Crypto assets have been fully integrated into the global macroeconomic financial cycle. They are no longer “independent narrative assets” that are detached from the mainstream, but rather high-beta risk assets that are driven by oil prices, inflation expectations, interest rate paths, and volatility.

Article author and source: TechFlow TechFlow

TL;DR

Background: Escalating geopolitical risks have made the crypto market a high-beta risk asset deeply embedded in the global macroeconomic cycle.

Quantitative Framework: The GPR index can be broken down into "threats" and "actions," with negative effects primarily driven by "threats."

Transmission Mechanism: Risk Appetite Shift | Inflation and Interest Rate Cut Concerns | Market Structure Amplification

Causes of high beta: Enhanced correlation of risky assets + forced liquidation due to high leverage + contraction of endogenous liquidity

Outlook: Baseline scenario: consolidation and correction | Pessimistic scenario: double bottom | Optimistic scenario: high volatility and excess rebound

Implications: Investors need to incorporate geopolitical risks into a unified macroeconomic framework and dynamically assess their impact on risk premiums and liquidity.

I. Overview of Geopolitical Risks

- What do geopolitical risks mean?

Geopolitical risks are often perceived as "the shock of a breaking news event." But a more accurate understanding is that it is a collection of events and expectations—escalation of war or conflict, terrorist attacks, sanctions and counter-sanctions, diplomatic confrontation, disruption of key shipping routes, trade frictions and tariff escalations, etc., all of which contribute to increased uncertainty about the future.

The key to geopolitical risk lies not in the events themselves, but in the market's repricing of the probability of future paths. In other words, the GPR (Gross National Rate) is a "macroeconomic risk premium generator." It doesn't necessarily erupt every day, but whenever it rises, the market responds with a higher discount, a stricter risk appetite, and tighter funding constraints.

- How can geopolitical risks be quantified?

