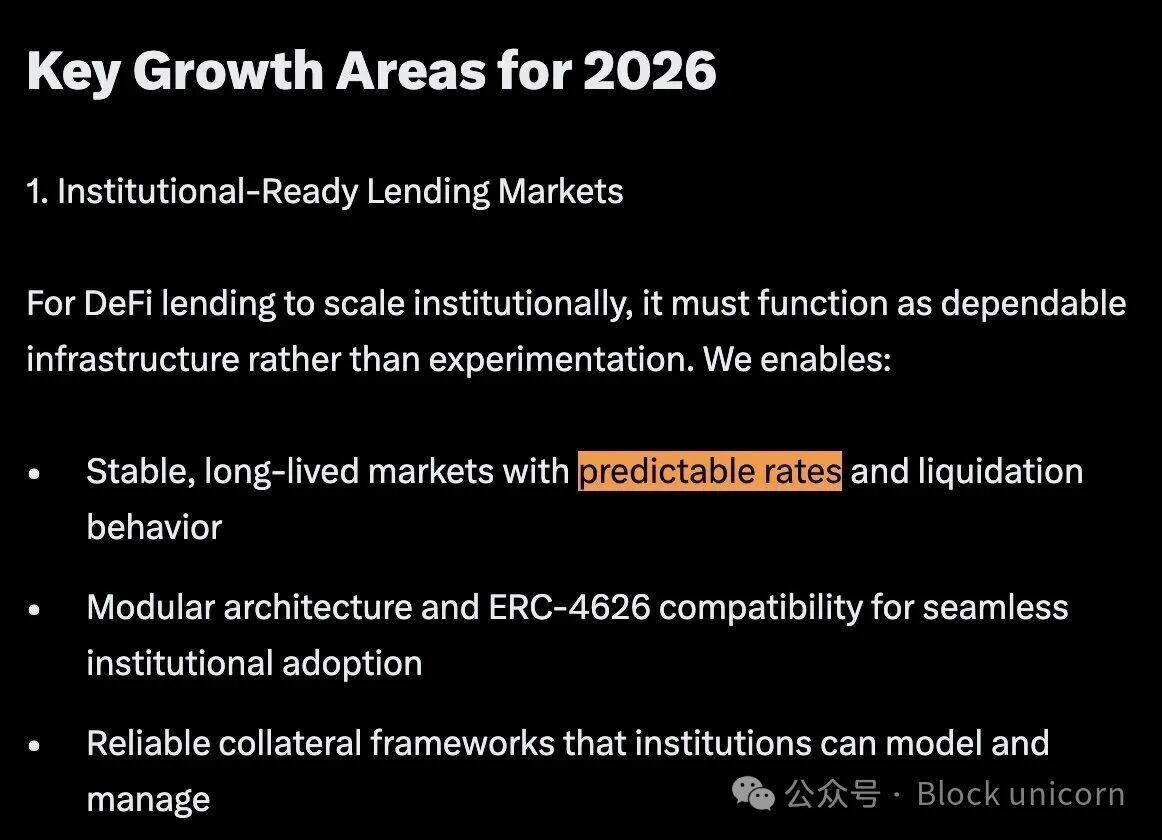

From Euler

Euler 2026 Roadmap

In the 2026 announcements released by Morpho, Kamino, and Euler, the phrase "fixed rate" or " predictable rate" appeared 37 times. This was the most frequently used word in their announcements (excluding filler words) and was listed as a top priority in all three roadmaps.

Other recurring keywords include: institution, RWA , credit.

So, what happened?

In the early stages of DeFi: the borrower's fixed interest rate was irrelevant.

Early DeFi was fun and experimental for developers. But for users, early DeFi can be summed up in two sentences: surreal speculation and terrifying hacking.

Surreal speculation

From 2018 to 2024, DeFi was like a "casino on Mars" detached from reality. Liquidity was primarily driven by early retail investors and speculation. Everyone was chasing four-figure annualized yields (APY). Nobody cared about fixed-rate lending.

Markets are extremely volatile and rapidly changing. Liquidity lacks stickiness . Total Value Locked (TVL) fluctuates wildly with market sentiment. While demand for fixed-rate borrowing is low, demand for fixed-rate lending is even lower.

