Prediction markets Polymarket and Kalshi recently announced the launch of perpetual futures, while cryptocurrency exchange Hyperliquid is entering the prediction market through event contracts. Perpetual contract trading volume is seven times that of spot trading, generating nearly $1 billion in annual revenue. However, prediction markets suffer from insufficient user stickiness; only 8%-11% of users are still trading after a year, and approximately 75% churn within 90 days. Operating perpetual contracts requires a complex technology stack including highly liquid order books, risk engines, and funding rate mechanisms. Hyperliquid has already completed stress tests using real-world events. Prediction market platforms lack cross-margin systems, making it difficult to hedge risks between different asset classes, and users are mostly retail investors unfamiliar with cryptocurrencies. Institutional partnerships may be a breakthrough, but building stress-tested infrastructure is essential.

Article author and source: Prathik Desai (translated by Block unicorn)

Over the past year, we've spent considerable time covering perpetual futures trading platforms. Their rapid rise is undeniable. Perpetual futures allow participants to price events shortly after they occur, offering high leverage and ample liquidity around the clock. This service was never offered by existing exchanges due to time and day restrictions. An 11-member team has built Hyperliquid into one of the fastest-growing cryptocurrency exchanges, with annual revenue approaching $1 billion, thanks to this 24/7 trading philosophy.

Throughout 2025, perpetual contract trading volume averaged seven times that of spot trading volume. This seemed like a reliable path to building a sustainable business. And so, inevitably, others followed suit.

Last week, two major prediction markets, Polymarket and Kalshi, announced the launch of perpetual futures and cryptocurrency trading within hours of each other. Just a few months earlier, Hyperliquid also announced the launch of event contracts. The convergence of perpetual contracts and prediction market platforms seems like a natural progression. Everyone wants to be an all-encompassing exchange, offering a one-stop shop that integrates attention, capital, and leverage.

Three weeks ago, Saurabh wrote in a report on X that Hyperliquid's foray into prediction markets would help the exchange dominate the financial sector. But does the reverse hold true? Will Polymarket and Kalshi's moves yield similar returns?

Why perpetual contracts are important for prediction markets

Prediction markets suffer from stickiness. They are typically cyclical, with trading volumes reaching record highs when there are major events to bet on, as we see during US presidential elections, the Super Bowl season, or Federal Reserve Open Market Committee meetings.

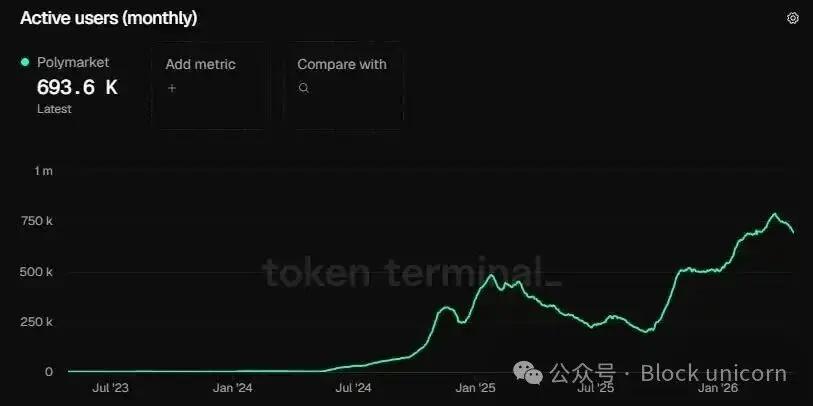

Polymarket's monthly active users peaked at 321,500 during the US presidential election in November 2024. Three weeks later, that number dropped by 25% to 245,000.

However, the number of users fluctuates every month due to seasonal factors.

In January 2025, Polymarket's user base peaked at 500,000, before falling below 200,000 in September. This reflects Polymarket's user retention rate.