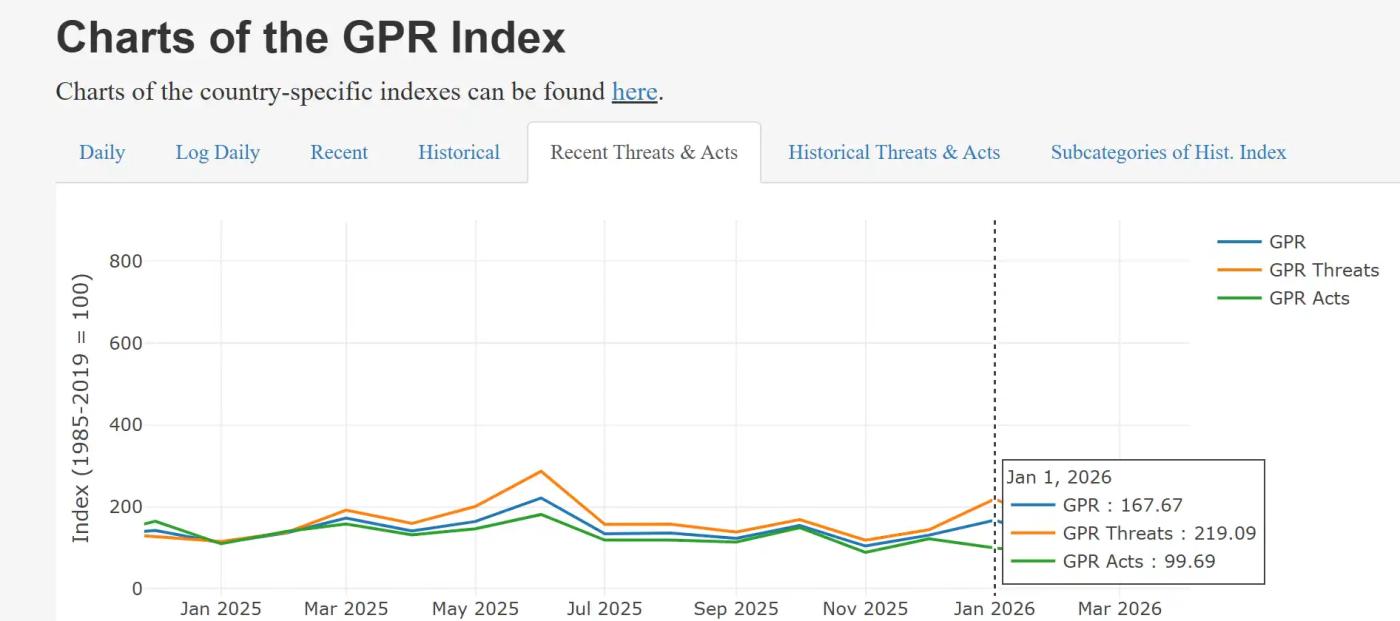

The Geopolitical Risk Index (GPR Index), compiled by U.S. Federal Reserve economists Dario Caldara and Matteo Iacoviello, tracks the proportion of negative geopolitical events or threats discussed in international newspapers and magazines since 1900, with data sourced from the top 10 international newspapers.

The geopolitical risk index is an indicator that measures changes in global geopolitical risk. It is typically used to assess the potential impact of factors such as political instability, conflict, war, and policy changes on the economy and markets of a country or region. More importantly, this system breaks down risk into two more "transactional" components:

- Threats: The stage where risks are brewing but have not yet materialized—a period marked by a dense appearance of terms such as threats, warnings, concerns, risks, and tensions. When threats rise, the market often trades on "possibility" (expectations) first, manifested by rising fear indicators, a stronger gold/dollar exchange rate, and the emergence of a risk premium in oil prices;

- Actions: Risks have occurred or escalated—the proportion of "factual" reports such as the start of war, escalation of conflict, and carrying out of terrorist attacks increases. At this point, the market begins to trade "real shocks" (supply and demand/policy/growth), which tend to be more volatile and more likely to trigger cross-asset chain reactions.

According to data from the MacroMicro platform, the global geopolitical risk "threat" index rose significantly in January 2026, reaching a reading of 219.09. When the GPR (Gross National Rate) rises, the market's first reaction is often to reduce risk exposure before considering whether to buy the dips. This will manifest as increased volatility (a rise in the VIX), a pullback in risky assets, and a greater preference for safe-haven assets and cash-like assets.

Source: https://www.matteoiacoviello.com/gpr.htm

II. The Impact and Transmission of Geopolitical Risks

The rise in geopolitical risk (GPR) does not directly cause volatility in the crypto market. Instead, it first increases macroeconomic uncertainty, which is then transmitted through multiple channels, ultimately resulting in sharp, homogeneous fluctuations in the crypto market. This is an inevitable consequence of the transmission of macroeconomic pressures and their amplification through market structure.

The rise in GPR mainly plays a role through the following four mechanisms: (1) Risk appetite shift: VIX rises, credit spreads widen, and risk assets are reduced in general; (2) Energy and commodity shocks: Gold and oil prices rise, and inflation expectations rise; (3) Policy and liquidity repricing: interest rate cut expectations are delayed, the US dollar strengthens, and long-term interest rates rebound; (4) Market structure expansion: liquidity is thin over the weekend, high leverage derivatives, and forced liquidation waterfall.

The combined effect of these mechanisms has led to more pronounced co-current fluctuations in the crypto market than in the stock market.

- Risk preference switching

Escalating geopolitical conflicts first trigger risk aversion. This leads to increased risk aversion in the stock market, a rise in the volatility index VIX, and a withdrawal of funds from high-volatility assets into traditional safe-haven assets.

The VIX (Chicago Board Options Exchange Volatility Index) is a core indicator measuring the expected volatility of US stocks over the next 30 days. Calculated using S&P 500 index option prices, it reflects implied market volatility rather than historical actual volatility. Because it spikes significantly during market downturns, it's known as the "fear index." Its value range directly reflects market sentiment: below 20 indicates stable optimism; 20-30 indicates caution; above 30 indicates high fear; and above 40 indicates extreme fear (often seen during major crises).

