No conflict of interest: I did not receive any payment for this article.

One of the most surprising stories in the crypto industry over the past two years comes from a small team in Singapore that has long had only about a dozen employees.

This company, founded just three years ago and valued at tens of billions of dollars, has never received a single penny of VC funding. Last year, its 11 employees generated over $900 million in profit, making it one of the most profitable companies per employee on Earth.

The founder who doesn't attend meetings, doesn't use Twitter, and doesn't speak out.

The story of Hyperliquid revolves almost entirely around one person—Jeff Yan (X account @chameleon_jeff).

Jeff's parents are Chinese immigrants. They divorced when he was in the third grade of elementary school, and he was raised by his mother, who was an accountant. His mother often worked overtime during tax season and frequently reminded him that "there will always be someone better than you." Jeff represented the United States in the International Physics Olympiad, winning a silver medal in Estonia in 2012 and a gold medal in Denmark in 2013.

He graduated from Harvard with a degree in Computer Science in 2017 and then worked as an algorithm developer at the high-frequency trading firm Hudson River Trading. In early 2020, he turned to the crypto space, founding the market maker Chameleon Trading, and eventually partnered with others to create Hyperliquid.

The name Chameleon comes from his high school gaming ID and his fascination with chameleons. He genuinely admires chameleons, explaining on a podcast that their eyes can move independently in different directions, "the front two toes point forward and the hind three toes point backward," and they possess powerful, ejector-like tongues, making them seem like "aliens on Earth."

Before Hyperliquid, Jeff lived in Puerto Rico and ran Chameleon Trading, one of the largest anonymous trading businesses in the crypto space, almost single-handedly. In late 2019, he moved to Puerto Rico and started market making with $10,000. In two and a half years, the fund grew by several thousand percentage points annually, allowing him to achieve financial freedom at the age of 27.

The founder's personal style is quite extreme. Jeff is not driven by money, lives a minimalist life, wears the same clothes every day, cuts his own hair to save time, works at least 14 hours a day, sometimes up to 100 hours a week, and believes that most people are "generally too soft." As his public exposure as the founder of Hyperliquid increased, he began to take strict security measures after being followed into his apartment elevator, including moving, hiring bodyguards, and being accompanied by two private security guards when going out.

According to a senior crypto executive who knows both Jeff and SBF, Yan's image is more refined, professional, and genuine—"Jeff got a haircut, SBF didn't," and "SBF's shorts were too long and didn't fit properly, while Jeff looked clean and sharp." This contrast between his appearance and behavior and that of the FTX era has become part of the Hyperliquid narrative.

Jeff, founder of Hyperliquid

predecessor

Jeff's earliest foray into prediction markets was in April 2018. Influenced by the rise of crypto and Ethereum, he co-founded Deaux, a blockchain-based prediction market, within the Binance Labs incubator. The project attempted a design of off-chain matching plus on-chain settlement, but ultimately failed to attract users, with only about 100 users, and eventually shut down.

What truly made him his first fortune was Chameleon. In May 2023, Yan put Chameleon's strategies, which had been validated over many years, into an on-chain vault called HLP (Hyperliquidity Provider). Users could deposit as little as $10 or as much as $10 million, with no management fees or performance sharing. The vault ran automated strategies, and every dollar of profit went entirely to the depositors. All accounts were on-chain—if FTX had built it this way back then, Alameda's hole would have been known to the whole world.

HLP is key to understanding Hyperliquid. It provides liquidity to exchanges while offering ordinary users a zero-fee "high-frequency strategy entry point".

An early user described it as the first time in history that ordinary people could invest in high-frequency trading strategies at zero cost.

"I was willing to pay Jeff a 2% management fee plus a 50% performance share to get into this strategy."

Starting in the second half of 2023, users traded on the platform and accumulated points weekly. The point calculation rules remained confidential, and iliensinc announced the weekly points every Friday. Community members gathered on Discord each week to compare their gains.

Jeff later stated that "rewarding real users is key," and the points program "may have reduced the proportion of bots from 99% to 20%."