Lenders prefer the flexibility to access funds at any time. Nobody wants to be locked up for a month—because in a rapidly changing and nascent market, a month feels like an eternity.

Terrible hacking attack

From 2020 to 2022, hacking incidents occurred frequently. Even blue-chip protocols were not spared: Compound suffered a major governance vulnerability in 2021, resulting in tens of millions of dollars in losses. During this period, losses caused by DeFi vulnerabilities totaled billions of dollars, exacerbating institutional investors' concerns about the risks of smart contracts.

Institutional investors and high-net-worth individuals lack trust in the security of smart contracts. Consequently, participation from more conservative fund pools remains low.

Conversely, institutions and high-net-worth individuals are choosing to borrow from off-chain channels, such as Celsius, BlockFi, Genesis, and Maple Finance, to mitigate the risks associated with smart contracts.

At the time, Aave was not the most secure DeFi protocol, so there was no such thing as "using Aave directly".

Catalyst for change

I'm not sure if this was intentional or just a coincidence, but we often refer to platforms like Aave and Morpho as "lending protocols," which is quite accurate—even though both lenders and borrowers use them.

The name "loan agreement" is actually quite apt: these platforms excel at serving lenders, but are clearly lacking in serving borrowers.

Borrowers want fixed borrowing costs, while lenders want the ability to access funds at any time and receive floating interest rates. The current agreement favors lenders but disadvantages borrowers. Without fixed-rate lending options, institutions won't engage in on-chain lending, and the two-sided market cannot develop—which is why these platforms are now actively working to build fixed-rate functionality.

Even within this clearly lender- biased structure, change requires addressing user pain points or improving the product. Over the past year and a half, DeFi has accumulated both of these aspects.

In terms of pain points, fixed-income cyclical strategies are constantly affected by fluctuations in borrowing costs, while the premium between off-chain fixed rates and on-chain floating rates is also widening.

User pain point 1: Fixed income cycle

Traditional finance (TradFi) offers a wide range of fixed-income products. Prior to 2024, DeFi had virtually no revenue-sharing mechanisms until Pendle and liquid staking protocol began splitting the returns from ETH liquidity staking.

When using revolving fixed-income tokens (Pendle PT), the pain caused by interest rate volatility becomes apparent – the 30-50% annualized yield (APY) promised by revolving strategies is often eroded by interest rate fluctuations.

I've personally tried automatically adjusting these strategies for opening and closing positions based on interest rate changes, but each adjustment incurs multiple layers of fees: the underlying yield source, pendle fees, money market fees, and gas fees. Clearly, volatile lending rates are unsustainable—often resulting in negative returns for me. Dynamically pricing lending costs based on on-chain liquidity introduces volatility far exceeding acceptable levels.

This pain is merely the prelude to everything that will happen once private lending is on-chain. Private lending generally tends towards fixed-rate lending because the real world requires certainty. If DeFi is to shed its image as a "casino on Mars"—detached from real economic activity—and truly support meaningful business activities, such as GPU-backed loans and credit lending from trading firms, then fixed rates are imperative.

User pain point 2: Widening premium between fixed and floating rates

On-chain lending liquidity has been steadily increasing due to the superior services offered to lenders by lending protocols—flexible withdrawals, no KYC required, and easy programming.

