Author: Adhi Rajaprabhakaran

Compiled by: Jia Huan, ChainCatcher

On the evening of February 12th, in an exchange that typically reacts little to sporting events, three NBA games suddenly ignited the trading market: the Dallas Mavericks vs. the Los Angeles Lakers, the Milwaukee Bucks vs. the Oklahoma City Thunder, and the Portland Trail Blazers vs. the Utah Jazz. These three games generated over 13 million contracts traded. ForecastEx, a prediction market operated by Interactive Brokers and regulated by the U.S. Commodity Futures Trading Commission (CFTC), is a licensed, legitimate exchange, but prior to that night, it had never seen any substantial NBA trading volume.

I don't believe ForecastEx created any customer acquisition miracle overnight. It didn't improve its product, launch a marketing campaign, or deepen its order book with more liquidity. What happened was actually quite simple: Robinhood directed its massive order flow to another exchange specifically for this night consisting of three NBA games.

Currently, Robinhood dominates the retail distribution of prediction market contracts. When a user opens the Robinhood app, clicks on an NBA game, and places a bet, the trade is assigned to an exchange regulated by the CFTC for execution. For most of Robinhood's prediction market history, this exchange has been Kalshi. But users are unaware of this, and they don't care. Regardless of which exchange is behind it, the interface is exactly the same: the same app, the same buttons, the same odds. The exchange has become an invisible infrastructure.