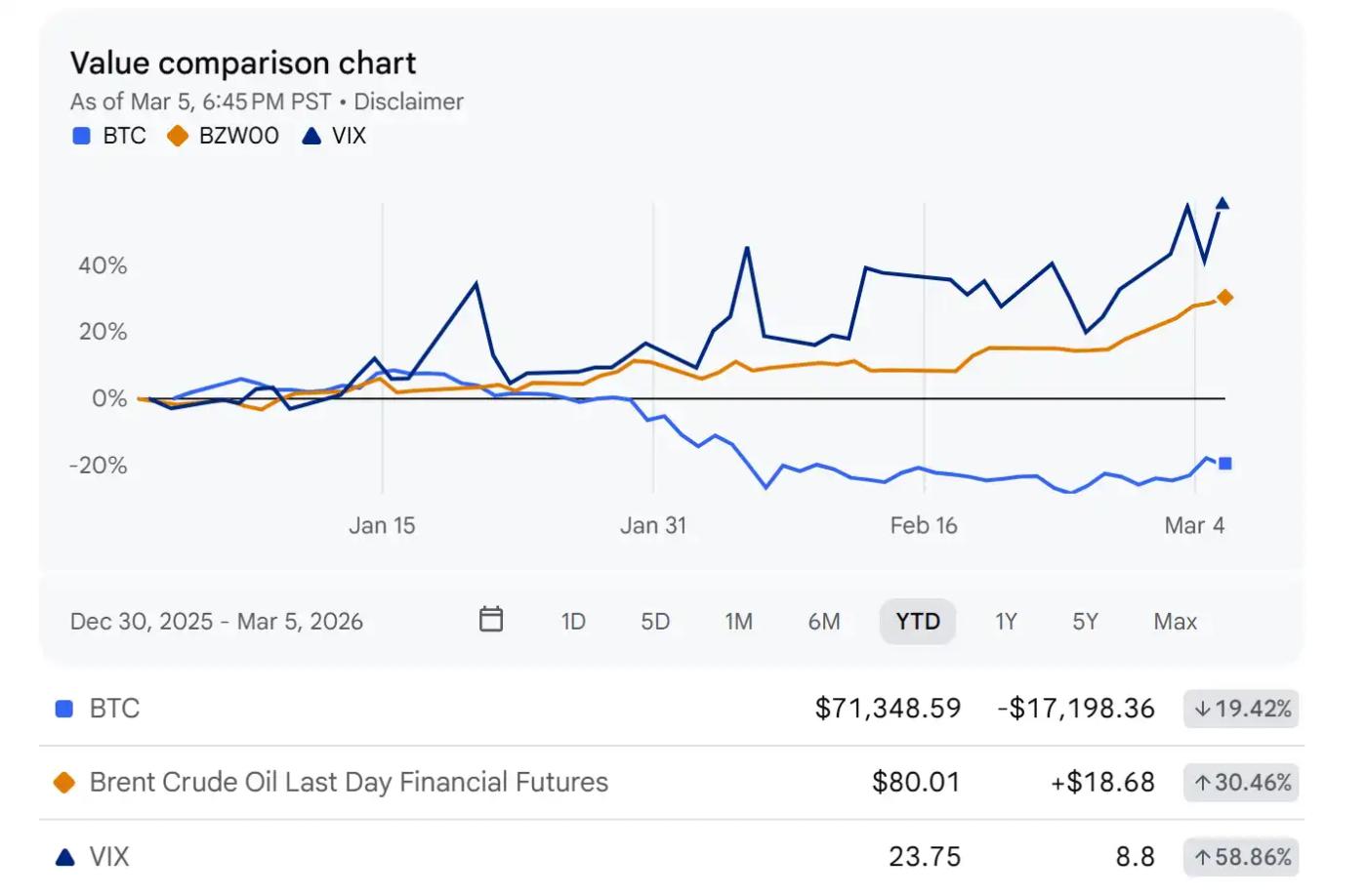

In March 2026, the VIX index had risen rapidly from around 14.50 at the beginning of the year to above 20, reflecting market panic over military conflicts and disruptions to energy supply chains. Gold, as a classic safe-haven asset, typically exhibits strong buying interest in the early stages of geopolitical crises. Research by the World Gold Council shows that for every 100-point increase in the GPR index, the price of gold rises by an average of about 2.5%. Spot gold is highly positively correlated with the GPR index, and its safe-haven value even surpasses that of traditional currencies, especially during periods of sovereign credit risk or escalating tensions.

- Concerns about inflation and interest rate cuts

Escalating geopolitical conflicts in the Middle East and elsewhere often first impact oil prices and shipping expectations, fueling inflation concerns and forcing the market to lower its expectations for interest rate cuts, thus putting sustained pressure on highly valued and volatile assets.

