Faced with the new industry order reshaped by the White House Framework, corporate decision-makers must not harbor illusions of a "cyclical recovery," but must carry out a strategic restructuring based on a bottom-line mentality.

Article author and source: 0x9999in1, ME News

Introduction: From "Wild Growth" to the Complete Takeover by "National Will"

On March 20, 2026, the White House officially released the "National Artificial Intelligence Policy Framework" (hereinafter referred to as the "Framework"). If the global AI industry has been racing ahead for the past two years, driven by Moore's Law of computing power and the spirit of open source, then this 100-page policy document marks a complete takeover of the development path of Artificial General Intelligence (AGI) by "national will." According to long-term tracking and data comparison by ME News Think Tank, this "Framework" is not a simple continuation of the "Executive Order on Safe, Reliable, and Trustworthy Artificial Intelligence" issued at the end of 2023, but rather a strategic leap from "defensive regulation" to "offensive industrial deployment."

This article will strip away the policy text to deeply analyze the core logic of the Framework, and combine detailed data and cases to extrapolate its future impact in dimensions such as computing power geopolitics, competition for basic models, and the integration of Web3 and AI, providing decision-makers with highly insightful industry perspectives.

Core Content Deconstruction: The Balancing of Security Bottom Line and Technological Hegemony

The framework contains a vast amount of information, but its core focus can be summarized in three dimensions: absolute control of the computing power supply chain, "access-based" regulation of basic large-scale models, and the redistribution of benefits related to data and copyright.

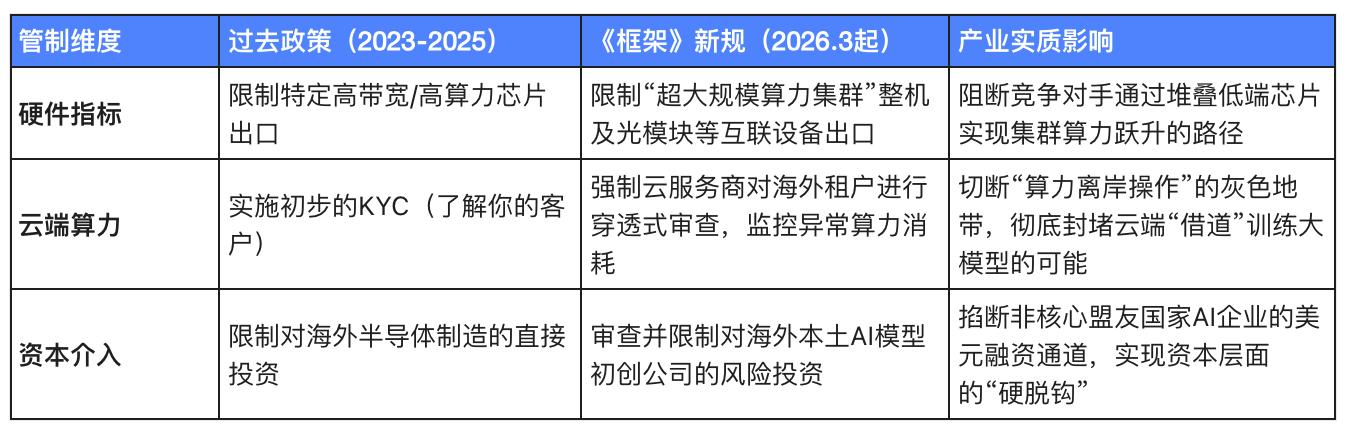

Upgraded Computing Power Control: From "Precision Strike" to "Complete Ecosystem Blockade"

The most noteworthy provision in the framework is the further tightening of restrictions on high-end computing chips and cloud computing power leasing. Past export controls mainly targeted single-chip computing power indicators (such as interconnect bandwidth and floating-point computing power), while the new framework extends regulatory reach to "system-level capabilities of computing power clusters" and "cross-border calls to cloud computing power APIs".

Data shows that computing power dominance has become the forefront of geopolitical competition. Taking market data from the fourth quarter of 2025 as an example, eight of the world's top 10 AI large-scale model training clusters are located in North America, and all of them use GPU architectures with tens of thousands of GPUs.

(Table 1: Comparison of the evolution of US AI computing power and ecosystem management policies)

This shift means that future AI computing power will be transformed into a strategic resource similar to "enriched uranium." The White House is attempting to lock the world's most cutting-edge AI technologies within its own borders and those of its core allies by establishing a computing power alliance system similar to the Nuclear Non-Proliferation Treaty.

Basic Model Regulation: The debate between open-source and closed-source approaches has been officially settled.

The framework sets unprecedented compliance thresholds for foundation models. The document stipulates that models with training computational power exceeding a certain threshold (10^26 FLOPS) must undergo red-teaming tests by a national-level AI security committee before release, and must be required to embed an immutable watermark in the generated content (such as the mandatory promotion of SynthID technology).

On the surface, this policy is intended to prevent deepfakes, biosafety risks, and election manipulation. However, from a business perspective, it is a implicit protection for "closed-source giants." Open-source communities (such as some geek projects in the Hugging Face ecosystem) will face extremely high policy risks due to a lack of sufficient funding for extensive compliance testing.