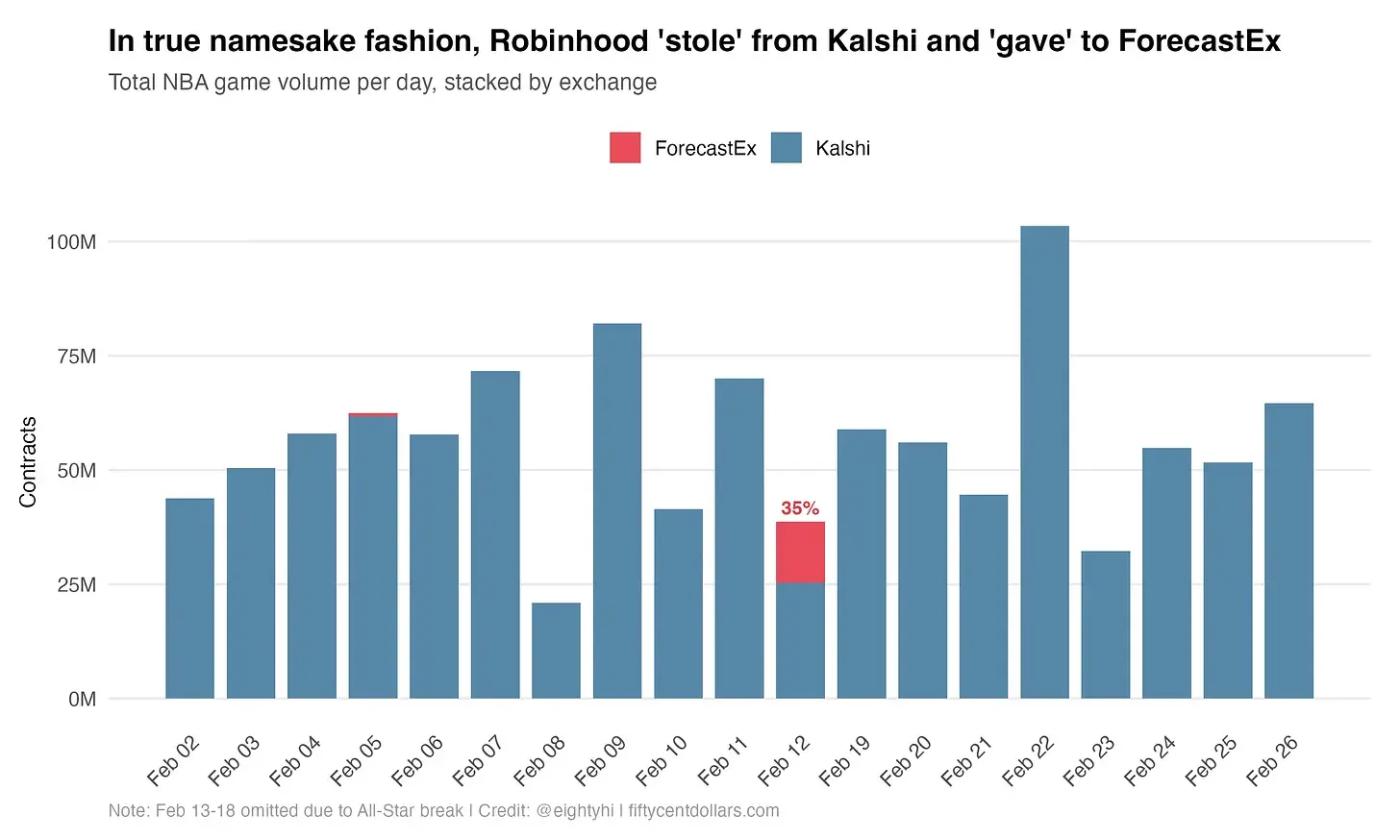

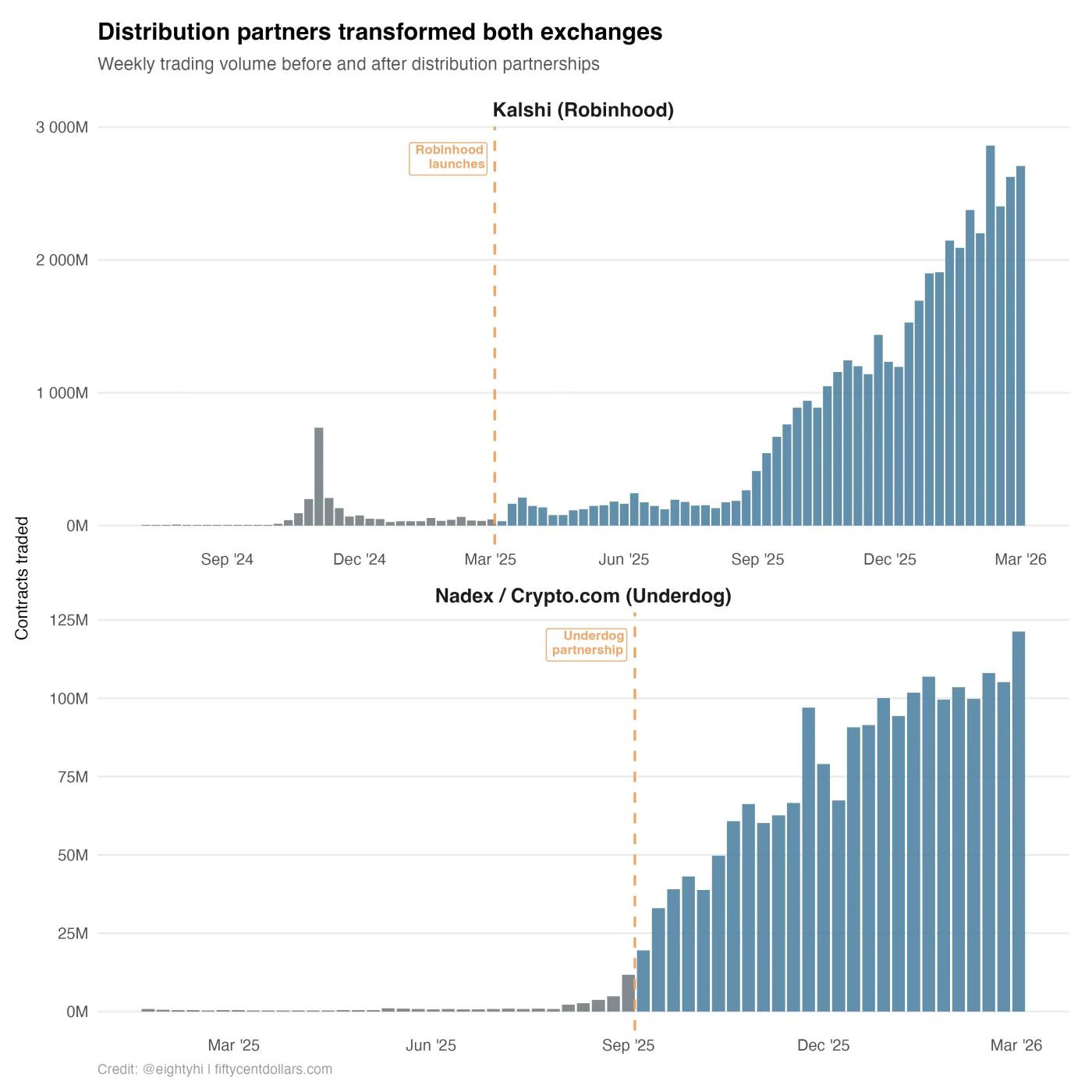

A sudden migration of 35% of trading volume

Each bar represents a day's NBA game trading volume, stacked by exchange. Blue represents Kalshi, and red represents ForecastEx. Except for February 12th, every day was entirely blue, but on that day, 35% of the trading volume suddenly appeared on ForecastEx. Then everything returned to being entirely blue, as if nothing had happened.

The red area on February 12th represents those three games: Mavericks vs. Lakers, Bucks vs. Thunder, and Trail Blazers vs. Jazz. Together, they generated 13.4 million contracts on ForecastEx. Regardless of which exchange handles the trades, Robinhood's user experience is identical: the same app, the same buttons, the same odds. Users can't tell the difference. Because to them, there truly is no difference.

This is why the 35% figure is so important, as it's a relatively straightforward metric for measuring Robinhood's market share of NBA betting volume on both exchanges. ForecastEx has virtually no organically built-up sports betting user base, so it's reasonable to assume that every contract on ForecastEx that night originated from a Robinhood order.

Furthermore, since Robinhood's interface remains the same under all circumstances, these users place bets at exactly the same frequency as on Kalshi. It's reasonable to infer that approximately one-third of Kalshi's NBA betting volume in February came from Robinhood.

Robinhood controls where the trading volume goes, and it can flip that switch overnight.

Similar stories on the weather track

The NBA's order backlog was brief and dramatic, constituting a remarkably clear and compelling natural experiment for analysis. However, the rise of the weather market on ForecastEx tells a similar story on a different scale.