The core driver of oil price fluctuations is the risk of supply disruptions, not simply sentiment. The security of key shipping lanes like the Strait of Hormuz directly determines the level of the "geopolitical premium." Prolonged conflict will bring persistent inflationary pressures. While gold primarily reflects safe-haven demand due to uncertainty in the financial system, oil prices directly reflect the impact of conflict on the supply and inflation of the real economy. As soon as the market begins to worry about supply chains, sanctions, and counter-sanctions, oil prices will be repriced.

Brent crude oil has recently surged, with a monthly increase of over 20%. When geopolitical risks escalate, energy price shocks and increased volatility often occur simultaneously, driving a shift in risk appetite and a repricing of liquidity. Rising oil prices reinforce concerns about sticky inflation, directly weakening the certainty of interest rate cuts. When market expectations shift from "easing is on the way" to "higher and longer interest rates," crypto assets, as highly volatile and high-expectation assets, are often the first to come under pressure, especially during periods of low liquidity.

Since the beginning of 2026, crude oil and the VIX have shown a high positive correlation, and their simultaneous rise indicates that soaring energy prices are directly driving market panic. Meanwhile, the price of Bitcoin (BTC), considered "digital gold," shows a clear negative correlation with the VIX; the greater the market panic, the greater the selling pressure on Bitcoin. The underlying reason is that rising crude oil prices have reinforced expectations of high interest rates, which has a double impact on high-risk assets (Bitcoin) and the stock market (reflected in the VIX).

- Crypto market structure characteristics

After macroeconomic pressures are transmitted to the crypto market through the first three pathways, the market's own structural problems will further amplify the impact. The structural characteristics of the crypto market mean that it tends to experience more severe volatility than traditional risky assets during risk events.

- 24/7 trading: making weekends the time when macroeconomic shocks are most easily amplified: traditional markets are closed, hedging tools are reduced, and market depth is shallower;

- Derivatives and high leverage account for a large proportion: price declines can easily trigger margin calls and forced liquidation, forming a "passive selling" waterfall;

- The liquidity stratification is obvious: the uneven liquidity stratification is reflected in different aspects such as large exchanges vs. small exchanges, spot trading vs. perpetual trading, mainstream coins vs. Altcoin. When risk appetite contracts, liquidity quickly concentrates in the top, while the decline of tail assets is more extreme.

These mechanisms determine that the "high beta" characteristic of the crypto market is determined by mechanisms, rather than simply by emotions.

It's worth noting that when conflicts are compounded by sanctions, capital controls, or restrictions on the banking system, cryptocurrencies, due to their cross-border transfer and alternative settlement attributes, may become a localized safe-haven tool, providing buying support. The early stages of the Russia-Ukraine war saw active fiat currency trading and a significant increase in related demand. While this path can provide short-term support, it typically struggles to reverse a downward trend driven by macroeconomic risk appetite, unless accompanied by a stronger narrative such as prolonged inflation or a sovereign debt crisis.

The chart below, created using Yahoo Finance, shows the 6-month trend. The blue-filled area represents the CBOE Volatility Index (VIX), overlaid with the performance of Brent crude oil futures, gold, and Bitcoin during the same period. Entering 2026, with the continued escalation of geopolitical risks, the VIX index rose significantly, closing at 23.75 on March 6, 2026. Brent crude oil also rebounded strongly; gold, as a safe-haven asset, rose significantly; while Bitcoin experienced a sharp correction. This chart clearly illustrates that geopolitical risks are transmitted through a dual path of "a surge in VIX + a sharp rise in energy prices," on the one hand pushing up market volatility and inflation expectations, and on the other hand causing significant pressure on high-beta risk assets such as cryptocurrencies.

