This may be the most regulatory-friendly era for the crypto industry right now.

Written by: Mahe, Foresight News

On May 29, the U.S. Commodity Futures Trading Commission (CFTC) made two landmark moves on the same day: formally approving the Bitcoin perpetual contract submitted by KalshiEX, LLC (Kalshi). In addition, the CFTC issued a letter to Coinbase refusing enforcement action, allowing Coinbase to offer certain perpetual futures products to U.S. customers through its subsidiary.

The CFTC has released a "Policy Statement on the Listing of Perpetual Contracts," providing a clear framework for the listing of perpetual products in regulated markets. This series of actions signifies a crucial step forward for US cryptocurrency derivatives regulation, moving from a long-standing gray area towards a truly compliant path for perpetual contracts.

Kalshi and Coinbase both received regulatory approval

The CFTC review determined that Kalshi's Bitcoin perpetual contracts complied with the Commodity Exchange Act and the core principles of the Designated Contract Market (DCM), including the depth and liquidity of the underlying Bitcoin spot market, contract design, and risk management capabilities. The approval order requires Kalshi to continue operating in compliance and clarifies that the perpetual contract design "may not necessarily be applicable to all asset classes," encouraging other market participants to communicate with regulators and submit perpetual products for different underlying assets through the formal approval process.

In addition, the CFTC's Market Participants Division issued an explanatory letter and a no-action letter to registered futures commission broker Coinbase Financial Markets (CFM), allowing it to offer U.S. users crypto options and perpetual contracts listed on its affiliated foreign exchange, Deribit FZE. The letter confirms that these perpetual contracts can be classified as foreign futures under CFTC Rule 30.1. Under certain conditions, the CFTC will not recommend enforcement action against CFM for transferring clients' digital commodities and payment stablecoins to its foreign brokerage affiliates for margin purposes, and such affiliates may exercise reuse rights over these client assets.

Previously, the US market lacked truly perpetual contracts (without an expiration date). Coinbase Derivatives launched a self-certified "perpetual-style" futures contract (with a contract term of up to 5 years) in July 2025, aiming to simulate the characteristics of a perpetual economy, but still retaining an expiration date. Today's approval and lack of enforcement action provide a dual compliance path for "true perpetuality": Kalshi is pursuing the DCM standard futures route, while Coinbase is reaching US customers through foreign futures plus crypto collateral.

Mike Selig

In his statement, CFTC Chairman Mike Selig emphasized that perpetual contracts are an important risk management and price discovery tool in the global crypto asset market. The launch of true perpetual contracts in the United States is a significant step towards making the US a global crypto hub. He pointed out that the CFTC has established a viable regulatory framework for crypto asset perpetual contracts and will maintain market order by limiting excessive leverage, market volatility, and systemic risk.

Selig also acknowledged that the CFTC's current regulatory stance has not yet formed formal, permanent rules, and future policies may still be adjusted as the regulatory environment changes.

A trillion-dollar market cake

So why hasn't the CFTC approved a true Bitcoin perpetual contract before?

Perpetual contracts are considered a "new" product within the traditional commodity futures framework. They lack an expiration date and final delivery, which conflicts with the conventional understanding of traditional futures under the Commodity Exchange Act that they "must have an expiration date and a settlement mechanism." The CFTC has internally debated whether to classify them as futures or swaps, as different classifications would bring entirely different regulatory requirements (including clearing, margin requirements, and reporting obligations). This ambiguity in their legal status makes it difficult for platforms to achieve a stable compliance path.

In addition, its high leverage and speculative nature, as well as concerns about market manipulation, have always made the CFTC take a cautious approach.

BTCPERP is a perpetual contract that tracks the spot price of Bitcoin. It has no fixed expiration date and settles between long and short positions periodically through a funding rate mechanism to maintain a close anchor between the contract price and the spot price.