In January 2024, Yan released a four-line manifesto.

No investors.

No paid market makers.

No fees to the development team.

No insiders.

The project's neutral stance has been formally established. The HYPE token airdrop was completed on November 29th, with the team's portion unlocked over time, and no shares distributed to investors.

How did "no venture capital" become a product strategy?

Hyperliquid's decision to reject venture capital (VC) funding was a well-thought-out strategy. Yan and his team decided against seeking VC funding, having already earned a substantial amount of money from their crypto trading business. Yan covered the costs himself, believing that "if you want to build a truly trustworthy and neutral platform that anyone can build on, an important principle is that there can be no insiders."

"We raised the funds ourselves; we didn't need any financing at all, so the decision was very simple."

This choice had a subsequent effect: because no share was reserved for VCs, the team was able to distribute almost all of the 31% genesis share to real users. When the platform launched HYPE, 31% of the supply was directly allocated to users based on transaction activity, making it one of the most user-centric allocations in crypto history; the remaining allocation was distributed as follows: 38.88% for future community rewards, 23.8% for core contributors, 6% for the foundation, 0.3% for community funding, and a very small amount for protocol upgrades.

Jeff decided not to sell the equity to the VC, so the VC could not demand a preferred share, thus ensuring the realization of this distribution structure.

CEX Experience × DEX Transparency (The Boring Technical Part)

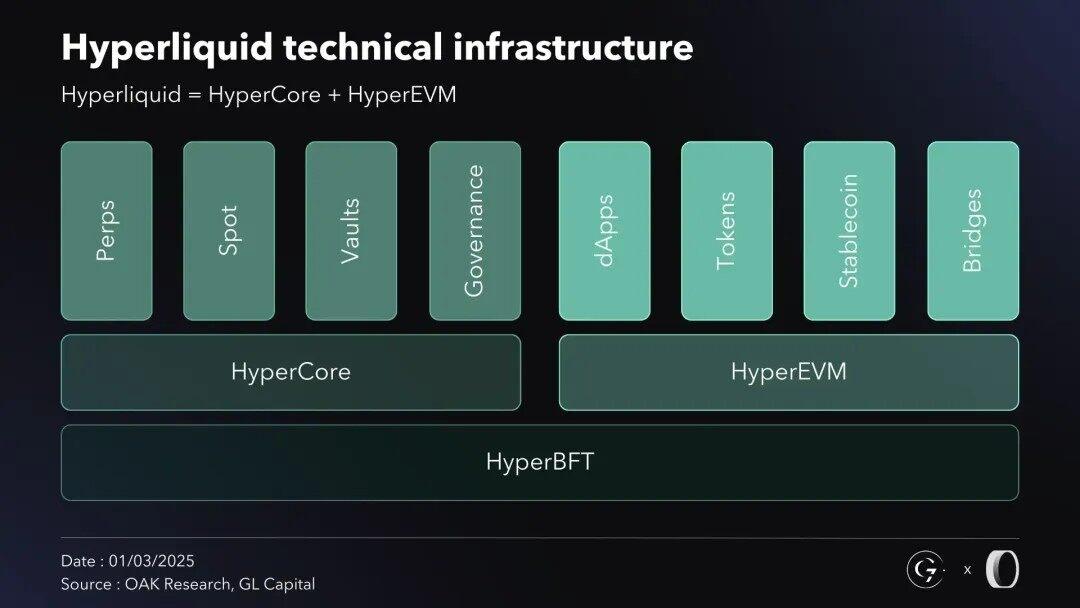

Hyperliquid is a standalone Layer 1 architecture designed specifically for transactions, independent of ecosystems such as Ethereum or Solana.

The network is protected by HyperBFT. This is a BFT protocol designed from scratch for high latency and high throughput, and can tolerate malicious nodes with no more than two-thirds of the staked amount.

HyperBFT supports approximately 200,000 transactions per second with a block time of 0.07 seconds. Holders delegate their HYPE tokens to validators, from whom the system selects 24 active validators based on their staked amount. Each round of transactions requires a quorum of more than two-thirds of the staked tokens, and a 7-day unstaking queue is used to prevent large-scale consensus attacks.

