Original author: Long Yue

Original source: Wall Street News

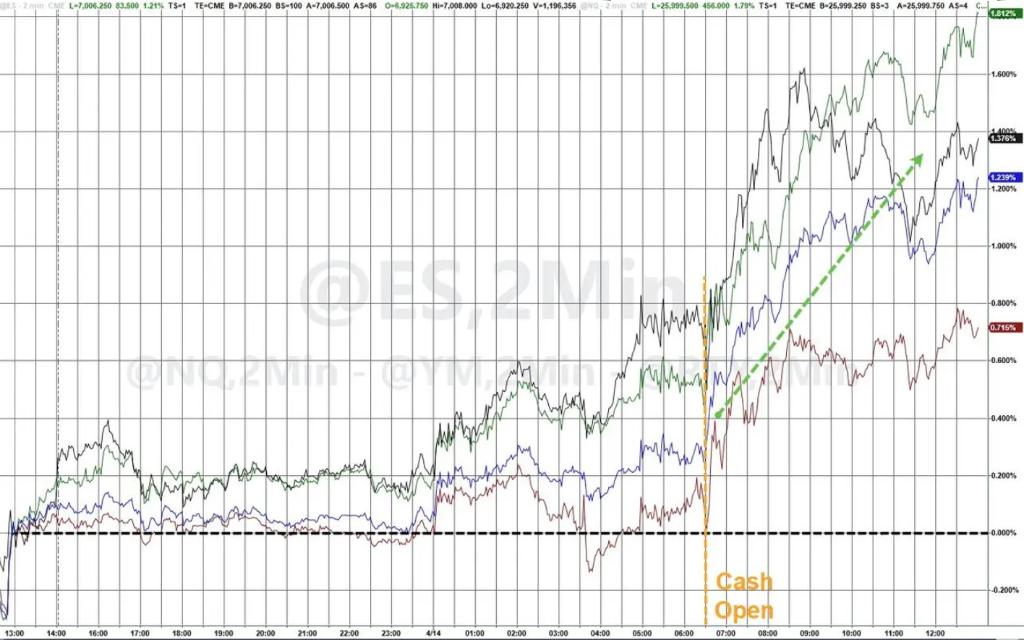

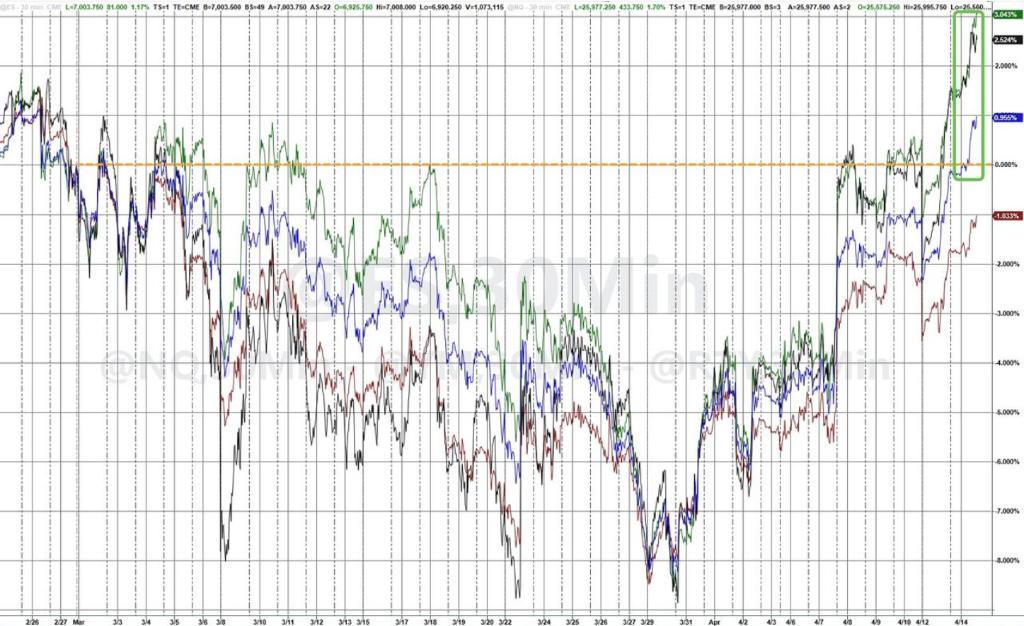

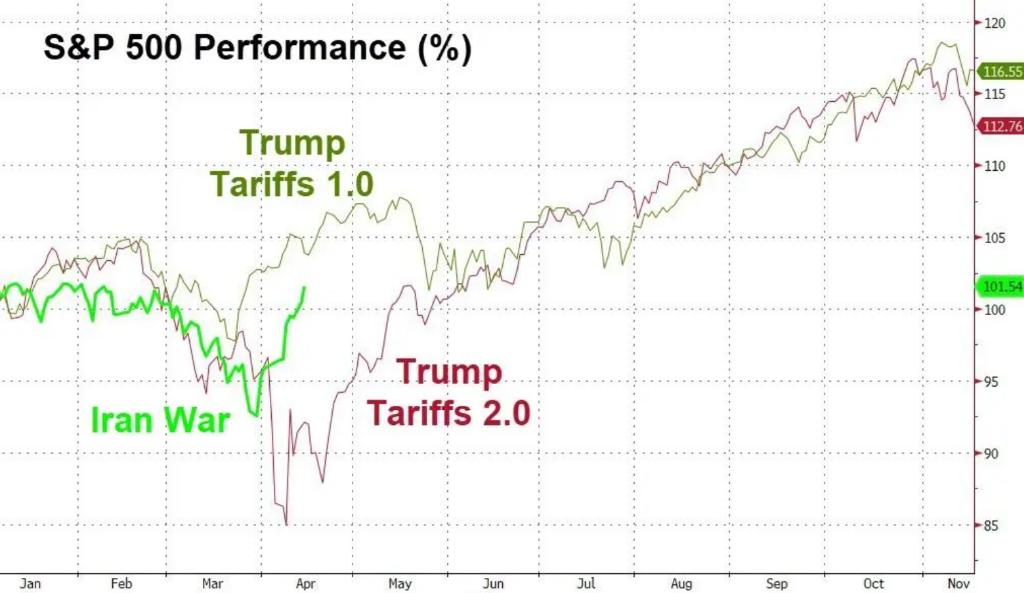

More than a month after the outbreak of the Middle East conflict, US stocks have rebounded.