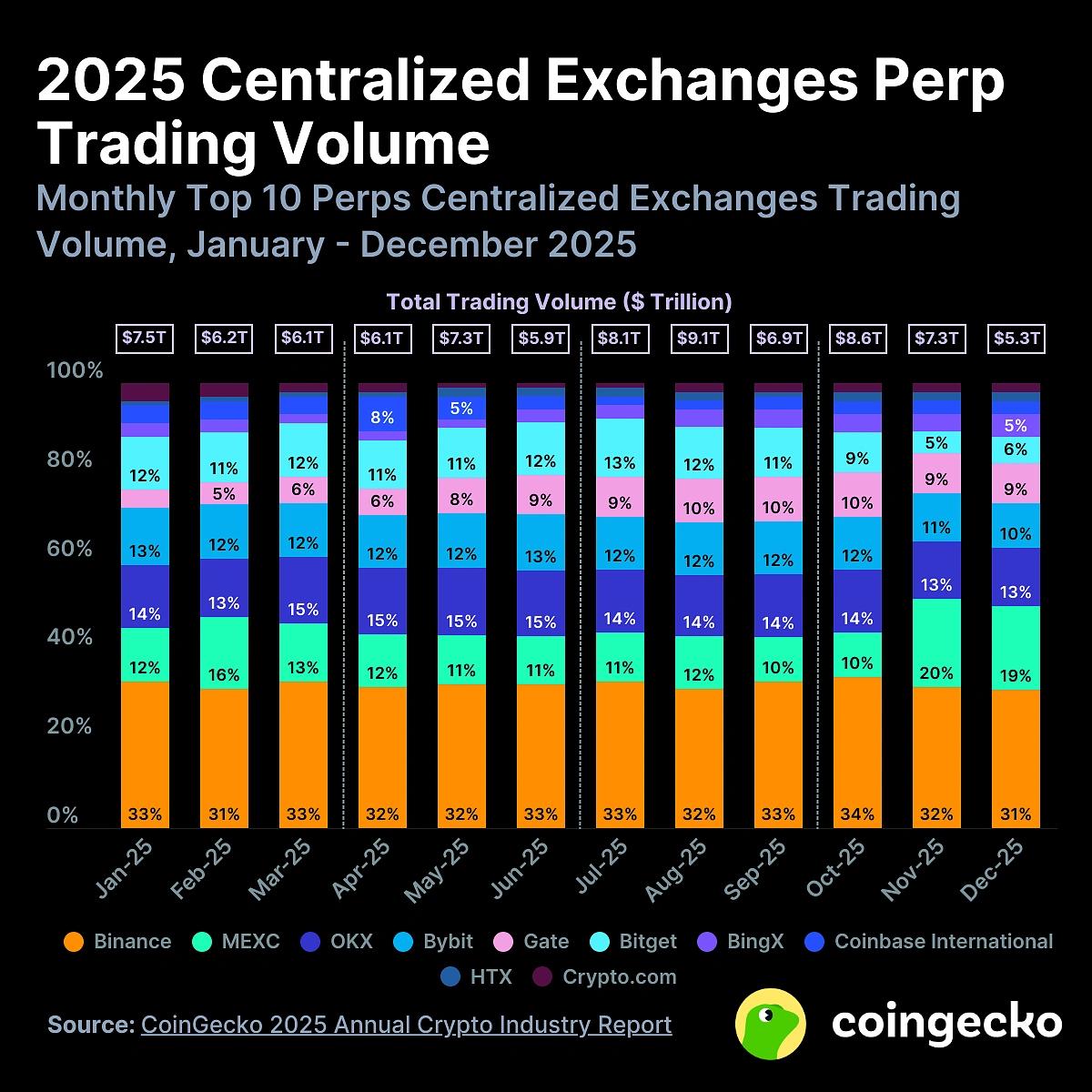

In the global crypto derivatives market, perpetual contracts have long held a dominant position. According to CoinGecko's 2025 annual report, the cumulative trading volume of crypto derivatives on centralized exchanges worldwide was approximately $85.7 trillion, with perpetual contracts accounting for about 78%. In 2025, the cumulative trading volume of perpetual contracts on decentralized exchanges was approximately $6.7 trillion (a year-on-year increase of 346%).