The blockchain itself is divided into two layers. The complete execution state, including HyperCore and HyperEVM, is protected by HyperBFT. Every order, cancellation, execution, and settlement is completed on-chain and has one-block finality. Hyperliquid adopts a non-custodial model, meaning the platform does not manage user funds. It is best known for its perpetual and spot trading of cryptocurrencies, stocks, commodities, and forex, and users can also lend, issue, and transfer assets. HyperEVM is an Ethereum-compatible execution layer that allows users and developers to build applications using smart contracts.

HyperEVM allows DeFi applications deployed by external developers to directly connect to Hyperliquid's on-chain liquidity and order book, transforming the exchange into an underlying infrastructure that other projects can overlay, creating an open ecosystem platform. Launched on February 18, 2025, HyperEVM enables EVM smart contracts to directly access native trading liquidity without the need for cross-chain bridges.

The matching mechanism itself is designed to run backwards.

Jeff discovered a common problem: high-frequency traders use bots to quickly take orders placed by market makers, forcing market makers to widen spreads to protect themselves, ultimately resulting in higher costs for ordinary users.

Hyperliquid addresses this issue by lowering the priority of fast order takers, giving market makers a fair chance to update quotes and resulting in narrower spreads.

The matching engine uses a price-time priority principle and allows special orders such as cancel-or-flip or post-only orders to take precedence over ordinary orders under certain conditions, ensuring that market makers can adjust their quotes without being overtaken by faster traders.

Hyperliquid Deep Dive: Understand HYPE and HLP Model

Hyperliquid Deep Dive: Understand HYPE and HLP Model

The largest airdrop that has been repeatedly mentioned

The circulating supply of HYPE is 222 million, with a total supply of 1 billion; the FDV at the current price is approximately $60.27 billion; the allocation is as follows: 38.89% for future release and community rewards, 31.00% for genesis distribution, 23.80% for core contributors, 6.00% for the Hyper Foundation budget, 0.30% for community grants, and 0.01% for HIP-2 Hyperliquidity.

The November 2024 airdrop distributed approximately 310 million HYPE tokens, equivalent to 31% of the total supply, making it one of the largest airdrops in crypto history in terms of both absolute quantity and dollar value distributed to real users.

The airdrop was completed on November 29, 2024, distributing HYPE to over 90,000 eligible users, a stark contrast to many projects that give away large amounts of tokens to venture capitalists.

A portion of the core contributors' tokens are subject to a lock-up arrangement. Over 61% of the HYPE supply remains locked; approximately 310 million HYPE were immediately distributed to early protocol participants and community members at genesis, with approximately 237 million reserved for core contributors, subject to a one-year cliff period plus a 24-month unlocking schedule.

Most allocations adopt a cliff-style release mechanism, with the entire unlocking schedule extending to 2027. The next unlock will take place on June 6, 2026, for core contributors.