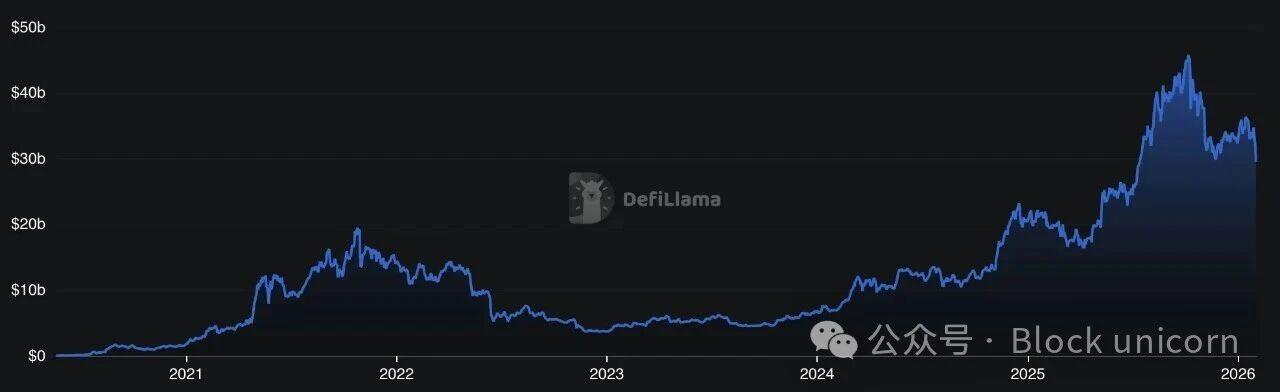

Aave's TVL over the years. The chart shows that its growth rate is approximately twice that of Bitcoin's price growth rate.

As lending liquidity increases, the speed of floating-rate lending on these protocols decreases. While this may seem advantageous to borrowers, it is irrelevant to institutional borrowers—who prefer fixed-rate loans and are accessing them through off-chain channels.

The real pain point in the market lies in the widening gap between off-chain fixed-rate borrowing costs and on-chain floating rates. This gap is quite significant. Institutional investors pay an average premium of 250 basis points for fixed-rate borrowing, while the premium can reach as high as 400 basis points when using blue-chip Altcoin as collateral. Based on an average annual interest rate (Aave) of 4%, this translates to a premium of 60% to 100%.

Aave approximately 3.5% vs Maple approximately 8%: The premium for fixed-rate cryptocurrency mortgages is approximately 180 to 400 basis points.

On the other hand, on-chain yields are also being compressed. Because the current lending market is structurally biased towards lenders, it attracts more lenders than borrowers—which ultimately hurts lender yields and hinders protocol growth.

Product Progress: DeFi Becomes the Default Choice for Lending

In terms of progress, Morpho has been integrated into Coinbase, becoming its main source of revenue; while Aave has become the cornerstone of protocol fund management, retail stablecoin savings applications, and new stablecoin banks. DeFi lending protocols provide the most convenient way to obtain stablecoin yields, with liquidity continuously flowing into the blockchain .

As TVL increases and revenue decreases, these lending protocols are actively iterating to become better "lending protocols" that can better serve borrowers and balance the two-sided market.

Meanwhile, DeFi protocols are becoming more modular—a natural evolution from Aave's "one-size-fits-all" liquidity pool model (note: although I believe the liquidity pool model will continue to be in demand for a long time—this could be the topic of another future article). With Morpho, Kamino, and Euler leading the modular lending market, loans can now be more precisely configured based on collateral, LTV, and other parameters. This has given rise to the concept of independent credit markets. Even Aave v4 is upgrading to a hub-and-spoke modular market structure.

The modular market structure has paved the way for the introduction of new types of collateral, such as Pendle PT, fixed-income products, private credit, and risk-weighted assets (RWA), further amplifying the demand for fixed-rate lending.

Mature DeFi: The money market thrives through the interest rate market

Market gap:

Borrowers strongly prefer fixed interest rates ( with well-developed off-chain services) .

Lenders strongly prefer floating interest rates and the flexibility to withdraw funds at any time (due to well-developed on-chain services).

If this market gap is not bridged, the on-chain money market will stagnate at its current size and will be unable to expand into the broader money and credit markets. There are two clear paths to bridge this gap, which are not competing with each other, but rather highly complementary and even symbiotic.

Path 1: P2P fixed-rate loans operated by risk management institutions

The P2P fixed-rate model is simple and straightforward: for each fixed-rate loan request, an equal amount of funds is locked up for a fixed-rate loan. While this model is simple and efficient, it requires a 1:1 liquidity match.

According to announcements from major lending platforms in 2026, they are all moving towards a P2P fixed-rate model. However, individual users will not borrow directly from these P2P fixed-rate markets, mainly for two reasons:

They value the flexibility of withdrawals.

They face too many markets that need to be evaluated and selected.

Conversely, only the liquidity currently deployed in the vaults of risk management firms can be borrowed into these fixed-rate markets—and even then, only partially. Risk management firms must maintain sufficient liquidity to meet the immediate withdrawal needs of their depositors.

