Author: Momir@momir_amidzic, Managing Partner at IOSG Ventures

The altcoin market has endured one of its most difficult years, and understanding why requires looking back at decisions made years ago. The 2021–2022 funding bubble created a cohort of projects that raised significant capital, and these projects are in their token issuance cycle. This creates a fundamental problem: massive supply hitting the market with virtually no corresponding demand.

The root issue isn’t just oversupply — it’s that little has changed since the mechanisms that created this problem first emerged. Projects continue to launch tokens regardless of product-market fit, treating token issuance as an inevitable milestone rather than a strategic decision. As VC capital dried up and primary round investments declined, many teams turned to token launches as their only path to capital or liquidity events for insiders.

This article diagnoses the four-way loss dynamic destroying the altcoin market, examines failed attempts to fix it, and proposes what equilibrium could look like.

The Low Float Problem: A Lose-Lose-Lose-Lose Game

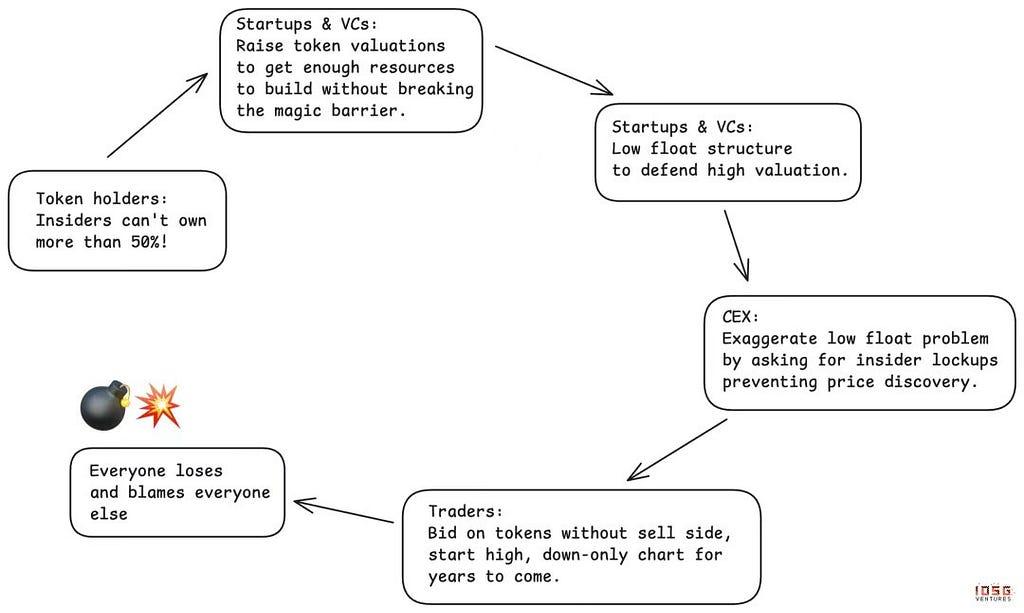

For the past three years, the industry has relied on a deeply flawed mechanism: low float token launches. Projects issue tokens with extremely low circulation — often in the low single-digit percentages — to artificially defend high fully diluted valuations. The logic seems sound at first: less supply means better price stability.

But low float tokens don’t stay low float forever. As more supply inevitably hits the market, prices collapse. Early adopters get punished for their loyalty, and the data confirms this across the board — most tokens have performed poorly since launch.

What makes this particularly insidious is that low float creates a situation where everyone thinks they’re winning, but everyone actually loses:

Centralized Exchanges think they’re protecting retail investors by demanding lower float and more control. Instead, they end up with angry communities and poor price performance.

Token Holders think they’re protected from insider dumping by keeping circulation low. Instead, they never see proper price discovery, and they get punished for being early supporters. When they demand that insiders can’t hold more than 50% of supply, they push valuations in the primary market beyond reasonable levels, which forces insiders to defend those valuations with — you guessed it — low float strategies.

Teams think low float manipulation lets them justify high valuations and minimal dilution. In aggregate, this approach destroys capital access for the entire industry if the trend continues.

VCs think they can mark-to-market their low float token positions and raise more capital. Instead, they lose access to capital in the medium/long term as the strategy’s flaws become obvious.

It’s a perfect lose-lose-lose-lose matrix. Everyone thinks they’re playing smart, but the game itself is rigged against all participants.

Market Reactions: Meme Coins and MetaDAO

The market has attempted to solve this problem twice, and both attempts reveal something important about the complexity of token design.

