Table of Contents

ToggleWhen AI agents possess the ability to autonomously acquire data and conduct decision-making analysis, traditional investment analysis models on Wall Street are facing a fundamental transformation. Within 12 minutes of SpaceX submitting its S-1 filing, an AI agent completed a 226MB prospectus reading, purchased real-time market data via USDC on the Base blockchain, and generated an investment committee memorandum encompassing multi-faceted arguments, valuation models, and a risk matrix—all at a cost of only $1.87. This is not a demo, but a real-world paid API call record, signifying that automation tools are reshaping the way the financial analysis industry works.

An AI agent autonomously accomplished what would take an investment analyst team several days: reading 226MB of SpaceX S-1 documentation, purchasing real-time market data on the Base blockchain using USDC, and generating an investment committee memo encompassing multi-faceted arguments, valuation models, and a risk matrix—all at a cost of only $1.87. This isn't a demo; it's a real-world example of a paid API call. When AI agents can pay for data and make their own analytical decisions, the way Wall Street operates is being restructured.

An AI agent read through the 226MB SpaceX S-1 file submitted on Monday, purchased real-time market data using USDC on the Base blockchain, and then produced this investment committee memo within 12 minutes. Total cost: 6 paid API calls, $1.87 USDC, no API key required.

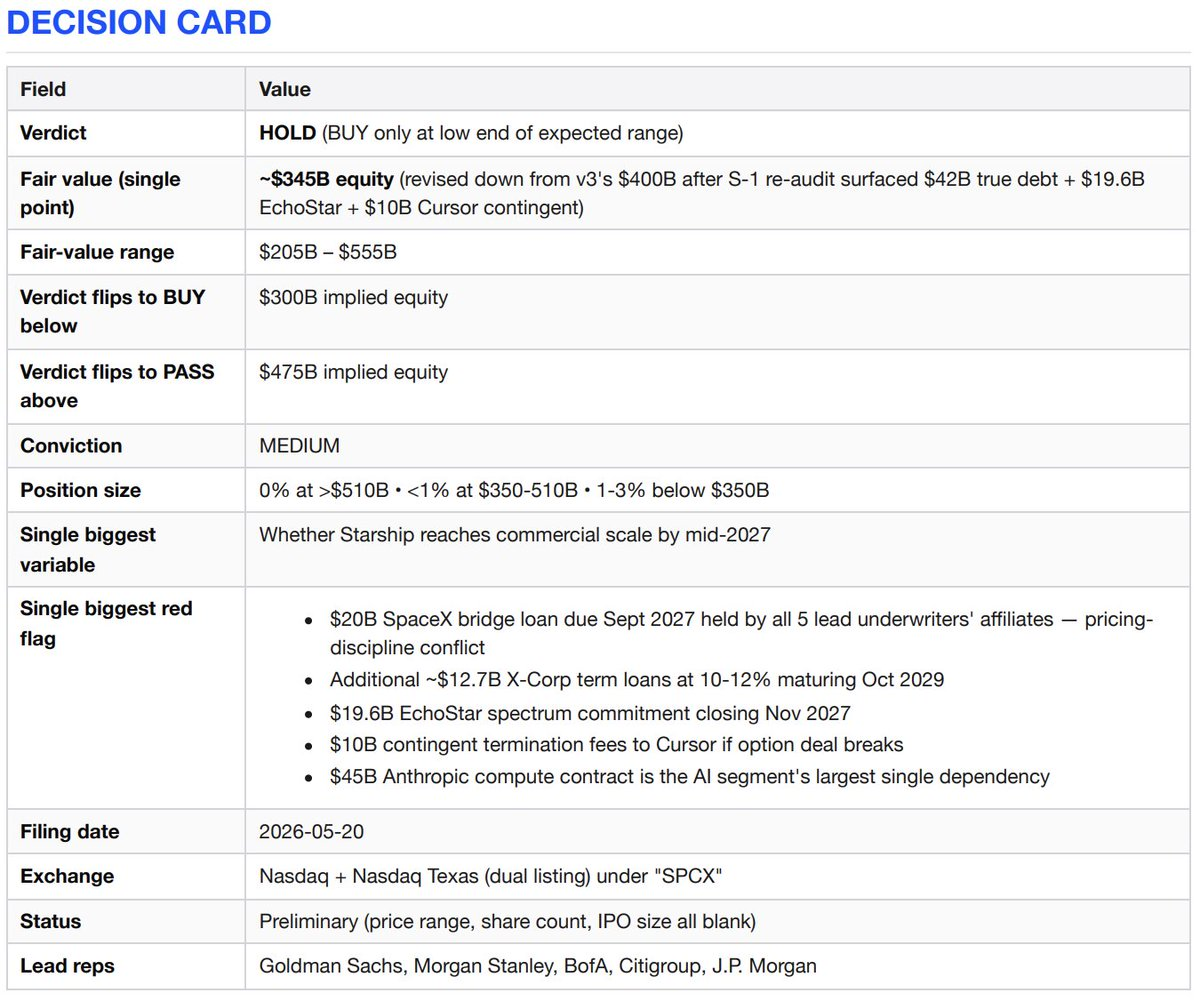

Decision Card (Conclusion = Hold and Wait)

Multiple arguments

SpaceX possesses three business advantages that competitors cannot replicate. First, a near-monopoly on commercial space access—accounting for 80% of global orbital launches since 2023, boasting a 99% Falcon mission success rate, and leading reusable technology by 10 years. Second, the world's only deployed low-Earth orbit broadband network—Starlink—has 10.3 million subscribers in 164 countries, a 49.8% year-over-year increase, with adjusted EBITDA reaching $7.2 billion. Third, since acquiring xAI in February 2026, it has become the only AI lab vertically integrated into the launch vehicle level, and will deploy orbital computing capabilities in the future. Regardless of the valuation method used, this is a generational asset.