This presents a tricky dynamic for risk management institutions that need to meet immediate withdrawal requirements:

When withdrawals surge and vault liquidity decreases due to funds being locked in fixed-rate lending, vaults lack mechanisms to discourage withdrawals or encourage deposits. Unlike money markets with utilization curves, vaults are not structurally designed to maintain withdrawal liquidity. Increased withdrawals do not necessarily lead to higher vault yields.

If the vault is forced to sell its fixed-rate loans on the secondary market, these loans are likely to trade at a discount—potentially leading to the vault's bankruptcy. (Similar to the situation at Silicon Valley Bank in March 2023.)

To mitigate this tricky dynamic, risk management firms tend to adopt the approach typically used by traditional lenders: converting fixed-rate loans into floating-rate loans through interest rate swaps.

They pay a fixed rate to the swap market and receive a corresponding floating rate, thus avoiding the risk of being locked into a low fixed rate when floating rates rise and withdrawals increase.

In this context, institutional lenders and risk management firms utilize interest rate markets to better provide fixed-rate liquidity.

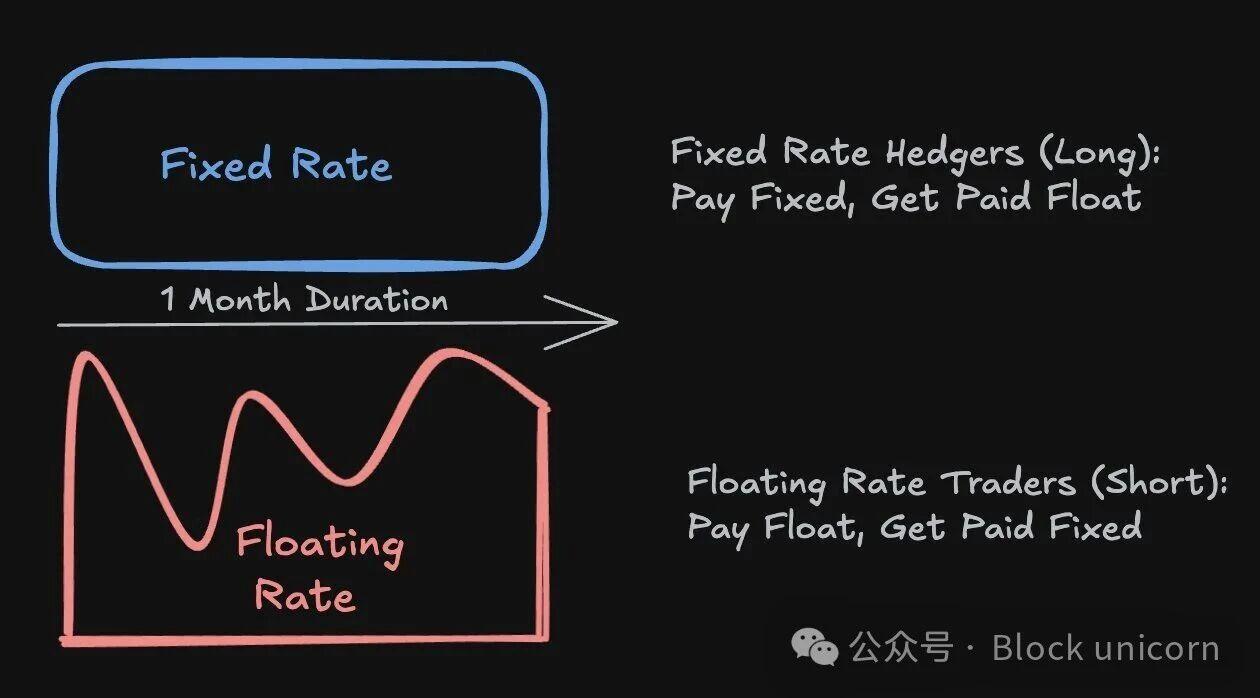

Path Two: Interest Rate Market Based on the Money Market

The interest rate market does not directly match fixed-rate lenders with borrowers. Instead, it matches borrowers with capital willing to bridge the gap between the agreed-upon fixed rate and the floating rate in the money market utilization curve. This approach provides capital efficiency 240-400 times higher than the 1:1 matching liquidity required by the P2P market.