Source: https://finance.yahoo.com/

III. Reasons for the High Beta of Crypto Assets

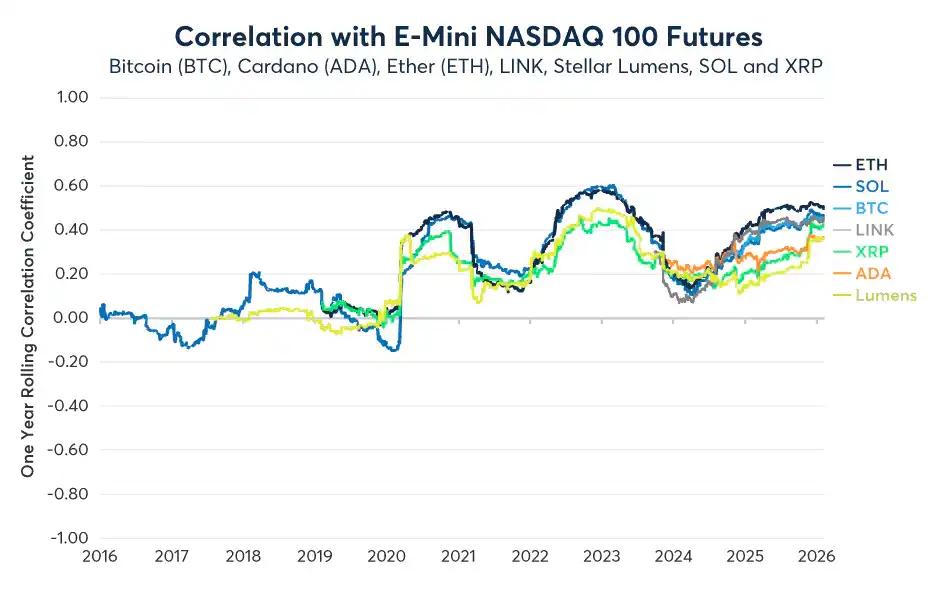

Many people simplify BTC to "digital gold," but in most macroeconomic phases, it's more like a "high-volatility version of the Nasdaq." This is mainly due to its three-layered structure: its correlation with risk asset pricing, the fact that price discovery occurs more frequently in derivatives, and the "endogenous liquidity cycle" formed by stablecoins and exchange margins.

- Risk asset correlation

A study by CME Group indicates that the correlation between crypto assets and the Nasdaq 100 has been consistently positive since 2020, and that during certain periods in 2025 and early 2026, the rolling correlation could reach approximately +0.35 to +0.6 (clearly a phase, not constant).

Source: https://www.cmegroup.com/insights/economic-research/

This means that once a macroeconomic shock triggers a "simultaneous reduction in risk assets" (escalation of war, rising oil prices, and delayed expectations of interest rate cuts), BTC will find it difficult to remain unaffected and will often fall even faster. This is the first layer of "high beta".

- High leverage amplifies volatility

The dramatic ups and downs in the crypto market are often not due to drastic changes in fundamentals within 24 hours, but rather to the accelerated deleveraging of the funding rate-margin-liquidation chain.

In the "1011" crash in 2025, more than $19 billion in leveraged positions were liquidated within 24 hours, setting a record for the largest single-day liquidation in crypto history. At the same time, the open interest in perpetual contracts shrank significantly, indicating that the "liquidation waterfall" would push the already fragile market into non-linear fluctuations.

- Endogenous liquidity mechanism

When expectations of macroeconomic tightening intensify, stablecoin funds become more cautious, and lending and margin requirements tighten simultaneously, leading to a "self-draining" effect in the market: reduced available margin → passive liquidation → price decline → reduced collateral value → further passive liquidation.

It is evident that the crypto market does not rely primarily on central bank "easing/reducing" of liquidity like traditional markets. Instead, it is more like a system that automatically contracts liquidity under pressure, making it more prone to sharp drops and rebounds.

So, does the "digital gold" concept still hold true? The historical peak of the rolling correlation between BTC and gold is limited, and it has fallen to near zero since 2024. Therefore, a more accurate framework is: under short-term shocks, BTC is more like a high-beta risk asset; in the medium to long term, under structural scenarios such as capital controls, cross-border frictions, and sovereign credit concerns, BTC is more likely to demonstrate its narrative advantage of being "transferable across borders and not diluted."

IV. Outlook for Future Trends

The impact of geopolitics on crypto is not essentially about whether "war will benefit Bitcoin," but rather how risk appetite and liquidity conditions will change. While Middle East risks remain uncertain, we will use a three-scenario framework to project possible paths, key triggers, and corresponding price movements.

- Baseline Scenario: Oscillation Recovery

Assuming the conflict remains under control and there are no long-term disruptions to key shipping and energy supplies, oil prices will fluctuate at high levels but will no longer surge. Market concerns about a second wave of inflation will ease, the VIX will gradually decline, and expectations for interest rate cuts will "slowly recover" after data confirmation.

