Original title: What I Learned from Two Weeks Inside China's AI Ecosystem

Original author: José Maria Macedo, co-founder of Delphi Labs

Original article translated by: TechFlow TechFlow

TechFlow Dive: The founder of Delphi Labs spent two weeks intensively visiting China's AI ecosystem, meeting with a large number of founders, investors, and CEOs of listed companies.

His conclusions were unexpected: he was more optimistic about hardware than expected, more pessimistic about software than expected, and his observations of Chinese founders overturned his previous understanding.

The article also touches on popular topics such as valuation bubbles, the humanoid robot industry, and information asymmetry between China and the West.

The full text is as follows:

I spent two weeks in China, meeting with a large number of founders, VCs, and CEOs of listed companies in the AI ecosystem. Before going, I was optimistic about this ecosystem, expecting to see world-class AI talent working at valuations far lower than in the West.

When I left, my perspective had changed—becoming more specific: the hardware was stronger than I had anticipated, the software was weaker than I had expected, and some of my observations about the Chinese founders also surprised me.

The founder's problem

The outstanding founders I've invested in share a common characteristic: independent thinking, rebelliousness, extreme focus, and unwavering dedication. They don't listen to advice. They constantly ask "why" and refuse to accept secondhand wisdom. Their decisions may seem inexplicable to outsiders, but they themselves find them perfectly logical. They possess an inner, uncontrollable intensity, often manifesting as a long-term obsession and excellence. As a VC, I meet countless intelligent people every day, and these are the kinds of people you can spot at a glance because their life trajectories have a distinct "sharpness."

Many of the founders I met in China were a different type, which surprised me.

They were exceptionally talented—top universities, resumes from ByteDance or DJI, Nature publications, multiple patents. In the West, these achievements are reserved for the most elite technical talent; in China, they're the entry ticket. They also worked harder than almost everyone I've ever met. We had meetings at all hours, even on weekends, rushing between cities. One founder even came to see us on the day his wife gave birth.

But independent thinking, a rebellious spirit, and a vision to go from zero to one—these are even harder to find. The founders' backgrounds are highly similar, their pitches tend to be conservative, and many ideas are simply upgrades of existing products (impressive V2s) rather than truly original gambles. Given the sheer size of China's tech talent pool, I had expected to encounter more people "bringing ideas I've never heard of before."

My interpretation is that China's education system cultivates excellence, but it doesn't leave enough room for deviation . It produces top-notch implementers who excel at solving known problems, rather than those who "appear with a problem that nobody knows exists."

VC is reinforcing this model

What's even more interesting is that local investors are exacerbating this trend.

Most Chinese funds' investment logic is based on one premise: invest in the best people who came from ByteDance or DJI. They look at resumes, not talent; background, not beliefs. VCs themselves also portray themselves this way—from large companies or consulting and investment banking backgrounds, very similar to European VCs a decade ago.

Ironically, most of the founders of truly great Chinese companies throughout history never actually worked for a large corporation. Jack Ma was an English teacher who took the college entrance exam twice before finally getting accepted. Ren Zhengfei founded Huawei at 43, having previously served in the military. Liu Qiangdong started by selling goods at a market stall. Wang Xing dropped out of his doctoral program to start his own business. More recently, Liang Wenfeng, who runs DeepSeek, has never worked outside his own company. These people are outliers, those without a "standard resume"—precisely the kind of people the current investment system misses.

There are real alphas among these people, but it seems that very few people are looking for them right now.

Shenzhen and hardware ecosystem

The most impressive thing I've seen in China isn't any startup pitch.

It's like an underground hardware workshop in Shenzhen—engineers systematically acquire high-end Western products, disassemble them component by component, and reverse engineer everything in an extremely rigorous manner. When I emerged from that workshop, I honestly wasn't sure if most Western hardware founders understood what they were competing against. The network effect here isn't theoretical; it's physical, intensive, and the result of decades of accumulation.

The entrepreneurs we met confirmed this with data: over 70% of their hardware investment came from the Greater Bay Area, and nearly 100% from mainland China—meaning their iteration cycles are something Western hardware companies simply cannot match.

Most of the founders I've met are using DJI's strategy: focus on a niche market of consumer hardware—electric wheelchairs, lawnmowers, next-generation fitness equipment—build eight- to nine-figure revenues (in US dollars), and then leverage their customer base or underlying technology to enter adjacent product categories. Some of these companies are already much larger than you might imagine. The strongest company I saw this time was Bambu Labs, a 3D printing company that most Westerners haven't heard of, reportedly with annual profits of $500 million, doubling every year.

Bearish on Chinese software

When I left, my skepticism about the Chinese software opportunity was even deeper than when I arrived.

At the modeling level, China's open-source models are indeed very strong, but closed-source models still lag significantly behind the best in the West, and this gap may be widening. The difference in capital expenditure is enormous. GPU acquisition remains limited. Western labs are increasingly cracking down on distillation. Revenue figures speak for themselves: Anthropic reportedly generated $6 billion in ARR in February alone. The best Chinese modeling companies, on the other hand, generate ARR in the tens of millions of dollars.

In the software startup arena, the mainstream profile consists of PMs and researchers from ByteDance, developing academic or ambient consumer software for Western markets. While the talent pool is undeniably strong, many of these products fall within the scope of features natively released by large labs—potentially rendering them redundant with a single release. Another surprising point is the lack of large, rapidly growing privately held software companies in China. In the West, besides model companies, a number of startups are already achieving nine-figure or even ten-figure ARR (Average Revenue Per Transaction), with astonishing growth rates—Cursor, Loveable, ElevenLabs, Harvey, and Glaan. Breakthrough privately held software companies at this level are virtually nonexistent in China—a few exceptions like HeyGen, Manus, and GenSpark, but those companies eventually left after achieving success.