The mathematical calculation of capital efficiency is as follows:

Borrow $100 million from Aave's existing liquidity at a floating rate.

The borrower wants to convert this floating-rate loan into a one-month fixed-rate loan. Assume the fixed rate is 5% per annum.

100 million * 5% / 12 = 416,000

Interest rate swaps can achieve an inherent leverage of 20 * 12 = 240 times.

Interest rate swaps help hedgers and traders price and swap fixed and floating interest rates.

Interest rate swaps based on the money market cannot provide completely unleveraged fixed-rate loans like the P2P model—if interest rates surge tenfold and remain high for an extended period, hedgers may theoretically face automatic deleveraging (ADL).

However, the likelihood of this happening is extremely low, and it has never occurred in the three-year history of either Aave or Morpho. Interest rate exchanges can never completely eliminate ADL risk, but they can employ multiple layers of protection—conservative margin requirements, insurance funds , and other safeguards—to reduce it to a negligible level.

This trade-off is extremely attractive: borrowers can obtain fixed-rate loans from tried-and-tested money markets with high TVL (total value loan-to-value ratio) (such as Aave, Morpho, Euler, and Kamino) while benefiting from capital efficiency that is 240-500 times higher than in the P2P market.

Path two is similar to how traditional finance operates—interest rate swaps have a daily trading volume of up to $18 trillion, boosting credit, fixed-income products, and real economic activity.

This strategy, which combines the security of a mature money market, $30 billion in liquidity from existing lending protocols, appropriate risk mitigation measures, and superior capital efficiency, makes interest rate exchanges a pragmatic choice for expanding fixed-rate lending on-chain.

An exciting future: Connecting markets, expanding credit

If you've patiently read through the previous section on dry mechanisms and market microstructures, hopefully this section will inspire your boundless imagination about the exciting development path ahead!

Some predictions:

1. The interest rate market will become as important as existing lending agreements.

Because lending primarily occurs off-chain, while borrowing mainly takes place on-chain, the market remains incomplete . Interest rate markets, by connecting lending and borrowing demands to satisfy the different preferences of both parties, significantly expand the potential of existing money market protocols and become an integral part of the on-chain money market.

In traditional financial transactions, interest rate markets and money markets are interdependent. We will see the same dynamics on-chain.

2. Institutional Credit: Interest Rate Markets Will Become a Pillar of Credit Expansion

Disclaimer: The credit mentioned here refers to uncollateralized or undercollateralized money markets, not overcollateralized modular markets such as the Morpho Blue market.

The credit market is even more dependent on the interest rate market than on over-collateralized lending. Predictable costs of capital are crucial when institutions finance real-world activities such as GPU clusters, acquisitions, or trading operations through credit. Therefore, the interest rate market will evolve alongside the expansion of on-chain private lending and risk-weighted assets (RWA).

In order to connect off-chain real-world yield opportunities with on-chain stablecoin capital, the interest rate market is a crucial pillar for the expansion of on-chain lending.

3. Consumer Credit: "Borrowing money to consume" benefits everyone.

Selling assets triggers capital gains tax and other tax issues, which is why ultra-high-net-worth individuals almost never sell assets; they choose to borrow to consume. I envision a near future where everyone will be able to "borrow to consume" rather than "sell to consume"—a privilege currently reserved for the super-rich.

Asset issuers, custodians, and exchanges will have a strong incentive to issue credit cards that allow people to borrow and spend directly using assets as collateral. For this system to function seamlessly with a fully self-custodied system, a decentralized interest rate market is essential.

EtherFi's credit cards spearheaded the trend of collateral-based consumer credit, with its credit card business growing by 525% last year and reaching a peak daily transaction volume of $1.2 million. If you haven't yet applied for an EtherFi card, I highly recommend giving it a try and experiencing the fun of "borrowing to spend"!

Finally, I want to point out that fixed interest rates are far from the only driver of money market growth. Money markets can solve many pressing problems, such as enabling off-chain collateral and RWA-based oracles to support circular strategies. The future is challenging, and I look forward to seeing this market develop and hope to contribute to it.