Introduction: A Silent "Heart Transplant" of the Financial System

In late 2025 and early 2026, the global financial market did not witness a wave of bank failures as dramatic as in 2008, but a more profound and far-reaching transformation was quietly taking place. This is not a simple crisis repair, but a complete reconstruction of the "operating system." As revealed in the video "When 'Old Money' Starts Playing DeFi: How Does BlackRock Enter the $68 Trillion On-Chain Market?" released by Silicon Valley 101, the cornerstone of the global financial system—assets themselves—is being "tokenized" at an unprecedented speed, migrating from the physical world and traditional electronic ledgers to the blockchain. The core driving force of this transformation does not come from the original disruptors of the crypto world, but from the heart of Wall Street—the "old money" giants led by BlackRock, the world's largest asset management company.

The core argument is thought-provoking: We are at a historic turning point comparable to the dawn of the internet in 1996. Back then, most people's understanding of the internet was limited to a tool for sending and receiving emails; no one could have foreseen how it would completely revolutionize every aspect of business, social interaction, and life. Today, asset tokenization plays the same role. It's not merely about issuing a new "digital collectible" or cryptocurrency, but about transforming the real-world assets (RWAs) that make up the lifeblood of the global economy—such as stocks, bonds, real estate, private equity, and infrastructure—into programmable, composable digital tokens that can circulate frictionlessly 24/7 on the blockchain. This heralds the activation of a massive $68 trillion market, and every move BlackRock makes attempts to define the rules and order of this emerging on-chain universe.

This article will use the video content as its core framework, combined with BlackRock CEO Larry Fink's annual letter to shareholders, the official announcement from the Depository Trust & Clearing Corporation (DTCC), the strategic plans of key industry players such as Binance, and relevant in-depth research reports, to write an in-depth analysis. It will not only summarize the video's viewpoints, but also delve into the driving forces, technological logic, market landscape, and future challenges behind them, striving to present a panoramic view of this grand revolution led by "old money" and aimed at reshaping the global capital market for the next decade.

Chapter 1: The Trigger of History — The DTCC Opens the Floodgates, 68 Trillion Yuan in Assets Flows into the Chain

To understand the disruptive nature of this change, we must first recognize the source of its "legitimacy." The "first shot" of this revolution was not fired in a decentralized community, but rather in the boardroom of the most central and conservative institution in the global financial system—the Depository Trust & Clearing Corporation (DTCC).

1.1 DTCC: The "Hidden Heart" of Global Financial Markets

For ordinary investors, DTCC is an unfamiliar name. However, it is the "invisible heart" supporting the vast majority of global financial transactions. As the largest financial market infrastructure provider in the US and even globally, DTCC and its subsidiaries (such as DTC) provide clearing, settlement, and custody services for massive amounts of assets, including stocks, corporate bonds, government bonds, and money market instruments. According to its official website, DTCC processed securities transactions worth over $2.5 trillion in 2024, and its total assets under custody approached $100 trillion. It can be said that DTCC is behind every single US stock transaction. Its stability and efficiency directly determine the lifeline of the global financial system.

