Author: Baheet

Compiled by: Jia Huan, ChainCatcher

The construction of institutional-grade financial infrastructure often follows a predictable pattern. You can't start with the most expressive product and then work backward.

You need to start with the liquidation layer, prove that it can function properly under pressure, and then unlock all the functions that depend on it.

The New York Stock Exchange did not add derivatives before it had a well-functioning stock market. Similarly, the Chicago Mercantile Exchange did not launch options before it launched futures.

This order is by no means arbitrary. The order of the lower levels determines the possibilities for the upper-level structures.

Hyperliquid understands this very well.

Hyperliquid is widely regarded as a DEX that continuously delivers new products. It's an exchange that has added spot trading, tokenized assets, and then prediction markets through perpetual contracts. It has a fast-moving team.

That statement isn't wrong, but it completely misses the point.

Hyperliquid didn't build a DEX and keep adding products. They built a liquidation engine and unlocked it layer by layer.

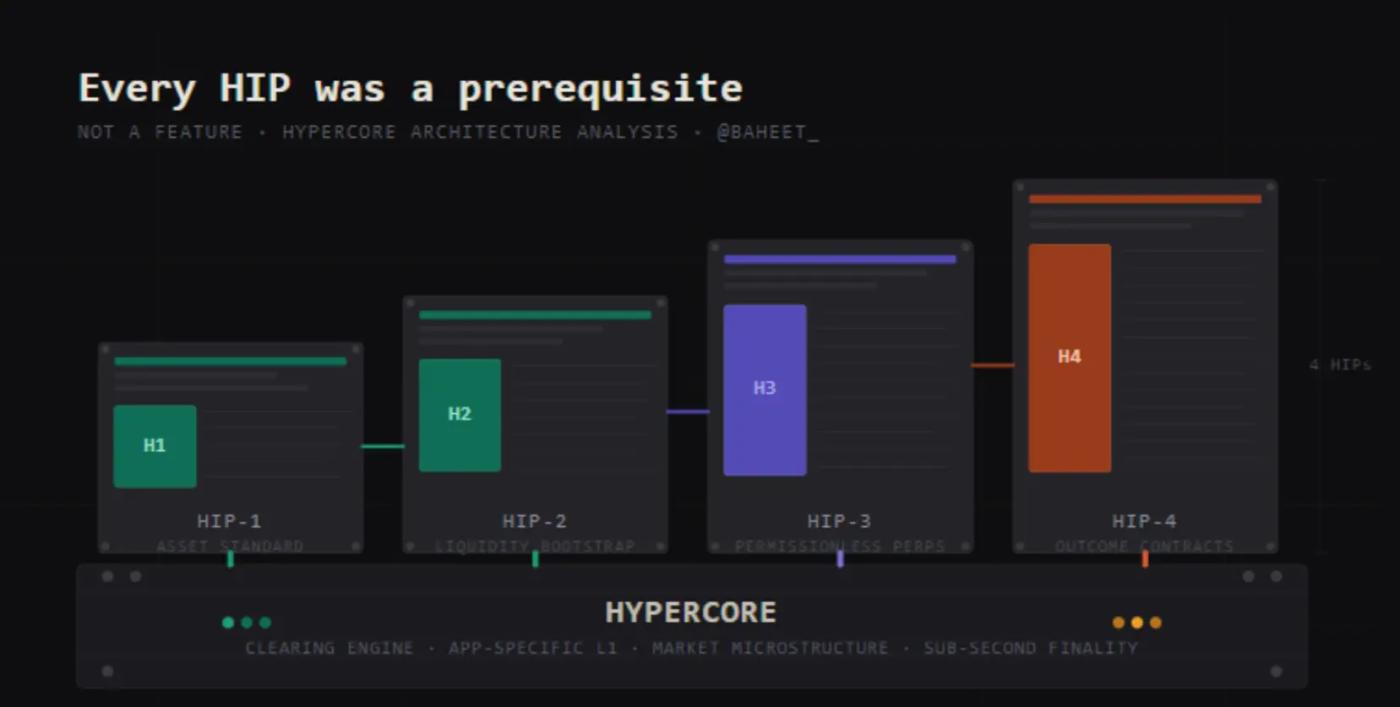

Each HIP is a prerequisite, not just a function.