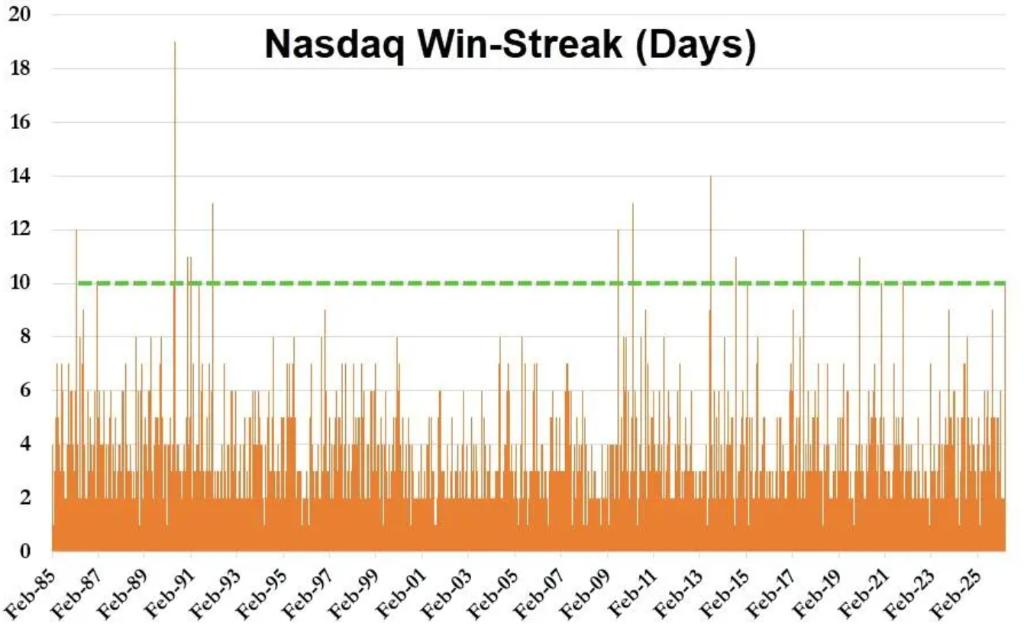

For some time now, Wall Street has been selectively "blocking out the noise." The S&P 500 has risen nearly 10% since March 27, while the Nasdaq 100 has gained about 12% over the same period, marking its 10th consecutive day of gains—its longest winning streak since 2021.