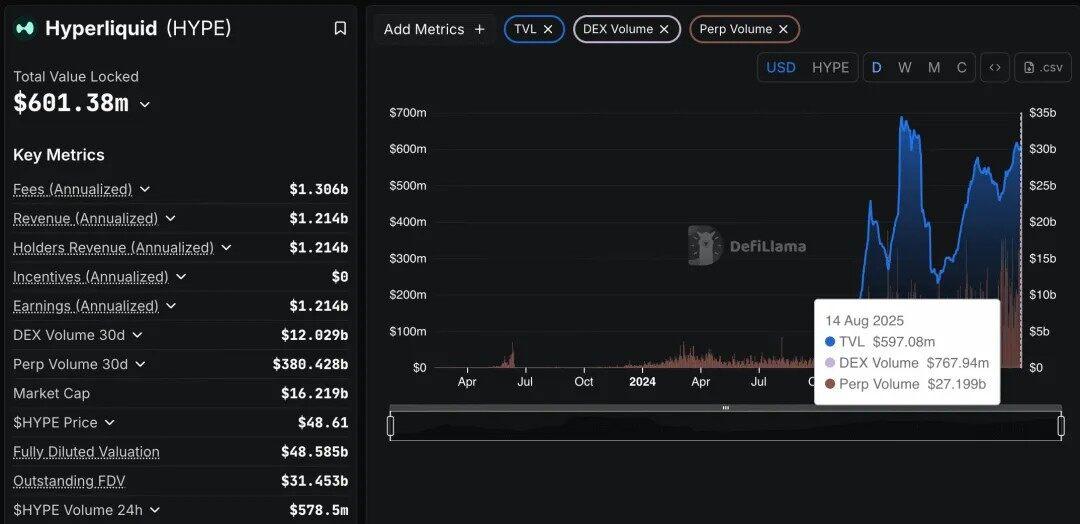

The most crucial design element is the buyback mechanism. Hyperliquid uses 99% of its transaction fees to buy back HYPE, driving the token above $62. This buyback is an on-chain mechanism that is automatically executed block by block, converting transaction fees into HYPE for purchases, unaffected by market conditions. Since its launch, the protocol has generated over $1.16 billion in revenue, almost all of which has been used to buy back its own tokens, including $316.8 million worth of HYPE in the third quarter of 2025 alone.

This structure creates sustained buying pressure beneath the token; the underlying business remains strong, and Hyperliquid has become one of the leading decentralized perpetual exchanges, supported by real transaction fees without relying on inflationary token incentives. However, this also brings risks – the price of HYPE is becoming increasingly tightly linked to the trading volume of a single exchange.

HYPE has a fixed total supply of 1 billion tokens, with over 70% allocated to the community and 97% of transaction fees used for token buybacks. The protocol has generated a cumulative $1.24 billion in transaction fees, with an annualized revenue of $800 million to $1 billion, placing it among the top fee producers in DeFi.

Buyback flywheels also have their vulnerabilities.

This relationship is bidirectional; as crypto activity cools down, buyback revenue also declines. Hyperliquid's quarterly buybacks have dropped from $316.8 million in Q3 2025 to $192.3 million in Q1 2026, a decrease of about 40% over two quarters. At the same time, more locked tokens will enter circulation, creating potential selling pressure that the Assistance Fund needs to absorb.

From Developer Sandbox to Trillions in Transactions

Hyperliquid's growth was not linear; it exploded as soon as it was released. In 2023, Yan launched Hyperliquid on his self-developed L1 platform. Early versions looked like a developer sandbox, but they offered sub-second finality, an on-chain order book, and a user experience close to Binance. Within a few months, daily trading volume exceeded $1 billion, and subsequently, monthly trading volume exceeded $10 billion.

By mid-2025, it will be directly competing with CEX giants.

By mid-2025, Hyperliquid's monthly trading volume reached $2.48 trillion, a scale comparable to Binance and Coinbase. It took two years to grow from 0 to 545,000 users. Jeff himself said:

"We don't have a marketing department; our community does a better job than all the CEXs' marketing departments combined."

By early 2026, the market capitalization level will be pushed to another level.

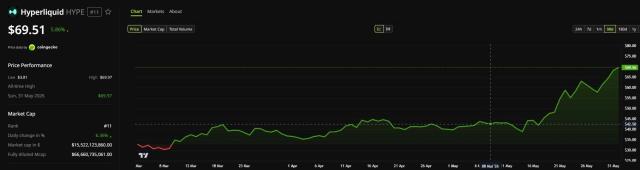

HYPE is one of the top ten crypto assets by market capitalization, hovering around $11 billion, and has been trading for less than two years. On May 15, 2026, Bitwise launched BHYP, the first natively staking-enabled Hyperliquid spot ETF in the United States.

On-chain growth comes not only from transactions. In early 2025, the platform launched HyperEVM, allowing developers to build financial applications directly on the Hyperliquid chain. The ecosystem expanded rapidly, with the CDP protocol Felix managing over $400 million in assets and the lending protocol HyperLend managing $380 million in assets.