First Iteration: The Meme Coin Experiment

Meme coins emerged as a reaction to VC-backed low float launches. The pitch was simple and appealing: 100% circulating supply on day one, no VCs, complete fairness. Finally, the game wouldn’t be rigged against retail investors.

The reality was far darker. Without any filtering mechanism, the market got flooded with unvetted token launches. Solo, often anonymous, operators replaced VC-backed teams, and rather than creating fairness, this created an environment where 98%+ of participants lost money. Tokens became rug-pull vehicles, with holders getting wiped out within minutes or hours of launch.

Centralized exchanges found themselves in an impossible position. If they didn’t list meme coins, users would go on-chain without them. If they did list them, they’d be blamed when prices inevitably collapsed. Token holders suffered the most catastrophic losses. The only winners were the teams behind launches and platforms like Pump.fun who extracted significant value.

Second Iteration: The MetaDAO Approach

MetaDAO represents the market’s second major attempt at a solution, swinging the pendulum in the opposite direction by heavily favoring token holder protection.

The benefits are real:

- Token holders gain control levers that make deployment of capital more attractive

- Insiders can only achieve liquidity by hitting specific KPIs

- New funding mechanisms open up in an environment where capital is scarce

- Starting valuations are comparatively low, offering fairer access

But MetaDAO creates new problems by overcorrecting:

Founders lose too much control too early. This creates a “founder lemon market” where resourceful teams with options avoid the model, while desperate teams with no alternatives embrace it.

Tokens still launch at extremely early stages with high volatility, but now with even less filtering than the VC cycle provided.

Infinite mint functions make tier-one exchange listings nearly impossible. MetaDAO is fundamentally misaligned with centralized exchanges that control the vast majority of liquidity. Without CEX listings, tokens remain trapped in illiquid markets.

Each iteration has attempted to solve problems for one group of stakeholders, and each demonstrated the market’s capacity for self-regulation. But we’re still searching for a balanced solution that addresses the interests of all key participants: exchanges, token holders, teams, and capital providers.

The evolution is ongoing, and we won’t have a sustainable model until we find equilibrium. That equilibrium must satisfy all stakeholders — not by giving everyone everything they want, but by establishing clear boundaries between harmful practices and legitimate rights.

What Equilibrium Looks Like

Centralized Exchanges

Must stop: Demanding excessively long lockups that prevent proper price discovery. These extended lockups create the illusion of protection while actually harming the market’s ability to find fair value.

Are entitled to: Predictability around token supply schedules and meaningful accountability mechanisms. The focus should shift from arbitrary time-based locks to KPI-based unlocks with shorter, more frequent vesting schedules tied to demonstrable progress.

Token Holders

Must stop: Overcompensating for historical lack of rights by demanding excessive control that drives away the best talent, exchanges, and VCs. Not all insiders are the same — demanding identical long lockups for all ignores the different roles and prevents proper price discovery. The obsession with magical ownership thresholds (“insiders can’t own more than 50%”) creates the exact conditions that led to low float manipulation.

Are entitled to: Strong information rights and operational transparency. Token holders deserve clear visibility into the business underlying their tokens, regular reporting on progress and challenges, and honest communication about runway and resource allocation. They’re entitled to guarantees that value won’t leak out through side deals or alternative structures — tokens should be the primary IP holder, ensuring that value created accrues to token holders. Finally, token holders should have reasonable control over budget allocation, particularly for significant expenditures, while not micromanaging daily operations.

Teams

Must stop: Issuing tokens without clear product-market fit signals or compelling token utility. Too many teams launch tokens as glorified equity with inferior rights — a junior tranche to venture equity without the legal protections. Tokens shouldn’t be issued just because “it’s what crypto projects do” or because the runway is running low.

Are entitled to: The ability to make strategic decisions, take bold bets, and run operations without subjecting every decision to DAO approval. If teams are accountable for outcomes, they need the authority to execute.

Venture Capital Firms

Must stop: Pressuring every portfolio company to launch a token regardless of whether it makes sense. Not every crypto company needs a token, and forcing token launches to mark positions or create liquidity events has flooded the market with low-quality issuances. VCs need to be more selective and honest about which companies genuinely benefit from token models.

Are entitled to: Fair compensation for the extreme risk they’re taking by backing early-stage crypto projects. High-risk capital deserves high-risk returns when bets pay off. This means reasonable ownership percentages, fair vesting schedules that reflect their contribution and capital at risk, and the ability to achieve liquidity for successful investments without being demonized.