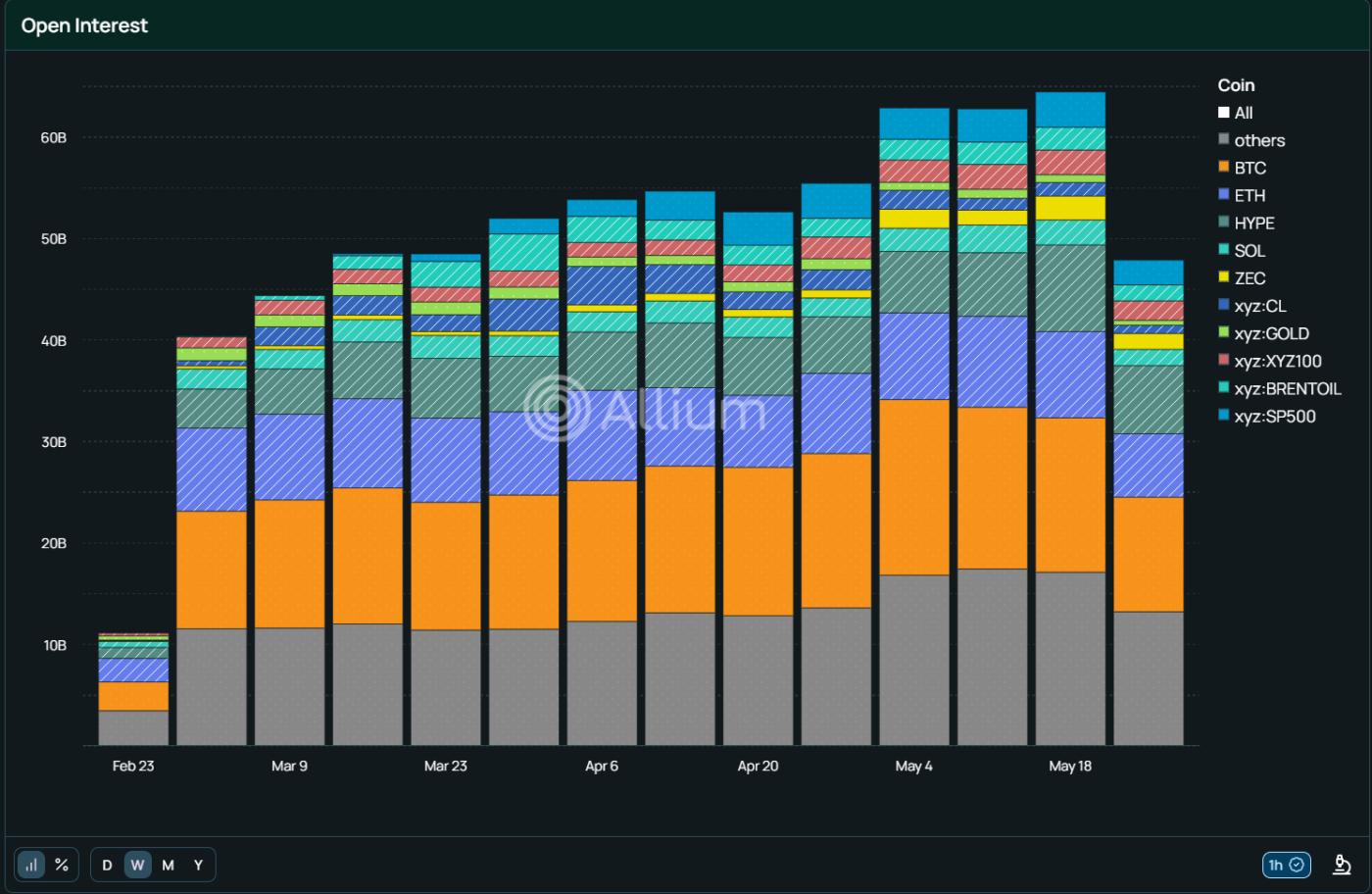

Ironically, while regulatory traditionalists in Washington are embroiled in compliance debates, offshore decentralized perpetual platforms, exemplified by Hyperliquid, have already extended their reach to the S&P 500, crude oil, and gold through on-chain synthetic assets. As of the end of May 2026, Hyperliquid's perpetual trading volume had already reached $586.12 billion, and according to Allium on-chain data, Hyperliquid's total derivatives holdings also reached a record high of nearly $60 billion at the end of May, with an increasing number of individuals and institutions choosing to trade on the platform.

Hyperliquid latest holdings

This unprecedented approval by the CFTC is not only a compromise with the crypto market, but also a necessary "onshore defense" by the compliance world in the face of the innovative demand for "perpetual assets" from offshore entities.

In contrast, while regulated Bitcoin futures such as those from CME provide institutions with stable hedging tools, their leverage and trading characteristics differ from the perpetual products preferred by retail/professional traders.

This CFTC approval undoubtedly opens up a new battleground for Kalshi in the prediction market, blurring the lines between the prediction market and the traditional crypto derivatives market. Kalshi can leverage compliant event-based settlement logic to disrupt the perpetual liquidity pools that previously belonged to centralized exchanges. For Coinbase, the trading volume and revenue of its perpetual contracts will likely be reflected in its next financial report.

Previously, US traders primarily relied on offshore platforms, facing custody risks, regulatory uncertainty, and barriers to institutional entry. This regulatory policy release, supporting crypto collateral, will attract traditional institutions such as hedge funds and family offices. Traders can hold leveraged positions to hedge spot markets long-term, eliminating the need for frequent trading; simultaneously, it will attract some offshore traffic back to compliant US channels.

Meanwhile, the approvals for Kalshi and Coinbase will stimulate the accelerated rollout of other products, such as ETH perpetual bonds, forming a more complete crypto derivatives matrix. In the long run, this policy may enhance the US's competitiveness in the global crypto derivatives ecosystem, attracting more capital, talent, and infrastructure, creating favorable conditions for the deep integration of crypto assets and traditional finance.

This may be the most regulatory-friendly era for the crypto industry right now.