The VN-Index reversed course and rose nearly 9 points after a period of volatility, thanks to the pull from the real estate sector, especially VIC and VHM, even though the market remained "green on the outside, red underneath".

The trading session on April 13th saw strong fluctuations, with a prolonged period of divergence before improved buying pressure towards the end of the session helped the main index reverse and rise.

At the opening of the session, the market moved cautiously with a fairly balanced number of rising and falling stocks. Pressure from large-cap Capital ... VN-Index It remained below reference for most of the morning.

Despite some recovery phases, overall demand remained weak, while sellers maintained a wait-and-see attitude, preventing the index from breaking through. At the end of the morning session, the VN-Index fell 8.06 points to 1,741.94 points; liquidation reached over 10,695 billion VND.

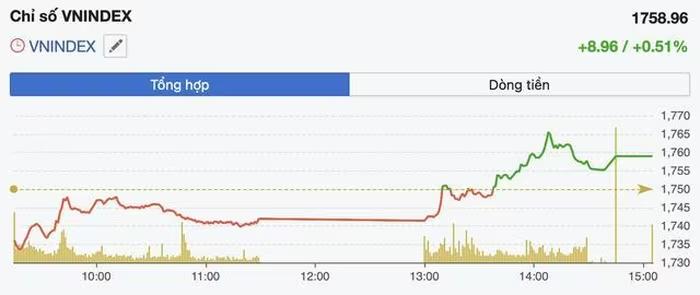

VN-Index performance during the April 13th trading session.

VN-Index performance during the April 13th trading session.

In the afternoon session, a positive trend gradually became clearer from around 2 PM onwards, as capital flowed back in, helping the index regain its reference level and surge. At one point, the VN-Index rose by more than 15 points, surpassing the 1,765 point mark before narrowing its gains towards the end of the session.

At closing, the VN-Index stood at 1,758.96 points, up 8.96 points (0.51%), while the VN30-Index still fell slightly by 0.13% to 1,925.66 points.

Notably, the market continued to exhibit a "green on the outside, red on the inside" pattern, with the index rising but breadth leaning towards declines. On the entire HOSE exchange, 171 stocks fell compared to 137 that rose; within the VN30 basket alone, the number of declining stocks overwhelmingly outnumbered rising stocks with 21, three times the number of rising stocks.

Looking at the sectors, red dominated in many areas such as finance, technology, consumer goods, and basic materials.

Specifically, the financial sector declined by 0.68%, with the largest trading value in the market, reaching over 8,700 billion VND. Conversely, real estate and energy were the two prominent gainers, increasing by 3.02% and 1.10% respectively, indicating a clear selective flow of capital.

The real estate sector played a leading Vai in the session, with many stocks experiencing positive price increases. In particular, stocks within the ecosystem performed well. Vingroup They all increased sharply.

In there, VIC Rising by 5.47%, VHM contributed the most to the VN-Index with 12.77 points; VHM also provided significant support with a contribution of approximately 1.6 points. The accelerated performance of these two stocks in the afternoon session was the main factor driving the overall index upwards.

In addition, some individual stocks such as BSR, GEX, VIB, NVL, CII , STB, and HCM also contributed to supporting the market. CII attracted attention with its surge to the ceiling liquidation and high trading volume, while many mid- and small Capital stocks recorded gains of over 2-3%, indicating a tendency for capital to seek opportunities in this group.

Conversely, the banking sector exerted significant pressure on the index as many large-cap stocks declined. Stocks such as VCB, BID, TCB, MBB, CTG, VPB, and SHB were among the most negatively impacted, with VCB alone deducting more than 1 point from the VN-Index.

Nevertheless, thanks to the upward momentum from blue-chip stocks, especially the real estate sector, the VN-Index maintained its gains until the end of the session. Market liquidation remained high, with trading value on the HOSE reaching over 22,500 billion VND.

One negative aspect of the session was the continued net selling by foreign investors, amounting to approximately 123 billion VND, which partly reflects the cautious sentiment of foreign Capital flows.