~$1.2B in non-USD stablecoins vs ~$300B USD stables made me realize crypto liquidity is just dollarized.

at first, I thought stablecoin dominance was just a scale thing. Like USD got there first, liquidity compounds, others will catch up later.

But after digging into how the flows actually behave, I don’t think it’s that simple. Here’s how I frame it:

1/ The data looks small, but the signal is loud

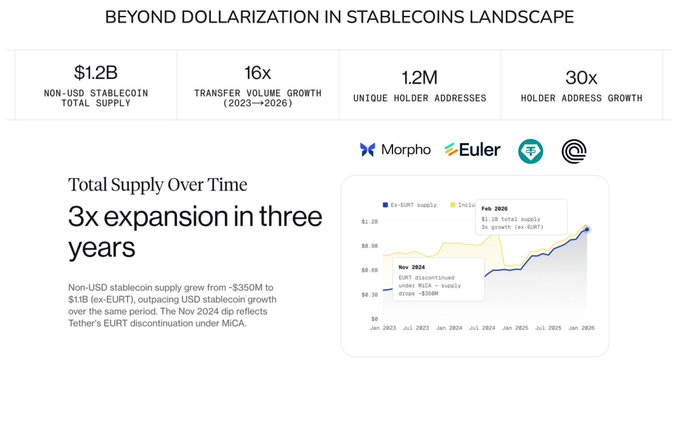

- Total stablecoins: ~$315B vs Non-USD: ~$1.2B (~0.4%).

- Transfer growth: +16x since 2023 an Users: +30x.

So yeah, size is tiny but adoption curve is not.

2/ Liquidity is about usage

- ~80% of non-USD flows = payments, payroll, settlement.

- Only ~29% lending, ~17% DEX, ~14% CEX.

Compare that to USD stables and I realized it’s heavily financialized, looping in DeFi and collateral for leverage.

If I’m being honest, most USD liquidity is still inside the system, non-USD liquidity is already touching the real world.

3/ Not all stablecoin liquidity is the same

There are 2 completely different liquidity systems forming:

(1) USD liquidity - global, financialized.

Dominant in DeFi, RWAs, collateral, backed by T-bills → deeply tied to TradFi.

Extremely efficient, but centralized around a few issuers.

This is where players like @tether | $USDT and @circle | $USDC completely own the game.

(2) Local currency liquidity - regional, transactional

This is used for payments, FX, settlement, plugged into local rails, kinda less liquid, but more economically real.

Some references I’m watching:

- $EUR → dominating DeFi lending within Aave, Morpho.

- $BRL → integrated with PIX.

- $SGD / $JPY → cross-border settlement in Asia.

It’s finance entering crypto rails elsewhere, outside of crypto and outside of dollarizarion.

Top protocols I’m watching right now:

→ @SkyEcosystem | $SKY - USDS & DAI combined ~$13-16B (USDS ~$8-11B + DAI ~$4.5B). Endgame rollout emphasizes RWA integration.

→ @ethena | $ENA - USDe ~$5.9B. Integrates with DeFi for "cash-and-carry" yields.

→ @PayPal - PYUSD ~$4B, enterprise payments focus.

→ @fraxfinance - FRAX/USDF, Algorithmic/hybrid models.

→ White-label infrastructure: Bridge (Stripe), @brale_xyz , @m0 , @Paxos - enable enterprises to launch custom stables quickly.

4/ Where liquidity infra is actually being won

There are 3 layers that matter:

→ Issuance = still dominated by USDT / USDC, but local issuers will win regionally (regulation + banking access).

→ Liquidity sinks in money markets such as Aave, Morpho, etc. whoever captures deposits → controls idle liquidity.

→ Payment + settlement rails where real volume is forming, integrations > incentives

5/ My takeaway

USD stablecoins won phase 1 → store of value + DeFi collateral.

Non-USD stablecoins are playing phase 2 → real payments + local settlement.

If that continues, liquidity will fragment across currencies, regions, and rails.

I do think we’re moving from one global liquidity pool → to many localized liquidity zones connected onchain.

And honestly, that system is way harder to build but also much closer to how real economies actually work.

DYOR.

v interesting take

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content