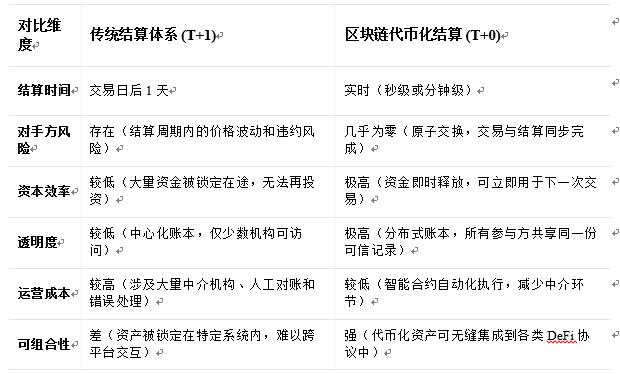

However, the heart of this vast system hasn't fundamentally changed in the past half-century. It still relies on a settlement cycle known as "T+2" or "T+1" (two days or one day after the trading day). This means that when you sell stocks, the funds don't arrive immediately but circulate through a complex clearing network for one to two days. This time lag not only ties up massive amounts of capital and reduces capital efficiency but also hides enormous settlement risks during periods of market volatility—counterparties may default before settlement is complete, triggering a chain reaction. The "Paperwork Crisis" following the 1929 Wall Street crash was an extreme example, with piles of paper stock certificates unable to be processed in time, paralyzing the entire market. Although digitization was later implemented, the underlying step-by-step, non-real-time settlement logic remains unchanged.

1.2 The SEC's "Birth Certificate": The Historical Significance of a "Letter of No Action"

The key event repeatedly emphasized in the video occurred on December 11, 2025. On this day, the U.S. Securities and Exchange Commission (SEC) issued a crucial "No-Action Letter" to DTCC's subsidiary, DTC[1]. This seemingly mundane legal document actually cleared the biggest regulatory hurdle for DTCC to launch its real asset tokenization service, granting it a "birth certificate" to enter the on-chain era.

A "no-action letter" means that SEC staff have assured the DTC that if the DTC carries out its tokenization services according to its submitted proposal, the SEC will not recommend that the Commission take enforcement action against it. This provides the DTC with a valuable "safe harbor" for exploring and deploying blockchain-based asset tokenization in a regulated and risk-controlled environment.

According to a subsequent announcement by DTCC, its tokenization service is expected to officially launch in the second half of 2026. The initial pilot will cover some eligible securities held in custody by DTCC, such as Russell 1000 index constituents and U.S. Treasury bonds. This means that investors holding Apple stock or U.S. 10-year Treasury bonds could, in the future, be represented as a digital token issued on mainstream public blockchains such as Ethereum. This token will have the same legal rights and protections as the original asset, but its trading, settlement, and usage will be drastically different.

1.3 From the “Paper Crisis” to the “Quantum Leap”: A Century of Evolution and the Final Chapter of Settlement Efficiency

To truly understand the revolutionary nature of DTCC's move, we need to look back at Wall Street in the late 1960s. At that time, due to a surge in trading volume, manually processed paper stock certificates piled up, leading to the infamous "Paperwork Crisis." Brokerages were overwhelmed, transaction failure rates soared, and the entire market teetered on the brink of collapse. This crisis directly spurred the establishment of the DTC and the centralization and electronicization of securities custody, gradually shortening the settlement cycle from T+5 (5 days after the transaction). However, even in the T+1 era, the core logic remained "net settlement" rather than "real-time full settlement," and the risks were not eradicated.

The inherent drawbacks of T+1:

• Credit risk and market risk exposure: In the day between transaction execution and final settlement, the counterparty may still default, or the market price may fluctuate sharply, causing losses to the participants.

• Liquidity black hole: Trillions of dollars in funds and securities are frozen in a one-day settlement process, unable to be used for other investments, constituting a huge opportunity cost.

• Systemic risk transmission: The settlement failure of a single institution may spread rapidly through a complex clearing chain, triggering a "domino effect" and threatening the stability of the entire financial system.

Blockchain and tokenization technologies offer a radical solution to this problem—atomic swaps. Through smart contracts, the transfer of assets (cash on delivery) and the change of ownership (goods on delivery) can be completed simultaneously within a single, indivisible transaction. If either party fails, the entire transaction is automatically rolled back as if it never happened. This fundamentally reduces settlement risk to zero.

1.4 From "T+1" to "T+0": A "Quantum Leap" in the Financial System

DTCC's entry signifies that asset tokenization is no longer a small-scale experiment, but a systemic upgrade of financial infrastructure. Its most direct and significant impact is compressing the settlement cycle from "T+1" to "T+0," i.e., real-time settlement. The video describes this as "Speed is Safety" and reviews the historical lessons of 1929.

