Author: Turbo @TurboGuo

TL;DR

- Cross-border payment companies’ stablecoin strategies fall into three buckets: stablecoin acceptance (settling payments in stablecoins), stablecoin issuance (applying for licenses to issue their own), and operating through separate offshore brands to isolate regulatory risk.

- Stablecoins offer little fee or speed advantage in cross-border payments. As local payment rails have proliferated, traditional transfer costs have compressed dramatically. The remaining friction sits in domestic settlement, exactly where stablecoins can’t help. FX conversion is also unavoidable, so stablecoins don’t actually solve either core pain point.

- Neobanks are the highest-value segment in the stablecoin cross-border payment value chain. The real advantage of stablecoin payments is closed-loop ecosystems — zero friction only materializes when both sender and receiver settle in stablecoins. Regions with thin banking infrastructure (Southeast Asia, Middle East, Africa) are the strongest use cases. Tether’s investment in SQRIL is a clear signal.

Part 1: Breaking the myth of stablecoin cross-border payment

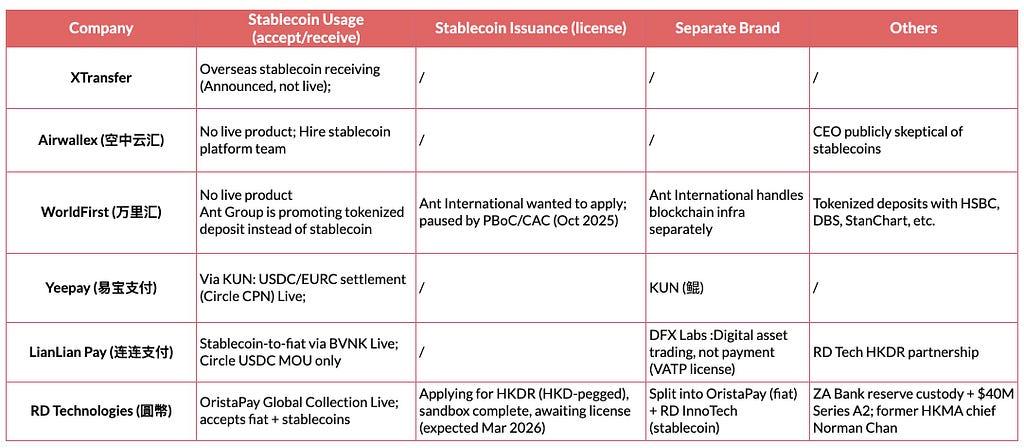

Stablecoin Strategy for main Cross-border payment companies

Asian cross-border fintechs’s stablecoins strategies have three main part:

- Stablecoin Usage: accepting s settling payments in stablecoins)

- Stablecoin Issuance : applying for licenses to issue their own stablecoins

- Separate Brand: operating crypto/stablecoin businesses through independently branded offshore entities to isolate regulatory risk from their domestic licenses.

- The separate offshore entity is essential

Every company with meaningful stablecoin activity operates through a separate offshore entity: KUN (for Yeepay), DFX Labs (for LianLian), RD InnoTech (for RD Technologies). This is due to regulation requirment. PBoC’s October 2025 intervention against Ant Group and JD.com and the February 2026 eight-agency ban, made brand separation a regulatory necessity for any mainland-linked company.

2. Stablecoin acceptance is the only live product, but not many companies disclosed the fee and speed

Most companies are starting with stablecoin acceptance, not issuance. This includes LianLian, KUN, OristaPay. Only RD InnoTech is close to actually issuing a stablecoin (HKDR, license expected March 2026 if pass). However, have not see companies that disclosed the fee and speed of stablecoin payment services like other established payment companies. The only one disclosed fee is BVNK, the fee structure is : 0 for transfer + standard conversion fee + services fee to transfer fund from/to outside wallet + Blockchain fee.

3. The March 2026 HK License Issurance will be a turning point

HKMA will issue its first stablecoin issuer licenses in March 2026. Only a very few companies will be approved. Comfirmed companies that apply for the license are RD InnoTech, JD and Anchorpoint Financial. RD has high possibility of getting the license since they are in the HKMA Stablecoin Issuer Sandbox. JD is unlikely to be approved due to the regulation requirment. Whether KUN or LianLian’s DFX Labs applied is unconfirmed. The license outcome will determine which companies can move from stablecoin usage to issuance, and whether HK becomes a real stablecoin hub or remains constrained by Beijing’s influence.