HIP-4, the proposal dubbed the "Polymarket killer" by everyone, is the ultimate proof that its objective was very clear from the very beginning.

Base

Before any HIP existed, there was a design decision that determined everything that followed.

Hyperliquid builds HyperCore as an application-specific L1 layer optimized entirely around market microstructure. It does not pursue general programmability or the execution of arbitrary smart contracts.

Focusing solely on market microstructure. Sub-second confirmation, predictable execution, clear state management, and a matching engine capable of handling the throughput demands of professional derivatives trading.

This is a deliberately imposed constraint. By refusing to build a universal chain, Hyperliquid has relinquished the developer breadth that Ethereum and Solana are vying for.

In return, they received a clearing engine that could reliably support the institutional market from day one.

This performance guarantee is based on AMM's DEX and general L1, which has been attempted to be modified for many years but has not yet been fully realized.

Every subsequent HIP was made possible because HyperCore was first built in this way.

Constraints themselves are a strategy.

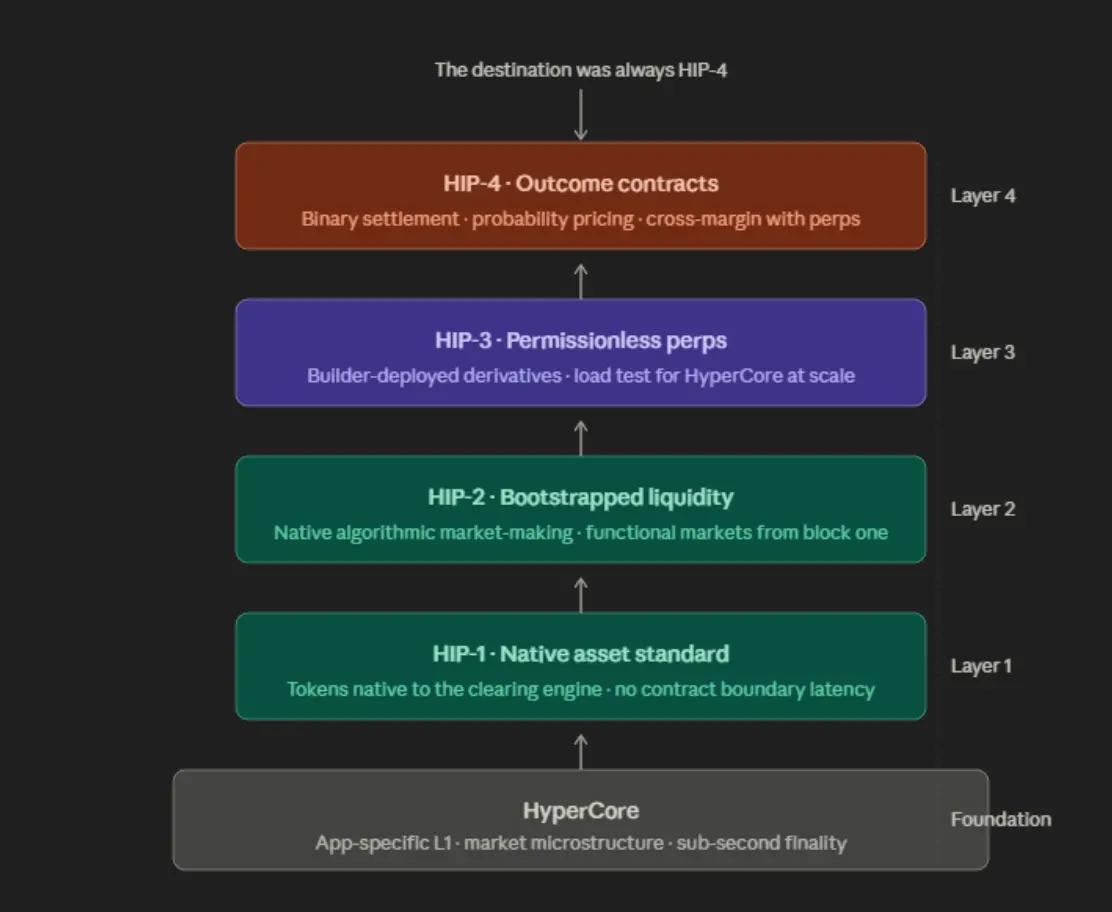

HIP-1: Asset Standard

The first layer is the most basic and also the least discussed.

HIP-1 introduced Hyperliquid's native token standard, which is the protocol's response to ERC-20, but there is a key structural difference.

Tokens under HIP-1 are not smart contract balances existing on a general-purpose virtual machine. They are native units of the HyperCore engine itself, and from the moment of their existence, they can be traded directly within the high-performance matching infrastructure.

This distinction is far more important than it sounds.

On Ethereum, assets and the exchanges that trade those assets are separate systems and must communicate across contract boundaries.

On Hyperliquid, assets and exchanges are the same system. There are no bridges between them, no latency introduced by cross-contract calls, and no execution risk space that plagues DeFi protocols built on a general-purpose chain.

HIP-1 addresses the asset availability issue.

But its deeper function is to establish HyperCore as the native home for financial primitives, rather than just an execution environment for arbitrary code.

Without this proof, everything that follows will be unreliable.

HIP-2: Guiding Liquidity