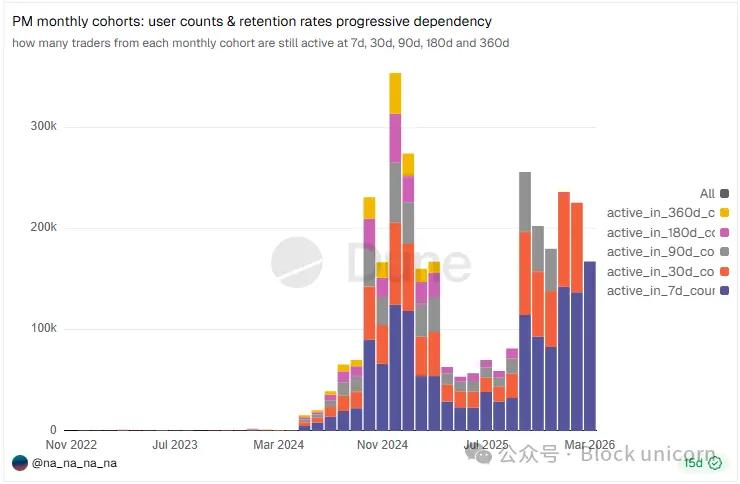

Dune's user base data shows that since 2024, only 8% to 11% of its monthly user base have remained active in trading a year after joining. Approximately 75% of users churn within 90 days. Users may return to participate in events, but this doesn't necessarily translate to a sense of loyalty to the platform.

But that's only part of the problem.

Prediction markets also freeze funds until the issue is resolved. Perpetual contracts, on the other hand, update event prices every second, thus attracting attention for extended periods and building sustained user engagement. This is also more advantageous for prediction markets, as traders have higher trading volumes and generate higher transaction fees.

By 2025, the notional trading volume of malicious traders will exceed $60 trillion, while the notional trading volume of precious metals traders will be $28 billion.

Therefore, this expansion into adjacent sectors of prediction markets (PMs) is a natural evolution. Platforms that cater to certain speculative needs often expand their business into other areas. They either develop the relevant functionality themselves or acquire other platforms that offer that functionality. We have witnessed this many times: Robinhood expanded from the stock market to the options market, the cryptocurrency market, and finally into prediction markets (PMs). Coinbase acquired Deribit for a record $2.9 billion, entering the derivatives trading space. Binance also expanded from offering spot trading to futures trading, eventually creating its own native blockchain.

We often see this in traditional sectors. A company expands its services, hoping to cross-sell new products to the same group of customers. This serves two purposes: first, to increase average revenue per user (ARPU), and second, to diversify its reliance on multiple revenue streams, thereby enhancing the company's resilience to market cycle fluctuations.

In the early 1970s, commodity futures revenue at the Chicago Board of Trade (CBOT) was declining. So, they used a former 4,000-square-foot smoking lounge at their parent company, the CBOT, to create the Chicago Board Options Exchange (now known as Cboe). Because both required shared infrastructure, they were able to operate synergistically: risk management, clearing, and a network of professionals knowledgeable in derivatives pricing.

However, there is a huge gap between wanting to operate a perpetual contract trading platform and actually having the ability to put it into practice.

