Author: Max Wong @max0dte

Introduction

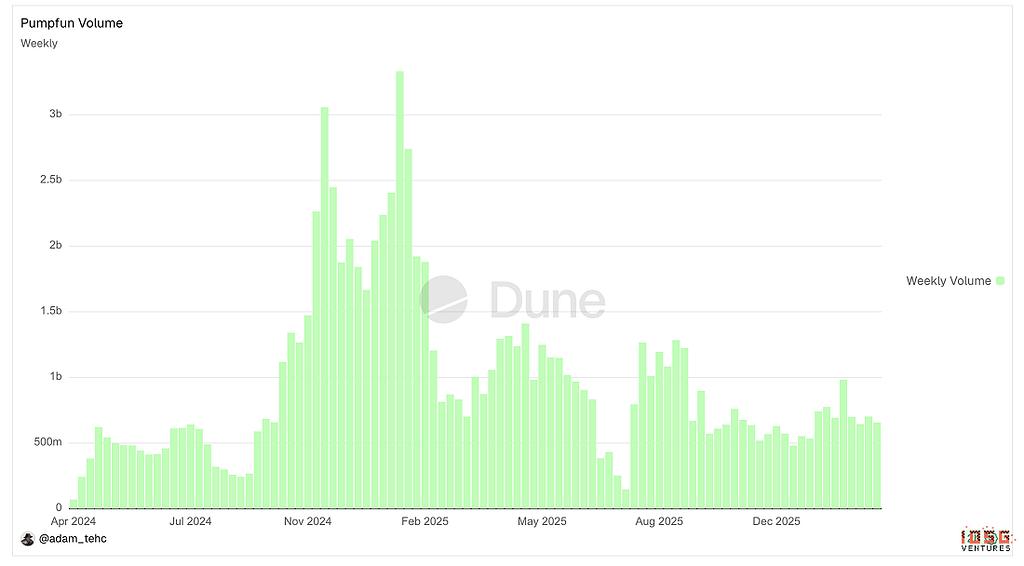

Pump.fun launched in early 2024 as a permissionless meme-coin launchpad on Solana, allowing anyone to create and trade a token in seconds using a bonding curve mechanism. What began as a niche experiment quickly evolved into one of the highest-revenue applications ever deployed on a public blockchain.

Throughout 2024 and 2025, Pump.fun consistently rivaled or exceeded Hyperliquid in daily protocol revenue, a feat made more remarkable by the fact that it operates in the inherently cyclical memecoin market. As a result, there was massive demand for their native token, $PUMP, which launched via a $600mn ICO at $0.004 (implying a $4bnFDV).

Over the past few months, even with record high revenues and 100% value accrual to token, $PUMP currently trades down roughly 80% from its ATH of $0.086 ($8.6bn FDV), at approximately $0.0019, placing its current market cap near $679 mn on a $1.9bn FDV. There clearly is a structural mismatch between price and value.

This report aims to: (1) catalogue Pump.fun’s evolving product suite and ecosystem strategy; (2) stress-test the sustainability of its revenue with a forensic wash-trading analysis; and (3) assess whether the current valuation represents a genuine mispricing or a rational discount for structural risk.

The Product Suite

Pump.fun has evolved well beyond its original launchpad. Since late 2024 it has systematically expanded into adjacent verticals, diversifying its revenue mix and tightening its grip on the onchain speculative trading stack

- Launchpad (Core Product)

The original product and still the brand’s defining feature. Anyone can deploy a token for a nominal fee.