Illuminated assets are meaningless. This is the cold start problem, which kills far more promising protocols than any technical glitches.

You need liquidity before traders appear, and you need traders before liquidity providers appear.

Most projects try to mitigate this conflict through incentive programs, token release schedules, and market maker subsidies. These are not solutions. These are delays.

HIP-2 introduces Hyperliquidity, a native algorithmic market-making mechanism directly built into the protocol layer.

Unlike AMMs that passively wait for trading volume and expose liquidity providers to inevitable Impermanent Loss at market settlement, Hyperliquidity automates the provision of liquidity for spot assets in a way that makes the economic model sustainable from the first block.

Any asset launched on Hyperliquid will immediately have a fully functional market. Not "eventually." Immediately.

The significance of HIP-2 extends beyond the operational level. It demonstrates that HyperCore can natively solve the cold start problem without outsourcing liquidity routing to external market makers or incentive programs.

This proof laid the foundation for further development. Licenseless perpetual contracts would face the same cold start problem on a larger scale. HIP-2 demonstrated that the engine was fully capable of handling it.

HIP-3: Stress Test

It is from here that this argument becomes undeniable.

HIP-3 broke the monopoly on listing tokens. Prior to this, each marketplace on @HyperliquidX was deployed and managed by a core team. This centralized model ensured quality but limited diversity.

HIP-3 introduces perpetual contracts deployed by builders, allowing external teams to deploy perpetual markets for any asset without requiring permissions.

Memecoins, indices, pre-market tokens, niche trading pairs. Anyone who can stake one million HYPEs can list on a marketplace and operate within HyperCore's infrastructure.

The results were immediate. Open interest surged from less than $200 million to over $1.26 billion. Daily trading volume reached $5.9 billion.

Early entrants have captured up to 85% of the market share in their respective categories. By any standard, HIP-3 represents a breakthrough.

But the most important thing HIP-3 does is not to generate trading volume.

It demonstrates that creating a permissionless marketplace on HyperCore can operate at scale under real-world conditions and withstand real financial risks.

The matching engine held up. The state management system held up. The fee mechanism held up.