The significance of real-time settlement goes far beyond speed. It will fundamentally eliminate the enormous risk exposure caused by time lags in the financial system, releasing trillions of dollars of liquidity currently trapped in the settlement process. For institutional investors, this means lower transaction costs and higher returns on capital. For the entire financial system, it means greater resilience and stronger risk resistance.

DTCC's step is like laying the final "digital asphalt" on a series of information superhighways, allowing the "vehicles" carrying global economic value—stocks, bonds, and other assets—to travel at near-light speed without friction. A massive asset class worth $68 trillion (or even more) is preparing to flood into this emerging value internet superhighway of blockchain with unprecedented momentum. And BlackRock has already deployed significant resources at the entrance to this highway.

Chapter Two: BlackRock's Overt Strategy — From the BUIDL Fund to the "Central Bank of Everything"

If DTCC's entry into the market heralded the asset tokenization revolution, then BlackRock's actions are drawing up a detailed battle plan for this revolution. As the world's largest asset management giant managing over $11 trillion in assets, every move BlackRock makes is enough to cause an industry earthquake. Its foray into RWA is not a simple "trial run," but a meticulously planned and step-by-step "open strategy," with its ultimate goal perhaps being to become the "central bank of everything" in the future on-chain world.

2.1 BUIDL Fund: A "Precision Missile" Aimed at the Heart of DeFi

The core case study in the video is the BlackRock USD Institutional Digital Liquidity Fund, launched by BlackRock in March 2024, with its token abbreviated as BUIDL. While this product appears to be just an ordinary money market fund, its structural design contains profound strategic intentions.

Product essence: BUIDL's underlying assets are highly liquid, low-risk cash, U.S. Treasury bonds, and repurchase agreements. It is essentially a traditional financial product regulated by U.S. securities laws, designed to provide institutional investors with a safe dollar cash management tool and generate stable interest income.

Disruptive Innovation: BUIDL's disruptive nature lies in its "tokenization" of fund units, issuing them on public blockchains like Ethereum. Investors no longer hold traditional paper or electronic certificates of fund units, but rather an ERC-20 standard token. This means:

1. 24/7 Real-time Transfer: BUIDL tokens can be transferred peer-to-peer globally around the clock, eliminating the time constraints of traditional banks and securities firms.

2. On-chain transparency: Every transaction is recorded on a public blockchain, providing unprecedented transparency.

3. Programmability and composability: As a standardized digital asset, BUIDL can be seamlessly integrated into any decentralized finance (DeFi) protocol as collateral, trading pairs, or a source of yield.

The launch of BUIDL is like a precision-guided missile, directly targeting the core of the DeFi world—stablecoins. For a long time, the DeFi ecosystem has heavily relied on stablecoins issued by private companies, such as USDT and USDC. While these stablecoins provide basic liquidity for DeFi, the transparency and compliance of their reserve assets, as well as their disconnect from the traditional financial system, have always been a "sword of Damocles" hanging over their heads.

The emergence of BUIDL offers an alternative to "dimensional reduction attack." It possesses unparalleled advantages:

• Top credit backing: Issued and managed by BlackRock, the world's largest asset management company, with underlying assets being the safest U.S. Treasury bonds, its credit rating far exceeds that of any commercial company.

• Fully compliant: As a securities product registered with the U.S. SEC, BUIDL is fully compliant with regulatory requirements, paving the way for large-scale adoption by institutional investors.

• Intrinsic income: Unlike stablecoins that do not generate interest, BUIDL holders can continuously receive interest income generated by the underlying government bonds, which means it is a stable asset that “generates interest”.

2.3 Fierce Competition: The Battle for Tokenized Treasury Bonds

While BlackRock entered the market with tremendous momentum, it is not without its challenges. The tokenized US Treasuries sector has long been a battleground, attracting participation from both traditional financial giants and crypto-native protocols. Among them, Franklin Templeton is BlackRock's most direct competitor.