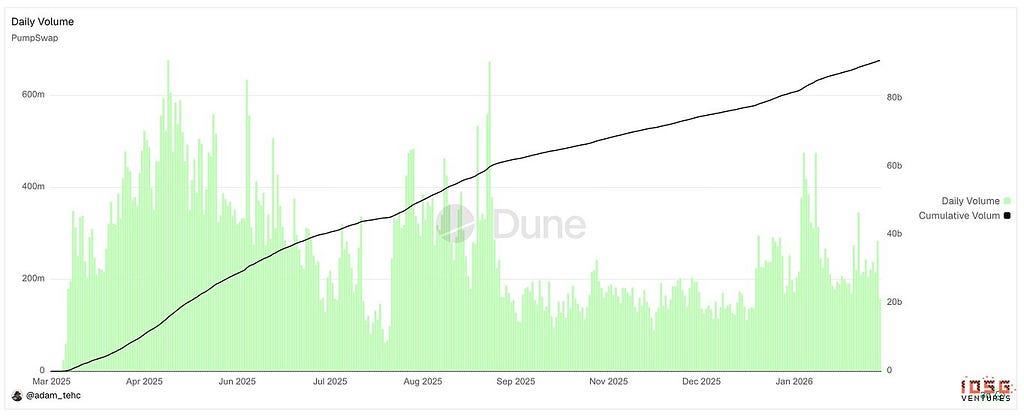

2. Pumpswap

PumpSwap is Pump.fun’s native AMM DEX. It launched in March 2025 to recapture the postgraduation fee revenue that had previously flowed to Raydium (which charged 6 SOL per graduating token). The protocol retains 0.05% of each swap; 0.20% goes to LPs and a further 0.05% to token creators under the May 2025 revenue-sharing updates

- Free creation of custom liquidity pools for any token

- Ability to add liquidity to existing pools

- Trading of all PumpSwap-listed tokens

3. Padre / Pump Terminal

Padre, now rebranded as Terminal following its acquisition by pump.fun, serves as a specialized trading terminal. It currently supports tokens on Solana, BNB, Base and ETH.

Like most terminals, it has advanced toolings and analytics to support traders including but not limited to:

- Trenches feature (check newly migrated tokens, tokens about to migrate etc)

- Customizable features

- Sniping, Instant buy, etc.

- Multiwallet strategies

- Bundle checker

4. Pumplive

Pump live is pump.funs inplatform livestreaming product, where streamers can create a stream whilst simultaneously having a token attached it

The core thesis behind this is the publisher exchange thesis, similar to Parti,. Kick → stake.com etc.; the main value prop is to have streamers and tokenholder incentives align, where streamers want to drive volume to their token as they get a % total volume fees, and tokenholders want greater volume / liquidity / buy pressure

The more they stream, the more active the token, the more volume they generate

Ecosystem Strategy and Initatives

Since their TGE, Pump.fun has been strategically using their ~$1bn cash treasury to as continued to spin out multiple product lines, e.g their acqusition of Padre, and implement initiatives to continue to grow out their ecosystem.

Pumpfund

Pump Fund represents Pump.fun’s strategic pivot toward sustainable ecosystem development, launching a $3 million “Build in Public” (BiP) hackathon on January 19, 2026. The initiative will fund 12 selected projects with $250,000 each at a $10 million valuation, prioritizing market-driven selection based on public traction rather than traditional venture judging.

Glass full foundation

GFF represents Pump.fun’s strategic liquidity injection initiative launched in August 2025 to stabilize and support its ecosystem memecoins. The foundation deployed $1.69–1.7 million (2,022 SOL) across five transparent wallets into 10 selected tokens including Tokabu (21.3%), House (20.6%), USDUC, NEET, MASK, and FART, targeting projects with strong community engagement.

Project ascend

Project Ascend is Pump.fun’s foundational creator incentive program launched in 2025, to introduce a new, sustainable growth model for olatform featuring dynamic, tier-based creator fees (0.95% to 0.05%) designed to increase earnings by 10x. It focuses on long-term sustainability and accelerating Community Takeover (CTO) applications.

Aggregate Metrics (All Products)

The following table consolidates all three reportable product lines. The 2025 actuals reflect a genuinely exceptional revenue year and the 2026E’s shows a stable runrate ahead.

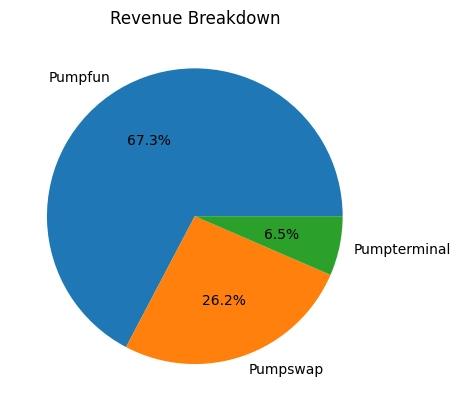

At present, ~32.7% of the platform’s total revenue is being generated from non-launchpad products, clearly signifying early success towards their goal of revenue stream diversification and to seek growth in other areas.