4. Reasons for Cross-Border Payment Companies’ Stablecoin Adoption are slow

4.1 Stablecoins Offer nearly No Fee or Speed Advantage in Cross-Border Payments

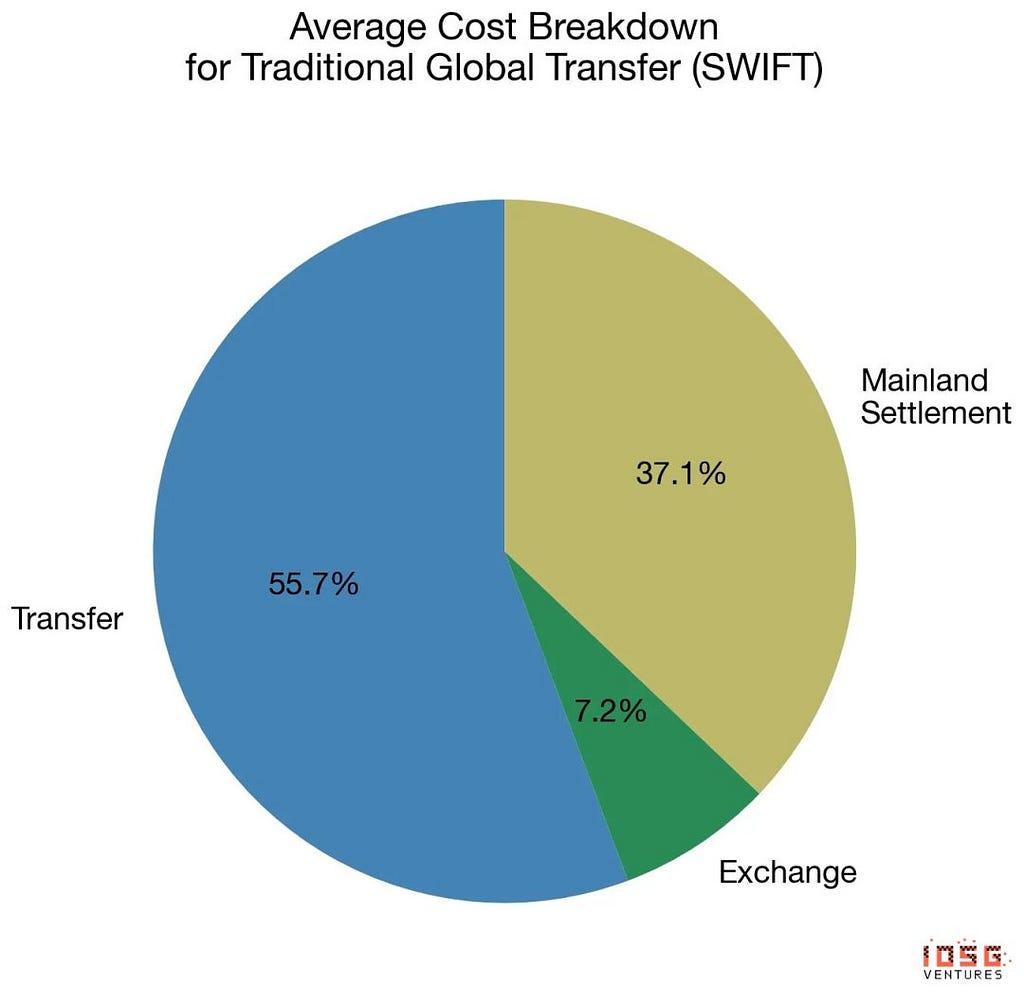

If we want to do cross border payment from oversea to China mainland as a business owner, there are three main steps: Transfer, Exchange and Mainland Settlement.

- Transfer: Moving funds from the overseas buyer to the payment platform, via methods like SWIFT, local bank rails, or internal wallet transfers.

- Exchange: Converting the foreign currency (e.g., USD, EUR) into CNY at a given FX rate.

- Mainland Settlement: Withdrawing the converted CNY to a China mainland bank account or Alipay.

4.1.1 New rails including local rails that bring down traditional transfer to ~0% fee and instant speed

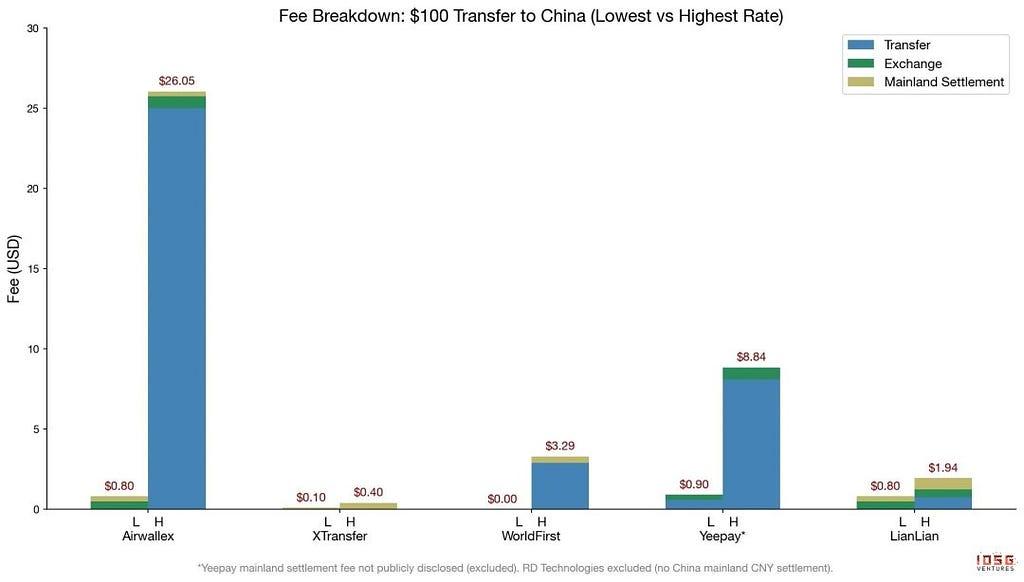

Traditionally, transfer will cost most of the fees and time since SWIFT will take large fees. For the companies that we analysis in this article, it takes 56% of the total fees. For example, it takes $25. to use SWIFT by Airwallex.

However, many cross border fintech have Local Rails now, It means:

- Fintech collects funds using the sender’s domestic payment network (e.g., ACH in the US, SEPA in Europe, UPI in India), internally moves them across its own global network in some way, then pays out via the receiver’s local network, bypassing SWIFT entirely.