Bearish Argument

Connectivity is real and profitable. But everything else is either burning through cash at an alarming rate—the AI division lost $6.4 billion in 2025 with $3.2 billion in revenue—or betting on Starship, which has completed 11 test flights but has yet to launch a payload into orbit. This IPO is partly a refinancing event. SpaceX took out a $20 billion bridge loan to acquire xAI, maturing in September 2027, and the bridge lender is the underwriter of this IPO. If the valuation exceeds $500 billion, you're paying for unrealized execution capabilities, corporate governance you have no say in, and a refinancing deal that the underwriters must successfully complete.

Investment Arguments

Starlink is a strong independent business. Projected revenue of $11.4 billion (+49.8%), operating income of $4.4 billion (+120%), and adjusted EBITDA of $7.2 billion (+86%) by 2025. It offers a high-priced subscription service with 10.3 million paying users.

SpaceX IPO: AI reads the prospectus in 12 minutes

Its launch operations are unparalleled. Since 2023, it has accounted for more than 80% of the global orbital mass, with a Falcon success rate of over 99% and the Falcon 9 first stage rocket having flown a maximum of 34 times.

Vertical integration is real and generates compound interest. Rocket → Satellite → Spectrum (EchoStar AWS-4/H band transaction has been approved by the FCC) → AI computing power (approximately 1GW from two COLOSSUS clusters).

Government dependence is a moat, not a risk. The primary launch provider for U.S. national security: 11 of the 12 national security space launches scheduled for 2025, and all 5 of NASA's crewed and cargo flights.

The option value of orbital AI computing power, planned for deployment in 2028. If Starship achieves even 50% of its established economics—a 99% reduction in launch costs—the reachable market will expand by an order of magnitude.