Is Pump.fun Wash Trading?

Clearly, fundamentals on the surface for $PUMP seems extremely strong; however a critical question for any assessment of Pump.fun’s fundamentals is whether its volume numbers reflect genuine economic activity or are artificially inflated by wash trading and bot activity.

- The Volume Correlation Hypothesis

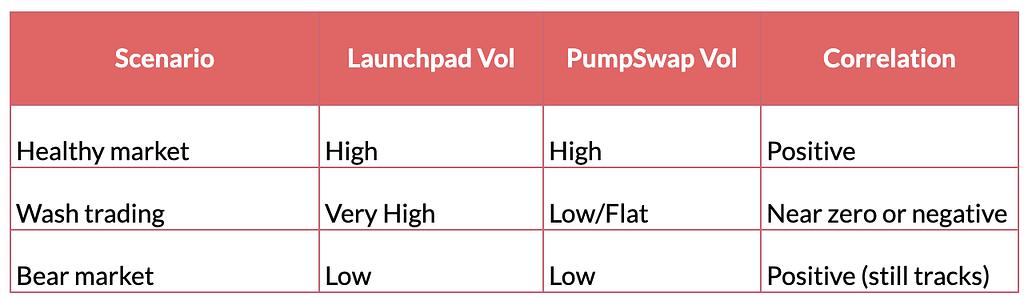

Under organic conditions, launchpad and PumpSwap volume should be moderately positively correlated with a lag. High launchpad activity reflects genuine speculative interest, some of which flows through graduation and sustains post-listing trading. Under heavy wash trading, this relationship inverts. Launchpad volume becomes artificially inflated and decoupled from real demand; tokens graduate based on fabricated bonding curve activity and arrive on PumpSwap with no genuine buyer base behind them. The result is launchpad volume spiking while PumpSwap volume stays flat or declines; correlation collapses toward zero or turns negative.

- In a healthy market, launchpad volume and high PumpSwap volume move together. In a wash-traded market, launchpad volume surges while PumpSwap volume remains suppressed. In a bear market, both fall in tandem and correlation stays positive. The direction of divergence is therefore the signal, not the level of either series in isolation.

- The most telling combination of indicators would be a spike in graduation rate (more tokens artificially hitting the bonding curve threshold), paired with low and rapidly decaying per-token PumpSwap lifetime volume, and average PumpSwap liquidity depth that fails to grow proportionally with the number of graduating tokens.