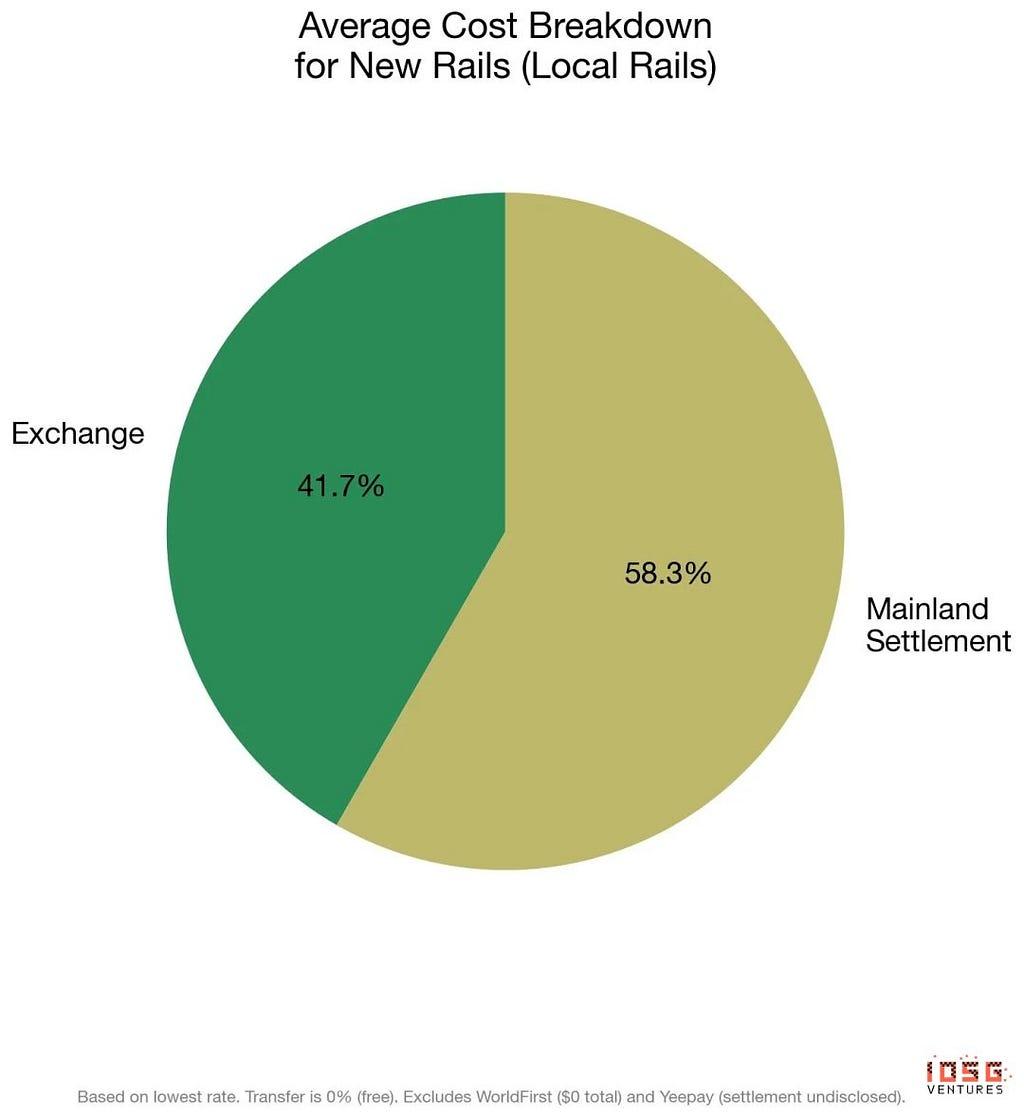

New rails bring down the transfer fee by a lot for cross border transfer. Currently mainland settlement takes 58% of the fees.

However, mainland settlement is not a path that Stablecoin can bypass since people will always want CNY cash in their banks.

Not only stablecoin payment can’t bypass mainland settlement, exchange is also an essential step for cross border payment, there is nearly no room for stablecoin to improve the user experience. The transfer is close to instand and $0 fee, the exchange take most of the fee and stablecoin companies also need to do exchange for users.

Overall, if we do a fair comparison within cross border transfer and excluded mainland settlement and exchange, there is no room for stablecoin to improve.

4.2 Regulation: The pause of stablecoin issurance and concerns

Beijing has moved from passive skepticism to active enforcement against stablecoin activity by mainland companies.

In October 2025, the PBoC and CAC directly ordered Ant Group and JD.com to suspend their Hong Kong stablecoin plans (Source: Financial Times, and these two company doest pause the applying). Both companies had been preparing to apply under Hong Kong’s new stablecoin licensing regime.

Then in February 2026, eight government agencies (PBoC, CSRC, SAFE, and five others) jointly issued 《关于进一步防范和处置虚拟货币等相关风险的通知》.

The notice explicitly bans mainland entities and their controlled overseas subsidiaries from issuing CNY-pegged stablecoins abroad without government approval, stating that such stablecoins “perform some of the functions of fiat currency in circulation” (在流通使用中变相履行了法定货币的部分功能). The regulation also bans RWA tokenization within mainland China and prohibits companies from even including terms like “stablecoin,” “virtual currency,” or “RWA” in their registered business names. This two-step escalation, from targeted orders against specific companies to a blanket legal prohibition, signals that Beijing views private stablecoin issuance as a direct challenge to monetary sovereignty and the e-CNY (digital yuan) strategy.

Concern 1: Currency Over-issuance and Market Manipulation

- Over-issuance without full reserves. Issuers may mint stablecoins without genuinely holding 100% reserves, effectively creating money out of thin air.

- Leverage-driven money multiplication. Even when issuers do maintain 100% reserves, stablecoins still generate a multiplier effect through downstream activities such as lending, collateralization, trading, and revaluation. This means that in a potential bank run scenario, the redemption demand could be several times larger than the original reserve pool

Chinese officals argued that from the perspective of financial and asset market trading, the most critical risk to guard against is market manipulation, especially price manipulation, which requires sufficient transparency and effective regulation.

Concern 2: Stablecoins Won’t Actually Reduce Costs

While many believe stablecoins will reshape the payment system, the current infrastructure, especially in retail payments, already has very limited room for further cost reduction. The existing retail payment ecosystem already includes third-party payment platforms, CBDC, software and hardware wallets, and clearing infrastructure.

This is true in some level according to our previous analysis.

Part 2: Investment Implications: The Neobank Thesis

2.1 Core Thesis: Neobanks is the key of stablecoin cross border payment

The stablecoin cross-border payment value chain has three layers:

- Issuance (Tether, Circle, HKMA licensees): Creating stablecoins

- Infrastructure (Bridge/Stripe, BVNK, Circle CPN): Moving and converting stablecoins

- Distribution/Endpoint (Neobanks): Converting stablecoins to local spending power

Neobanks are the core bottleneck and the highest-value opportunity for the following reasons:

2.1.1 Neobanks Are the Last Mile

The real implication is that stablecoin cross-border payment only has an advantage in ecosystems where stablecoin itself is the final destination, not a bridge to fiat.

If a merchant earns in stablecoin and pays suppliers in stablecoin, if employees receive salary in stablecoin and spend through a stablecoin-native neobank, the entire transaction stays on-chain and never touches traditional rails at all.

In that scenario, there is no transfer fee, no FX spread, and no settlement cost. The problem is that this requires both ends of the transaction to live inside the stablecoin economy.

The moment either party needs to convert back to fiat (CNY, USD, HKD), the cost of off-ramping reintroduces the same settlement fees that fintech local rails already handle cheaply. This is why stablecoin payment has the strongest case in regions with underdeveloped banking infrastructure, high remittance corridors, or crypto-native communities where people already hold and spend stablecoins daily.

Additionally, neobank users can have above average yield on top of stablecoin, which can bring additional reason for users to use stablecoin cross-border payment.