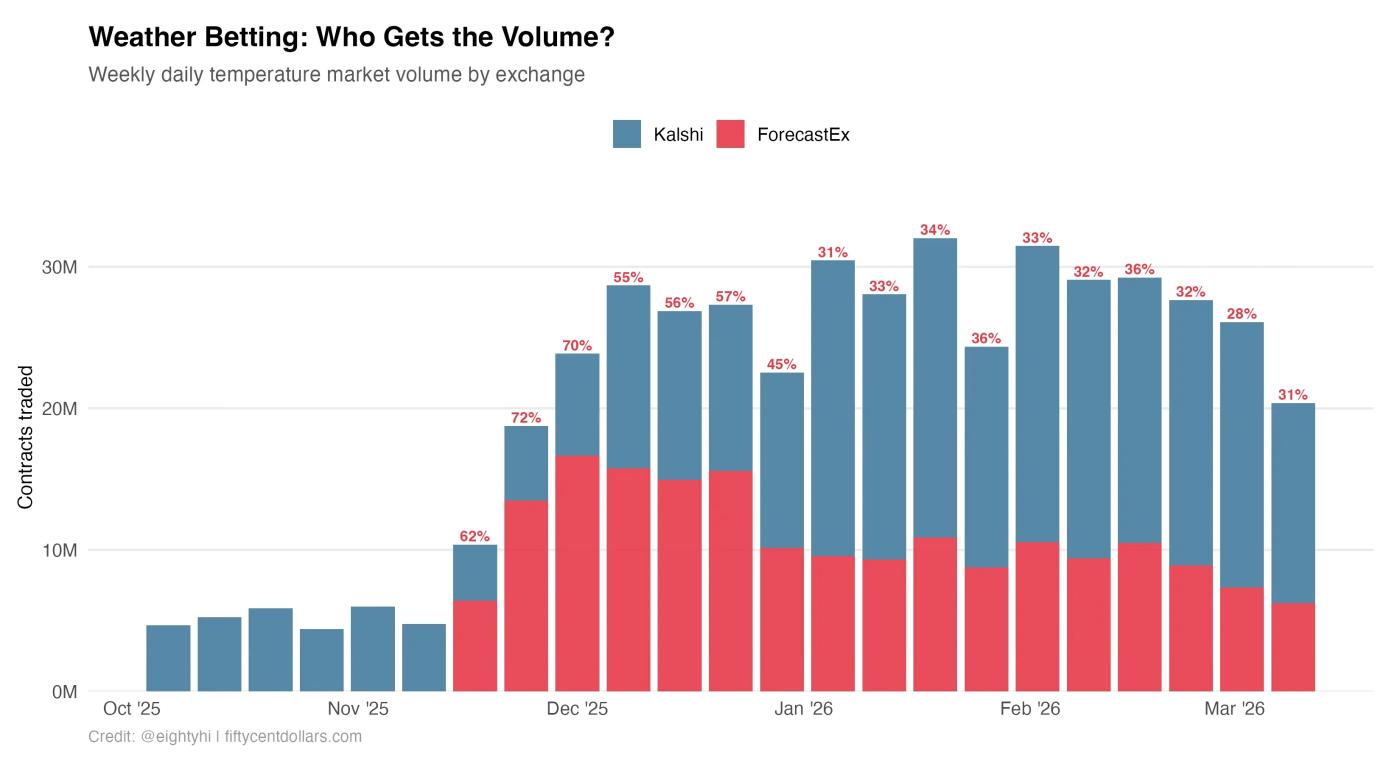

Both ForecastEx and Kalshi offer daily high temperature contracts: binary options on whether a city's high temperature will exceed a given threshold on a given day. These two markets offer the same product, covering the same cities and dates. The only real difference lies in the exchange that matches the trades.

Prior to November 18, 2025, weather trading activity on ForecastEx was zero. Then, trading volume exploded overnight, without a spontaneous growth transition period or a gradual adoption curve. This step function pattern is perfectly consistent with the characteristics of the NBA. To measure overlap, I matched markets on ForecastEx and Kalshi that had the same "city-date" pair, excluding cities that existed on only one exchange. This yielded 454 matching "city-date" pairs.

Incidentally, this chart provides an interesting case study illustrating that platform competition is a net positive for trading volume across the industry. Robinhood's opening of the weather market boosted overall activity on both exchanges, likely due to cross-exchange arbitrage. Market makers participating in such activities effectively distribute liquidity throughout the ecosystem.

For the first five weeks, only Kalshi was available, which served as the baseline. Then ForecastEx emerged and immediately captured 60% of the total daily temperature market trading volume. It peaked at 72% in late November and has since generally remained between 53% and 67%.

The key detail is that Kalshi's weather trading volume didn't collapse when ForecastEx appeared. The blue bars remained roughly stable. Therefore, my interpretation is that ForecastEx's trading volume was superimposed on Kalshi's existing traffic. This likely means that Robinhood opened its weather marketplace for the first time and started sending its traffic to ForecastEx from the beginning without its users' knowledge.

This distinction is crucial. In the January NBA case, Robinhood briefly diverted trading volume that was originally flowing to Kalshi. In the weather market, Robinhood appears to have added ForecastEx as a parallel destination while keeping Kalshi's original traffic intact. Both scenarios demonstrate the same structural point: Robinhood determines where trading volume goes. Exchanges can only passively receive the orders that Robinhood chooses to deliver.

Distribution channels amplify the impact of product innovation.

NBA and weather data suggest that Robinhood can drive traffic. Meanwhile, parlay betting (combining two or more independent bets into a single bet; a player wins only if all the outcomes of the parlays are predicted correctly; if any one is wrong, the entire bet is lost. Because of the increased difficulty, the odds and rewards are usually very high) suggests that it can amplify already growing demand.