In this environment, crypto assets, being high-beta assets, are unlikely to immediately break out of a one-sided trend. They are more likely to experience a "range-bound oscillation + slow rise" recovery: the downside is supported by the decline in risk premiums and buying on dips, while the upside is constrained by the still cautious macro environment and the time required for leverage recovery.

- Pessimistic scenario: Double dip

If the conflict spills over to a wider area, resulting in substantial supply disruptions or a prolonged increase in shipping costs, the continued surge in oil prices could lead to renewed inflation, forcing the market to further postpone interest rate cuts or even recalculate a higher real interest rate path, leading to an overall downward revision of risk asset valuations.

At this point, the triple amplifier of encryption will be superimposed: falling along with risky assets + deleveraging of derivatives + contraction of endogenous liquidity (margin/lending tightens simultaneously), making it more likely to form a structure of "accelerated decline - weak rebound - further breakdown", that is, the so-called double bottom.

- Optimistic Scenario: High Volatility and Excessive Rebound

If the risk events subside quickly, oil prices fall, the VIX declines, and the macroeconomy releases clearer easing signals, the market will regain confidence in the interest rate cut path, and risk appetite will recover rapidly.

Cryptocurrencies often experience more resilient outperformance during these phases: capital inflows combined with short covering and reopening of leverage can lead to a rapid price surge. However, caution is advised: the structural characteristics of cryptocurrencies mean they often "rise quickly but also fall quickly," making them prone to sharp pullbacks when sentiment is overheated.

V. Lessons Learned and Conclusion

Crypto assets have been fully integrated into the global macroeconomic financial cycle. They are no longer “independent narrative assets” that are detached from the mainstream, but rather high-beta risk assets that are driven by oil prices, inflation expectations, interest rate paths, and volatility.

Three points of inspiration

Lesson 1: The real destructive power of geopolitical risks lies in the pre-pricing of risk premiums by the "threat".

After breaking down risk into "threats" and "actions," the GPR index shows that negative effects are mainly driven by the former. This means that the market often completes repricing before the conflict escalates, through VIX spikes, oil price premiums, and delayed interest rate cut expectations, demonstrating that "expectations are reality."

Lesson 2: The high beta characteristic of the crypto market is an inevitable result of the combined effects of macroeconomic transmission and market structure.

Risk appetite shifts, concerns about inflation and interest rate cuts, and the repricing of policy liquidity, coupled with the mutually reinforcing mechanisms of 24/7 trading, forced liquidation of high leverage, and contraction of endogenous liquidity, have made crypto assets significantly more volatile than traditional markets under similar macroeconomic shocks. This is not driven by sentiment, but by mechanisms.

Lesson 3: The macro-level impact of Bitcoin has become an irreversible structural trend.

Bitcoin and US stocks have shifted to a long-term positive correlation, indicating that Bitcoin is increasingly being traded as a risk-averse asset. In the short term, it resembles a "high-volatility version of the Nasdaq"; in the medium to long term, its "digital gold" attributes will only truly emerge under scenarios involving capital controls, sovereign credit crises, or escalating cross-border frictions.

Conclusion

In the current environment of high interest rates and geopolitical conflicts, Bitcoin's "digital gold" attribute is temporarily dominated by its high-beta risk. Investors who understand the transmission mechanism of geopolitical risks will shift from passively enduring volatility to actively seizing opportunities. Only by transforming geopolitical uncertainty into quantifiable risk premiums and liquidity signals, and dynamically assessing their impact on asset allocation, can rational decisions be made in complex situations. The long-term value of the crypto market has never lay in avoiding macroeconomic cycles, but in deeply understanding and utilizing them.

about Us

Hotcoin Research, as the core research arm of the Hotcoin exchange, is dedicated to transforming professional analysis into practical tools for your investment decisions. We analyze market trends through our "Weekly Insights" and "In-Depth Research Reports"; and with our exclusive column "Hotcoin Selection" (AI + expert dual screening), we help you identify potential assets and reduce trial-and-error costs. Every week, our researchers also host live streams to discuss hot topics and predict trends. We believe that warm support and professional guidance can help more investors navigate market cycles and seize the value opportunities of Web3.