2.1.2 Must Be in Regions with Lacking Financial Infrastructure

Stablecoins have the strongest case where they are more convenient than traditional banking:

- SE Asia (Philippines, Vietnam, Indonesia): 44%+ unbanked, high smartphone penetration

- Middle East/Africa: Large expatriate remittance corridors, weak local rails, progressive regulation (UAE 4 regulatory frameworks)

Tether act as a parallel financial system in Vietnam. In the meanwhile, Tether invested in SQRIL, this is a move that showing their growth strategy is on funding neobank-layer companies that let people spend USDT locally in less developed countries, which is the strongest market signal that the neobank endpoint is where the real value accrues.

2.1.4 Why Series A/B Is the Sweet Spot

Stablecoin neobanks are relatively heavy infrastructure businesses that require:

- Local licenses and regulatory approval

- Local banking partners for fiat on/off-ramps

- Local compliance infrastructure (KYC/AML)

- Merchant network development

- Consumer trust building

This means:

- Seed/Pre-A is too early: The business model is not yet proven in the local market. Regulatory risk is high. Unit economics are unclear.

- Series A/B is optimal: After proving the local market has demand, the business has run successfully, regulatory standing is confirmed, and unit economics are validated. Investment risk decreases materially. The upside (expansion to adjacent markets, deeper market penetration) becomes clearer.

- Late stage/IPO may be too late: Valuations will already reflect proven business models

Part 3: Breakdown of each cross-border payment companies’ stablecoin strategies

Airwallex (空中云汇)

Airwallex is taking a more cautious approach: build internally first, deploy when regulatory and market conditions are favorable. This may reflect the company’s strength in traditional rails reducing the urgency to adopt stablecoins immediately.

1. Stablecoin/Blockchain Integration: Skepticism, no live product yet

1.1 CEO Jack Zhang has been skeptical of stablecoins.

- He has argued that Airwallex already moves money “at the cost of less than 0.01% and real time,” and that “you can’t be cheaper than free and faster than real time.”

- The company’s official blog echoed this position, citing fragmented regulation, the complexity of on/off-ramping, and limited mainstream adoption as key barriers, concluding that “stablecoins can’t yet solve cross-border payments at scale.”

1.2 Internal stablecoin Team

Airwallex posted 22 stablecoin engineering jobs in July 2025 to build a token settlement platform. Job postings revealed that the company is building infrastructure to “allow customers and internal systems to buy, hold, send, and settle tokens globally, support near-instant global payments, and enable on-chain liquidity as well as seamless fiat-to-stablecoin conversion”

The planned use cases include cross-border settlements in emerging markets, on-chain liquidity management and programmable payments with fiat-to-stablecoin conversion services.

1.3 Current Status:

- No live stablecoin product yet. 2025 end-of-year mission update contain zero mention of stablecoins.

- No public partnerships with Circle, Tether, or other stablecoin issuers

- 2026 strategic priorities are geographic expansion , AI-powered developer tooling, and customer experience, not stablecoins

- Company blog (Jan 2026) states “the jury is very much still out on the benefits of stablecoins”

XTransfer

1. Stablecoin/Blockchain Integration: Have positive views, but have not launched any live product; no hidden blockchain brand found

1.1 Overseas stablecoin receiving service (Announced, not live)

XTransfer announced in August 2025 that it will launch an overseas stablecoin receiving service (海外稳定币收款服务) within 2025, initially opening to select customers. However, as of February 2026, there is no public confirmation that the service has gone live.

1.2. Assumtion: Dual Wallet Model

XTransfer’s stablecoin strategy centers on a “dual-currency wallet” approach, allowing businesses to hold both fiat and stablecoins at the same time.

In addition, there is no hidden crypto/blockchain related brands is found for XTransfer

WorldFirst (万里汇-蚂蚁集团)

1. Stablecoin/Blockchain Integration: Not at WorldFirst product level, but Ant International is building blockchain rails

WorldFirst’s own product does not currently offer stablecoin or crypto services. Its official services has not include blockchain, stablecoin, or digital currency. All WorldFirst products operate on traditional banking rails

However, parent Ant International is building significant blockchain infrastructure that will likely flow through to WorldFirst:

1.1 Whale Platform’s Tokenised Deposit Service (TDS)

In 2024, over 1/3 of Ant International’s $1 trillion+ total fund processing volume was processed through Whale using blockchain technology. This is not stablecoin usage, but Tokenised Deposit Service (TDS).

Tokenised deposit is issued by regulated banks instead of stablecoin companies. Take HSBC as an example, tokenized deposit allows HSBC’s clients to create digital records of their traditional, fiat deposits. While HSBC maintains the fiat deposits, each one of the digital records on the DLT is a token that can be transferred. Clients can transfer funds without having to wait for batch processing.

In May 2025, Ant Group launched Hong Kong’s first blockchain settlement solution, the “Tokenized Deposit Service” with HSBC, allowing real-time payments in HKD and USD via corporate wallets

- Additional tokenized deposit integrations with: DBS, Standard Chartered, OCBC, BNP Paribas, JP Morgan’s Kinexys Digital Payments, and Deutsche Bank

- UBS Digital Cash (Nov 2025): UBS Singapore signed MoU with Ant International for multi-currency tokenized deposit capabilities integrated into Whale

- Standard Chartered (Dec 2025): Launched tokenized deposit solution for HKD, CNH, SGD, and USD on Whale, including a cross-bank transfer of HKD $3.8M from HSBC to StanChart via deposit tokens

- Ant International has worked with ten international banks supporting tokenized deposits on Whale

- Participate the Singapore’s MAS “Project Guardian” on tokenized deposits in transaction banking (ISDA and Ant co-led an industry report on tokenized bank liabilities for FX settlement)

1.2 Stablecoin License Applications: Ant wanted to apply but the government stopped it

- In around June 2025, Ant Group said they will apply to HKMA once Stablecoin Ordinance takes effect.

- In Oct 2025, Financial Times reports Alibaba-backed Ant Group and JD.com have been instructed to suspend their stablecoin plans in Hong Kong from 中国人民银行(PBoC)and 国家互联网信息办公室(CAC)

- In Feb 2026, the new regulation 《关于进一步防范和处置虚拟货币等相关风险的通知》emphasized that:No mainland companies can participate in CNY related stablecoin issuance.

