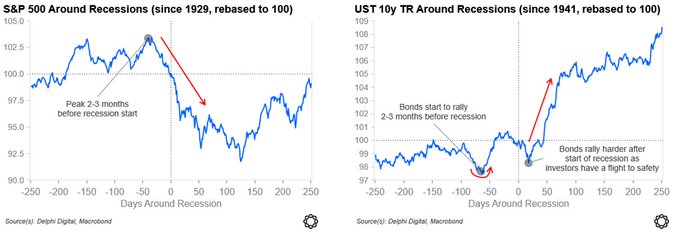

Markets are not pricing a recession. Both positioning data and current price levels highlight the disconnect between risk assets and what are the relatively clear macro consequences of an energy shock on the economy. Meanwhile, the macro setup is fragile, leaving the economy susceptible to a shock. The US fiscal impulse is negative and set to worsen. Global liquidity offers little margin of safety. Central bank easing breadth is rolling over. And supply-driven inflation is rising at the worst possible time. Roughly 20 to 30% of global crude, LPG, LNG, and key commodity flows pass through the Strait of Hormuz. The conflict dynamics suggest this drags on. Iran is fighting a narrative war where capitulation is existential. The US and Israel cannot walk away without ceding control of the Strait. History says these conflicts take longer and cost more than anyone projects at the outset. Every recession since 1990 (excluding 2020) was preceded by an abrupt rise in energy prices. If oil remains elevated into April and makes a new high, recession becomes the base case. twitter.com/Delphi_Digital/sta...

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content