Over the past 12 months, Hyperliquid's trading volume reached $1.8 trillion, accounting for more than 10% of the global perpetual contract volume and more than 70% of the total perpetual contract volume on DEXs. After its launch in 2023, its daily trading volume reached $1 billion within 100 days, and by mid-2025, its monthly trading volume reached $2.48 trillion, ranking alongside Binance and Coinbase. In two years, the platform has accumulated over 545,000 users from scratch.

Jeff Yan rarely speaks publicly, doesn't use social media, and has never received VC investment, yet he was still listed in CoinDesk Most Influential 2025.

His Hyperliquid platform processes approximately $10 billion in transactions daily, and DefiLlama shows that it reached $308 billion in October alone. The platform has over 570,000 users and its self-built blockchain offers speed and stability comparable to centralized platforms.

Fee revenue presents an interesting contrast to Ethereum. Hyperliquid once surpassed Ethereum in weekly protocol revenue, reaching $12.8 million and $11.5 million respectively; it holds approximately 70% of the perpetual contract market share; as of February 10, 2025, its daily trading volume reached $470 million, with a cumulative trading volume approaching $1 trillion; HYPE has increased by over 500% since its airdrop on November 29, 2024, with a TVL reaching $1.27 billion.

What is Hyperliquid (HYPE): A Beginner's Guide

A massive landslide and a test from the general (loyalty!).

If you only look at the positive side, Hyperliquid seems like a fairy tale. But two major account liquidations in March 2025 nearly sent it to the intensive care unit.

The first instance was a large ETH order. On March 12, 2025, one or more experienced traders discovered a vulnerability in ETH perpetual bonds. The attack occurred during a window of low market liquidity. They used $4.3 million USDC as collateral to open a $200 million notional position with 50x leverage (the platform's maximum leverage at the time, which was later reduced to 20x), pushing up the price of ETH on Hyperliquid by more than 3% relative to other exchanges.

HLP recorded a profit of $4 million at the time, but subsequently, due to the market's loss of confidence in Hyperliquid's risk management, HLP withdrew more than $80 million. Attackers exploited the platform's feature that allows withdrawals of unrealized profits to amplify the effect; mainstream CEXs such as Binance generally do not offer this feature.

Then, on March 26, the even more serious JELLY incident broke out.

In March 2025, Hyperliquid nearly suffered a $12 million loss when attackers exploited a vulnerability in the protocol's liquidation mechanism to artificially inflate the price of the JellyJelly token by 429%. The attackers established two long positions and one short position against JellyJelly, with the short position valued at $4.1 million, representing a significant portion of its $25 million market capitalization, while the two long positions offset each other.

Subsequently, the attackers manipulated the price of JELLY on multiple exchanges, causing it to surge by over 400% within an hour, resulting in significant unrealized losses on their own short positions. Following Hyperliquid's inheritance rules, HLP automatically took over the short position.

When losses reached $12 million, the validator quickly delisted the JELLY token and settled all positions at $0.0095 (the attacker's short price), while the listed price at the time was $0.50.

The fact that validator consensus was reached within two minutes exposes a high degree of centralization.

The attackers eventually withdrew $6.26 million of the $7.17 million deposited into the platform before the agreement froze their withdrawals.

The incident quickly sparked criticism within the industry.

Bitget CEO Gracy Chen called the move "immature, unethical, and unprofessional," and said that "Hyperliquid may be heading towards FTX 2.0." He believes that this treatment sets a dangerous precedent and describes Hyperliquid as "an offshore CEX without KYC/AML disguised as an innovative decentralized exchange, facilitating illicit funds and bad actors."

On-chain investigator ZachXBT pointed out that Hyperliquid seemed indifferent to North Korean hackers using stolen funds to open accounts on the platform, but took decisive action in the JELLY incident.

"When the Radiant hack and DPRK funds involved thousands of victims, there was nothing they could do; when a low-market-cap PVP meme coin went wrong, a small number of validators and a large proportion of staked tokens controlled by Hyperliquid rushed in to liquidate at arbitrary prices. True decentralization remains rare in this space."