Counterargument

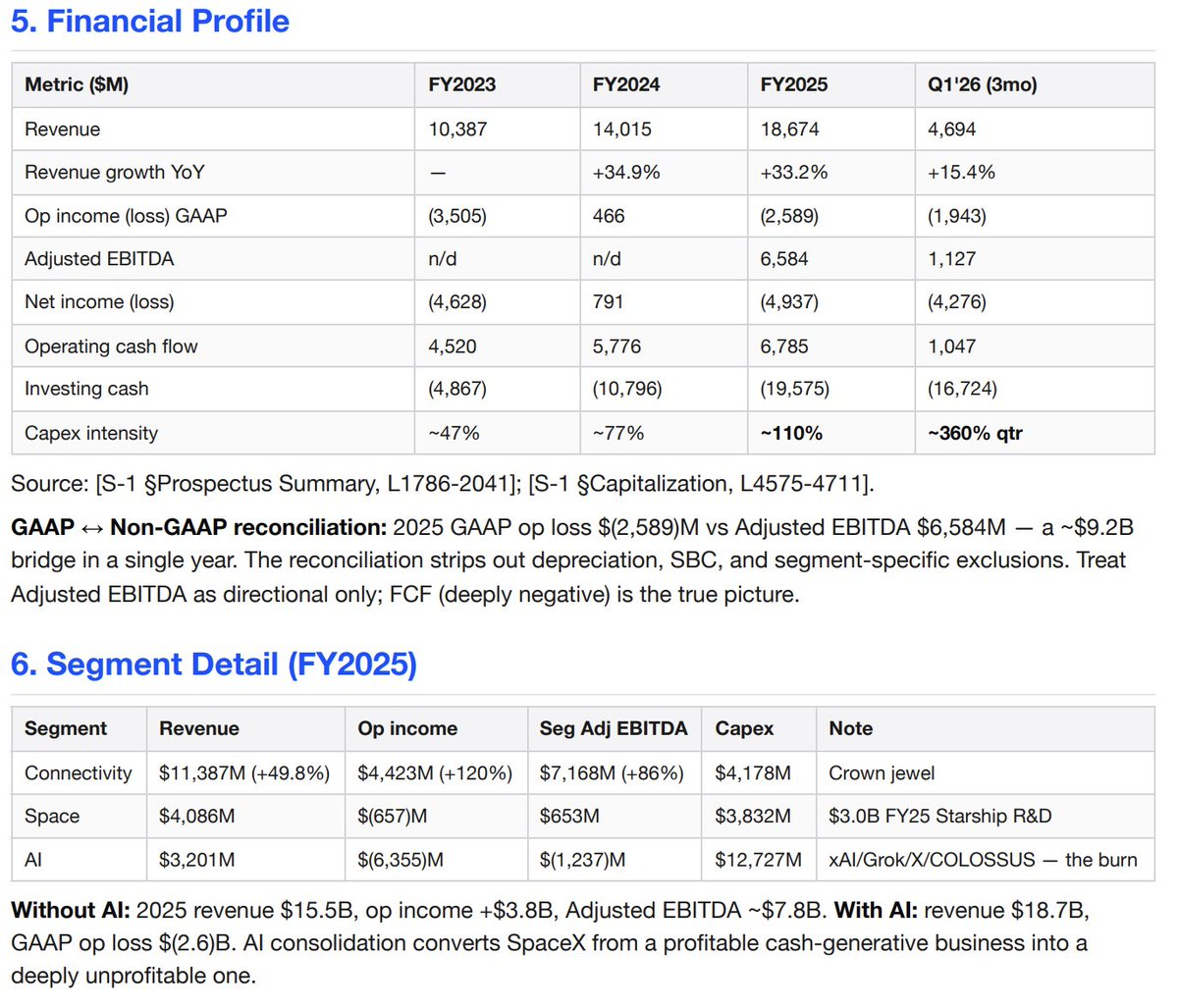

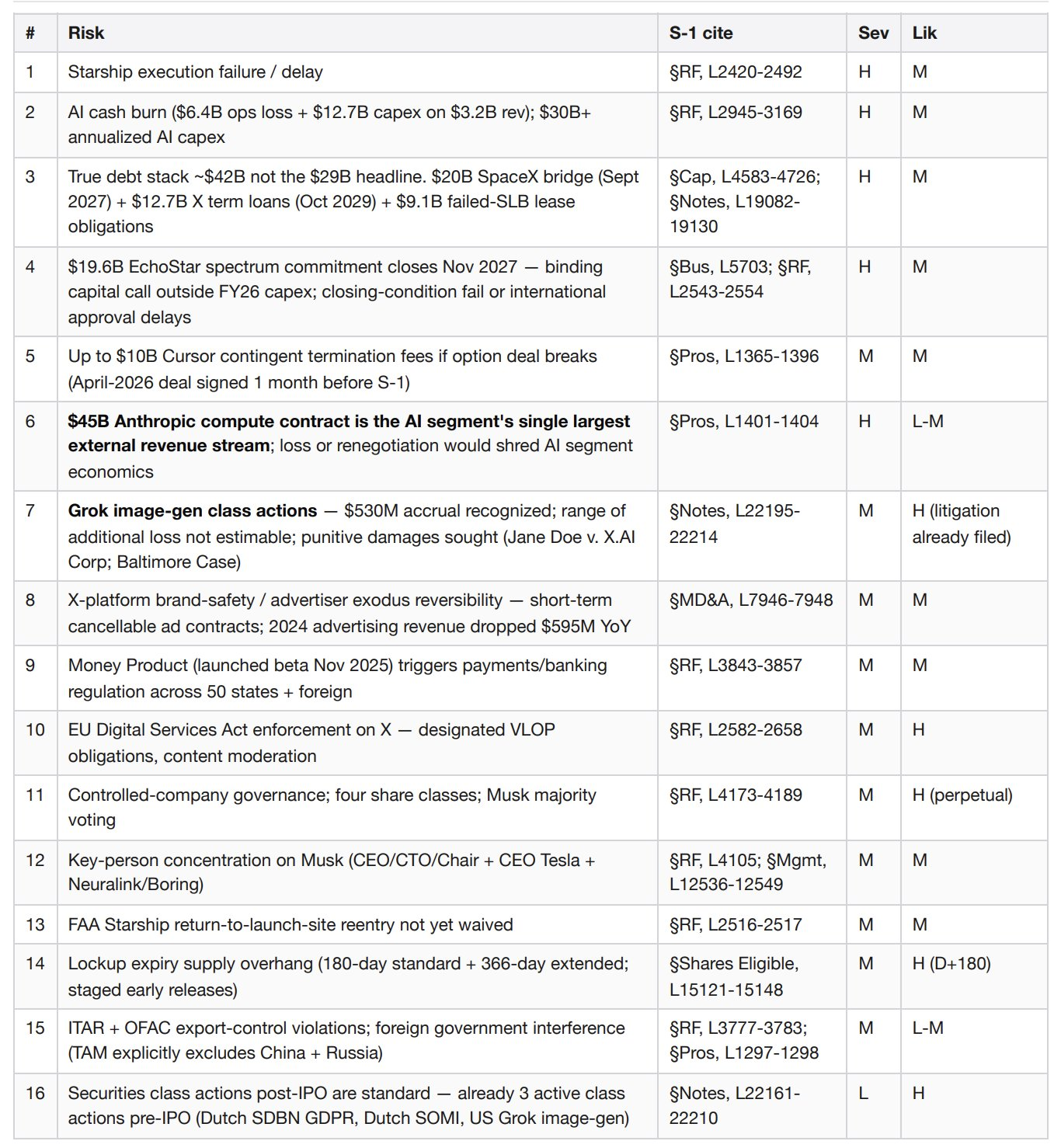

The AI division is a bottomless pit, burning through over $6 billion annually. In 2025: $3.2 billion in revenue versus an operating loss of $6.4 billion, adjusted EBITDA of -$1.2 billion, and capital expenditures of $12.7 billion. In Q1 2026 alone: revenue of $818 million versus an operating loss of $2.5 billion, and capital expenditures of $7.7 billion. Annualized AI capital expenditures now exceed $30 billion, while AI revenue is only $3.2 billion.