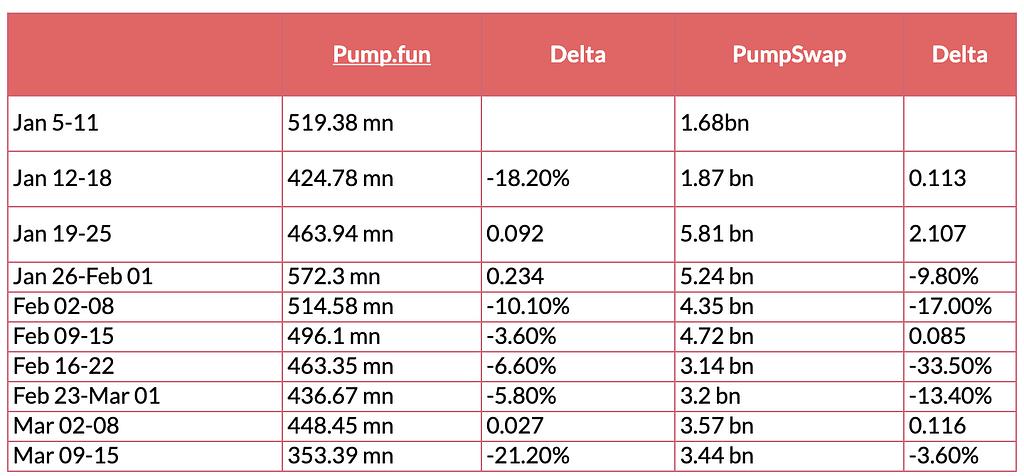

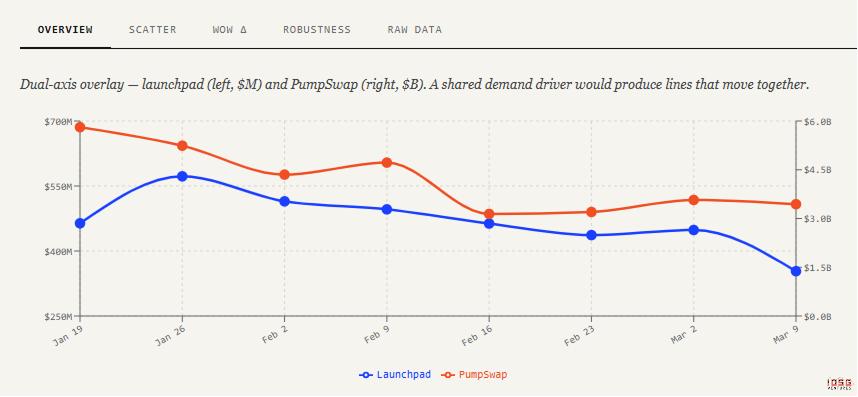

Volume dataset since Jan 2026 until present:

(The first two datapoints — Jan 5–11, Jan 12–18 — were excluded from the correlation analysis due to the implementations of fee and liquidity provider changes to pumpswap, leading to a large outlier spike in volume)

Key Findings

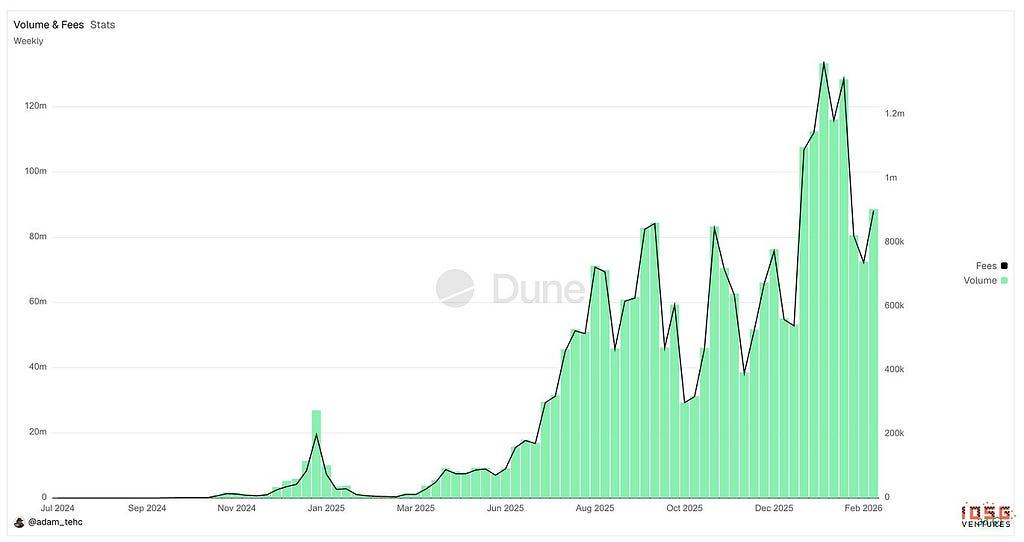

Launchpad vol is quite flat. Over 8 weeks, launchpad volume ranged only ~40% around its mean, from $~400mn to $570mn. That’s the behavior of a volume floor maintenance. This makes sense considering a large amount of bundlers/farmers creating volume for the platform which is entirely different from was trading

PumpSwap is a bit more reactive; during this same period, it ranged ~60% $5.8bn to $3.5bn, driven by increased memecoin trading demand in mid Jan, along with additional pumpswap incentives by the team without any corresponding spike in launchpad volume

r = 0.579, moderate correlation. With n=8, the significance threshold at p=<0.05 would need to be r= ~0.63 but the direction and magnitude are consistent with the organic hypothesis.

2. The University of Pisa Paper

Researchers at the University of Pisa provides the first full on-chain parse of Pump.fun’s launchpad, covering every transaction across 655,770 tokens launched in September–October 2025. Bot-initiated transactions are distinguished from human-initiated trades using Solana transaction log metadata.

Four findings bear directly on the wash trading question.