Valuation bubble

Despite the poor software performance, the bubble is real – both in the early and late stages.

In the early stages, top talent from ByteDance, DeepSeek, and The Dark Side of the Moon were indeed significantly cheaper than their American counterparts of similar caliber, but median valuations have converged. Valuations of $100 million to $200 million for consumer startups without products are common. Seed and pre-seed funding rounds exceeding $30 million are not unusual.

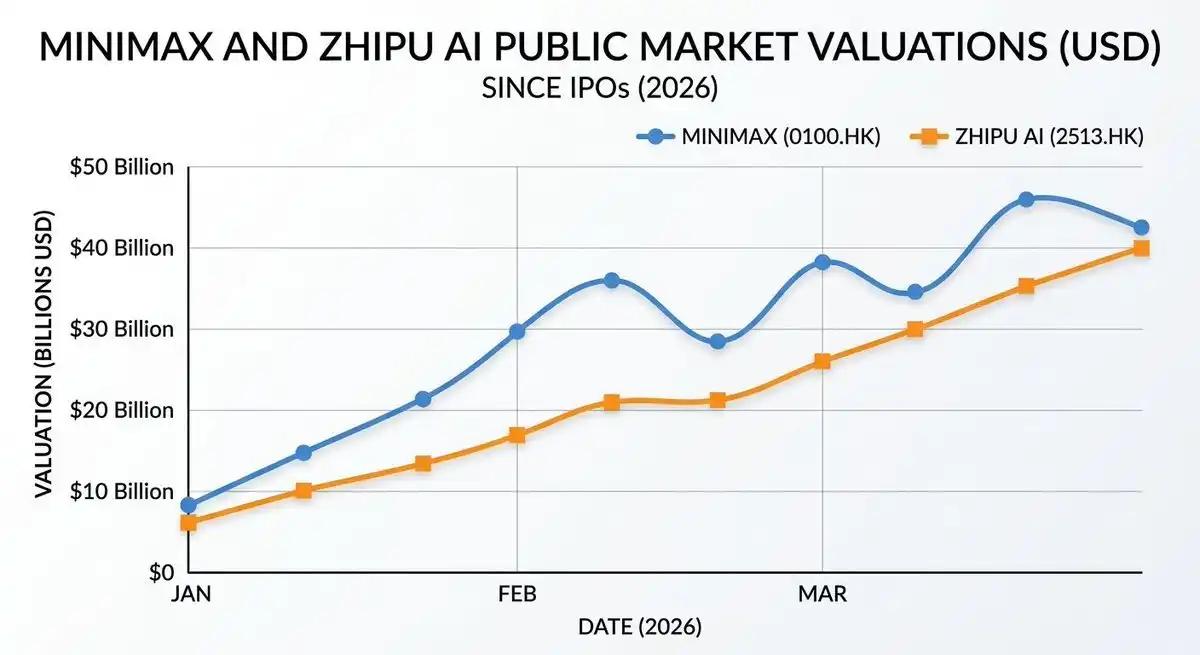

Later-stage figures are even harder to justify. MiniMax is valued at approximately $40 billion in the public market, with an ARR of less than $100 million—roughly 400 times its revenue. Zhipu is valued at approximately $25 billion with $50 million in revenue. For comparison: OpenAI's highest valuation round was approximately 66 times its ARR, and Anthropic's was approximately 61 times.

Privately held companies like Dark Side of the Moon used these public market benchmarks to raise funds—rising from $6 billion to $10 billion and then to $18 billion within a few months. Those familiar with crypto will recognize this pattern: investors compare private valuations to a pre-unlocked public market price. Furthermore, the ability of companies like Zhipu and MiniMax to maintain this level is partly due to their current status as the only source of exposure to the "Chinese AI narrative," which inherently carries a premium.

However, as more companies go public, this premium will be diluted. Finally, the IPO window has one major characteristic—it closes suddenly, without warning. No one can guarantee that you'll have time to close out your arbitrage before the benchmark price moves.

The humanoid robot sector presents a similar situation. China has approximately 200 humanoid robot companies, with about 20 having raised over $100 million, and several valued at billions—almost all without revenue. Most plan to IPO in Hong Kong in 2026 or 2027. If this market is genuine, China's hardware advantages make the long-term landscape relatively clear. However, commercialization may be much slower than the current fundraising pace suggests, and I doubt whether the Hong Kong stock market can support the large number of multi-billion dollar humanoid robot companies currently queuing for IPOs. I'm staying away for now.

Image: I couldn't resist sharing a video I filmed of a humanoid robot doing a front flip.

Information asymmetry that deserves attention

One thing surprised me: almost every founder I met focused on the global market before moving to the Chinese market. They used Claude Code, watched Dwarkesh's podcast, and were extremely knowledgeable about the San Francisco startup ecosystem—often more so than Western investors who hadn't been following it closely.

The West's hostility towards China is significantly greater than China's hostility towards the West . Chinese founders believe that combining China's engineering execution capabilities and hardware expertise with the West's go-to-market and product-centric thinking is not contradictory at all. When this combination takes shape within a suitable founding team, it can give rise to some truly remarkable companies.

Finding these founders—those who don't fit the "standard resume template" optimized by the local VC system—is what we're doing now.

Special thanks to @woutergort for opening up his excellent network of Chinese contacts, @PonderingDurian for organizing this trip, and Claude for patiently editing my ramblings on the plane.