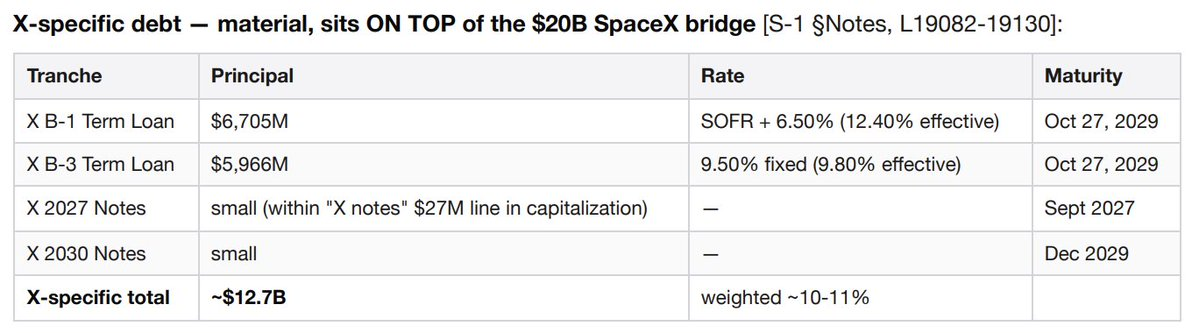

The actual debt size is approximately $42 billion, not the $29 billion figure in the headline. It comprises: approximately $20 billion in SpaceX bridge loans (maturing in September 2027), approximately $6.7 billion in SpaceX B-1 term loans and approximately $6 billion in SpaceX B-3 term loans (both maturing in October 2029, with effective interest rates of 10-12%), and approximately $9.1 billion in "other financing," including obligations arising from failed sale-leaseback agreements for AI infrastructure. X-related loans alone generate approximately $1.2-1.3 billion in interest expense annually, recorded within the AI division.

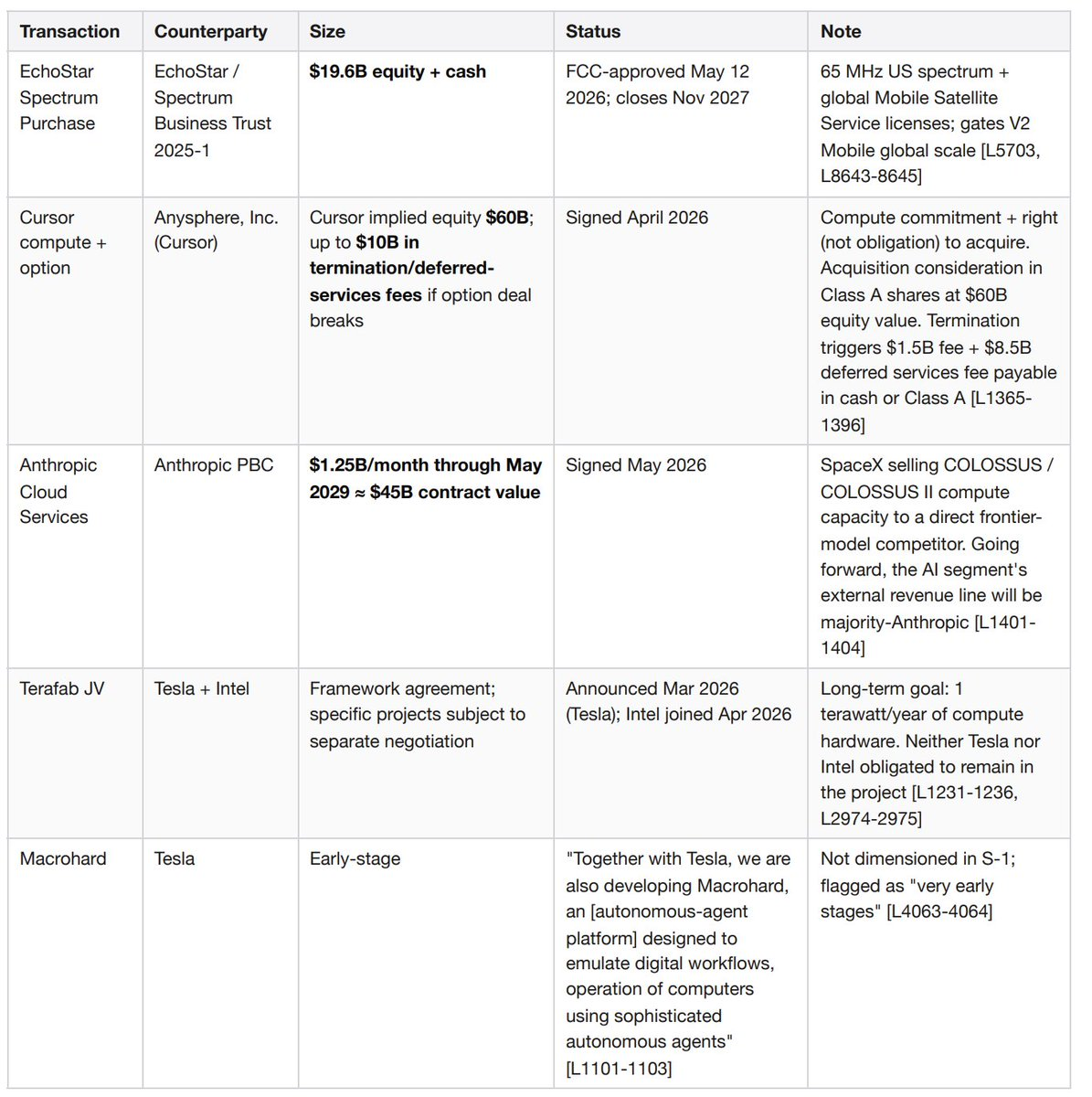

The $19.6 billion EchoStar spectrum commitment is set to be finalized in November 2027. This involves an equity-plus-cash deal for 65MHz of U.S. spectrum and a global mobile satellite service license. This is a binding capital commitment in addition to bridge loans and fiscal year 2026 capital expenditures.