Large human buys are the dominant graduation predictor

The single strongest predictor of graduation is fast SOL accumulation via a small number of large trades. The median successful graduation required only ~457 bonding curve events and completed in ~4.4 minutes from token creation. This pattern, large, infrequent capital commitments from distinct wallets is consistent with coordinated human speculation (Telegram calls, influencer-driven hype) or serial creator pump-and-dump, not sustained high-frequency wash trading bot volume churn. By contrast, bot-dominated tokens accumulate many small trades and stall before graduation.

and Vice Versa, bot volume actually suppress graduation; the majority of bots are Snipers and Bundlers which also act as a volume floor; but different from wash trading

Tokens with high bot-activity exhibit systematically lower graduation probabilities beyond early bonding curve stages. At the time, graduation requires accumulating ~85 SOL in the curve. If bots were inflating volume toward that threshold, bot-heavy tokens would graduate at higher rates, however, it was found bot activity is actually negatively correlated with graduation. Why? The mechanism is structural: at graduation, the bonding curve transitions from virtual to real AMM reserves, causing a discrete drop in effective liquidity depth. Selling before graduation into virtual-reserve-supported depth is more profitable than selling after.

Further, they found that the top ten token creators in September 2025 each launched over 2,000 tokens within the single month and found statistically anomalous sell sequences by wallet clusters on each of these tokens before the graduation threshold. Bundlers and snipers would front-load positions and dump into retail demand attracted by the curve’s upward momentum

The paper concludes most bots the platform are front-runners that extract value from human counterparties on entry and exit immediately, not volume inflators with an interest in pushing tokens to graduation. Essentially, bots snipe / conquer a large amount of supply, and near graduation, dump on retail participants — distinctly different from wash trading

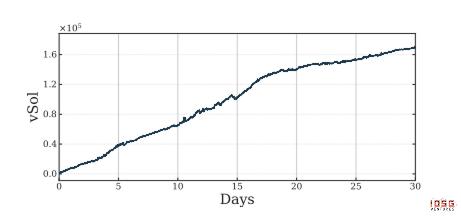

Net SOL flow is strongly and persistently positive; structurally incompatible with was trading

The paper computes net SOL flow — total SOL committed to bonding curves minus total SOL withdrawn via sells — across the full dataset. Cumulative net SOL retained in the ecosystem reached ~160,000 SOL (~$32mn at September 2025 prices) over the single observation month. This is the definitive empirical test for wash trading: circular volume between related wallets leaves net capital flow near zero, as buys and sells cancel. A $32mn

net retention is structurally inconsistent with meaningful circular volume and confirms that real outside retail capital continuously enters the launchpad, loses to the 1.25% fee on every trade, and funds the protocol revenue.

The paper’s findings is similar to the key findings in our volume corrleation analysis: a large volume on the launchpad is generated via pump and dumps by bundlers and snipers, creating a floor, but this is not wash trading. The distinction is material: wash trading generates zero net protocol revenue because fees cancel across related wallets. Pump-and-dump generates real fees on every transaction from genuine retail counterparties who lose capital to the house. The ~$390mn ARR figure is consistent with a platform monetising enormous real retail volume via a pump-and-dump ecosystem, not manufacturing synthetic metrics