HyperCore has now passed stress tests for simultaneous permissionless derivatives trading across dozens of assets.

HIP-3 is an exam. HIP-4 is where the real significance of the exam lies.

HIP-4: The Ultimate Goal

The resulting contract appears to predict market products, but it is actually a closed loop in the entire architecture.

HIP-4 introduces fully collateralized, binary-settled contracts that trade between 0 and 1 and are settled to one of the values based on verifiable event outcomes.

There is no clearing process; entry involves fixed risk exposure, and settlement is made in cash using USDH.

On the surface, this puts Hyperliquid in direct competition with Polymarket and Kalshi. The framework itself isn't wrong, but it underestimates the substantial changes that are taking place.

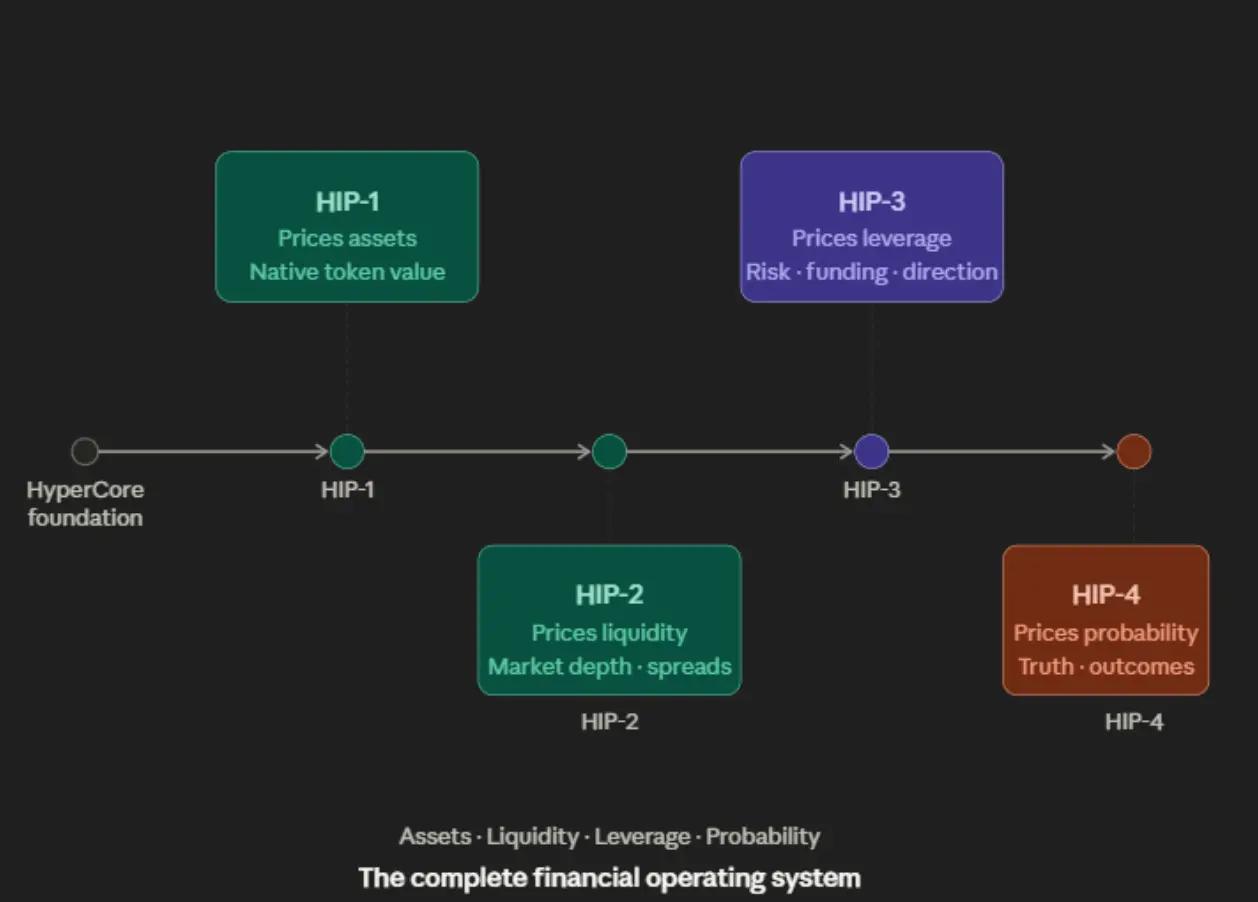

The deeper function of HIP-4 is to extend HyperCore's pricing power from assets and leverage to probability itself.

Prior to HIP-4, HyperCore could price the value of an asset and how much leverage the market could support. After HIP-4, it can price whether something will happen.

This step completes the final link in the financial operating system.

Price direction, leverage, and probability are the three fundamental dimensions of financial risk. HyperCore can now natively express these three dimensions within a unified margin environment, on the same clearing engine.

This is why cross margin margin capability is the most important function of HIP-4, not just the superficial market prediction.

Traders can use the same collateral to hold a leveraged perpetual contract position and purchase a result contract simultaneously.

Idle funds at the market level are predicted to become active capital at the perpetual contract level.

These two systems are not adjacent products sharing a balance sheet. They are the same system, representing different dimensions of risk for the same clearing infrastructure.

No existing prediction market can provide this, because no existing prediction market is built on a proven derivatives clearing engine.

Polymarket and Kalshi are the settlement layers for binary betting. HyperCore, a financial operating system, happens to support binary betting as one of its many primitives.