The options agreement with Cursor could trigger a termination fee of up to $10 billion. SpaceX signed a computing power and options agreement with Anysphere (Cursor) in April 2026—one month before this S-1 filing—implying a $60 billion valuation for Cursor. If either party terminates the agreement, SpaceX will have to pay Cursor a $1.5 billion termination fee plus $8.5 billion in deferred service fees, payable in cash or Class A stock.

The $45 billion Anthropic contract is the largest single external revenue source for the AI division. A cloud services agreement signed in May 2026 stipulates that Anthropic will pay $1.25 billion per month until May 2029. SpaceX is selling its COLOSSUS computing power to a direct competitor, a leading modeling company, creating extreme counterparty concentration risk.

The balance sheet recognized $530 million in litigation reserves for the Grok Imaging Productions class-action lawsuits—Jane Doe v. X.AI (January 2026), Jane Doe 1 (March), and Baltimore (March). The plaintiffs are seeking compensatory, statutory, and punitive damages. The S-1 stipulation explicitly states that the extent of additional damages is incalculable.

Revenue growth slowed to 15.4% in Q1 2026 (US$4.69 billion compared to US$4.07 billion year-over-year), down from 33.2% for the full year of 2025.

Starlink surges: 10.3 million subscribers become its moat

SpaceX will be a controlled company with four classes of equity. Musk will hold a majority of the voting rights after the IPO. The company will rely on Nasdaq's controlled company exemption, exempting it from the requirements of the independent compensation committee and the independent nominating committee.

Adjusted EBITDA beautified by approximately $9 billion. Management's 2025 headline figure is $6.6 billion in "adjusted EBITDA," while GAAP operating loss is -$2.6 billion. Adjustments exclude depreciation, stock-based compensation, and segment-specific exclusions.

Company Profile

SpaceX (SEC CIK 0001181412) designs and operates reusable rockets, the world's largest LEO satellite constellation (approximately 9,600 broadband satellites plus approximately 650 direct-connect cell satellites), and—following its acquisition of xAI in February 2026—gigawatt-scale AI training infrastructure. It has three reporting segments: Space, Connectivity (10.3 million Starlink subscribers), and AI (Grok models, the X social platform with 550 million monthly active users, and the COLOSSUS/COLOSSUS II computing power cluster). 2025 revenue is projected at $18.7 billion; GAAP operating loss is $2.6 billion; cash on hand is $15.85 billion against $29.1 billion in long-term debt capitalized on the cover of the capitalization statement.

X (social platform) is a business unit, not a footnote.

The business chain deserves to be retraced. SpaceX acquired xAI in February 2026. xAI acquired X Holdings in March 2025. X Holdings acquired Twitter in October 2022. Result: Twitter/X is now integrated into SpaceX's AI division, with its own balance sheet projects, its own litigation, and its own debt structure.

Scale. Supported 1.3 billion accounts and 550 million monthly active users over the past 12 months (up from 520 million in December 2025), with 350 million posts per day. Of these monthly active users, 117 million use Grok features—X is the primary distribution pipeline for this model. Money products (payments, banking, financial services) launched in beta in November 2025 and are progressing towards full availability. X Ads Manager will begin phased rollout in April 2026.

Financial Contribution. The AI division's revenue in 2023-2024 came almost entirely from X—advertising, X Premium subscriptions, and data licensing. In 2024 alone, advertising revenue declined by $595 million year-over-year due to "X losing advertising partners," partially offset by a $157 million increase in X Premium subscription revenue and a $90 million increase in data licensing revenue.

Including the $20 billion SpaceX bridge loan (to September 2027) and the $9.1 billion “other financing” item, the total long-term debt is approximately $42 billion—not the $29 billion headline figure on the capitalization cover.

X-specific risks not present in SpaceX's other businesses. Enforcement of the EU Digital Services Act on mega-platforms. The reversibility of advertiser brand security on short-term, easily cancelable advertising contracts—the mass exodus of 2024 could be repeated within a single news cycle. Money products triggering payment/money transfer/banking regulations in all 50 US states and every foreign jurisdiction. Reversals of content audit policies could simultaneously trigger advertiser suspensions and user migrations.