We believe this signifies that the White House has completely sided with "closed source to ensure control" over "open source to promote innovation." The oligopoly of closed-source models will effectively build extremely high regulatory barriers by participating in the development of red-blue team competition standards, keeping startups with fragile funding chains out of the AGI arena.

Independent perspectives and future impact projections

Based on the above policy analysis, we propose the following three core projections for the global AI and technology industry landscape over the next 3-5 years.

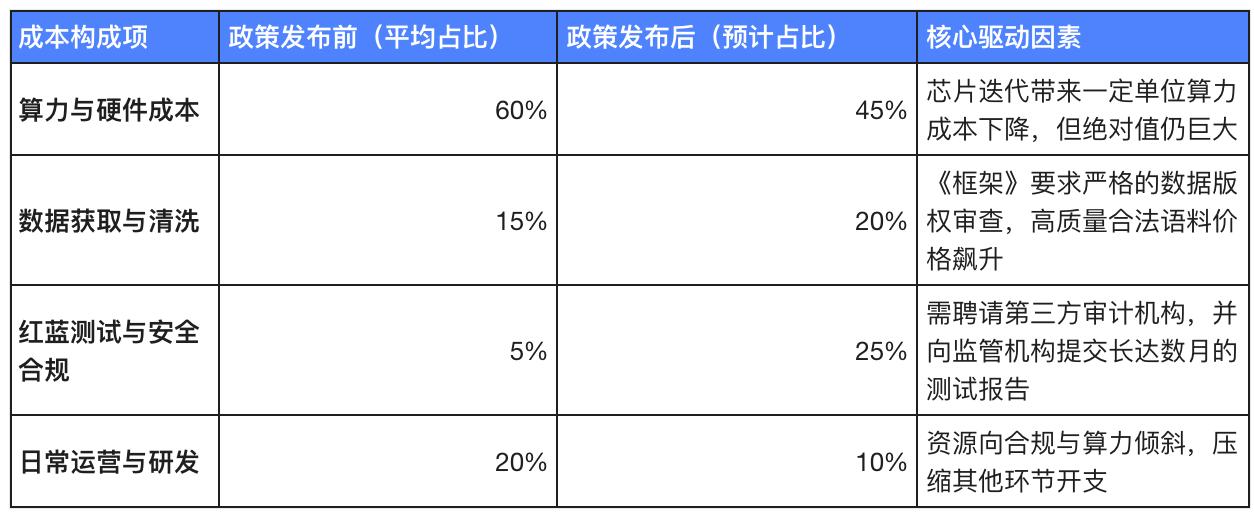

Viewpoint 1: Soaring compliance costs have ushered in an "oligopoly game" for AI foundational model startups.

The implementation of the framework marks the complete end of the romantic era of "training world-class large-scale models in a garage." With increasingly detailed requirements for security reviews, data traceability, and copyright compliance, the non-technical costs for AI companies will increase exponentially.

According to publicly disclosed market data and industry estimates, training a model with hundreds of billions of parameters, comparable to the current state-of-the-art technology, would cost hundreds of millions of dollars in computing power alone. With the release of the new framework, compliance costs will become an even greater and unbearable burden.

(Table 2: Forecast of the Evolution of the Cost Structure for the Development of Large-Scale Basic Models)

Our clear assessment is that in the future, no more than five companies globally will be capable of sustaining iterative development of cutting-edge, fundamental models. Small and medium-sized AI startups will completely abandon the development of basic models, fully transitioning to application-layer (Agent, vertical industry fine-tuning) development, or relying on the ecosystems of large companies. This is not merely a gap in computing power, but a devastating blow from both capital and compliance capabilities.

Viewpoint 2: The era of "great divergence" has arrived, and the global AI ecosystem is heading towards complete decoupling.

The Framework is not only a domestic policy, but also a declaration of global digital hegemony. By imposing dual restrictions on computing power and capital, an irreversible "Great Divergence" will occur between China and the United States, and even globally, in the AI technology stack.

This decoupling is not only reflected in the chip supply disruption, but also in the comprehensive differentiation of underlying architecture, open-source ecosystem, and application implementation. On the one hand, the US-led ecosystem will launch a sprint towards multimodal and general artificial intelligence (AGI) based on the most advanced computing power; on the other hand, countries limited by computing power bottlenecks will be forced to take another evolutionary route—namely, the route of "algorithm optimization under computing power degradation".

This will objectively force technology companies outside the US to abandon their blind worship of "parameter scale" and instead seek breakthroughs in hybrid expert models (MoE) that are characterized by "small data, high verticality, and edge operation (Edge AI)". For example, in the fields of industrial internet, smart manufacturing, and autonomous driving in closed scenarios, the dependence on extreme computing power is relatively low, which will be a structural opportunity to break through the current limitations.

