Now that this challenge has concluded, here's how to frame this challenge under the view that LP positions = options (& why LVR/edge benchmark is not what real traders worry about):

- You sell a straddle, hedging the delta after each spot price move. The edge benchmark is measuring the theta minus gamma-bleed.

The basic assumption from LVR is that you need to hedge after every trade, so the best performing hooks want to limit trades getting to the AMM to only those coming from benign/non-arbitrage flow.

But hedging after every trade is one extreme end of the spectrum. The other end is not hedging at all, and the "final" loss is IL when the position is closed:

|---------------------|

𝙻𝚅𝚁 𝙸𝙻

𝚑𝚎𝚍𝚐𝚎 𝚊𝚏𝚝𝚎𝚛 𝚍𝚘𝚗'𝚝

𝚎𝚟𝚎𝚛𝚢 𝚝𝚛𝚊𝚍𝚎 𝚑𝚎𝚍𝚐𝚎

Most funds would never hedge after every trade, not even Citadel or other HFT firms doing cross-arbitrage between very similar products like SPX, SPY, and /ES.

So constraining the solution space to everytrade/LVR misses how real funds handle risk.

Somewhere between LVR and IL is where most funds need to manage risk, leading to more elegant mechanism designs for better AMMs:

- hedge at fixed time intervals (markouts)

- hedge at fixed delta (reverse gamma scalping)

- hedge before every trade (propAMMs)

- hedge with TradFi vs. perpetual options

- hedging dynamics when LPs are arbitrageurs, arbitrageurs are LPs

Dan Robinson

@danrobinson

02-07

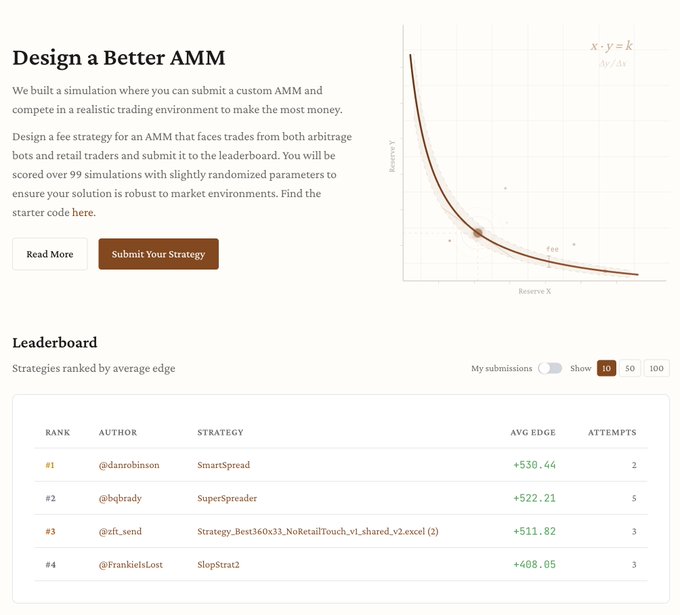

Are you a better AMM designer than me?

@bqbrady and I built a challenge that lets you prove it

Create your own dynamic-fee AMM and submit it to get onto our leaderboard

Link in 🧵👇

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content