More importantly, the S&P 500 has completely erased all its losses since the Iran war in Monday's trading.

"The market has declared victory."

Rich Privorotky, head of Goldman Sachs' Delta One trading desk, noted: "The market seems to have declared itself the winner of the 'war' with Iran, even though the conflict itself is not really over yet."

While some believe Iran is simply waiting for the right moment, Privorotky is surprised by Iran's current response: "The Houthis have not escalated any actions in the Red Sea region, drone attacks have not increased, and the ceasefire agreement has not been broken." He believes it may be too early to declare victory, but the stock market clearly already considers the situation to have stabilized.

Goldman Sachs strategist Chris Hussey stated bluntly: " More than a month has passed since the outbreak of the Iran war, and incredibly, the S&P 500 has risen 1.6% year-to-date, which was unthinkable just last week. Despite the many ups and downs on the road to eventual peace, equities are forward-looking instruments, and as we've written before, markets cannot afford to wait for a problem they know will eventually be resolved —this dynamic explains today's market behavior and the reason for the renewed strong performance."

The market's logic is shifting. Doug Peta, chief U.S. investment strategist at BCA Research, stated, "The stock market, and indeed the entire financial market, seems less concerned about the situation in the Strait of Hormuz."

Overnight, leading companies in the field of artificial intelligence are also emerging in the market. Mag 7 continued its strong performance, rising 3%, and has accumulated a 15% increase over the past 10 trading days (rising in 9 out of 10 trading days).

The chip sector has been a major driver of this rebound. Bloomberg data shows that earnings expectations for the chip sector jumped by about 10% in three trading days, significantly boosting overall S&P 500 EPS forecasts. Goldman Sachs data shows that Nvidia and Micron are expected to contribute more than 50% of the S&P 500's EPS growth this quarter.

This rebound is not just a story about stocks.

U.S. Treasury yields fell along with declining oil prices, declining by about 3 to 4 basis points across the board. Bitcoin broke through $76,000, reaching a new high since the outbreak of the conflict. Gold traded above $4,800, its highest level since March 18. The U.S. dollar continued to weaken, almost erasing all gains since the start of the war.

Market liquidity is also returning to normal. Goldman Sachs data shows that top-of-book liquidity for S&P 500 stocks has rebounded to $13.16 million from approximately $3.5 million at the peak of geopolitical uncertainty, a 141% increase from the 20-day average. ETF trading volume as a percentage of total market trading volume has also fallen from its peak of approximately 50% to 29%.

An interesting phenomenon is that Trump's "familiar script" seems to be playing out again...

Funds "one-way chasing the rise," forcing short sellers to cover their positions.

Regarding this strong rebound in US stocks, a veteran stock trader said, "The flow of funds is one-way... CTAs and clients, everyone is underweight and now they're chasing the rally."

Behind this "panic buying" are multiple forces at play:

Institutional investors are driving the rebound. Nationwide's chief market strategist, Mark Hackett, points out that after the previous massive sell-off, institutional attention has shifted back to fundamentals, and the fundamental data is supportive.

CTA funds were buying heavily, but long-term funds and hedge funds were selling. According to Goldman Sachs trading desk data, long-term funds (LO) were net sellers with a slight net outflow, while hedge funds (HF) were net sellers with a net outflow of 3%, mainly reducing their holdings in the information technology, industrial, and communications services sectors—they were "taking over" the CTA buying.

Short covering accelerated. Goldman Sachs' rolling short basket saw three sharp rallies, with unprofitable tech stocks surging and the most short stocks experiencing a short squeeze.

Goldman Sachs attributed the continued strength of the "Mag 7" to four factors: improved geopolitical environment leading to the replenishment of index hedging positions (Mag 7 accounts for about 33% of the S&P 500 weighting), the easing of money laundering since Q1, market positioning for strong earnings season expectations, and continued stock buyback programs.

Earnings season takes over, fundamentals are repriced.

The shift in market narrative is supported by data.

This week, major financial institutions such as JPMorgan Chase, Citigroup, Wells Fargo, and BlackRock released their first-quarter earnings reports. Goldman Sachs' Chris Hussey pointed out that the banking sector is often seen as a barometer of the overall health of the U.S. economy, "This morning's earnings reports show that despite market concerns about inflation, AI, private credit, and consumer spending, households and businesses remain robust."