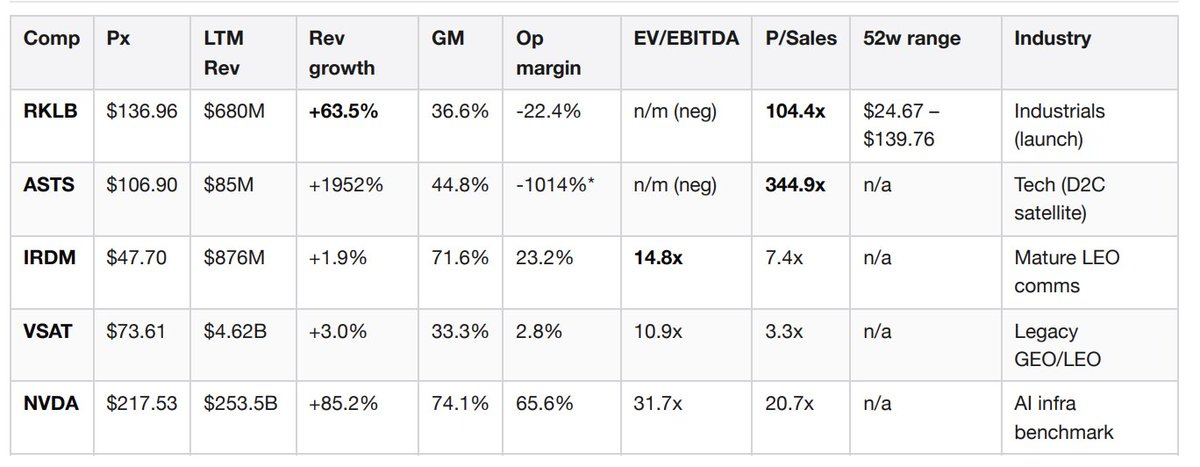

Market position – real-time comparable data

This comparison table was assembled on-the-fly during the analysis, using batch fundamental data for all five comparable companies obtained by paying $0.10 to Jintel's GraphQL endpoint. No Bloomberg terminal or FactSet contract was required.

Debt default: $42 billion in bridge loans mature

ASTS' operating profit margin reflects significant pre-revenue investments. Source: Obtained from Jintel entitiesByTickers via Base on-chain x402, retrieved on 2026-05-22.

Let's analyze the comparison groups. Rocket Lab's 104x P/S ratio is the closest narrative benchmark—investors are willing to pay extremely high multiples for scalable, reusable launches plus the value of low-Earth orbit options, even with negative profit margins. SpaceX should have a higher multiple than RKLB, but blindly applying 104x to SpaceX's $11.4 billion revenue from its connectivity business alone to equate to a $1.2 trillion equity value is not anchored to anything. AST SpaceMobile's 345x is purely a pre-revenue narrative valuation, serving only as a ceiling reference for the value of direct-connect phone options. Iridium's 7.4x sales and 14.8x EBITDA represent what a mature, profitable LEO communications business looks like—applying 7.4x to Starlink's $11.4 billion gives an $84 billion value for Starlink's standalone business (a bearish anchor). NVIDIA's 31.7x EV/EBITDA corresponds to 85% revenue growth, which is the level the AI division needs to grow to justify a fundamentally based valuation. We haven't reached that point yet.

A noteworthy signal. Rocket Lab filed its 424B5 supplemental prospectus on May 20, 2026—the same day SpaceX unveiled the S-1. RKLB's issuance of secondary shares during SpaceX's news cycle suggests management believes the IPO window is open and competitive supply pressure is imminent.

Pending major transactions and contingent obligations

These four items are all important and overlap. Two of them must be signed within 60 days prior to this S-1 filing.

Why this matters for valuation. A clear “adjusted net obligation” perspective is: $42 billion in total debt plus $19.6 billion in EchoStar commitments plus up to $10 billion in contingent liabilities to Cursor, minus $15.85 billion in cash on hand, equals approximately $55 billion in net obligations, not including any IPO proceeds. This is three to four times the figure obtained from a simple read of the capitalization cover page, substantially altering the short-selling scenario.