contrast

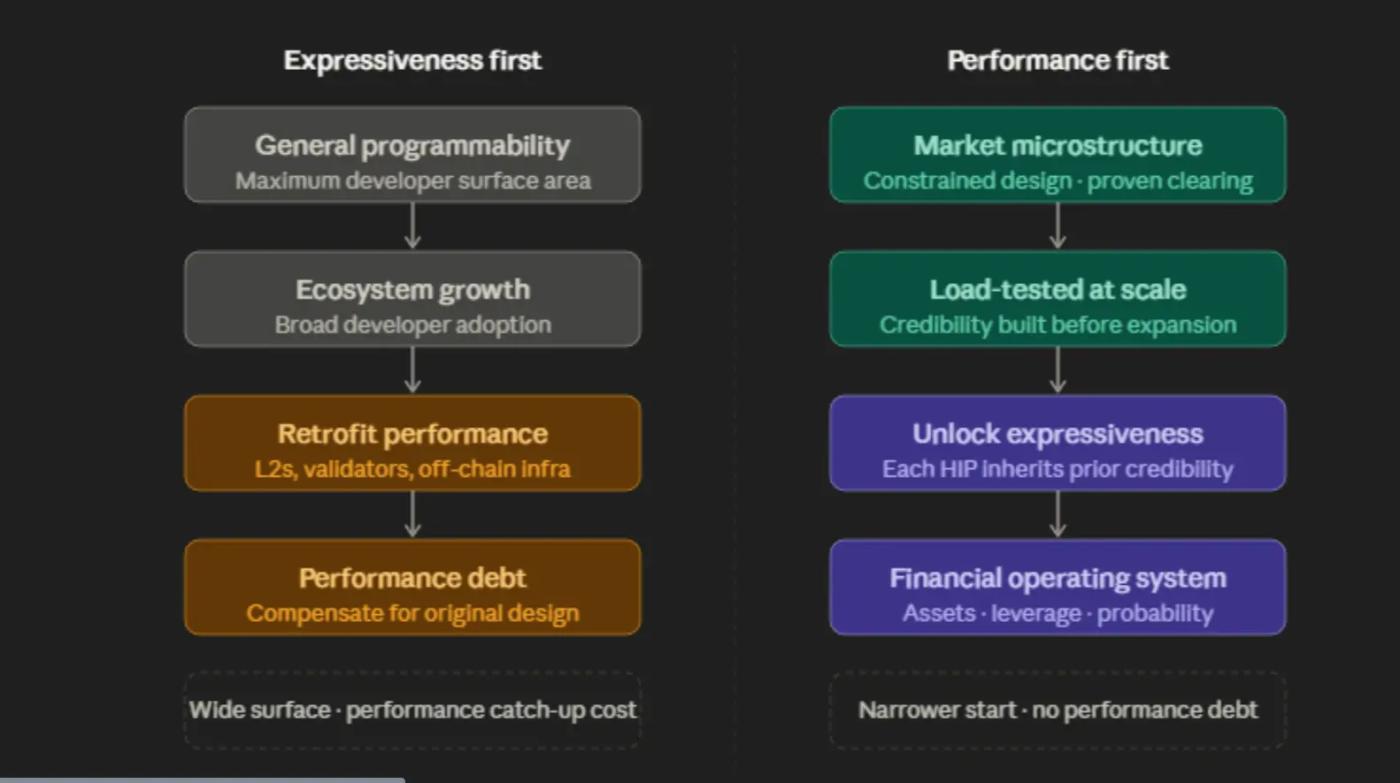

The order in which Hyperliquid chose to proceed becomes clearer when you observe how the broader ecosystem handles the same problem.

Most blockchain infrastructure is designed around a core belief: first, give developers maximum programmability, and performance will follow.

This is not a mistake. Considering the demand in the industry in its early years, it was a rational bet.

Ethereum's programmability has unlocked an entire class of previously impossible financial experiments. Solana's throughput demonstrates that on-chain systems can approach the speed requirements of real-world financial applications.

Both chains have achieved real breakthroughs and continue to support some of the most important applications in the crypto space.

However, prioritizing programmability over performance creates a specific technical debt.

When applications built on a general-purpose blockchain become complex enough to require institutional-level execution, the blockchain must be modified to address the performance guarantees that were not prioritized when it was first built.

This kind of transformation is difficult, expensive, and can never be completely clean and simple.

The execution environment was not designed around the market microstructure, and no amount of Layer 2 scaling or validator optimization can fully compensate for the original design choices.

Hyperliquid took the opposite bet. It completely confined the design space to the market microstructure at the base layer, and then unlocked the programmable space on top of a liquidation engine that had already been validated under real-world conditions.