Inflation data also provided support. The PPI rose 0.5% month-on-month in March, lower than expected. However, Blake Gwinn, interest rate strategist at RBC Capital Markets, cautioned that "the market is increasingly interpreting PPI data through the lens of PCE transmission" and tends to "view weak data as a lagging indicator, suggesting that inflationary pressures are still on the way."

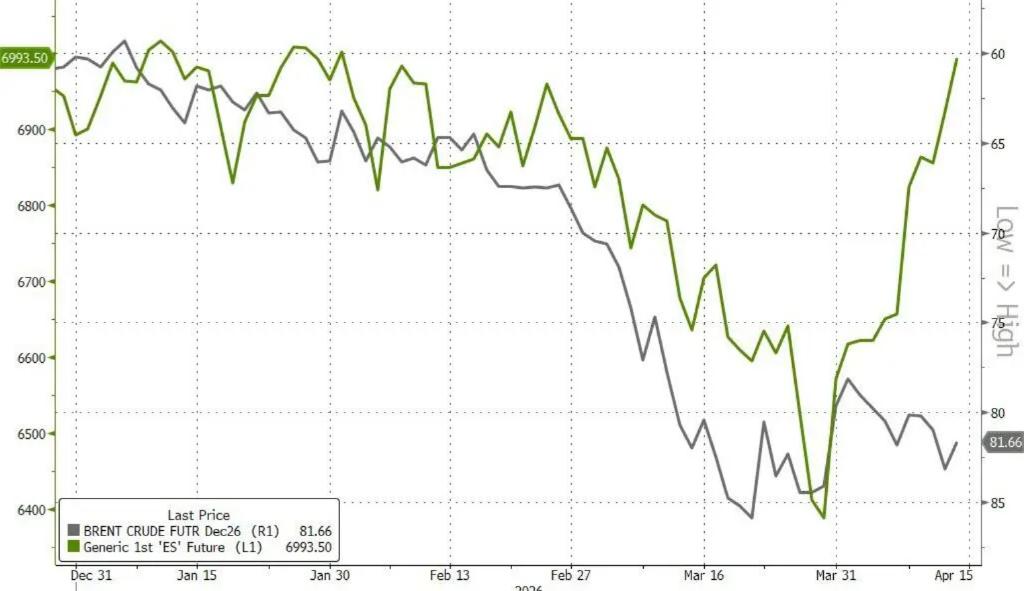

Stocks are looking ahead, while the oil market is still waiting.

It is worth noting that a clear divergence has emerged between the stock market and the oil market.

WTI crude oil futures fell below the $91 mark on the day, and Polymarket data shows that the probability of WTI falling below $90 by the end of the month is rapidly increasing. The direct triggers for the price drop were reports that Iran is considering suspending some oil exports to advance negotiations, and that the US and Iran are discussing a second round of peace talks.

Market data—the crude oil forward curve (represented by December Brent futures)—shows that the crude oil market believes the resolution of supply disruptions will take longer—a contrast to the stock market's "mission accomplished" optimism.

Goldman Sachs' Chris Hussey explained, "Equities are forward-looking instruments, and markets cannot afford to wait for a problem they know will eventually be solved—this dynamic explains today's market behavior and the reasons for regaining superior performance."

Risks remain after the rebound.

Despite a significant improvement in market sentiment, many strategists remain cautious about the market outlook.

Lori Calvasina of RBC Capital Markets warned that the uncertainty surrounding the war and its ripple effects still keep the risk of a "growth panic sell-off" high. In a client note on Sunday, she wrote, "If the fundamental narrative surrounding the war or its impact changes, from a valuation perspective, there is still room for the stock market to fall further, and possibly even deeper."

Nationwide's Hackett, however, is skeptical about whether the S&P 500 can break its all-time high: "I doubt we can truly break through the all-time high until there is substantial progress in the negotiations. But once that day comes, conservative positions, strong fundamentals, and reset expectations will create a long-compressed spring-like force."

Bond investors also remain skeptical of news of improving inflation. Raghav Datla, global market rates strategist at Citigroup, said, "It's difficult to see lower inflation data in future reports, and nobody can accurately predict what the number will be."

Veteran strategist Ed Yardeni is more optimistic. In his investor report on Sunday, he stated that, similar to the Russia-Ukraine conflict, financial markets are learning to coexist with a war with Iran, and he maintains his assessment that the S&P 500 bottomed out on March 30.