- Ant Group filed “ANTCOIN” trademarks with HK’s IP Department (interpreted as strategic IP protection), but no public indication that Ant has resumed its actual license application

Yeepay (易宝支付)

1. Stablecoin/Blockchain Integration: Not directly at Yeepay, but founders operate a hidden stablecoin brand “KUN (鲲)”

Yeepay’s official product does not integrate stablecoins. However, Yeepay’s co-founders are actively building a stablecoin payment company through a separate brand: KUN (鲲)

KUN (鲲) is Yeepay’s “Overseas Ecological Partner” . Key personnel overlap:

- Liu Jialiang (刘家良), Yeepay’s Partner and SVP, is KUN’s Founder and CEO (“Louis Liu”)

- Chen Yu (余晨), Yeepay’s Co-Founder and President, is KUN’s Chief Advisor

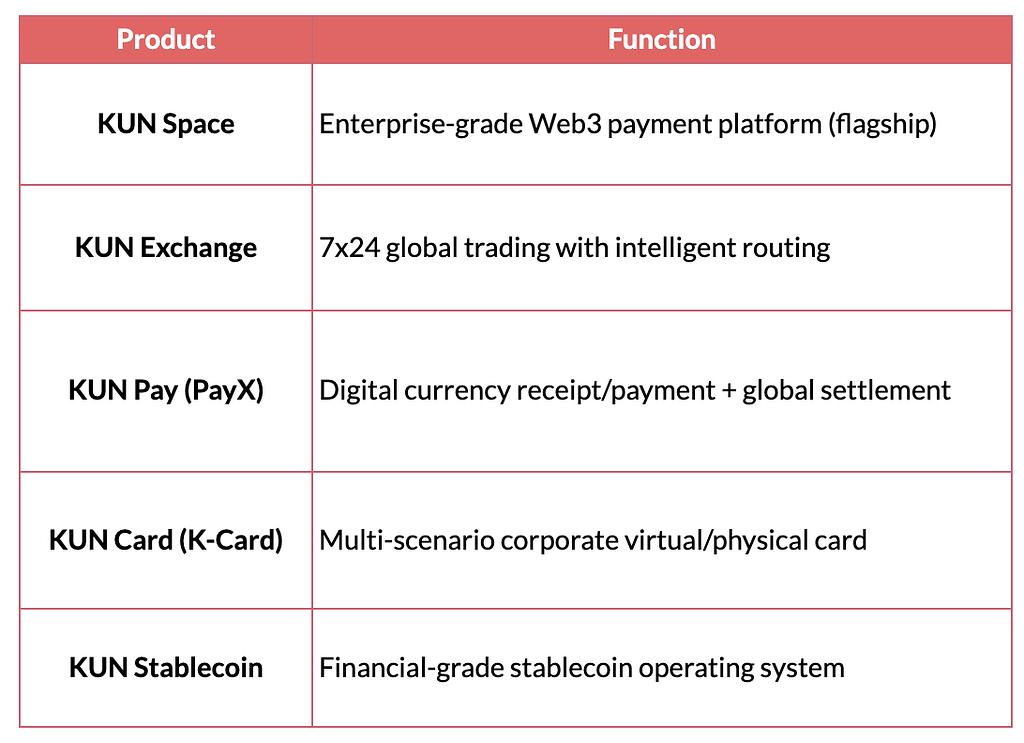

- 1 KUN’s Products

Note: KUN does not publicly disclose its fee structure. KUN states it serves “customers outside mainland China and the United States” only

2. KUN’s Partnerships & Integrations

- Circle Payments Network (CPN): Live. Confirmed by Circle as a CPN partner for 24/7 USDC/EURC-based stablecoin settlement. CPN mainnet launched mid-2025 with 29 financial institutions.

- WSPN: Integrated WUSD (USD-pegged stablecoin) into KUN Space platform for cross-border enterprise transactions (March 2024)

- Marco Digital (马可数字, 01942.HK): Reported to have completed Asia’s first USDT-based insurance commission payment via KUN (Aug 2025).

LianLian Pay (连连支付 / 连连数字)

1. Stablecoin/Blockchain: YES, integrate stablecoin by partnerships

LianLian has one of the most aggressive stablecoin strategies among Chinese cross-border payment companies.

1.1 Circle/USDC MOU with LianLian: Still exploration phase, not yet live product.

Signed MOU with Circle. Evaluating USDC for high-volume international payment flows. Exploring Circle’s layer-1 blockchain Arc for future payment use cases.

1.2 BVNK Partenership: Live Stablecoin-Powered Payments Partenership (June 2025)

Flow: Merchants deposit stablecoins -> BVNK auto-converts to USD -> LianLian routes through global network.

1.3 RD Technologies (圆币科技): HKDR Stablecoin

Partnered with RD Technologies . RD plans to issue HKDR (HKD-pegged stablecoin) on Ethereum. LianLian uses RD Technologies’ RD ezLink enterprise identity verification and RD Wallet payment tools. Also partners with HashKey Exchange, Cobo.

HKDR remains a sandbox/testing product, not a licensed stablecoin. The partnership cannot become fully operational until RD Technologies obtains a formal HKMA stablecoin issuer license, expected March 2026.

1.4 DFX Labs: Virtual asset trading platform; Wholly-owned, Hong Kong-listed subsidiary company

Their offerings include:

- Crypto trading: buying/selling Bitcoin and other cryptocurrencies

- Wallet services: secure custody/storage of virtual assets

- Liquidity services

- DFX Labs received HK SFC VATPlicense.VATP license: Type 1-dealing in securities + Type 7-automated trading. Conditions: must complete rectification per SFC on-site inspection and pass independent penetration testing before full operations.

- No confirmed evidence that DFX Labs formally applied for HK stablecoin.

RD Technologies (圓幣科技)

Founded by the former HKMA chief. Its competitive advantages are:

- Regulatory pedigree: Former HKMA chief as chairman, first-batch sandbox participant

- Dual licensing: SVF (fiat payments) + stablecoin sandbox

1. Core Business: Payment (OristaPay)+Stablecoin Issurence(RD InnoTech)

- Operates under the Stored Value Facility (SVF) License (SVF0016) granted by the HKMA in December 2022

- Multi-currency e-wallet supporting 8 currencies for business payment and FX management

- Transfer methods: FPS (Faster Payment System), CHATS, Telegraphic Transfer (TT)

Two independent business lines:

- OristaPay (源穩支付, operated by RD Wallet Technologies Ltd.): Fiat-basedB2B cross-border payment and wallet services under the existing SVF license. Positioned as a “next-generation payment infrastructure provider”

- RD InnoTech Limited (圓幣創新科技有限公司): Dedicated to stablecoinissuing (HKDR) and blockchain/Web3 initiatives

1.1 OristaPay (RD Wallet)

OristaPay launched the Global Collection product (confirmed live), enabling fiat and stablecoin cross-border payments. 24/7 liquidity, with particular depth in Africa and Latin America.