Franklin Templeton launched its tokenized money market fund, FOBXX (Franklin OnChain US Government Money Fund), as early as 2021, nearly three years earlier than BUIDL. FOBXX, also issued on a public blockchain, provides investors with exposure to tokenized US government bonds. By early 2026, FOBXX's size was comparable to BUIDL's, with both collectively accounting for half of the tokenized government bond market.

Besides traditional giants, crypto-native protocols like Ondo Finance have also emerged as strong contenders. Ondo, through products like USDY (US Dollar Yield Token), provides compliant, tokenized yield products backed by short-term US Treasury bonds and bank demand deposits to users worldwide (excluding the US). Ondo focuses more on deep integration with DeFi protocols, aiming to become a bridge connecting TradeFi yields and DeFi applications.

The essence of this competition is a battle for the "Base Yield Layer" of the future on-chain world. Whoever can provide the safest, most stable, and most liquid tokenized government bond products will become the most fundamental and indispensable building block in the DeFi "Money Legos" world.

"Money Lego" is the core idea of the DeFi ecosystem. It modularizes different financial functions (trading, lending, derivatives, etc.) through standardized protocols (such as the ERC-20 token standard), allowing them to be freely and permissionlessly combined like Lego bricks to create an endless array of new financial applications. A stable, compliant, and interest-bearing asset is the perfect foundation for all these superstructures. The emergence of BUIDL is like the largest, flattest, and most solid base piece in a Lego set, allowing developers to build more complex and magnificent DeFi castles upon it.

2.4 Partnering with Binance: Connecting the "Last Mile" of Liquidity

However, even the best asset is just a mirage if it lacks liquidity. BlackRock understands this well. Its most crucial move after launching BUIDL was forging a strategic partnership with Binance, the world's largest cryptocurrency exchange.

In November 2025, Binance announced that it would accept BUIDL as collateral for its institutional clients' over-the-counter transactions [2]. This collaboration is of great significance, as it perfectly solves the "last mile" problem of BUIDL and builds a powerful positive liquidity flywheel:

1. Scenario Creation: Institutional investors can now deposit their BUIDL holdings into Binance's third-party custodian bank and use them as collateral to conduct leveraged or derivative cryptocurrency trading on the Binance exchange.

2. Maximizing Capital Efficiency: Institutions no longer need to hold non-interest-bearing cash or stablecoins as margin. They can enjoy the government bond interest from BUIDL while using it as trading leverage, achieving a "two birds with one stone" effect and greatly improving capital efficiency.

3. Risk Isolation: Through Binance's "Banking Triparty" model, institutional collateral (BUIDL) is held in a regulated third-party bank (such as BNY Mellon or JP Morgan), rather than the exchange itself. This model draws on mature risk management frameworks from traditional financial markets, constructing a sophisticated "trust triangle":

1. Investors: Deposit their BUIDL assets into a segregated account at a partner bank.

2. Partner Bank: As an independent third-party custodian, it safeguards the assets and issues asset certificates to Binance.

3. Binance: Grants investors corresponding trading credit lines within the exchange based on bank asset verification.

The beauty of this arrangement lies in the fact that investors' core assets remain within a strictly regulated banking system, completely isolated from the operational risks of the exchange. Even if the exchange experiences extreme problems, investors' collateral remains safe. This significantly reduces counterparty risk for institutional participants in the crypto market, eliminating their biggest concern when entering the space.

This collaboration transforms BUIDL from a static store of value into a dynamic, efficient liquidity tool deeply integrated into the world's largest crypto market. It seamlessly connects the highest quality assets in traditional finance (US Treasury bonds) with the deepest liquidity in the crypto world (Binance exchange).

2.3 BlackRock's Grand Narrative: Becoming the "Underlying Central Bank" for All Stablecoins

A very insightful point: BlackRock's ambition may not be just to issue a successful tokenized fund, but to become the "underlying central bank" for all future stablecoins.

The logical chain is as follows:

• Define the “risk-free rate”: BUIDL’s yield is directly pegged to US Treasury bonds, which essentially defines a “risk-free rate” benchmark for the on-chain world.