Perpetual stacking

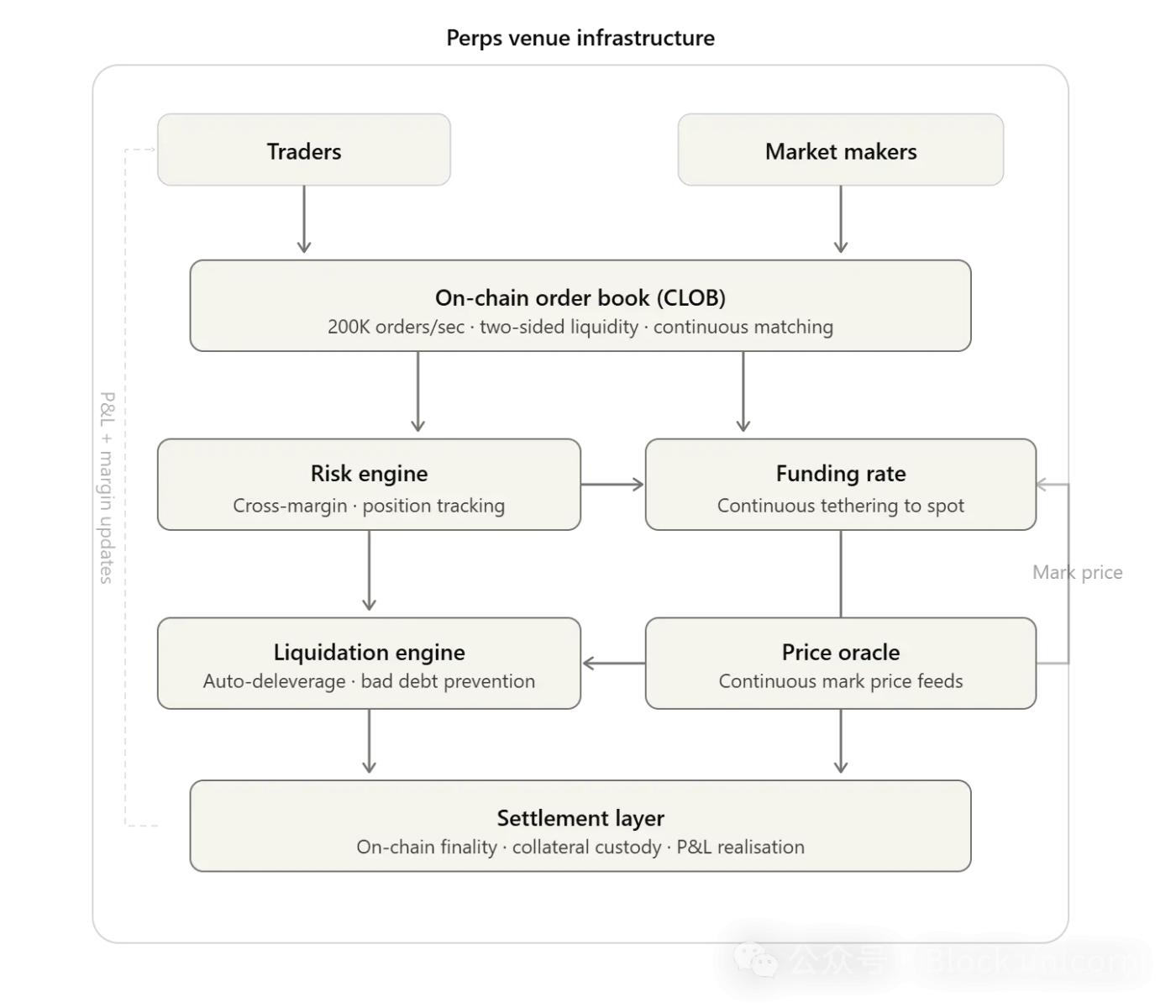

Operating a perpetual trading platform involves too many aspects. Let's start with liquidity.

The Hyperliquid platform processes over 200,000 orders per second using a fully on-chain order book. This exchange settles over $6-7 billion in transactions daily and operates on a two-sided market-making model. Insufficient liquidity can lead to extreme volatility, excessively wide bid-ask spreads, and high slippage, making it easier for whale to manipulate prices.

Secondly, there's the risk engine—the core of any derivatives platform. It tracks every transaction and checks the margin requirements for each order. In October 2025, the cryptocurrency market lost $19 billion, and the Hyperliquid platform processed billions of dollars in liquidations without interrupting service.

In addition, there is a funding rate mechanism that links traders' prices to the spot price of the underlying asset. This mechanism operates continuously by settling small amounts between long and short positions every few hours.

Building the entire technology stack isn't the main problem; I believe market prediction can handle that. The bigger problem lies in stress testing this technology stack.

Hyperliquid built all of these systems and stress-tested them in real-world scenarios, such as a 10/10 cryptocurrency liquidation event and the Iraq War. Afterward, with the entire system ready, it launched event contracts via HIP-4. Kalshi and Polymarket, on the other hand, are trying to do the opposite. They operate successful prediction markets that don't require any of the aforementioned systems. Now, they are not only competing with the highly successful Hyperliquid, but also with a system that hasn't been stress-tested and can't handle the high-frequency activity of perpetual trading, thus vying for market share.

For prediction markets, there are many headwinds that make it more difficult to expand toward perpetuality than the other way around.