- Receive payments in 100+ currencies across 200+ countries and regions

- Accepts major stablecoins for both merchant funds and third-party collections

- Features rapid settlement with real-time AML and KYT (Know Your Transaction) screening

- Specific fee details for Global Collection not publicly disclosed

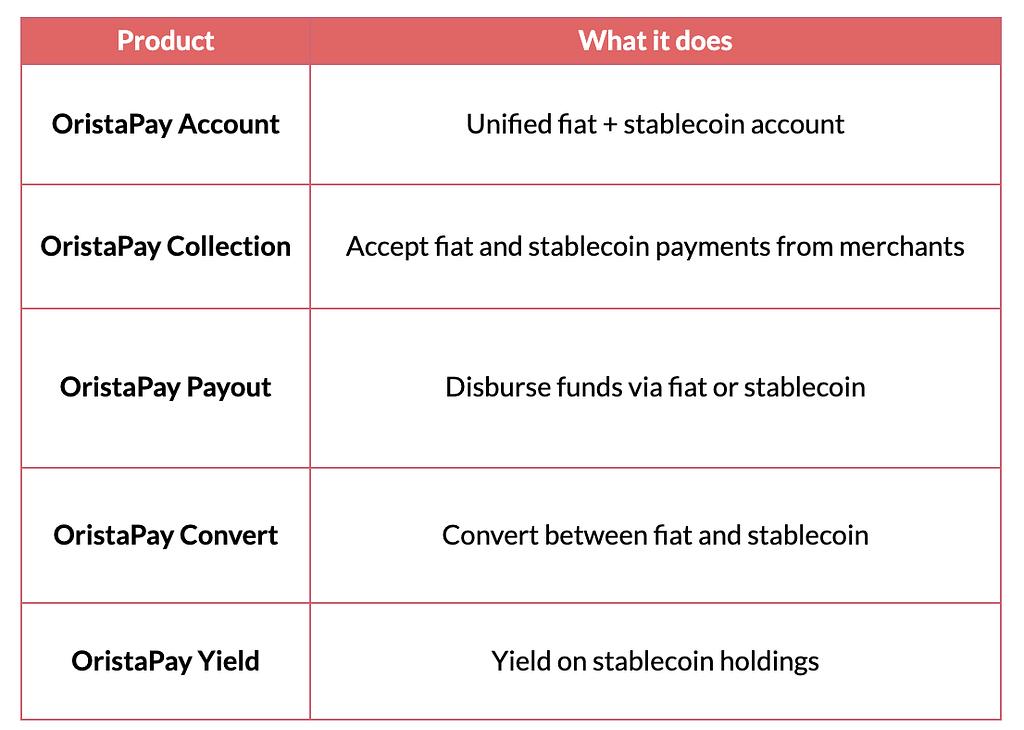

OristaPay Stablecoin Products

1.2 RD InnoTech Limited (圓幣創新科技有限公司)Stablecoin Issuing

1.2.1 HKDR Stablecoin

HKMA Stablecoin Issuer Sandbox (July 2024):

RD InnoTech was admitted into the first cohort of the HKMA stablecoin issuer sandbox, alongside Standard Chartered/Animoca/HKT (HKDG) and JD CoinLink (JD-HKD)

1.2.2 Regulatory Timeline for stablecoin

- Dec 2022: SVF License (SVF0016) granted by HKMA

- Jul 2024: Admitted to HKMA Stablecoin Issuer Sandbox (first cohort)

- Aug 2025: Hong Kong Stablecoin Ordinance takes effect

- Sep 2025: Brand restructuring, OristaPay and RD InnoTech separated

- Jan 2026: OristaPay Global Collection launched with stablecoin support

1.3 Key Partnerships

ZA Bank: Active partnership with investment

ZA Global co-led a US$40M Series A2 round in RD Technologies (alongside China Harbour, Bright Venture, Hivemind Capital). Signed MOU with ZA Bank covering

- Reserve custody: ZA Bank provides custody services for HKDR reserve assets (ZA Bank became HK’s first digital bank to offer reserve banking services for stablecoin issuers)

- Distribution: ZA Bank exploring becoming a sales/distribution partner for HKDR

- RD InnoTech is the inaugural stablecoin issuer to use ZA Bank’s reserve banking services

Additional Partnerships:

- Allinpay International: Stablecoin-enabled online/offline payment integration

- Ripple: Aligned for 2026 growth

- Circle Payment Network: Joined CPN

Appendix: Cross-Border Payment Companies Fees and Speed Breakdown and compairson

Comparison

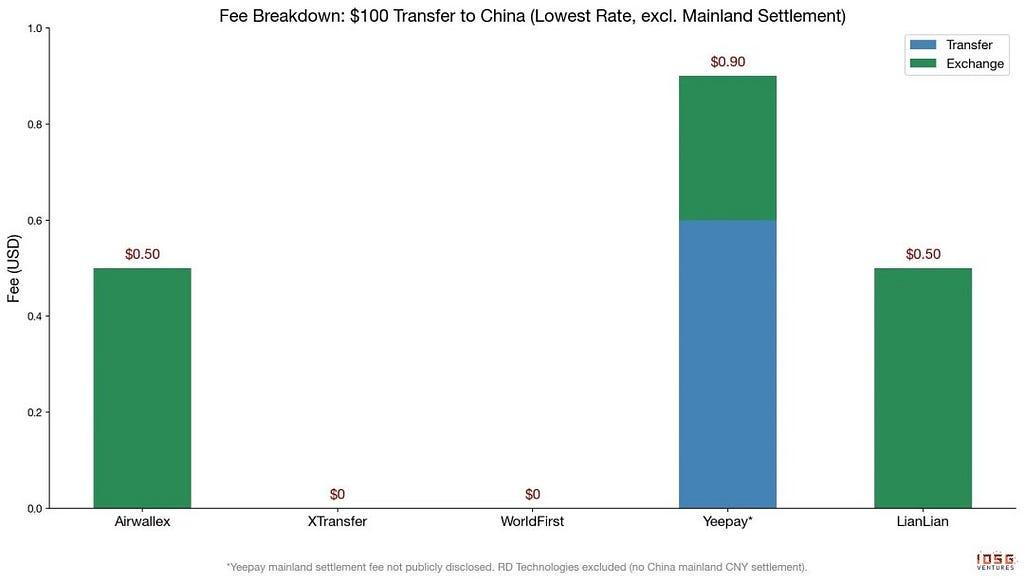

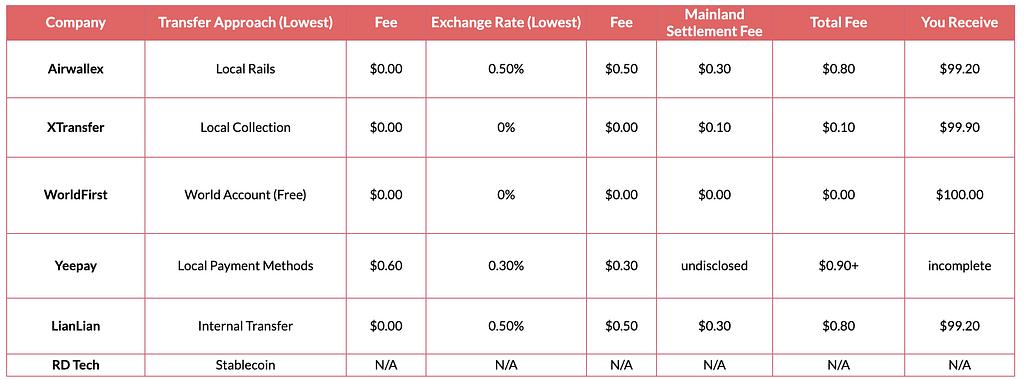

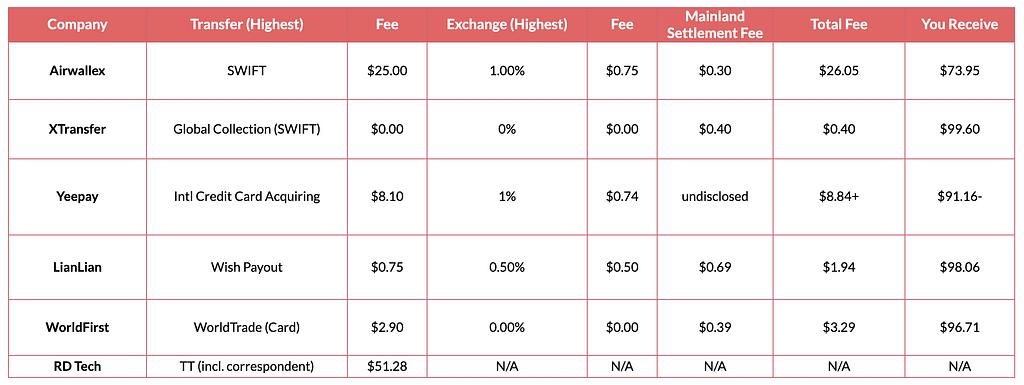

Cost Comparison: $100 Overseas to China Mainland (Lowest Rate)

Scenario: Transfer $100 USD from overseas to a China mainland bank account. Each step uses the lowest available rate from each company. Fees are applied sequentially.

Notes:

- XTransfer’s 0.1% settlement rate requires high volume; standard rate is 0.4% max ($0.40 fee, $99.60 received)

- WorldFirst’s $0 total assumes personal Alipay withdrawal; B2B bank withdrawal is 0.3% (B2C) or 0.4% (B2B)

- Yeepay’s Local Payment Methods fee ranges 0.6%-1.6%; lowest rate (0.6%) used here. CNY settlement fee not publicly disclosed

- LianLian’s 0.3% settlement is for high-volume users; standard can be up to 0.7%

- RD Technologies does not disclosed fee and speed information

Cost Comparison: $100 Overseas to China Mainland (Highest Rate)

Scenario: Transfer $100 USD from overseas to a China mainland bank account. Each step uses the highest/worst-case rate from each company. Fees are applied sequentially.

Notes:

- Airwallex SWIFT fee is $25/txn flat; at $100 this is 25% of the transfer. More reasonable at higher amounts

- Yeepay card acquiring: 3.8% + $0.30 base + 1% cross-border + 3% currency conversion = $8.10 on $100; FX spread up to 0.8%; CNY settlement fee not publicly disclosed

- WorldFirst settlement: 0.4% for B2B withdrawals to CNY per All Product Breakdown table

- LianLian Wish payout capped at 0.75%; settlement up to 0.7%

- RD Technologies TT with correspondent bank fees is HKD 400 (~$51.28); they do not offer mainland CNY settlement

- Flat fees (SWIFT, TT) disproportionately impact small transfers; percentage-based fees scale linearly