• Becoming a Reserve Asset: As BUIDL's scale and liquidity continue to expand, it will become the ideal reserve asset for other stablecoin issuers, DeFi protocol vaults, and even centralized exchanges. This is because holding BUIDL is both safe (backed by BlackRock's credit and government bonds) and generates interest (continuously producing yield).

• Building a “Monetary Pyramid”: In the future, we may see a multi-layered on-chain monetary system. At the top of the pyramid are central bank digital currencies (CBDCs) issued by various countries; the foundation of the pyramid are tokenized assets like BUIDL, issued by the strongest credit entities and pegged to the safest sovereign debt. Between these two will be various algorithmic stablecoins, commodity stablecoins, and so on. BlackRock, through BUIDL, has firmly secured its position at the foundation of the pyramid.

As Larry Fink stated in his 2025 letter to shareholders, the ultimate goal of tokenization is to “create a more efficient, transparent, and accessible financial market” [3]. Through BUIDL, BlackRock is not only selling a product, but also exporting a standard, a new standard based on its credit and expertise, connecting the underlying protocols of TradeFi and DeFi. This is exactly the game that “old money” is best at: not directly participating in the front-line battles, but becoming an indispensable “utility” company for the entire ecosystem by setting rules and providing infrastructure.

Chapter 3: An Inevitable Choice Under a Dual Crisis — Why Does the World Need a New Market Worth 68 Trillion?

BlackRock and DTCC's ambitious plans are not castles in the air, but built upon profound real-world needs. The video astutely points out the two fundamental drivers propelling this tokenization revolution: a global infrastructure investment gap and a growing personal retirement crisis. These two crises point to a single solution: breaking down the barriers of traditional capital markets and channeling liquidity to private markets that offer higher and more stable returns. Tokenization is precisely the "golden key" to achieving this goal.

3.1 The "Energy Bill" in the AI Era: A Hard Shortfall of $68 Trillion

In his 2025 shareholder letter, Larry Fink used a striking figure: by 2040, the global demand for new infrastructure investment will reach $68 trillion.[3] What does this figure mean? It is equivalent to building the entire U.S. interstate highway system and transcontinental railroad from scratch every six weeks over the next 15 years.

Where does this enormous bill come from? A key driver of growth is the artificial intelligence (AI) revolution. The development of AI, particularly the training and inference of large language models, is a massive energy-consuming monster. The construction cost of an AI data center can easily reach billions or even tens of billions of dollars, and its electricity consumption is comparable to that of a medium-sized city. With the widespread adoption of AI applications, global demand for digital infrastructure such as electricity, data centers, and network bandwidth will grow exponentially.

However, traditional sources of funding—government revenue and bank loans—are no longer sufficient to support such massive investments. Governments worldwide are generally heavily indebted, with fiscal deficits reaching record highs, making it impossible for them to invest in infrastructure through large-scale borrowing. At the same time, stricter capital regulations (such as Basel III) have limited banks' long-term lending capacity. This huge funding gap can only be filled by attracting private capital.

The problem is that infrastructure projects (such as power plants, ports, and data centers) are typically privately held assets, characterized by high investment thresholds, poor liquidity, and long terms, making them inaccessible to ordinary investors. Tokenization offers a perfect solution:

• Asset securitization 2.0: Package the future revenue rights or ownership of a large infrastructure project (such as a nuclear power plant) into countless digital tokens and issue them on the blockchain.

• Lowering the investment threshold: Investors can buy any amount of tokens, just like buying stocks, and become "shareholders" of the world's top infrastructure, even with only $100.

• Creates secondary market liquidity: These tokens can be traded 24/7 on global crypto exchage or DeFi markets, greatly improving the liquidity of previously illiquid assets.

By tokenizing, the $68 trillion infrastructure investment market has been opened to hundreds of millions of ordinary investors worldwide. This not only provides funding for projects but also offers investors a new channel to share in the dividends of the times.