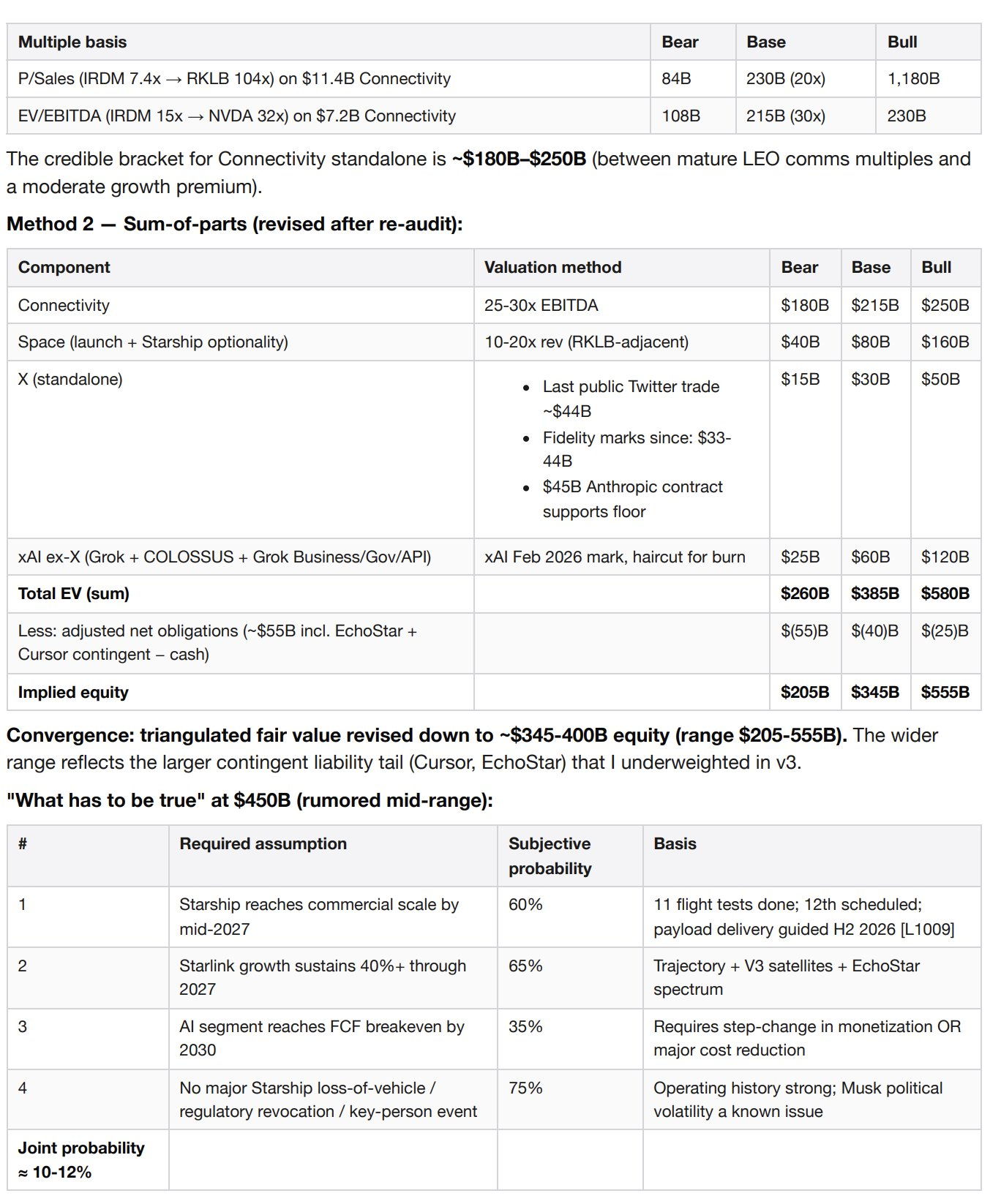

Valuation

Method 1 – Based on the independent trading multiple of the connected segment, since it is the only segment with positive independent economic benefits.

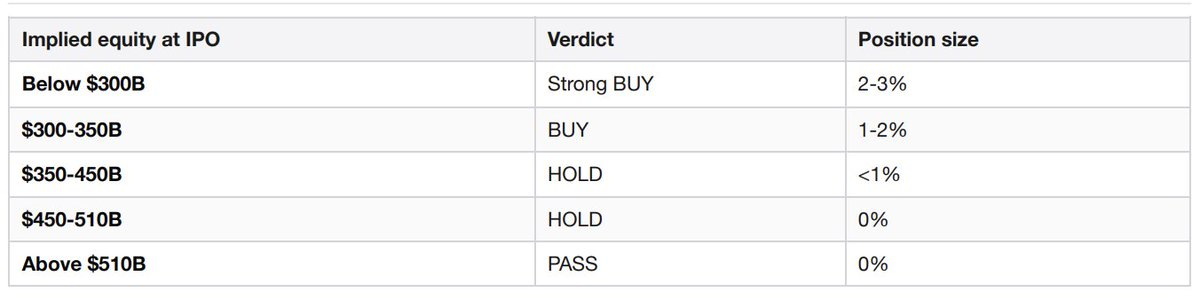

Position size tiers

Major risks (severity × likelihood)

Underwriter Conflict of Interest

This point, deeply embedded in the underwriting process and rarely covered in news reports, is crucial. The affiliates of the five lead underwriters (Goldman Sachs, Morgan Stanley, Bank of America, Citigroup, and JPMorgan Chase) and the five additional bookrunners (Barclays, Deutsche Bank, Royal Bank of Canada, UBS, and Wells Fargo) are all lenders on the $20 billion SpaceX bridge loan, and they are now pricing the IPO to refinance that loan. Morgan Stanley also served as an advisor to SpaceX on its acquisition of xAI (funded by the bridge loan). The underwriting syndicate has a direct financial interest in maximizing the amount raised in the IPO. This should keep the investment committee vigilant regarding pricing discipline.