Tokenomics

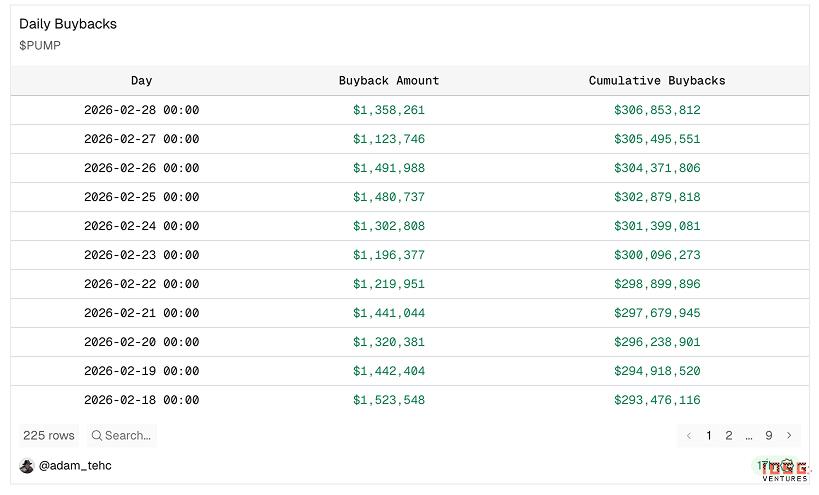

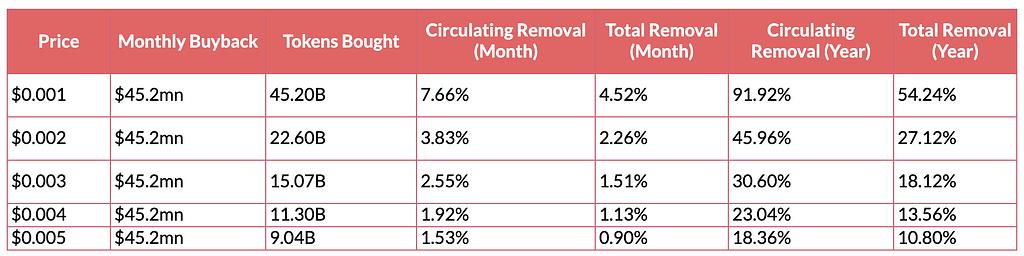

Buybacks

Currently, the Pump foundation uses 100% of revenues from all product lines to buyback

token on the open market. Since announcing their 100% revenue buyback program on July 15th; in 8 months, they have:

- Removed 27% of the circulating supply

- Removed 9.6% of the total supply

For reference, Hyperliquid has only burned 4.1% of total supply or ~12.3% of circulating since starting their buyback program on Nov 2024

At current prices and revenue numbers, they are clearing near ~45% of the circulating supply PER YEAR.