3.2 Public markets are failing: Capital markets need a second "democratization"

A pointed viewpoint: the public markets we know, namely the stock and bond markets, are, to some extent, "failing." This failure manifests itself on two levels:

1. The "Private Equity" of High-Quality Assets: More and more companies with the greatest growth potential are choosing to remain private for the long term rather than pursuing an early IPO. This is thanks to the booming private equity (PE) and venture capital (VC) sectors, which allow companies to secure ample funding during their private phase. As a result, by the time these companies finally go public, much of their value growth period has already passed, significantly reducing the potential returns for public investors. Ordinary people are excluded from sharing in the early-stage benefits of innovation.

2. Declining returns on traditional assets: In the context of low global interest rates and high inflation, the real returns of traditional "safe haven" assets, such as government bonds and high-credit-rating corporate bonds, are no longer sufficient to meet long-term investment needs, especially for pension funds that need to cover decades of retirement life.

This situation of "public market failure" actually exacerbates the inequality of social wealth. A small number of wealthy individuals and institutional investors who can access the private market continue to enjoy the high-growth dividends, while the vast majority of ordinary investors are trapped in the increasingly thin returns of the public market. Therefore, the capital market urgently needs a "second democratization" movement—the first being the birth of the stock market, which allowed ordinary people to own a portion of a company; the second being to break down the "Berlin Wall" between public and private funds.

Larry Fink offers a more profound perspective, arguing that this is not merely a matter of fairness, but also a question of the engine of economic growth. In his shareholder letter, he emphasizes that introducing private capital into areas such as infrastructure and private credit is the only way to resolve the dilemma of governments and banks being "willing but unable." Tokenization is precisely the "breaching hammer" of this democratization movement. Through technological means, it transforms previously "non-standard," "large-value," and "low-liquidity" private equity assets into "standardized," "small-value," and "high-liquidity" digital tokens, thereby enabling public participation.

3.3 “More Fearful Than Death”: Longevity Risks and Retirement Crisis

Another, more pressing crisis comes from each of us—we are living longer and longer.

A startling survey statistic reveals that over half of Americans fear living too long and running out of savings more than they fear death itself. Behind this lies a serious "longevity risk." With advancements in medical technology, average human lifespan continues to increase. A healthy couple who are 65 years old today has a 50% chance that at least one partner will live to be over 90. This means that retirement could last 30 years or even longer.

However, traditional retirement portfolios—60% stocks and 40% bonds (a 60/40 portfolio)—are at risk of becoming ineffective. In an era of low or even negative interest rates, bonds can no longer provide sufficiently stable returns to combat inflation and cover a long retirement. Meanwhile, publicly traded stocks are too volatile. There is an urgent need for a new asset class that can offer more stable returns than bonds while carrying less risk than pure stock speculation.

This answer also points to the private market. Private equity, private credit, infrastructure and other assets have proven to be powerful tools for optimizing long-term investment portfolios and combating longevity risk because they have low correlation with the public market and can generate stable cash flow. Larry Fink even predicted that the standard investment portfolio in the future will evolve into "50/30/20", that is, 50% stocks, 30% bonds and 20% private assets[3].

However, as mentioned earlier, the high walls of the private market keep the vast majority of ordinary people out. Tokenization once again plays the role of "wall-breaker." By tokenizing high-quality private assets and leveraging the open finance protocols of DeFi, anyone can easily allocate a small portion of their retirement savings to these assets that were previously only accessible to billionaires and large pension funds, thereby building a more resilient and truly diversified retirement portfolio.

Chapter Four: Challenges Ahead and Future Prospects

While the prospects for asset tokenization are incredibly promising, the journey to this "new continent on the blockchain" is not smooth sailing; it is fraught with hidden reefs and storms. Videos and related analyses also point out several key challenges.

4.1 The Double-Edged Sword of Regulation

Regulation is both a "passport" for RWA to enter the mainstream and its biggest "shackle." On the one hand, the emergence of fully compliant products like BUIDL has greatly boosted the confidence of institutional investors. On the other hand, regulatory policies for digital assets vary greatly across different countries and regions, and the legal framework is still imperfect. For example, the legal nature of tokens (are they securities, commodities, or new types of assets?), tax issues in cross-border transactions, and how to effectively implement anti-money laundering (AML) and know-your-customer (KYC) in a decentralized environment are all pressing problems that need to be solved. Any slight change in regulation can have a huge impact on the entire sector.