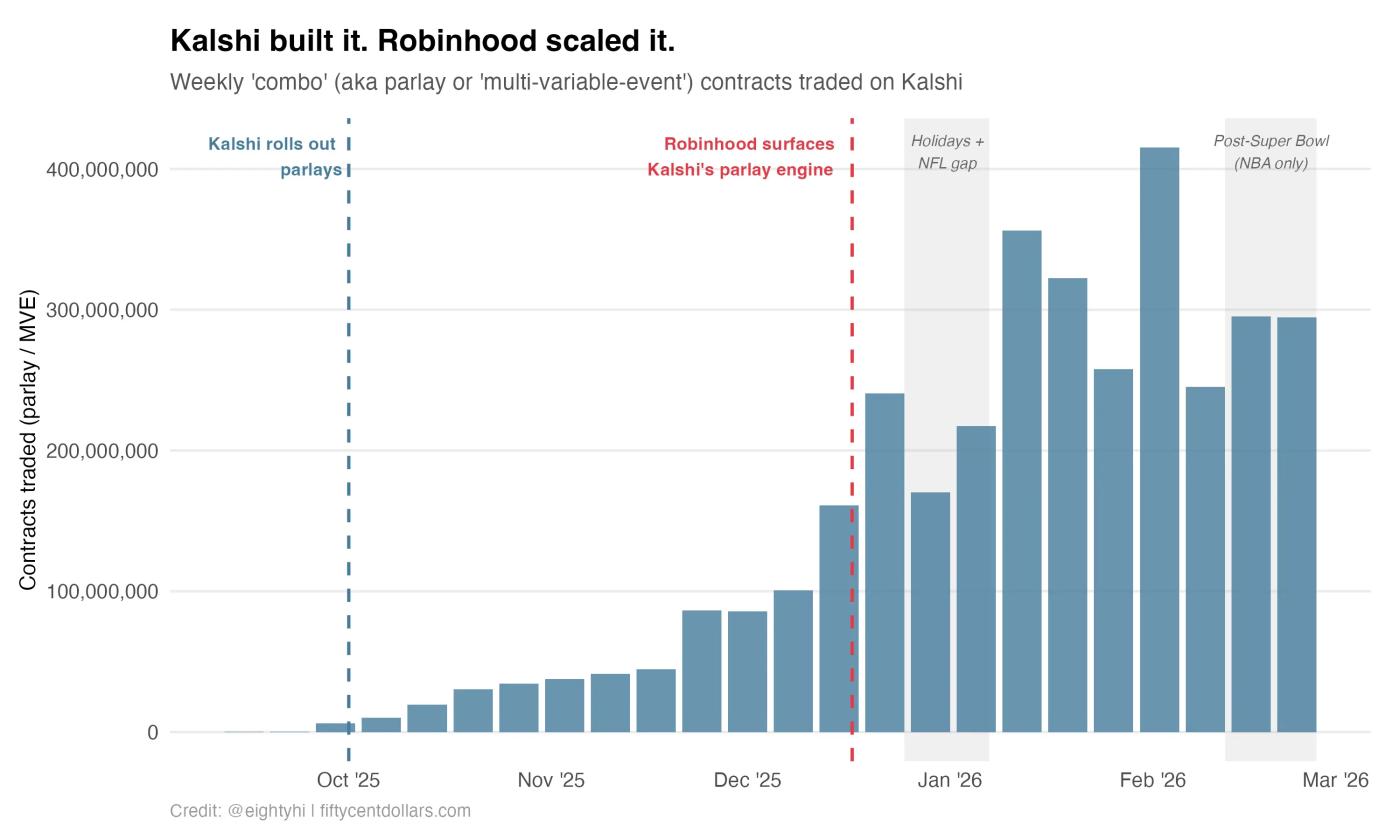

Kalshi launched multivariate event contracts (i.e., "combinations" or "passes") in September 2025, coinciding with the start of the NFL season. The product immediately gained attention: weekly trading volume organically grew from almost zero in September to approximately 45 million contracts per week by early December. This growth was self-driven and directly linked to Kalshi's platform. Kalshi built the product, submitted it for CFTC certification, and injected initial liquidity. The market responded positively.

Robinhood then intervened.

On December 17th, Robinhood announced the launch of pre-set parlays and player item predictions within its app. Within just a few weeks, weekly trading exploded, jumping from the 45-60 million range to nearly 100 million, then reaching 300 million per week in late January. The shaded area on the right marks the period after the Super Bowl, when NFL parlays disappeared, leaving the product solely supported by the NBA. Even without football, trading volume remained around 260-290 million per week.

Kalshi did the hard work of creating new product categories. Robinhood's distribution channels elevated it to a completely different scale. Both made real contributions. The question is, which one has greater structural leverage?

Not just Kalshi

Kalshi has experienced tremendous growth over the past year, from approximately 7 million contracts per day at the end of 2024 to over 100 million by the end of 2025. This isn't solely due to Robinhood. Kalshi has built real, direct demand: new product categories, a growing native user base, API traders, and institutional participation. A year ago, it was widely believed that Robinhood accounted for the vast majority of Kalshi's trading volume. Today, NBA data suggests that Robinhood accounts for approximately 35% of win/loss betting volume. This risk-free business execution is truly admirable.