The trade-off is a narrower reach for early developers. The reward is that every product built on HyperCore inherits the reliability of the underlying liquidation layer.

This is not a criticism of general-purpose blockchains. It is an observation: what possibilities arise when financial infrastructure is designed from first principles, around markets rather than programmability.

Two different starting points, two different ending points.

Final opinion

This team was never aiming to build a better Binance. Their vision was simply too narrow.

Hyperliquid is actually built as a minimum viable technology stack for a financial operating system, and it is assembled in a uniquely structurally sound order.

Liquidation first. Assets second. Liquidity third. Leverage fourth. Probability fifth.

Each layer serves as a proof of concept for the layer below. Each HIP is a prerequisite, not a function.

The evidence lies in the order itself.

HIP-3 didn't follow HIP-2 because the team had a great idea for a permissionless perpetual contract. It followed closely because HIP-2 had already demonstrated that HyperCore natively solved the cold start problem.

HIP-4 did not follow HIP-3 because prediction markets were popular. It followed closely because HIP-3 had already subjected the clearing engine to large-scale stress tests simultaneously across dozens of assets with real funds.

This order itself is the best argument.

HyperCore can now be used for asset pricing, maintaining liquidity, expressing leverage, and settlement probabilities.

This is not a feature list pieced together by a fast-moving team over time. This is an architecture with a clear objective.

The destination is always HIP-4. However, four prerequisites are required to reach it.

That's all for now!