Former BitMEX CEO Arthur Hayes also joined the criticism: "HYPE can't even handle JELLY, so stop pretending that Hyperliquid is decentralized."

There's another aspect that makes the incident even more intriguing.

After Hyperliquid was delisted, a larger player entered the market – Binance, the world's largest trading platform, saw an opportunity and announced the launch of JELLY futures, causing the spot price to surge by 560%.

At a time when Hyperliquid was teetering on the brink of collapse, Binance's listing of JELLY perpetual futures was interpreted by many as opportunistic profiteering. Both OKX and Binance have also listed JELLY futures.

This move was described as "suspicious" by Blockworks analyst Boccaccio. Although the exact motive is unknown, the fact that Hyperliquid was in trouble at the time made the incident "look like an attack on Hyperliquid."

Following the incident, the Hyperliquid team proactively addressed the issue and made a series of structural adjustments.

From then on, the proportion of Liquidator Vault in the overall HLP strategy was strictly limited to a small portion of the total vault value, and the frequency of reassessment was reduced; the OI cap formula was modified to directly consider the true market value of assets and order book depth to prevent the opening of excessively large positions in low-liquidity assets; validators will gain on-chain voting rights to vote on the delisting of assets that fall below key thresholds such as volatility, suspected manipulation, lack of trading volume, or market making.

a16z's money and CZ's shadow

As Hyperliquid grows in size, it's inevitable that a number of projects will try to "copy Hyperliquid"—that's an industry norm. The two most worthy competitors to discuss are Aster and Lighter.

Let's start with Aster. Its label is very clear. Aster is a rapidly growing DEX built on the BNB Smart Chain, positioned as a major competitor to Hyperliquid. Its daily trading volume has soared to the tens of billions of dollars range at times, occasionally surpassing Hyperliquid.

Its connection to Binance co-founder CZ has garnered significant market attention. Aster's momentum stems from its close relationship with CZ, who serves as an advisor; many in the industry directly refer to Aster as "Binance's DEX." It has launched tokenized stocks, allowing users to leverage up to 1000x, and plans to launch its own L1 platform.

This combination makes Aster one of the boldest experiments in DEX design to date.

Lighter took a different approach.

Novakovski, an early member of the Hyperliquid team, later left to found Lighter, which is backed by Founders Fund, Ribbit Capital, David Sacks' Craft Ventures, and a16z crypto.

The contrast between it and Hyperliquid is quite subtle—one represents "not having received VC funding," while the other represents "top-tier Silicon Valley VCs." Lighter, with its low latency, gas-efficient order book, and zk-rollup speed, has become a destination for institutions and smart money. Its standard account does not charge maker/taker fees, allowing retail users to trade across markets at zero cost, and its points system hints at future airdrops.

A "coup" occurred in September 2025.

The DeFi market experienced a sudden power shift. After launching its governance token, Aster accounted for nearly 70% of the global perpetual DEX trading volume, while Hyperliquid's share once fell to around 10%, causing a brief shift in the market balance.

The momentum didn't last long.

By January 2026, Hyperliquid will have regained its leading position, with weekly trading volume returning to around $40.7 billion, and competing platforms will struggle to maintain the previously surged activity. By March 2026, Hyperliquid will have a share of over 70% in perpetual DEX open interest.

The difference lies not primarily in speed, but in the quality of trading. Hyperliquid's open interest (OI) is approximately $9.57 billion, far ahead of the competition; its OI ratio is the healthiest in the sector, unlike Lighter, whose OI is artificially inflated for the purpose of boosting points. The $9.57 billion in OI indicates that this is genuinely committed capital that will not simply disappear once the reward period ends.

More incisive judgments also began to emerge.

The "points-for-airdrop" model is dying out as a sustainable growth strategy; the market in 2026 will no longer reward temporary TVLs, but rather technological moats and UI stickiness, two areas where Hyperliquid's L1 infrastructure remains ahead.