However, Kalshi is not the only exchange that has built its growth story on its distribution channels.

Nadex, a CFTC-regulated exchange operated by Crypto.com Derivatives, tells a strikingly similar story. Before Underdog's integration with Crypto.com in September 2025, Nadex's trading volume was unremarkable. After Underdog stepped in and began directing its users' sports betting to the exchange, weekly trading volume exploded. Same pattern, different name. Underdog is to Nadex what Robinhood is to Kalshi: the distribution layer that transforms a stagnant exchange into a bustling hub.

The most remarkable thing is that both of these distribution giants have now taken action and fully own their own exchanges. Robinhood acquired its own CFTC-regulated exchange, and Underdog did the same last week. The two companies, on parallel tracks, independently reached the same conclusion.

This is no coincidence. It's game theory. If you're a distributor directing millions of trades to third-party exchanges, you're taking a cut of every contract—infrastructure that your users can't distinguish from a white-label API. You're also handing over data, trading volume, and regulatory records to potential competitors, the very elements that make their exchanges valuable. When you're large enough, the rational move is to internalize that infrastructure. The exchange transforms from someone else's profit center into your cost center.

Weather and NBA data explain why this dynamic is so difficult to defend against from an exchange's perspective. Even with only 35% of trading volume, Robinhood could add a parallel exchange to the weather market overnight and immediately send most of the new traffic to it. It could direct three NBA games to another exchange on Tuesday, generating the same trading volume as anywhere else. Users are completely unaware. They don't choose exchanges. They choose Robinhood, or Underdog.

I was wrong

Last year, when rumors circulated that Robinhood was considering acquiring its own CFTC-regulated exchange, I publicly stated that it was impossible.

I was so confident that I was wrong for two reasons.

First, from my experience in Kalshi, I know firsthand how incredibly difficult it is to build and operate a regulated derivatives exchange: compliance infrastructure, monitoring systems, CFTC reporting, and so on. Robinhood earns huge revenues from prediction markets while doing only about 1% of the work. The exchange does the hard work, while Robinhood collects distribution fees—it's been the perfect partnership in fintech for years! Why break this deadlock?

Secondly, I applied the traditional thinking behind the derivatives market structure of the past fifty years. Brokers don't acquire exchanges. In the world I'm familiar with, the entire significance of an exchange lies in its irreplaceable trading channel. The Chicago Mercantile Exchange (CME), a $90 billion company with a net profit margin second only to Visa and Mastercard, owes its unbreakable moat to "liquidity depth."

An institutional trader managing a $50 million Brent crude position would be extremely concerned with order book depth, slippage, and counterparty concentration. This depth is incredibly difficult to establish and virtually impossible to replicate, especially in derivatives markets where contracts cannot be swapped across exchanges. In that world, exchanges have earned their structural dominance through their own strength. Brokers, on the other hand, are readily replaceable commodities.

Prediction markets have overturned this. On Robinhood, the average sports bet is simply an average user clicking a button and betting $10 on the Lakers. That user doesn't care about order book depth. Damn, they don't even know what an order book is. When trades are small and users aren't sophisticated enough, liquidity depth is no longer a moat. Robinhood changed its underlying pipeline one Tuesday night, but the same trading volume kept pouring in.

When the transaction size is extremely small and the users are not professional enough, liquidity depth is no longer a moat.

I was wrong, because I was still navigating with outdated maps. The structural leverage of predicting markets doesn't lie where the history of derivatives over the past fifty years has pointed. It truly resides in the hands of the ultimate users.

In fact, I've already written a rather blunt article about how ForecastEx messed up sports events. That might have resonated with some readers… There was also a tiny amount of activity on ForecastEx on February 5th that I can't explain. This could have been an early test by Robinhood. It's also possible that Robinhood is distributing traffic across multiple exchanges, but outside analysts have no way of knowing. I think this example is debatable because Kalshi's RFQ (Request for Quote) system and massive market-making network are indeed difficult to replicate here. There's an extremely deep technological moat there. Furthermore, the question of 'how important liquidity is in prediction markets' remains unresolved. This makes me wonder: under game theory, are we heading towards a homogenized competition finality—all exchanges trapped in a quagmire of imitation, vying to list on every market available?