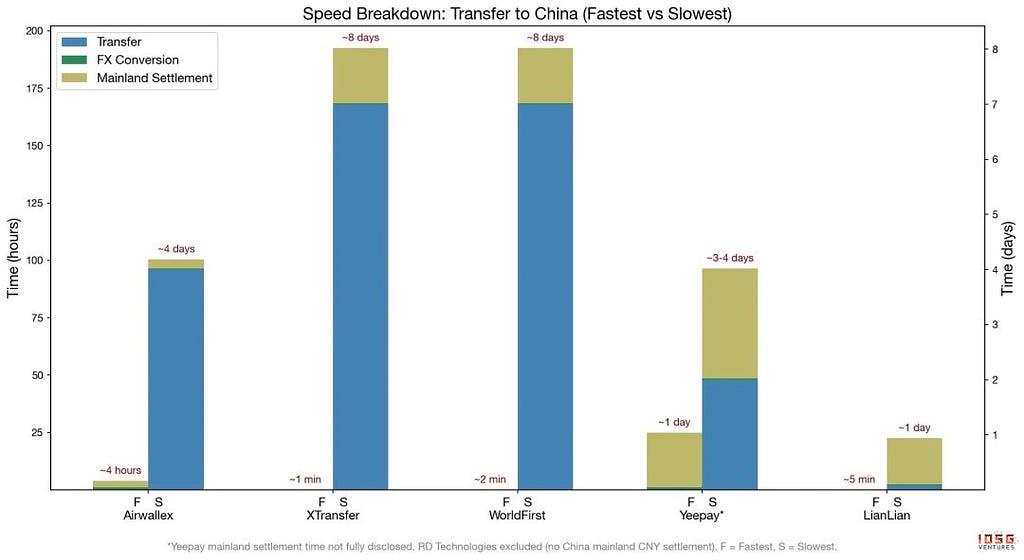

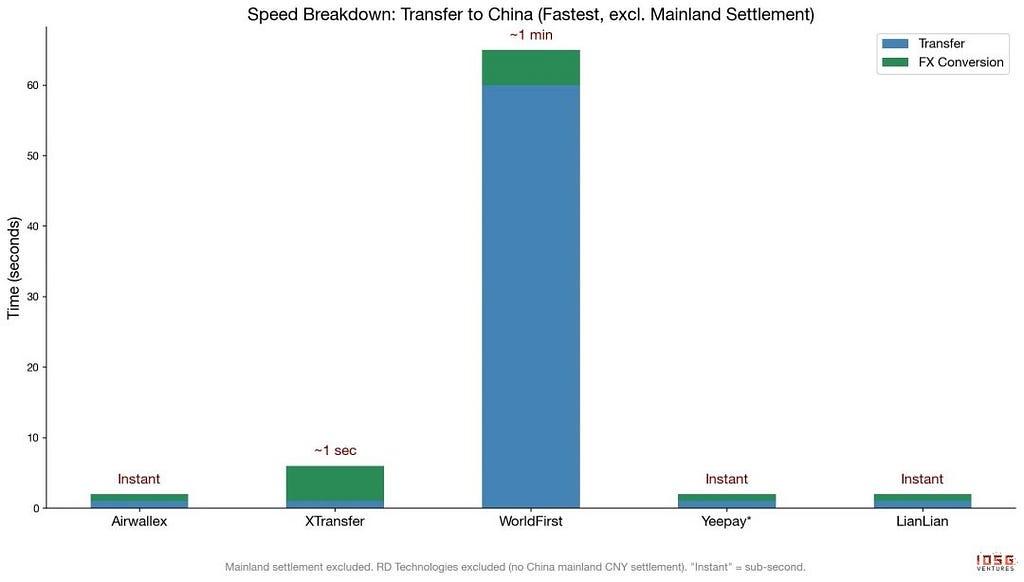

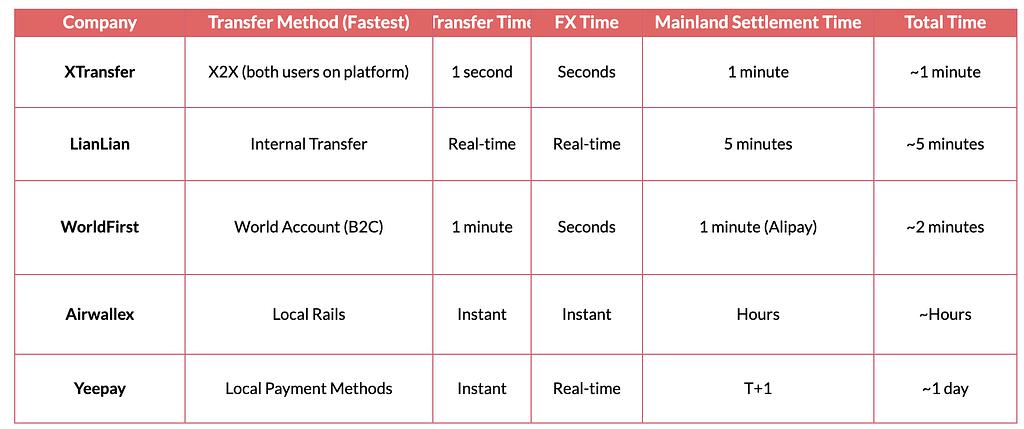

Speed Comparison: Overseas to China Mainland (Fastest)

Scenario: Transfer USD from overseas to a China mainland bank account. Each step uses the fastest available method.

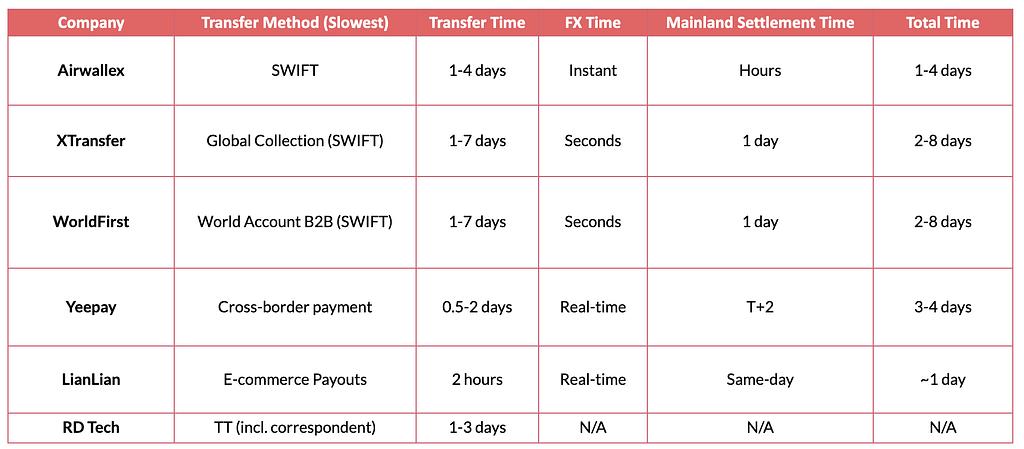

Speed Comparison: Overseas to China Mainland (Slowest)

Scenario: Transfer USD from overseas to a China mainland bank account. Each step uses the slowest available method.

Notes:

- XTransfer X2X requires both buyer and seller to be on the XTransfer platform

- WorldFirst’s 1-minute Alipay withdrawal is to personal Alipay, not business bank account

- Yeepay’s fastest transfer (Local Payment Methods, instant) is bottlenecked by T+1 to T+2 CNY settlement

- Yeepay’s slowest transfer is now Cross-border payment (0.5–2 days), replacing the removed Export Seller Collection product

- RD Technologies does not offer mainland China CNY settlement; times shown are HK-only

- The slowest path for all companies is driven by SWIFT, which adds 1–7 days before FX/settlement even begins

Stablecoins in Asian Cross-Border Payments: Strategic Landscape and Investment Thesis was originally published in IOSG Ventures on Medium, where people are continuing the conversation by highlighting and responding to this story.