When Wall Street started to get involved

Hyperliquid's story entered the "financialization" phase in the second half of 2025. It no longer remained within the scope of DeFi protocols, but gradually connected with more mainstream entry points such as stocks, ETFs, and SPACs.

ETFs are the fastest to come under the scrutiny of compliance regulations.

Bitwise has submitted an updated S-1 to NYSE Arca for the Hyperliquid ETF (ticker symbol BHYP), with an annual management fee of 0.67%.

On May 15, 2026, Bitwise launched BHYP, the first natively collateralized spot Hyperliquid ETF in the United States.

The SPAC path is already halfway complete.

In October 2025, Hyperliquid Strategies, a SPAC entity that merged with Sonnet BioTherapeutics, filed its S-1 petition with the SEC, planning to raise $1 billion and list on Nasdaq. The entity eventually traded under the ticker symbol PURR, holding 12.6 million HYPE tokens and planning to generate returns for shareholders through staking.

Stablecoins and compliance are also weaving new narratives.

Hyperliquid's USDH is a MiCA-compliant, USD-backed stablecoin that channels 95% of its reserve interest into HYPE buybacks. This not only complies with EU electronic money token (EMT) requirements but also creates a sustainable cycle of "stablecoin yield → native token demand".

HIP-3 cut fees by 90%, pushing TVL to $2.15 billion, and working with licensed custodians like Anchorage Digital and Circle's CCTP V2 to address institutional compliance and asset mobility issues.

One noteworthy hedging action is supply reduction.

Starting from the end of 2025, approximately 23.8% of the HYPE supply will be gradually released over 24 months, potentially leading to selling pressure. Analysts warn that if pledging or utility demand does not grow proportionally, the buyback absorption capacity may be offset. In response, Hyperliquid has proposed a 45% supply burn plan, reducing FDV from $49 billion to $16 billion, bringing it closer to circulating supply.

At the organizational level, Yan announced a hiring spree at the end of October 2025, expanding the Hyperliquid Labs team from 11 to 14 people, an increase of nearly 30%. Even so, this size is still counterintuitively small compared to a "quasi-Nasdaq company" with an annual profit of $900 million.

Some gossip I stumbled upon while writing this article

The stories of the crypto world are always intertwined with gossip.

The Lighter exodus. Hyperliquid's most dramatic internal conflict occurred after team member Novkovski left. His Lighter project had investors including Founders Fund, Ribbit, Craft Ventures, and a16z crypto—virtually all the VCs Hyperliquid had publicly rejected. This combination of a departing partner and top-tier VCs became the most direct counterattack against Hyperliquid's "VC-free model."

The shadow of Binance looms large. The relationship between Hyperliquid and the Binance ecosystem has always been a potential narrative. Then there's Aster, a "Hyperliquid clone," which closely aligns with the stance of the crypto exchage Binance. Add to that the fact that Binance and OKX conveniently listed Jelly perpetual contracts during the Jelly short squeeze, and the general consensus is that "CEXs are trying to deliver a blow to DEXs." These actions have amplified the potential losses for Hyperliquid, with some users in the community even publicly calling for Binance to list the token to "deliver a fatal blow to Hyperliquid."

Lighter itself suffered a major setback. Its launch was also fraught with difficulties. After eight months of private testing, Lighter launched its public mainnet on October 1st, only to experience a massive outage nine days later during the market crash on October 10th. The team later admitted that the system couldn't handle the traffic and upgraded the database capacity. Traders who lost approximately $50 million due to the downtime were compensated with Lighter Points, which could be redeemed for future airdrops. As a consequence, Lighter experienced a typical "post-airdrop hangover" after the TGE on December 30th, with trading volume plummeting by nearly 70% from its peak.

Internal disputes have erupted within the Aster community. Recently, there have been frictions within the Aster community, with token holders complaining about not receiving rewards and some accusing the continued airdrop program of diluting token value. A bigger issue is that even with increased buybacks, the price continues to fall, raising questions about whether the team is selling the repurchased tokens through another wallet.