Even with a path to equilibrium, timing matters. The near-term outlook remains challenging.

The Next 12 Months: The Final Wave of Oversupply

The next 12 months likely represents the final wave of oversupply from the last VC hype cycle.

After this absorption period, conditions should improve:

- By the end of 2026, the last cycle cohort will have either launched tokens or gone bankrupt

- Capital access remains expensive, constraining new project formation. The pipeline of VC-backed projects seeking token issuance is significantly smaller

- Primary market valuations have returned to more reasonable levels, reducing the pressure to artificially defend high valuations with low floats

What we did three years ago determines how the market looks today. What we’re doing today will determine the market two to three years from now.

Beyond the supply cycle lies a deeper threat to the entire token model.

The Existential Risk: The Lemon Market

The greatest long-term threat is that altcoins become a “lemon market” — a market which rejects the quality participants and invites those who don’t have an alternative.

Here’s how it could happen:

Unsuccessful projects continue issuing tokens to access liquidity or extend their runway, even when they have no signal of product-market fit. As long as there’s an expectation that projects should issue tokens regardless of success, failed projects will flood the market.

Successful projects observe the carnage and opt out. When strong teams look at aggregate token performance and see consistent underperformance, they might choose traditional equity structures instead. Why subject yourself to token market dysfunction when you can build a successful equity company? Many projects have no compelling reason to issue a token, tokens are becoming more optional than mandatory for a majority of application layer projects.

If this dynamic continues, the token market becomes dominated by projects that couldn’t succeed through other means — the “lemons” that no one wants.

Despite these risks, there are compelling reasons for optimism.

Why Tokens Can Still Win

Despite these challenges, I remain optimistic that the worst-case lemon market scenario won’t materialize. Tokens offer unique game-theoretic mechanisms that simply cannot be replicated with equity structures.

Accelerated growth through ownership distribution. Tokens enable laser-focused distribution strategies and growth loops impossible with traditional equity. Ethena demonstrated this by using token-enabled mechanics to bootstrap rapid adoption and create sustainable protocol economics.

Passionate, loyal communities that create moats. When done right, tokens create communities with skin in the game — participants who become sticky, loyal advocates for the ecosystem. Hyperliquid exemplifies this: their community of traders became deeply invested participants, creating network effects and loyalty that would be impossible to replicate without token.

Tokens can make growth dramatically faster than equity models while simultaneously enabling huge design space for game theory, which when done right can unlock great opportunities. When these mechanisms work, they’re genuinely transformative.

Signs of Self-Correction

Despite the challenges, there are encouraging signs that markets are adapting:

Tier-one exchanges are becoming dramatically more selective. Issuance and listing requirements have tightened considerably. Exchanges are implementing better quality control and providing more rigorous evaluation before listing new tokens.

Investor protection mechanisms are evolving. MetaDAO’s innovations, DAO-owned IP rights (as seen in Uniswap and Aave governance disputes), and other governance innovations show the community actively experimenting with better structures.

The market is learning, slowly and painfully, but learning nonetheless.

Recognition That We’re in a Cycle

Crypto markets are highly cyclical, and we’re currently in the trough. We’re absorbing the negative consequences of the 2021–2022 VC bull run, the hype cycle, the over-investment, and the misaligned structures that followed.

But cycles turn. In 2 years, once the 2021–2022 cohort has fully absorbed, once new token supply has declined due to current capital constraints, once better standards have emerged through trial and error — market dynamics should improve substantially.

The critical question is whether successful projects will return to token models or permanently shift to equity structures. The answer depends on whether the industry can solve the alignment and filtering problems.

The Path Forward

The altcoin market stands at a crossroads. The 4L dynamic — where exchanges, token holders, teams, and VCs all lose — has created unsustainable market conditions. But this is not permanent.

The next 12 months will be painful as the final wave of 2021–2022 supply hits the market. But beyond that absorption period, three things could drive recovery: better standards emerging from painful trial and error, alignment mechanisms that satisfy all four stakeholder groups, and selective token launches where teams only issue tokens when they genuinely add value.

The answer depends on choices being made today. Three years from now, we’ll look back at 2026 the same way we’re looking back at 2021–2022 today. What are we building?

Why Altcoins Are a Lose-Lose-Lose-Lose Game and How to Fix It was originally published in IOSG Ventures on Medium, where people are continuing the conversation by highlighting and responding to this story.