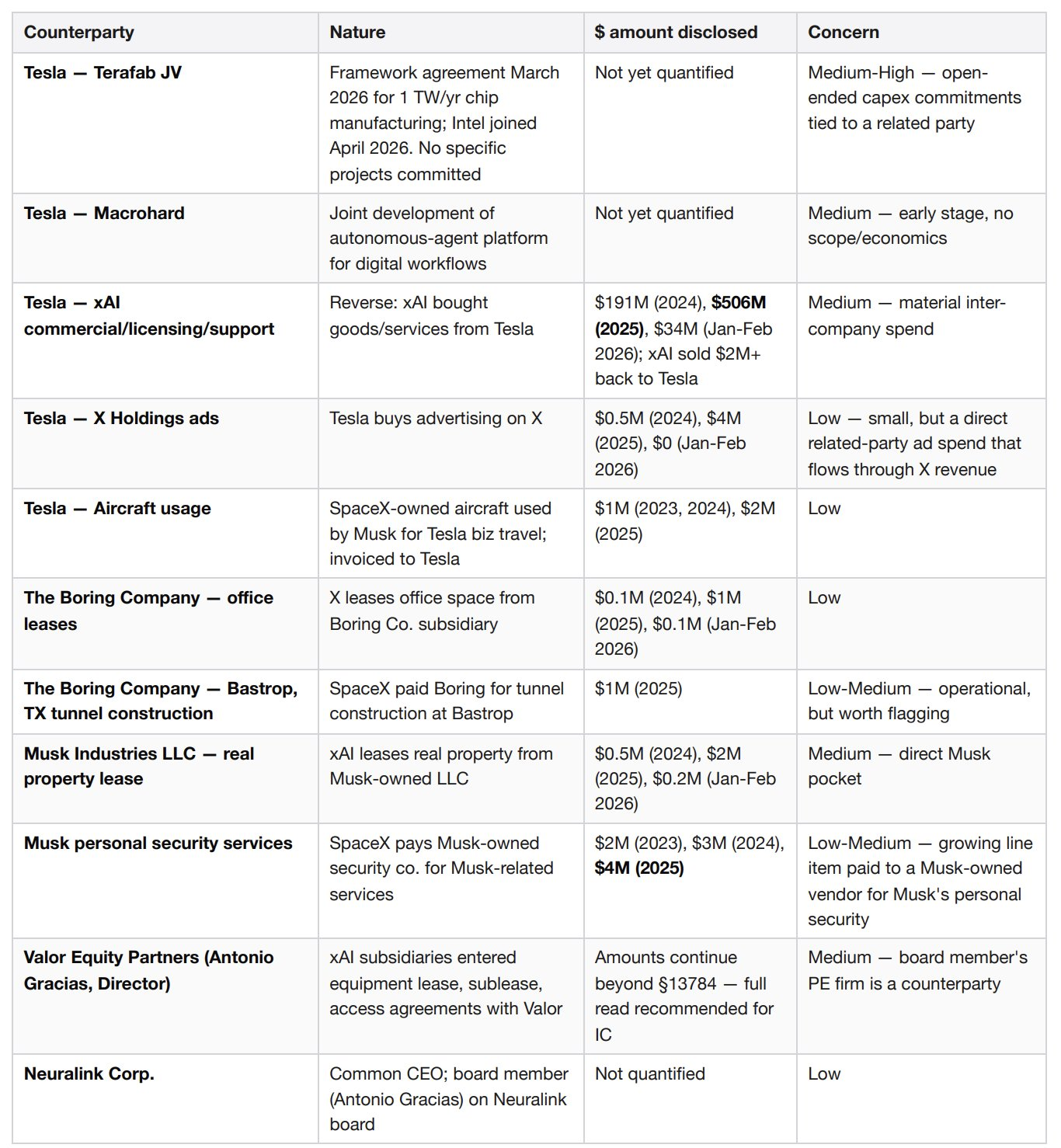

Related party density

Lawsuit collapses: Grok class action lawsuit prepares $530 million

None of these factors individually seem alarming. What is worrying is the density—Musk's network of entities has at least nine different financial contacts with SpaceX. Corporate governance committees typically review one or two such relationships. This adds an order of magnitude.

Decision trigger point

Upgrade to overweight if the transaction is priced at $350 billion or less of implied equity, and Starship achieves commercial payload delivery in the second half of 2026 as per guidance, and connected business revenue grows by more than 40% year-over-year in Q2 2026.

If the transaction price exceeds $510 billion, or if a Starship spacecraft loss event causes the V3 satellite deployment to be delayed until after 2027, or if the AI division's cash burn accelerates to an annualized operating loss of over $8 billion in Q2-Q3 of 2026, or if the FAA imposes a long-term grounding on Starship, then it will be downgraded to abandonment.

First 180-day plus multi-year observation list

D+1: First-day price increase benchmark compared to comparable IPOs

D+30: First Quarterly Financial Report (Q2 2026) – Triggers early release of locked-up shares (20% released immediately, and an additional 10% released if the share price is 30% higher than the offering price).

D+70, +90, +105, +120, +135: Early release of locked tiers in phases, 7% each.

D+90: Quiet period ends, sell-side analysts initiate coverage.

D+180: All standard echelons locked out upon expiration.

Second half of 2026: Starship guides commercial payload delivery

X Platform Integration: AI Division Merged into Twitter Assets

2026 Q2-Q3: Procedural milestone in Grok's imaging output class-action lawsuit (focus on whether the $530 million reserve will increase)

April 2027: Cursor Option Agreement One-Year Anniversary – Pay Attention to Exercise or Termination Signals

September 2027: SpaceX's $20 billion bridge loan matures (must be refinanced or repaid).

November 2027: $19.6 billion EchoStar spectrum deal completed – V2 Mobile's global launch constrained by this.

May 2029: The $45 billion Anthropic computing power contract ends; renewal terms will define the economics of the AI division for years to come.

October 2029: A total of $12.7 billion in X Company B-1 and B-3 term loans mature.

source

SpaceX S-1, SEC Registration No. 0001628280-26-036936, Submission Date: 2026-05-20

Real-time comparable fundamentals via Jintel GraphQL entitiesByTickers, Base on-chain x402, retrieved on 2026-05-22

The SEC comprehensive profile was retrieved via x402helper /companies/profile for RKLB, IRDM, and VSAT purposes, on 2026-05-22.

Through Parallel Search's industry IPO background, Base on-chain x402, search date 2026-05-22

Four Scenarios for SpaceX's IPO – Acadian Asset Management

Produced by the IPO analytics package on agentic.market. 6 paid x402 calls. $1.87 USDC on the Base chain. No API key required. No registration required. Pay-per-request.

A Bloomberg terminal seat costs $24,000 per year. This memo demonstrates what agents can now produce when they can pay for their own data.

Related reports

Related reports