Justin Sun's contrarian strategy: While most people were selling off their Lighter airdrops, Justin Sun increased his holdings, exchanging approximately $33 million for about 13.25 million LIT, becoming one of the whale in the Lighter ecosystem.

Security anxiety. The Colossus report begins with the story of a 43-year-old man in Saint-Léger-sous-Cholet, western France, being abducted, beaten, bound, and dumped in a small town 30 miles away on a Friday dawn in January. Twelve hours later, in Verneuil-sur-Seine, a suburb of Paris, three armed men kicked down the door of their home, beat and bound the couple in front of their children, and ransacked their house. This was the 70th such attack globally in less than a year. Yan himself has reportedly become very vigilant about personal and travel safety. This is a generally underestimated atmosphere within the crypto community from 2024 to 2026.

My Questions

Is decentralization a means or an end?

Jeff Yan has publicly stated that he "will not sacrifice speed for superficial decentralization." If incremental decentralization requires a 5-10 year timeframe, will early users and investors be willing to accept it? Will the market continue to value a "quasi-centralized" protocol as a decentralized protocol?

Is Hyperliquid building an exchange or a financial system?

Jeff's answer was clearly the latter, but his actual product roadmap emphasizes "trading" far more than "financial infrastructure." HyperEVM is an important first step, but the lending protocols and stablecoins built on it have not yet undergone a full deleveraging cycle test. In the crypto industry, there's a vast distance between "looking like a financial system" and "acting like a financial system during a crisis," spanning the entire distance from bull market to bear market.

How much more benefit can James Wynn's celebration bring?

To some extent, Hyperliquid's community culture was defined by a trader who "bet $100 million." The tension in this culture lies in the fact that while it attracts the most extreme traders, it also fosters an atmosphere where "losing everything is glorious." When KOL liquidations become a daily occurrence, can the community's trading culture evolve from a "degen-fueled frenzy" into a more sustainable paradigm?

If CZ really does launch a dark pool perpetual contract DEX, where will the trading volume go?

Hyperliquid's most prized feature to date—all positions and all settlements are publicly displayed on-chain—is also the structural reason it has been targeted and exploited by MEVs. If an alternative product emerges that can both protect the privacy of large traders and maintain the efficiency of on-chain settlement, the narrative of "transparency above all else" will face a real challenge.

at last

Hyperliquid achieved a leap that few projects in the crypto industry can accomplish in three years: from an idea to an independent chain, a product that crushes all competitors in the field of perpetual contracts, the largest community airdrop in history, and a commercial entity that generates nearly $1 billion in annual profit—all done by an 11-person team that refused VC funding.

It has also accumulated enough controversy, attacks and criticisms to make "whether it will become FTX 2.0" an industry-wide debate topic.

However, a closer examination of these controversies reveals that Hyperliquid's transparency—from on-chain liquidation data to the real-time verifiable Assistance Fund balance—is precisely the structural barrier preventing it from collapsing like FTX. Every liquidation at Hyperliquid can be verified by anyone, and every buyback is recorded on-chain.

This most fundamental difference distinguishes a semi-transparent black box from a fully transparent system.

Jeff Yan said the following in an interview with Colossus:

"Money is really just a number. I'm not super materialistic. I don't actually care about money. For me, it's about doing something interesting and valuable to the world."

You can read this as hypocrisy, sincerity, or a kind of elitist narcissism.

But the fact over the past three years is that he did not take any VC money, he gave 31% of the tokens to users for free, and he allowed 97% of the platform's revenue to flow into token buybacks on the open market.

Hyperliquid's next three years will answer a more fundamental question:

Can a financial system built at the intersection of high-speed, centralized technology and decentralized ideals find a time-tested balance between efficiency and security?

If not, it will be a fascinating experiment.

If so, just as Steve Jobs reinvented the mobile phone, Hyperliquid is reinventing the stock exchange.

I'm Dax, a PM at an LLM company, a veteran Web3 investor, and a hackathon bounty hunter.

Welcome to follow my column and Twitter. I hope you are doing well.