Supply Structure + Unlocks

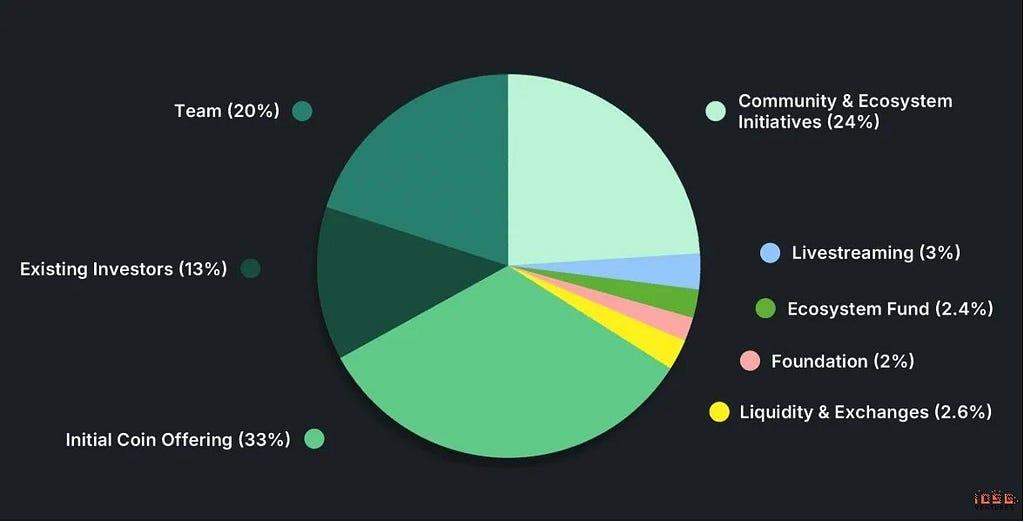

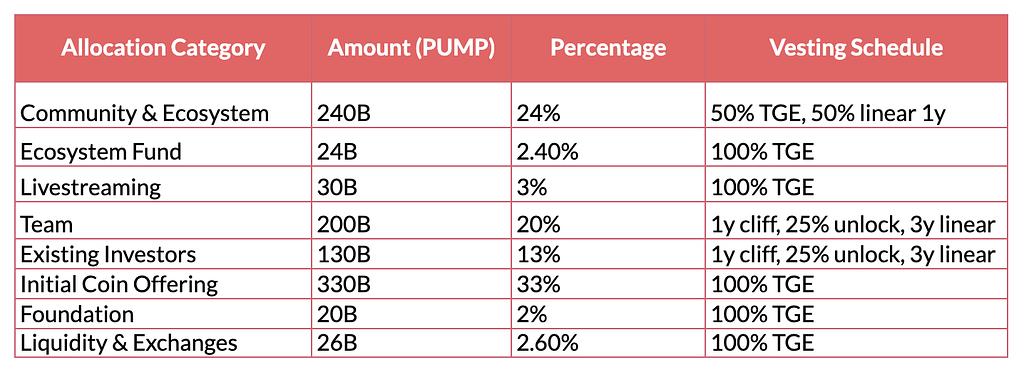

- Total Supply: 1,000,000,000,000 PUMP

- Circulating Supply: 430,000,000,000 (43%)

Remaining Locked: ~58% of supply

Major upcoming unlocks:

- Ongoing — 12% @ 2% monthly for C&E until July

- July 2026–8.25%, then 24.75% @ 0.68% monthly for 36 months

Valuation Reasoning and Analysis

In general, if we believe the washtrading analysis above, Pump is objectively undervalued by a massive factor and may represent an asymmetric upside.

This discounts likely due to a few reasons:

- The primary driver of this discount appears to be skepticism around revenue sustainability

The market broadly believes that Pumpfun’s platform-wide volume is largely speculative, cyclical, and heavily tied to short-term memecoin activity. As a result, investors are treating current earnings power as transient rather than durable. Buybacks, while mechanically accretive at these multiples, are not being capitalized in valuation models because the underlying assumption is that revenues will compress materially in a normalized environment. In other words, the debate is not centered on whether Pump is currently profitable, it is centered on whether that profitability still exists 24 months from now.

2. There is also a meaningful information and coverage gap contributing to the discount

For this piece, we spoke to 15 prominent VC and liquid funds to get their thoughts on $PUMP.

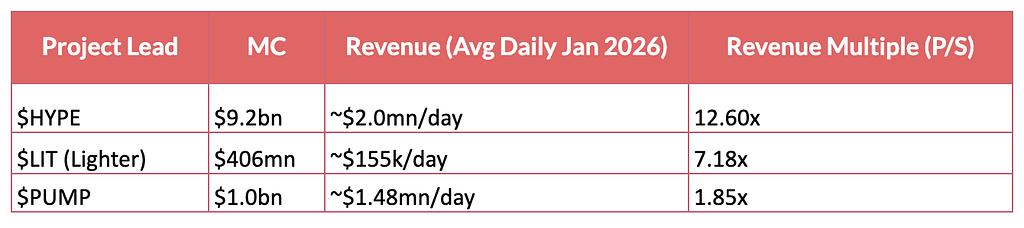

Out of the 15, only one was actively covering $PUMP with bottom-up analysis. The majority had not modelled the new product suite, segmented revenue by product line, or stress-tested volume durability assumptions. This lack of institutional coverage creates a narrative vacuum, where pricing is driven more by perception than by granular financial analysis. By contrast, assets like $HYPE benefit from deeper institutional sponsorship, stronger research coverage, and clearer product positioning, all of which support higher and more stable valuation multiples.

There is also a reflexive narrative element at play. Assets associated with memecoin infrastructure are often categorized as speculative and transient, and they trade accordingly. It takes time and data across market cycles for the market to update that framework. Until Pump’s revenue base survives a broader crypto drawdown and institutional coverage expands, valuation compression may persist regardless of current cash generation.

3. People don’t believe in Pumpfun’s management

Another component of the discount is a credibility premium that has yet to be earned.

Investors express concerns around:

- Long-term vision beyond memecoins

- Capital allocation discipline

- Execution of the broader product roadmap

- Transitioning from viral growth to durable platform economics

Markets tend to assign low multiples to founder-led, high-growth platforms until they demonstrate resilience through volatility and prove that growth can evolve into durable platform economics. Until Pump shows sustained revenue diversification through products such as Pumpswap and Pumpterminal, along with consistent execution and disciplined capital returns, a management credibility discount is likely to remain embedded in the multiple.

$PUMP Valuation Deep Dive: Inorganic Volume or Revenue Machine? was originally published in IOSG Ventures on Medium, where people are continuing the conversation by highlighting and responding to this story.