4.2 The "Three-Body Problem" of Technology: Security, Scalability, and Interoperability

Placing trillions of dollars of real-world assets on the blockchain places unprecedented demands on the underlying blockchain technology.

• Security: It is the cornerstone of all issues. Vulnerabilities in smart contracts, loss of private keys, hacker attacks—any security incident can cause catastrophic losses. This requires code to undergo the most rigorous audits and more sophisticated on-chain insurance and asset recovery solutions.

• Scalability: The transaction processing capacity (TPS) of current public blockchains (such as the Ethereum mainnet) is insufficient to meet the future demand for high-frequency trading of massive amounts of assets. Although Layer 2 scaling solutions (such as Rollups) are developing rapidly, their stability and decentralization still need time to be tested.

• Interoperability: Assets are distributed across different blockchains (such as Ethereum, Solana, BNB Chain, etc.). Achieving seamless and secure cross-chain communication between these "value silos" is key to leveraging the network effect of tokenization. The security of cross-chain bridges has always been a pain point in the industry, requiring the maturity of more underlying and secure interoperability protocols (such as CCIP).

4.3 The User Experience Gap in the "Last Mile"

For ordinary investors, the current barriers to entry for DeFi and RWA investments remain too high. Complex wallet creation, private seed phrase management, exorbitant gas fees, and user interfaces rife with technical jargon all constitute significant cognitive obstacles. True "democratization of capital markets" requires a revolution in user experience, offering interfaces as simple, intuitive, and secure as traditional brokerage apps. This necessitates collaborative efforts from wallet providers, exchanges, and protocol developers to hide complexity in the background and present convenience to users.

Conclusion: An irreversible financial migration, and where we are.

An ongoing and irreversible mega-trend is unfolding: global financial assets are undergoing an epic migration from a traditional, closed, and inefficient system to an open, transparent, and efficient on-chain system. This is not merely a technological upgrade, but a profound "democratization" movement in the capital markets.

The entry of established financial giants like BlackRock and DTCC is not intended to destroy the existing financial order, but rather to use blockchain technology to "rejuvenate" it, enabling it to better serve the economic needs of the 21st century. They bring not only massive amounts of assets and abundant liquidity, but also centuries of compliance experience, risk management capabilities, and credit backing accumulated by the traditional financial world. Their participation injects the crucial element of "trust" into asset tokenization, bringing it from the periphery to the mainstream.

Of course, the road to this revolution will not be smooth. Regulatory uncertainty, technological security, digital identity authentication, and user education are all challenges that need to be overcome. But once the wheels of history begin to turn, they do not easily stop. When a solution emerges that can bring a new $68 trillion market to hundreds of millions of ordinary investors while simultaneously resolving the global pension crisis, its realization is only a matter of time.

For each of us caught in this process, understanding the underlying logic of this transformation and discerning the strategic intentions of key players may be crucial to seizing opportunities and protecting personal wealth in the next decade. As the video concludes, we stand at the entrance to a new era, tickets are on sale, and BlackRock is attempting to become the core "ticket agent."

WeChat: battle000000

References

[1] US Securities and Exchange Commission. (2025, December 11). DTC No-Action Letter on Blockchain Tokenization Initiative. https://www.sec.gov/files/tm/no-action/dtc-nal-121125.pdf

[2] Binance. (2025, November 14). Binance Integrates BlackRock's BUIDL Fund into Institutional Collateral Framework. https://www.binance.com/en/blog/adoption/7508340130258534402

[3] Fink, L. (2025). Larry Fink's 2025 Chairman's Letter to Investors. BlackRock. https://www.blackrock.com/corporate/investor-relations/larry-fink-annual-chairmans-letter