Investors tried to pull $13 billion out of private credit funds this quarter. They got less than half. For many crypto investors, if the collapse of private credit continues, half could end up being a good outcome.

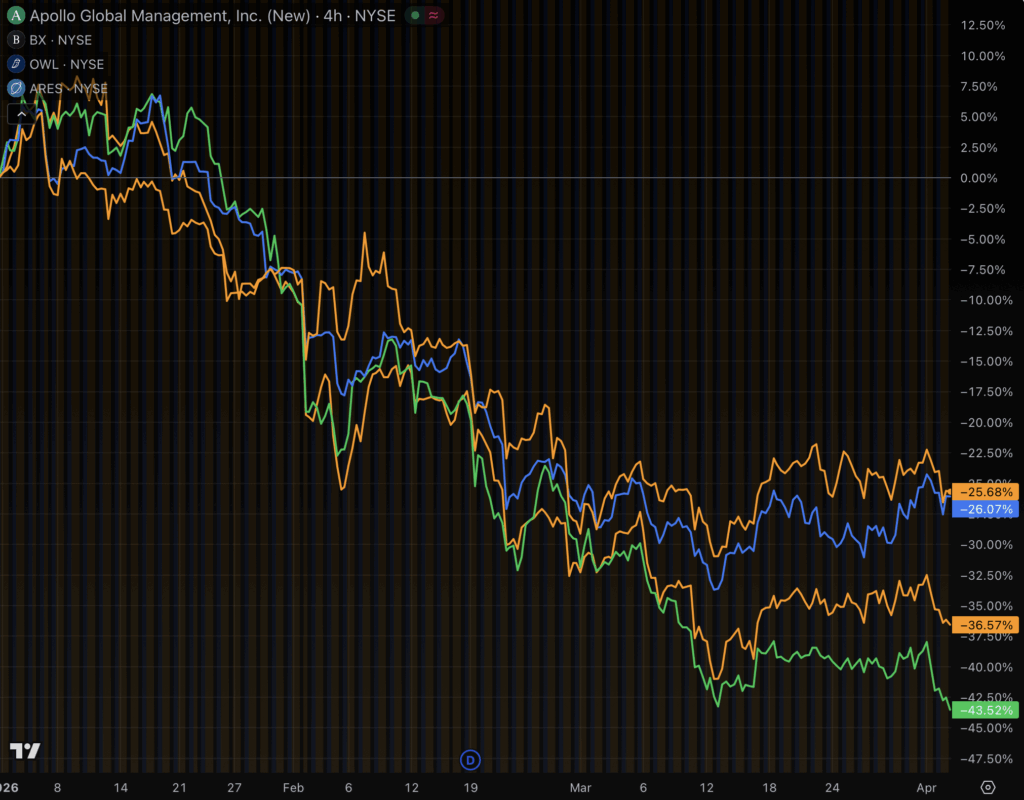

Seven private credit giants capped investor withdrawals this quarter, including Morgan Stanley, BlackRock, Apollo, Blue Owl, Cliffwater, Blackstone, and Ares. Oaktree almost joined that group, although it technically fulfilled its 8.5% in withdrawal requests by having parent Brookfield buy 1.7% of shares at the eleventh hour.

Private credit funds package up illiquid loans inside vehicles that typically go up, except during rare times of crisis, such as during a major war or mass job losses.

They also typically limit quarterly withdrawals to 5%, which is not a problem until many people want out, like they do now.

When more than 5% want to withdraw, everyone gets a haircut on their withdrawal request. At Apollo and Ares, 11% wanted out. Those funds returned less than half.

Crypto started joining the private credit bandwagon years ago, selling similar products in a different wrapper. Many stablecoin and altcoin treasury managers invest in private credit directly.

‘A quasi run on the bank’

Michael Saylor delivered a keynote at the Blockworks Digital Asset Summit on March 26, the same week Apollo and Ares gated withdrawals. He pitched his company’s dividend-paying stocks as competitors to private credit.

Saylor even called the multi-trillion dollar private credit crisis this year “a quasi-run on the bank.”

Worse, the same companies gating traditional private credit withdrawals are tokenizing private credit on blockchains. Apollo launched ACRED, a tokenized feeder into Apollo’s Diversified Credit Fund. A few months after that launch, Apollo’s partner Securitize had built sACRED, a derivative to goose yields even higher through risky decentralized finance (DeFi) protocols.

Holders can buy ACRED, deposit it into DeFi vaults, borrow stablecoins, buy more ACRED, and loop. Yields after looping, which are tantamount to risk, soared.

Securitize initially advertised daily redemption rights for ACRED holders, which was quite curious given that most private credit funds limit quarterly redemptions to 5%. Then, after crypto publication Unchained asked about the mismatch with the fund’s quarterly 5% cap, Securitize quietly removed daily liquidity rights.

Easier to buy, just as hard to sell

In other words, crypto tokenization changed the speed at which people could buy and add leverage. It did not change the speed at which they could sell.

Nor did crypto improve the most important characteristic of private credit: the deteriorating credit qualities of US borrowers who are suffering higher fuel prices, AI-induced job layoffs, wartime uncertainty, inflation, and rising costs of living.

Crypto sold versions of the same illiquid debt that investors cannot exit quickly in any environment, let alone the current “quasi run on the bank” reality.

By one analyst’s count, tokenized private credit surged from $25 million to $6 billion over the last year.

Private credit firms prepare for bank run-type panic by gating investor withdrawals