Hedging Synergy

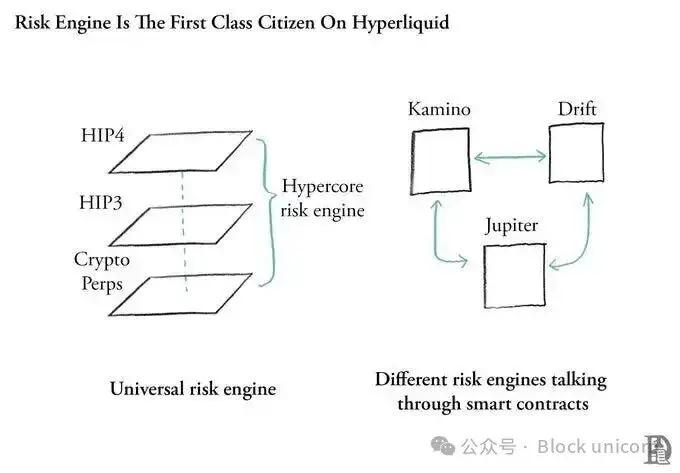

On the Hyperliquid platform, the Risk Engine monitors all your positions across all trading instruments, spot markets, and upcoming event contracts. Saurabh explained this in his HIP-4 report.

It will examine all your positions indiscriminately. Ultimately, the leverage you use and the margin you hold as cross-collateral determine when you will be forced to liquidate. The combination of your positions in spot, futures, prediction markets, or any other market determines how much margin you need to hold.

But aren't other blockchains like Saurabh, Ethereum, or Solana also composable? Absolutely. On a universal chain, each application runs its own risk engine within its own smart contract. They cannot atomically see each other's state. Therefore, Kamino cannot know what's happening on Pacifica. Aave cannot know what's happening on Lighter. All applications are smart contracts on their own chains. Each application or smart contract has an independent risk engine, and making them aware of each other—that is, creating a universal risk engine—requires massive collaboration.

This universal risk engine solves a core funding problem by optimizing the same amount of money used by traders in multiple trades across trading venues.

Imagine a trader on the Hyperliquid platform who is long ETH with 5x leverage. Worried about the Federal Reserve's interest rate decision next week, she buys a "Fed Keeps Rates Unchanged" outcome contract at $0.65. Because both positions use the same risk engine, they are held in the same margin account. If the Fed unexpectedly cuts rates, the price of ETH rises, her long position profits, and the outcome contract loses only her initial investment. If the Fed keeps rates unchanged, the outcome contract pays out the gains, partially offsetting the loss on long position.

This is why prediction market platforms or hedging trading venues cannot simply be additional features. This hedging capability is precisely where the value of HIP-4 lies on the Hyperliquid platform. Ordinary traders on the platform view prediction markets as a form of insurance in case their existing hedging positions reverse.

Currently, collateral on the Polymarket and Kalshi platforms will be locked until the events are resolved. Therefore, unless they provide a unified risk engine across their real-money and prediction market trading venues, they will lose a key factor in keeping traders on the platforms. Neither platform has yet announced a cross-margin system between its prediction market and real-money trading venues.

The segmentation of prediction markets and the profile of average traders have further fueled concerns about whether they can replicate their success in real-money trading.

Over 80% of Kalshi's total monthly trading volume comes from sports betting. Polymarket's figure is projected to exceed 40% by 2025. So, how can a sustainable pricing mechanism be built around these sporting events for paid trading platforms? This would prevent a significant portion of traders from participating in paid trading.

Furthermore, Kalshi's typical traders are retail investors with no prior cryptocurrency experience, who fund their prediction market accounts via ACH transfers from their bank accounts. Therefore, even assuming the possibility of cross-margining theoretically exists on the Kalshi platform, I doubt whether these traders possess the expertise required to double down on their investments and utilize perpetual contracts as a hedging strategy.

What methods might be effective for predicting markets?

If Kalshi and Polymarket announce cross-margining, I believe there's one scenario where these bets would work: their institutional relationships with major brokers and clearing houses could facilitate high-value, high-frequency trading activity in event contracts and perpetual futures.

This will enable institutional trading departments to view market prediction as part of a broader risk management toolkit.

Both Kalshi and Polymarket have partnerships that allow them to reach institutional clients.

Kalshi's collaboration with FIS and Tradeweb data, as well as Polymarket's trading with the Intercontinental Exchange (ICE), may help retain institutional clients who value using perpetual contracts to hedge their forecasting market positions on the same platform.

This remains a distant goal, requiring predictions that numerous market factors will develop in a favorable direction. They need to build stress-tested infrastructure, forge partnerships, and demonstrate to clients that their platform can help optimize capital allocation.

But this is essential for their survival in the fierce competition. With distribution channels already dominated by Hyperliquid, they have no choice but to seek the greatest opportunities elsewhere.

That's all for today. See you in the next article.