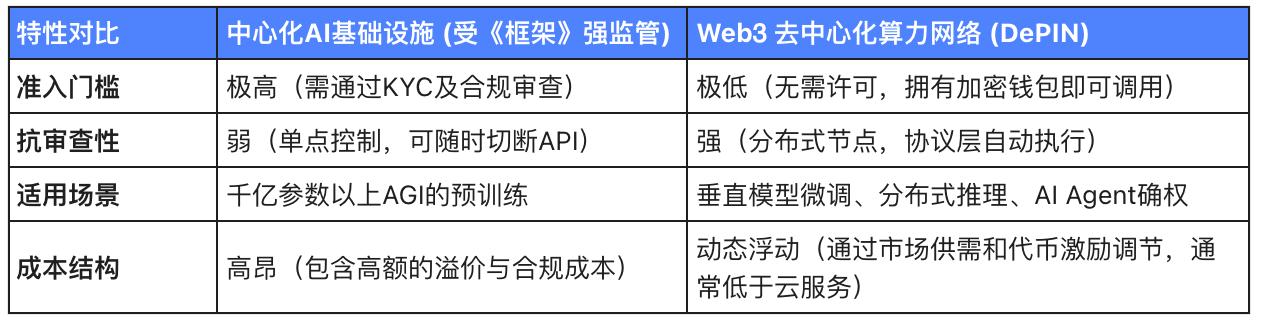

Viewpoint 3: The deep integration of Web3 and AI will become the inevitable way to break the monopoly of computing power.

In response to the trend of high centralization and oligopoly brought about by the White House Framework, ME News think tank believes that the self-regulating mechanism of the free market will give rise to a powerful counterforce, and the combination of Web3 and AI (Crypto x AI) will usher in a historic breakthrough.

With centralized cloud service providers (such as AWS and Azure) facing strict censorship and API call restrictions, a large number of developers operating on the fringes of regulation or constrained by geopolitical policies will urgently need a permissionless, censorship-resistant computing environment. The Decentralized Physical Infrastructure Network (DePIN) will directly address this overflowing demand.

Incentivizing the use of tokenomics to build decentralized computing networks from idle GPUs worldwide (such as consumer-grade graphics cards and idle computing power of small and medium-sized enterprises) may not be as efficient as centralized data centers in terms of cluster communication, but it has already demonstrated high commercial viability for fine-tuning AI models, federated learning, and decentralized inference.

(Table 3: Comparison of centralized AI infrastructure and Web3 decentralized computing networks)

We can assert that the core narrative of Web3 over the next three years will no longer be simply financialization, but rather becoming the infrastructure to combat the totalitarianism of AI computing power. Technical protocols capable of solving distributed computing collaboration, network latency optimization, and proof of computation in decentralized networks will give rise to super unicorns with market capitalizations in the hundreds of billions.

Recommendations from policymakers: Seek out structural benefits in the gaps.

Faced with the new industry order reshaped by the White House Framework, corporate decision-makers must not harbor illusions of a "cyclical recovery," but must carry out a strategic restructuring based on a bottom-line mentality.

First, strategically abandon the "large and comprehensive" approach and fully embrace the "small and beautiful" vertical market. For companies without substantial dollar capital backing, blindly investing heavily in large-scale model pre-training is tantamount to drinking poison to quench thirst. Decision-makers should quickly narrow resources to the edge closest to commercial monetization. Utilize anonymized and clearly proprietary industry-specific data to train small to medium-sized vertical models (SLMs) with tens of billions of parameters. In fields such as medical image analysis, high-frequency quantitative finance, and precision manufacturing defect detection, companies with high-quality industry know-how and closed-loop data will have a far greater commercial moat than companies that simply provide API wrapper services.

Secondly, it's crucial to proactively develop decentralized computing power (DePIN) and on-chain AI asset ownership verification. As ME News Think Tank predicted at the beginning of the year, computing power shortages will be a long-term reality. Companies with overseas expansion needs should actively explore and connect to Web3 computing networks to hedge against the risk of centralized cloud services being unavailable. Simultaneously, utilizing blockchain technology to verify the ownership of AI-generated digital assets (such as design drawings, code, and audio/video) will provide an irreplaceable first-mover advantage when facing complex AI copyright compliance reviews in the future.

Conclusion

The White House's "National Artificial Intelligence Policy Framework," released on March 20, appears to be an industry regulatory framework, but in essence, it's a "territorial demarcation agreement" on the eve of humanity's march towards a silicon-based civilization. It erects high walls of compliance and computing power, heralding the end of the AI idyllic era. But beneath these walls, new resistance and reconstruction will inevitably emerge. In this era where computing power equals power, future winners will no longer be merely those with the best algorithms, but rather those ecosystem disruptors who can find alternatives to computing power within geographically isolated cracks and reconstruct business loops within the framework of data compliance.

Source cited:

- The White House. (2026). National Artificial Intelligence Policy Framework . Executive Office of the President of the United States.

- Semiconductor Industry Association (SIA). (2026). Global AI Chip Trade and Export Control Impact Assessment 2025-2026 .

- Stanford Institute for Human-Centered Artificial Intelligence (HAI). (2026). Artificial Intelligence Index Report 2026: Costs and Compliance in Foundation Models .

- Messari. (2026). State of DePIN: Decentralized Compute Networks and the AI Convergence .